This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

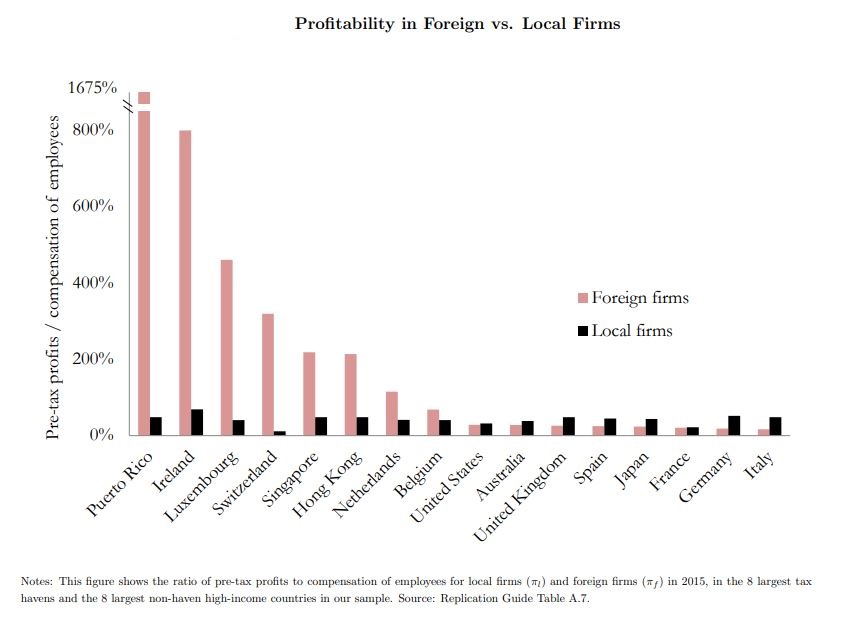

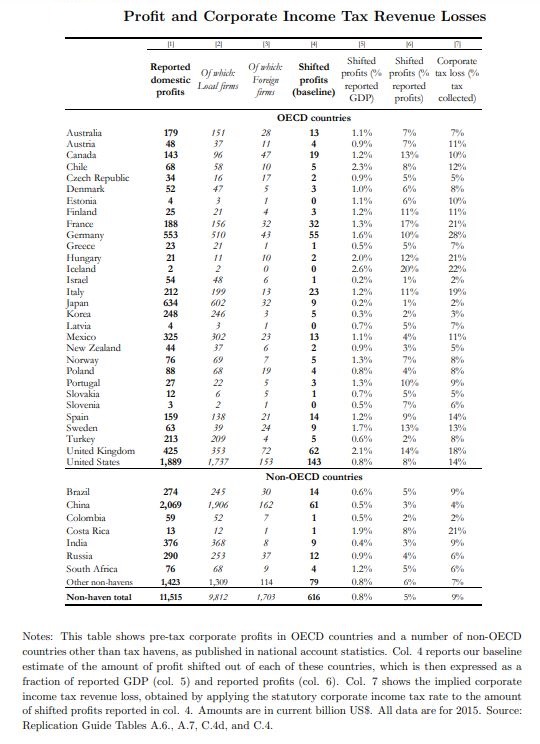

1) The missing profits of nations.

We hear a lot about profit shifting by multi-national corporations. Often this enables companies to effectively book revenue earned in one country in another, much lower tax jurisdiction. An example of this that I've written about features Visa and Mastercard, who are able to book their New Zealand revenues in Singapore, where they pay very low tax rates.

Now, a new paper, The missing profits of nations, estimates that 36% of multinational profits globally are shifted to tax havens.

The paper's by Thomas Tørsløv of Danmarks Nationalbank, Ludvig Wier of the Danish Ministry of Finance, and Gabriel Zucman of UC Berkeley and the National Bureau of Economic Research.

Since the beginning of the 2010s, the statistical institutes of most developed countries—including the major tax havens—have started releasing macroeconomic data known as foreign affiliates statistics. Following international guidelines, these data record the wages and profits of foreign firms, defined as firms more than 50%-owned by foreign shareholders (i.e., typically subsidiaries of foreign multinationals). These statistics greatly improve our ability to observe where multinational companies operate and book profits, in particular the amounts they book in tax havens.

Using these data, we propose a simple method to infer profit shifting by multinationals to low-tax countries. By combining foreign affiliates statistics with national accounts data (which cover all firms—foreign plus local—incorporated in a given country) we estimate the profitability of foreign vs. local firms within each tax haven. This exercise reveals that foreign firms are much more profitable than local firms in tax havens. Leveraging this differential profitability, we provide bounds for the amount of profits shifted by multinationals in each haven. Using new bilateral balance of payments data, we then re-allocate these shifted profits to the countries where the profits have been made, or where the multinationals’ parents are headquartered.

The specificity of our approach—its global and bilateral nature—sheds light on key aspects of globalization.

And;

Our main findings can be summarized as follows. In our preferred estimate we find that 36% of multinational profits—defined as profits made by multinationals outside of the country where their parent is located—were shifted to tax havens globally in 2015. We establish that U.S. multinationals shift comparatively more profits: in 2015, U.S. firms shifted more than half of their multinational profits, as opposed to about a quarter for other multinationals. The governments of high-tax European Union countries appear to be the prime losers of global profit shifting, with a reduction in domestic profit of about 20%, as opposed to 10% in the United States and 5% in developing countries.

The raw numbers are not insignificant.

Starting with absolute numbers, in our preferred estimates $143 billion in profit was shifted out of the United States in 2015 (23% of the global total), $216 billion was shifted out of the European Union (36% of the global total), $76 billion out of other OECD countries (12% of the total) and the rest (29%) from non-OECD countries. More than 70% of profit losses originate from high-income countries.

But never fear. Shareholders in the multinationals, surprise, surprise, are not losing out.

By our estimates, about half of the globally shifted profits accrue to the shareholders of U.S. multinationals (many of which, but not all, are Americans). Because equity ownership is concentrated (see e.g., Saez and Zucman, 2016), profit shifting reduces the effective tax rate of the wealthy, which may contribute to increasing inequality. A quantitative analysis of these redistributive effects across income and wealth groups would make it possible to make progress towards a full-fledged macro-distributional analysis of globalization. This raises major conceptual and empirical challenges for future research.

2) Will the RBA review probe 'one of the last taboos' in central banking?

Australia's new government has launched a wide-ranging review of the Reserve Bank of Australia. It comes at a time when the stimulatory actions of central banks during the Covid-19 pandemic are under scrutiny against the backdrop of soaring inflation.

ABC business reporter Gareth Hutchens suggests "one of the last taboos in central banking," their ability to create money, should be discussed in the review.

I have to say, based on the confusion, ignorance and misleading information around on this topic, including from our politicians, ex-politicians, media and pundits, this would be a useful discussion on this side of the Tasman too.

In New Zealand we've got the Reserve Bank's Funding for Lending Programme rumbling on, which has conjured up $12.66 billion for banks to date, and we also had the Large Scale Asset Purchase (LSAP) Programme. Through this LSAP, or quantitative easing (QE), the Reserve Bank bought $53.5 billion worth of NZ government and local government bonds on the secondary market from banks during 2020 and 2021.

Putting a bright official spotlight on these actions, explaining how they work, why they were undertaken, what they mean, and thoroughly questioning them, would be a useful public service.

Here's Hutchens (who goes on to delve into direct monetary financing):

In 2020, a younger generation of Australians saw for the first time how the federal government could conjure vast sums of money out of thin air.

Suddenly, in the first year of the pandemic, the government came up with hundreds of billions of dollars to subsidise the incomes of millions of households in the lockdowns.

Where did it come from?

The government "raised" the money by asking the Australian Office of Financial Management (AOFM) to sell bonds on its behalf, which led to an explosion in government debt.

But could the government have raised money a different way?

Why would a government that issues its own currency, and so has the power to create money to pay for things, want to fund its deficit spending with borrowed money?

It's a fascinating question.

And it wades into controversial territory that Reserve Bank governor Philip Lowe tried his best to avoid during the lockdowns.

Here is today's David Rowe cartoon. For more cartoons: https://t.co/lHSphNUJJW pic.twitter.com/DxWKBuJlHW

— Financial Review (@FinancialReview) July 20, 2022

3) Central Bank Digital Currencies & the threat to ticket clippers.

In an episode of our Of Interest podcast last month I spoke with Reserve Bank Director of Money and Cash Ian Woolford about central bank digital currencies (CBDCs).

CBDCs are a hot topic in international central banking circles and something we should be paying attention to.

Dong He, the Deputy Director of the Monetary and Capital Markets Department at the International Monetary Fund (IMF), tells an IMF podcast that CBDCs could allow ordinary citizens to have direct access to central bank money in a user-friendly way. Below is some of the transcript.

Dong He: At the moment, the central bank liabilities take two forms. One is currency- notes and coins, basically cash you and I hold in our wallets. I don't hold a lot of cash these days, but the other form of central bank money is reserves held by commercial banks. That's accessible only to commercial banks for the big institutions, not accessible to individuals. Now, central bank digital currency really provides a new form of central bank money. It has characteristics- it can be designed to have characteristics of both cash and reserves or deposits. Reserves are really deposits held by commercial banks with the central bank.

Dong He: Central bank digital currency is a new form of central bank money. It's digitalized in the sense that it can be held on your mobile phones. That allows us ordinary citizens to have direct access to the central bank money in a very user-friendly way. This is really a reflection of the very fast progress in digital technology, the proliferation of mobile devices. We can hold our cash in a app or in a wallet on our mobile phones. And that can be, as I said, a combination of different features. For smaller balances, it can be anonymous, it can be transferred peer to peer without going through the intermediaries that's the central bank itself. And it has features that can be integrated with the digital economy. If we look far into the future, the internet of things is going to be a very exciting development.

Dong He highlights how CBDCs could be a threat to intermediaries such as banks and other ticket clippers. This disintermediation threat is why banks, including local bank lobby group the New Zealand Banker's Association, are cautious about the CBDC concept. They could lose business and relevance.

Tara Iyer [the interviewer]: ... in terms of credit cards and debit cards, when we pay by cards in supermarkets or anywhere else, the money goes directly from a bank account, what is going to be so different about CBDCs and how would CBDCs differ from either using physical cash, one, and by using credit cards, two? How would they help ease the transactions? And we heard there are a lot of opaque things that go on behind the scenes, even though it might seem quite simple, if you could be, it'd really help us, if we would elaborate a bit more on that.

Dong He: Yeah. Very good question, Tara. One way to think about this is that of course, from the user point of view, when you and I pay with a credit card or debit card, if you want to buy a coffee in the cafeteria, you swipe your card and it's done, and it's very cheap from your point of view, but merchants who are providing, who are accepting the payments, they typically have to pay quite a high fee to their banks. It's usually 1.5% at least, sometimes as high as four or 5%. That goes to the bank. So, that's why some merchants actually don't accept the credit cards. And that's a reflection also of the very complicated clearing and settlement structure behind settling a credit card transaction, right? So, it's multilayered. Particularly when you go to visit a foreign country, when you are a tourist, the expenses add up to quite a bit.

Dong He: And if you want to make a cross border transfer, for some corridors involving lower income countries, you have to pay more than 10% of, let's say you want to send $200 back home to your parents, $20 of that would go to the service provider. Central bank digital currency certainly provide the potential that this cost will be drastically lowered to users. You don't feel the difference, but to a lot of merchants, that's a big thing. And for cross border payments, remittances for migrant workers, those will be much cheaper in the future. You certainly can envisage that.

Tara Iyer: I see. So, it's going to reduce transaction costs significantly for cross border payments. And in today's world, it's increasingly globalized, cross border payments play a huge role in the international financial system.

Dong He: Also of course, credit cards and debit cards, they have to be based on bank accounts. Exactly. You have to own a bank account. I should have started by saying that. One of the reasons why we think CBDC could help promote financial inclusion, because you can reach unbanked people. As you know, we have a lot of people in the world who don't have bank accounts and CBDC certainly provides possibility for them to access without only a bank account, with a much simpler onboarding processes as well.

In the Woolford interview he noted the Reserve Bank hasn't yet made a formal decision on whether it will launch a CBDC. Although conceptually disintermediation of banks by a CBDC could be possible, Woolford highlighted the Reserve Bank's focus on financial stability, suggesting private money will likely continue to dominate even if a CBDC is introduced.

Nonetheless he told the Of Interest podcast: "It is not our role to protect the interests of incumbents. We are interested in competition and innovation and I think it's fair to say we are of the view there has been a lack of competition and innovation in the New Zealand financial system, which is dominated by banks."

Watch this space.

4) China's Belt & Road Initiative: 'A mountain of non-performing loans.'

The well publicised economic woes in Sri Lanka saw the country defaulting on its sovereign debt in May, becoming the first Asia-Pacific country to do this in more than 20 years.

Sri Lanka is one of many so-called "developing" countries to borrow from China via the Belt and Road Initiative. The Financial Times has probed further, finding lots of problematic loans through the Belt and Road Initiative, which the FT describes as "a scheme that ranks not only as Beijing’s biggest foreign policy gambit since the founding of the People’s Republic in 1949, but also the largest transnational infrastructure programme ever undertaken by a single country."

This article's behind the FT's paywall, but well worth a read if you can access it.

In several countries in Asia, Africa and Latin America, the project risks metastasising into a series of debt crises. The issue is of crucial importance to the developing world because of the vast scale of the Belt and Road Initiative. Since the programme was first proposed in 2013 the value of China-led infrastructure projects and other transactions classified as “Belt and Road” in scores of developing countries had reached $838bn by the end of 2021, according to data collected by the American Enterprise Institute, a Washington-based think-tank.

But the loans that finance those projects are now turning bad in record numbers. According to data collected by Rhodium Group, a New York-based research group, the total value of loans from Chinese institutions that had to be renegotiated in 2020 and 2021 surged to $52bn. This was more than three times the $16bn of the previous two years.

This sharp deterioration brings the total of Chinese overseas loans to have come under renegotiation since 2001 to $118bn — or about 16 per cent of the total extended, Rhodium estimates.

China has had to manage a number of defaults on sensitive overseas loans in recent years but the cumulative impact of the multiple renegotiations that Beijing currently faces amount to the country’s first overseas debt crisis.

“This is the worst period of debt pressure since the start of the Belt and Road Initiative,” says Matthew Mingey, senior research analyst at Rhodium Group. “The Covid-19 pandemic took existing problems and supercharged them.”

Many of these loan renegotiations involve write offs, deferred payment schedules or a reduction of interest rates. But as increasing numbers of Belt and Road loans blow up, China has also found itself sucked in to providing “rescue” loans to some governments to prevent their debt distress from morphing into full-blown balance of payments crises.

A recent episode of Bloomberg's Odd Lots podcast was also interesting on the topic of China and sovereign debt. It featured Jay Newman, a long-time emerging markets debt specialist and a former portfolio manager for Elliott Management. Newman said when a sovereign owes money to a range of investors, China effectively takes a "super senior" position, and won't tell other investors how much it's owed. This, Newman implied, is frustrating for other investors and may hinder their efforts to work together. China doesn't play by the rules western investors expect.

5) The multi-billion dollar global illegal mining industry.

Picking up the story in a town in Ecuador named Zaruma, Bloomberg's Peter Millard and Stephan Kueffner tell a fascinating and disturbing tale of illegal mining around the world.

This is quite an opening:

Deep in the lush forests of southern Ecuador, in a cloud-covered village perched on the western edge of the Andes, a hole opened in the Earth one night late last year.

Small at first, it began to slowly expand and, over the course of an hour that evening, proceeded to swallow huge chunks of cobblestone road in the historic center of Zaruma. Panic spread among residents. They fled their homes—grand, early 19th century structures bathed in tropical pastels—and scurried to safety.

The sinkhole was caused by gold mining. According to Bloomberg, Zaruma "is loaded with bullion-rich rock, some of the best in the world." For more than 1,000 years people have apparently been digging it up.

There are so many tunnels and branches and offshoots that no one—not even the country’s top engineer on the job, Ivan Nunez—knows where they all go.

It 's far from a problem unique to just Ecuador.

Nunez, who’s been tasked with concocting a plan that will end the illegal mining and stabilize the ground under Zaruma, sounds daunted at times by the magnitude of the assignment. “It’s out of control,” he says. Across much of the developing world, authorities offer a similar lament. The value of gold and all sorts of other metals—copper, cobalt, silver, tungsten—is just too high for outlaw miners to pass up, especially after the rally that marked their ascent at the start of the century was supercharged by the easy-money policies that global central bankers have pursued throughout the pandemic.

Miners are wreaking havoc in Mali, Kenya and the Congo, stunting the size of harvests and funding rebel armies. And in South American countries all around Ecuador, they’re razing forests, spilling tons of mercury into Amazon rivers and destroying habitats. The continent’s vast mineral wealth coupled with its extensive organized crime network make it a growing hotbed of such activity. In Zaruma, gangs loosely affiliated with Mexican cartels control some of the mines.

All of this has caught the attention of international authorities.

In April, Interpol released a statement warning about the surge in illegal mining. Six years earlier, it had estimated the industry had reached about $48 billion globally. It hasn’t officially updated those figures yet but noted in its April release that the spike in gold prices and the growing presence of gangs, especially in Latin America, were accelerating the trend.

Precious metals

Select chart tabs

46 Comments

RE:2) Will the RBA review probe 'one of the last taboos' in central banking?

Why would a government that issues its own currency, and so has the power to create money to pay for things, want to fund its deficit spending with borrowed money?

Banks (including central banks) don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source.

"Banks (including central banks) don't take deposits and they never lend money."

So when funds are forwarded for a mortgage its not money but something else which we pay back but according to Audaxes is not money?

Step 1: You agree to a $500k loan from a bank

Step 2: The bank credits your bank account with $500k (this money is created literally out of thin air)

Step 3: The bank holds a loan document (asset) worth $500k (so the bank is all square)

Step 4: You make a lump sum payment of, say, $100k. The bank now holds a loan agreement worth $400k and $100k in cash (still all square)

Etc etc.

Money is just a construct of law and regulations - created at will by commercial banks and central banks.

This is how I imagine a year 7 student would describe banking.

Kind of correct though. Being able to explain things to 7 year olds means translating the complex into something meaningful and useful for understanding.

A) I said Year 7, not a 7 year old

B) He's completely wrong.

but otherwise......

I have designed several enterprise level systems to administer loans...! Tell me how I am wrong.

I really don't have the time. Banks do not create money out of thin air, that's Y7. Banks have a balance sheet like any other business, any loan has a risk weighting and the bank is obliged to hold capital against it. Most loans are funded by borrowing from investors (us and pension funds). It is not some mystical activity where someone with a wand says a spell.

Jeez. Have you learned anything about banking since a lazy teacher taught you economy 101 in Y10? This article seems designed for you...

If you don't understand how banks work, don't write about them.

Best that you read the Bank of England links that I posted. 'Money creation in the modern economy' and 'banks are not intermediaries of loanable funds - facts theory and evidence'.

The Reserve Bank also confirms that the BoE description of banking is correct.

Te Kooti,

Oh dear. This is embarrassing. Let me quote from an article from Real World Economics Review; "In the april edition of their monthly report, The Bundesbank has belatedly joined the BOE in explicitly stating that the treatment of banks and money creation in most textbooks is wrong: banks are not intermediaries, they create money ex-nihilo"(ps. that means from nothing).

I could go on at some length, but to quote you, i haven't got time. Go and do some homework.

If banks can create money from nothing then why do they fail? Why do we worry about them failing? Why do we need deposit insurance and bank guarantee's. Why don't we just get them to magic up the money for better health care.

Those articles are not saying what you think they are, that's embarassing.....

Bank lending creates both an asset and a liability for the bank on its balance sheet, if the bank looses on its asset side it is still responsible for the liability and will suffer a loss of its capital and other liquid assets which it holds against its lending.

A new loan creates a funding requirement for the lending bank = to the new loan less the marginal regulatory capital requirement. But what if the new loan was used to repay an exisiting loan, no money has been created.

What the BoE article is saying is that the cash from the new loan stays in the system and finds it's way back to the bank's as a deposit. This is true, but it's not money creation per se. A bank still has to fund the loan in the market (Net Stable Funding Ratio requirement), it cannot just do nothing and fund it with the Central Bank the next morning. What really grows the money supply is asset inflation.

I don't know anyone he thinks banks are only intermediaries like a credit union.

No. This is totally wrong. A new loan does not create a funding requitement. How it works operationally is that banks issues loans to anyone they think is credit worthy. They then check regularly to make sure their risk ratios etc are within their regulatory requirements. This is not contentious at all to be honest. The econ textbooks are literally clueless on banking.

.

The banks balance sheet is $1m asset and $1m liability, where has money been created? If Bob spends the $1m then the bank has to go to the market and borrow $1m

Nope. You're misunderstanding the settlement account system, and the fact that Bob's promise to pay is the bank's asset.

Te Kooti,

I'll try just once more. The following is taken from a lengthy article right here on interest.co.nz under Banking.

3. The banking and payment system, and how money and credit are created

In a modern economy, money can be created either by the central bank (the Reserve Bank, in New Zealand’s case) or by private sector institutions – in practice, mostly registered banks.3 Section 25 of the Reserve Bank of New Zealand Act 1989 gives the Reserve Bank the monopoly right to issue physical money (notes and coins), which enters public circulation through the private sector institutions to which it is issued.

A private sector institution can also create money by issuing claims on itself (ie, by accepting deposits) that may be transferred between, and are generally accepted by, members of the public as a means of payment. For that matter, any institution that can maintain the public’s confidence that its liabilities will be generally accepted as means of payment, can create money. Such an institution will, in practice, also be in the business of creating credit, which implies the issue of a greater value of claims on the institution than the value of Reserve-Bank-issued money the institution itself holds. In practice, by far the largest share of money – 80 percent or more, depending on the measure (discussed below) – is created by private sector institutions. For simplicity, in what follows, we use “bank” to refer to any institution that creates money or credit.

Could you please put your loan admin systems up here please? They may come in handy if they do what you say. The author of that article you linked with was roundly discreditted by a rational person who actually knew how money and credit work.

Reference please. I can debate this stuff all day. It's simple double entry book keeping, sadly misunderstood by most.

A) I said Year 7, not a 7 year old

B) He's completely wrong.

but otherwise...

Sorry, misread year 7. But my point remains.

Anyway, I don't understand why you're saying JF is 'completely wrong.' Not sure what I'm missing or what you're trying to express. Of course loan contracts are created out of 'thin air'. It's a euphemism and it basically means that loans are not created fully backed by cash deposits. You know that.

Confusing velocity of money with fractional reserve banking. https://medium.com/politicoid/fractional-reserve-banking-the-myth-of-cr…

Confusing velocity of money with fractional reserve banking

JF was not describing the 'velocity of money'. He was describing how a loan or credit is created by the banks.

Do you mean the fractional reserve banking that literally doesn't exist? Capital requirements and risk ratios etc through central bank regulation I recognise. But the rest is amateur hour, dodgy textbook nonsense.

The act of lending creates a corresponding deposit in the customers account. Before the loan took place nothing existed and so banks are not lending out money in that sense and when the loan is repaid nothing exists again.

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

https://www.bankofengland.co.uk/working-paper/2018/banks-are-not-interm…

What comes out of ATM machines..nothing?

Government currency which banks don't lend out, its part of their reserves. If a bank wants cash it has to swap it for some of its reserves which are also government currency.

FIAT aka Money

If a bank wants cash it has to swap it for some of its reserves which are also government currency.

What is cash then? At some stage we will get to money

Cash is government currency in a physical form that we can use. The majority of government currency takes the form of bank reserves which only the banks can use to make payments to each other. Cash is only a tiny part of the money that we use everyday, we mostly use bank created deposit money such as when we make electronic payments.

I was under the impression that the ANZ for example has to borrow $1 off someone for every dollar they lend out. Or they provide it out of previous profit on their interest that they have retained. Their profit, apart from fees, is borrowing at a lower rate than they lend out at. If I am wrong, I will just provide a 100% mortgage for the new owner of my house, and will draw up the documents mentioned above. Not a problem. I will take them to the owner of the new house I am buying, and they will do the same. No worries. Correct me if I am wrong please.

When I worked in the finance industry, every dollar we lent out had to be borrowed off someone else first.

Total new mortgage lending in NZ in June was $6 billion. That would require an average of $1200 extra savings/term deposits for every person in nz for the month to fully fund. That seems unlikely to me.

You need a banking licence to lend like a bank I believe.

This sounds more like a system of barter rather than money creation. Money is only a form of IOUs even government currency and anyone can issue an IOU but the problem is in getting another person to accept it. A bank only needs to have capital of 10% of its lending.

sit23,

Yes you are wrong. it doesn't work like that. I provided quotes from the Bundesbank-referencing the BOE-and our own RB. Banks are not just intermediaries taking money from people as deposits and lending it out. With every loan they create money which is destroyed when paid back.

You can try doing what you suggest but it won't work because they won't trust you.

by Audaxes | 14th Feb 20, 9:19am

Many buyers were sitting on the sidelines late last year in the expectation that mortgage interest rates could fall further this year but that now seems less likely, with recent rate movements being up and the Reserve Bank signalling no changes to the OCR this year and a possible increase next year. So buyers are deciding to get in now.

If falling interest rates are not the deciding factor for raising the animal spirits of property investors, I guess it must come down to banks' willingness to swap cash less IOUs with the public and hope for the best, given the consequent outcomes?

But from the point of view of the bank, it has acquired the security without giving up any cash; the counterpart, in its balance-sheet, is an increase in its liabilities. There is expansion, from its point of view, on each side of its balance-sheet. But from the point of view of the rest of the economy, the bank has ‘created’ money. This is not to be denied. Hicks (1989, 58)

We start with the idea of credit creation, specifically a swap of IOUs between a bank and myself involving a bank loan that is my IOU and a bank deposit that is the bank’s IOU. Nothing could be simpler, and yet the mind rebels, especially the well-trained economist’s mind, because this simple operation increases my purchasing power without decreasing anyone else’s. It seems like alchemy, or anyway a violation of some deep conservation law. Real productive resources are the same as they were before, and the swap doesn’t change that, does it?

Spending of the new purchasing power adds another layer of perplexity. If spending increases but real resources do not, then it seems logical that the increased spending must exhaust itself in higher prices—that is the intuitive appeal of the quantity theory of money. My purchasing power may increase, but everyone else’s decreases because their money balances buy less. From this point of view, the alchemy of banking seems like a kind of theft, something to be deplored in the name of economic science and if possible outlawed in the name of the general good. Link

Government borrowing is an interest rate mechanism, it drains reserves from the banking system which the governments spending has created. Too many reserves will cause the overnight cash rate which banks borrow from each other to fall towards zero.

Bonds and reserves are both liabilities of the government and are no different to each other in that respect. It is nonsensical to think of the government as borrowing back its own currency and then re spending it and it would make no difference to its overall liabilities or the amount of money in the system as bonds are just another form of currency.

https://www.levyinstitute.org/pubs/Wray_Understanding_Modern.pdf

Gareth's article got close to describing the last taboo. What he missed is that the sale of bonds does not raise the money for Govt to spend. Govt have to spend money first.

Operationally, it works like this:

- Govt maintain a balance in the Crown Settlement Account (memo note 1 here - currently $33bn)

- Govt pays me a chunky contract fee of, say, $1m into my Cooperative Bank Account

- My current account balance gets marked up by $1m (this is a liability for the Coop Bank and an asset for me)

- The Cooperative Bank's Settlement Account increases by $1m (this is an asset for the Coop Bank and a liability / debt for the Crown) (memo note 2 here). The Coop bank get paid interest on this balance (at OCR)

- If Govt now decided to sell a $1m bond - the Coop Bank could buy this bond and the purchase price would be deducted from their Settlement Account. Total Govt liability (debt) does not change - it just changes form

- If I got hit by a $100k tax bill, I would pay this tax back. My account would reduce by $100k, the Cooperative Bank Settlement Account would reduce by $100k, and the Crown Settlement Account would increase by $100k

It's just accounting.

Replay the same scenario with a house worth 1m. Buyer borrows 900k. House drops in value to 700 k... and the owner goes bankrupt and cant pay anything. Without the money being paid back it all looks a bit sick

RBA has a simple explanation - Box D: Recent Growth in the Money Supply and Deposits

Re corporate tax avoidance.

How about for a multinational company we simply add up the profits of all its entities throughout the world and local sales in each country. We would then simply claim that the companies profit attributable to our country is the total profit for the company proportioned on the basis of sales in our country. It may not be perfect but how can they complain given their lack of straight forward honesty.

China - led infrastructure in Asia, Africa and Latin America

"This sharp deterioration brings the total of Chinese overseas loans to have come under renegotiation since 2001 to $118bn — or about 16 per cent of the total extended..."

Is this lower than the $300 b owing by Evergrande.

I'm by no means an expert in central banks (something I suspect we are all going to agree on by the end of this comment) but I question if often they wouldn't be better off watching the flight instruments and charts instead of trying to peer through the clouds. Often by trying to be proactive they make major errors ("Path of least regrets", "Transitory inflation" etc.) whereas had they responded to the incoming data they would have been in a much better position to make decisions.

What I'm basically saying is behave less like prognosticators and more like scientists.

Uh, is the world gold price showing as $0 for anyone else?

FYI, this is getting fixed.

What exactly are the hidden questions about the Reserve Bank system? There are so many levels and maggot holes to go down.

As I understand it, we have inherited a fairly well functioning, if somewhat flawed, reserve banking system that is the current evolution, or degradation, depending on your point of view, of the system Sir Isaac Newton developed in the seventeenth century. This system allowed a dramatic rise in worldwide productivity and material wellbeing in the following centuries.

This system of Isaac's provided a means of measuring value against a fixed yardstick. It was very firmly aimed at preventing fraud by the state bureaucracy, whether for personal or tribal benefit.

This paralleled the development at that time of the system of representative parliamentary democracy and a constitutional monarchy. Here too, the emphasis was on constraining the power of the government machinery by forcing a budgeting process upon the spendthrifts that needed parliamentary approval.

The principal form of devastation, both materially and economically, was warfare. The French King, for example, encouraged by ambitious courtiers and civil servants, would decide to invade a neighbouring state because they were weak. Warfare, closely followed by famine and plague, regularly wiped out 30% of the populations of entire regions.

Lest you fall for the bureaucracies' favourite lie, Republics are generally just as bad, starting with Cromwell, effectively the President of the Republic of Britain, who happily slaughtered 30% of the population of Ireland. The mass murderers of the twentieth century; Mao, Stalin and Hitler; were effectively Presidents too.

The point is, the central bank system evolved as part of the system of representative democracy we inherited.

My sense is that this entire edifice is in danger of collapse. We are the third generation who gamble away the fortune built up by the two generations before us.

My problem, is the entire bunch of civil serpents and politicians seem totaly unaware of how destructive their actions are. They think they can add bits on and take bits off without consequence. They are so arrogant that they know best, that they think they can smash the system they inherited and build it back better.

I have been appalled at the state of New Zealand over the past few years and have not posted on this forum for several years. All our politicians and bureaucrats seem to be someone's useful idiot. A useful idiot being someone who happily acts against their own best interests, the phrase is attributed to Stalin, who was a master at using them. None of the dopey bastards represent me.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.