Adrian Orr, Governor of the Reserve Bank of New Zealand (RBNZ), says the central bank is effectively targeting core inflation and it is falling slower than the headline measure.

At the Waikato University’s annual economics forum, Orr spoke about the challenges of distinguishing between ‘transitory’ inflation and ‘persistent’ or ‘core’ inflation.

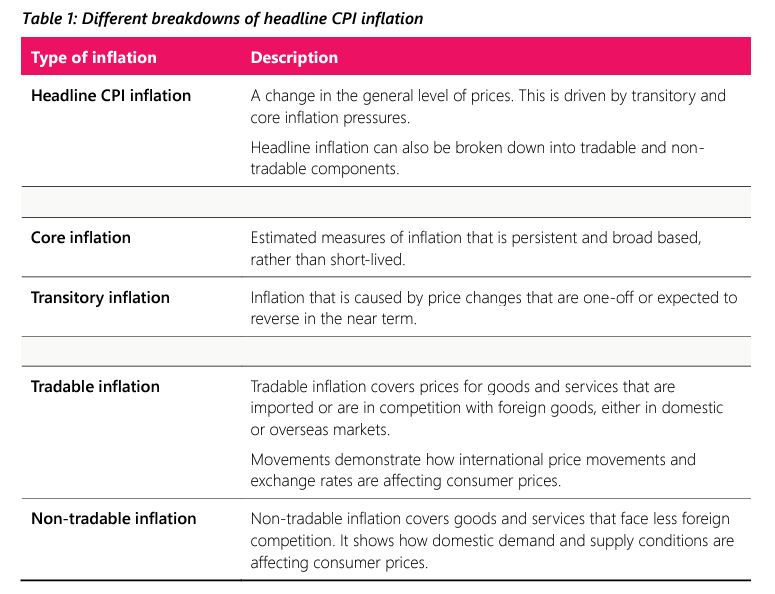

Transitory inflation is usually caused by unexpected relative price shocks which tend to dissipate over time. Core inflation is what is left in the system when the transitory shocks have worked their way out of the economy.

“So, we observe headline, but we are targeting, in a large sense, core inflation,” Orr said.

His speech notes phrased it differently: “Monetary policy leans against these more persistent inflationary pressures to ensure that headline inflation is expected to return to target over the medium term”.

The RBNZ Governor said measures of core inflation helped the Monetary Policy Committee identify how much of headline inflation was persistent and where pressure was coming from.

Headline inflation had fallen to 4.7% by the end of last year—from a peak of 7.3% in 2022—but core and non-tradable inflation have been much more stubborn.

Non-tradable inflation has fallen less than one percentage point from its peak of 6.8%, and other core inflation measures have also only just begun to react.

“While these declines in core inflation are moving us in the right direction, tackling the tail end of these persistent inflation pressures in the domestic economy remains key to achieving 2% inflation,” Orr said.

The monetary policy committee begins its February meeting next Monday and announces the result of its review on the 28th.

Orr said the proximity of this meeting meant he couldn’t talk about his views on how interest rates and other policies should be set.

However, he spoke several times about the Reserve Bank’s focus on core inflation and its intolerance of anything that threatened the return to the 2% target.

The central bank’s “appetite to look through” transitory price shocks was “significantly reduced” during a period of high inflation and inflation expectations.

“Central banks around the world have been trying to explain, ad nauseam, to the public that while inflation is coming down, we are not there yet, and the last few yards may be very difficult because we really need to re-anchor that 2% inflation expectation”.

Again, these lines were not specifically included in the speech notes.

Elsewhere in the speech, Orr spoke in support of the flexible inflation target focused on the 2% midpoint and reflected on how core inflation was underestimated during the pandemic.

In the speech Orr went into further detail on core inflation, describing it as representing pricing pressures likely to persist once temporary shocks have unwound.

"Core inflation is driven by things like capacity constraints – the balance between supply and demand – as well as labour market dynamics and wage inflation. They reflect general, rather than relative, price movement in the economy. Expectations of future inflation are also a key driver of core inflation," he said.

120 Comments

To raise or not raise interest rates.. That is the question.

HFL. Unleash the FOOP.

JH.. Embed FOOP

RBNZ'a move is both prudent and predictable.

While some may not like the taste of the medicine, it must be swallowed.

TTP

Can you take RBNZ medicine at the same time as record breaking immigration medicine? Asking for a friend.

Pour encourager les autres

Pour les encourager à faire quoi, ⁰Agnostium?

So you're suggesting the RBNZ has a social engineering agenda? ;-)

The beatings will continue until morale improves.

And after morale improves.

There'll be some normalcy to life

How does a "beating" improve morale?

Based on your personality, you should know that

Gee Yvil, its obviously tongue in cheek humour, much like your online name is a play on your actual name as well as your style

"Some of you may die but that's a price I'm willing to pay"

That sounds like David Seymours covid policy...

Brilliant , very funny , coffee everywhere , nearly fell off my stool ,, still chuckling

Yes those stab victims and those who died in car accidents who happened to have covid at the time definitely died of covid and would have been saved if the gov could have mandated that they had a few more vax

Let it go....

Et tu, Brute...

Politicians, in most cases, have and do, make decisions that directly or indirectly affect our lives and to such an extent it causes earlier death:

- funding Pharmac

- strategic funding of hospitals

- strategic funding of education

- law enforcement

- strategic funding of roads etc…

Na, just our smoke free (or lack of smoke free) policy.

Bang. HFL confirmed.

NZ housing market gets a taste of RBNZ Polonium poison Rate Hikes. Final Death rattle to take place.....

The market won't die, it will live on until the heat death of the universe. It just has to deal with an increasing number of disabilities, and learn to deal with incapacitation accordingly.

re ... "Bang. HFL confirmed."

What makes you say that? I couldn't find anything in the speech notes that said anything of the sort.

We’re already long past HFL. In 2022 the optimists were predicting cuts in H1 23. Spruiking brigade said they were happening in Q3 23… There may be small cuts late this year but new normal will be higher than most think - there will be no return to 2s or 3s.

As long as overall inflation keeps falling I think people will tolerate some unevenness returning to target. Where RBNZ might need to raise again is if tradable inflation (e.g. commodities) stop falling.

What's core inflation running at now?

Actually a jolly good question!

In the speech notes Orr says:

Measures of core inflation estimate this persistent inflation component by stripping out the transitory elements from headline inflation (Table 1). However, some estimates of core inflation are slow to evolve to new data and are prone to revision.

So whatever the number is, Orr is basically saying it's a guess, and may be too low or too high. (lol)

The table mentioned can be found here: https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/events/2024/0…. It also contains some interest graphs on 'core inflation'.

Figures 1 and 2 show the 'revised' core inflation numbers show that inflation actually took off earlier than the 'real time' reported number.

Note that Figure 3 shows the OCR rise in response to inflation.

I took this as a 'mea culpa' of sorts that the RBNZ was too slow in normalising the OCR. Quelle surprise!

Note that Figures 1 and 2 don't show past the point where the 'real time' and revised lines cross.

I've back checked this (very roughly) and - surprise, surprise - in the same way as their revised numbers show core inflation rising before the real time number, it also falls to target earlier too. Or put another way, the OCR is due for a trim about now. ;-)

Oh. Sorry. To answer your question, about 4%.

If you annualise the seasonally adjusted quarterly change for non-tradables (domestic inflation) between September and December just gone it was 5.4%.

Core inflation isn't non-tradeable inflation

Remember, higher rates have:

- Added billions of costs to businesses who are passing those costs through to prices. Businesses are paying $16bn a year in interest now (4% of GDP!)

- Benefited households in aggregate - debtors pay interest to banks, but savers are getting more interest back than debtors are paying (this is possible because businesses are massive net payers of interest)

- Pushed Govt deficit spending up (banks are getting $8M of interest per day on their settlement balances). Govt are now paying more interest into the economy than they receive, which is quite unusual in NZ.

The underpinning assumption Adrian is making above is that adding costs to businesses won't lead to price increases because the redistribution of money from spenders to savers will reduce the amount of money being spent in the economy. And, then prices will moderate, because...economics 101 etc.

However, what this misses is that prices can go up a lot without the total money being spent going up at all. People just buy less. That is exactly what the electronic card spending data shows us. The price of restaurant meals has gone up over 10% but spending on restaurant meals is the same as last year (down 10% in real terms). Restaurants can carry on selling meals at cost + margin - they just sell less of them, close on Mondays, lay of a few staff, etc.

What is happening under the hood here is that higher interest rates are pushing business costs up directly (credit as an input cost) and indirectly (e.g. workers pushing for salary increases to pay higher mortgage / rent / insurance, suppliers putting up prices to cover credit costs). However, lower demand is not pushing businesses to moderate their price increases because most don't have the margin to do that. So, they hold their margin and sell less.

Anyone who has managed a business will look at the above and say, 'yep'. Sadly, most central bank economists have never owned a business. They think the economy adheres to the dumb models in their textbooks.

This is the downside of using the model earlier to overinflate asset prices and devalue wages. Can't really say "oh well" and simply allow inflation to run away to protect all that debt.

Exactly.

Most people who want interest rates to come down werent complaining when they were low... the problem is that ocr is the only lever to be used and that cant change without excessive risk ( well run large businesses and economies know to expect it)

So if we have the ocr too low for too long we then must have it too high for too long.

How squirrels manage their nuts in relation to seasons is a great analogy for how businesses and people should manage their money/resources in relation to economic cycles.. those who did so are very relaxed now and simply getting on with the plan for the downward cycle and rate increase... it is what it is and wont change..

The conversation should be moving yo how to make money in the downturn

Yep, we've all collectively had some (very) good years, and now there'll be some less good years. Normal course of business.

Public has become so un-accustomed to a downward cycles this century.

An OCR increase should only add a one-off price increase, we should have already had those by now. If he were to decrease the OCR that would create demand, hence I don't see that happening until inflation is well under control.

Agreed.

It's not a one off increase if it is significant enough to kick off feedback loops - like:

- higher interest rates increase business costs

- higher business costs push on prices...

- higher prices and higher housing costs push on wages...

- higher wages and business-to-business prices push on business costs...

- back to number 2 until the shock dissipates (unless of course some fool in Wellington increases rates again, or we get an imported price shock)

Concur.

The RBNZ could cut the OCR to a still contractionary 5.0% and save a considerable amount of money while sucking oxygen from those pretending price increases are due to 'increased costs'.

Some good points raised here. Another data set to look at is composition of the tax take. The trend recently is a lower corporate tax take but a higher wage tax take. That suggests businesses are sacrificing profit to meet higher wage costs. If they continue to do that, the RB will be vindicated in their decision to hold rates and will be encouraged to continue, forcing employees to keep their hands out for further increases.

Then we have a catch 22 of higher wages and a stubborn RB. Meanwhile businesses are caught in the middle with ever shrinking margins.

I'm looking forward to the next release of tax revenue data to see if the trend is continuing.

Yay! Inflation word soup. Now we have ...

- headline inflation

- tradeable inflation

- non-tradeable inflation

- ‘transitory’ inflation

- ‘persistent’ inflation

- ‘core’ inflation

And can we measure any them well? Um, no.

Do we get up to date data? Um, no.

Is that data accurate? Um, no. It get's revised al the time.

But let's put the focus 'core' inflation. Why? Because economists have seen through the non-tradable inflation nonsense. (BTW - non-tradeable inflation will fall far faster than the RBNZ is projecting. Sticky it will not be.)

At an old work place, when EBITDA was a shocker, the bulk of the exec commentary would focus on how good 'Normalised' EBITDA was LOL.

It makes it easier to get the fat bonus if you 're-phrase' it...the C-suite rarely loses.

Agreed. 'Normalised' EBITDA became a much overused term. When it was actually justified, good buying could be had from a bad 'headline' EBITDA (and FBU take note - and once all the bad news was actually out and fully recognised.)

2% inflation is history! It isn't coming back! The inflation target would be 3% to 5%. That is without massaging the figures. With no oil Refinery, NZs fuel costs are exposed to global market prices and the global cost of finance. Diesel goes up, everything goes up.

J Powell recently said,"Higher. Longer."

We buy all our refined oils in now vs buying in crude and refining it less efficiently ourselves. Not sure how having a refinery would help us.

Or we could set up a local price stabilization mechanism for local fuel prices.

The USA has a 'Strategic Reserve' that warehouses millions of barrels. (Not that they need it nowadays.)

NZ could use a far cheaper option by simply adjusting the petrol excise duty to effect price stabilization. I.e. collect a bit more when prices are normal and hand it back when we get oil shocks. Golly! Sounds like insurance, right? And when kitty is large enough, they could hand the money to the NZ Super Fund to invest. Golly1 It sounds exactly like insurance.

As there are no profits to be made, people really can't really complain about this.

You can, however, expect profit driven businesses to squeal quite loudly about this as it takes away one way that they can justify price increases (that they never fully reduce after the oil shock), i.e. add to inflation. They'll claim such market intervention contravenes the rules of the 'free market'. So does insurance do this as well? No. It does not.

Most people don't know this, but oil prices are fairly constant in real terms over the medium to long term, thus the risk of such a price stabilization mechanism are low.

Can you see why I go on and on about inflation being something the government could do a lot more to help with rather than leaving it all up to the RBNZ? We have useless politicians. And have done for many years.

Great comment - diesel and petrol price stabilisation using flexible excise (and / or ETS) is so obvious it hurts. We even have the price monitoring regime all set-up ready to go.

Wouldn't this just encourage politicians to drop the excise tax in the 6-12 months before each election, then ramp it up afterward, sorta what Labour did with excise and road user charges? Seems like this would create a few new gov jobs to fiddle around and not actually achieve anything that helps anyone in the long term?

The price 'smoothing' would done by an organization separate to government. Much like how the RBNZ functions.

We should never accept anything like this if our woeful politicians have anything to do with it.

Setting the tone for a rate hike!!!

Did you read the speech notes? I couldn't find anything to suggest that was their thinking.

https://www.rbnz.govt.nz/-/media/project/sites/rbnz/files/events/2024/0…

You're expecting them to explicitly state ie?

So where does your original statement come from? You mentioned 'tone'.

Where did the 'tone' you mention come from?

No. Wait! Surely you didn't just make it up? ;-)

It's abundantly clear that you're not really interested in parsing this, but rather just cherry picking the bits that are closest to confirming your well established views. It's not interesting or informative.

Hahah that could be said about you.

"All measures of core inflation have also fallen over 2023. While these declines in core inflation are moving us in the right direction, tackling the tail end of these persistent inflation pressures in the domestic economy remains key to achieving 2 percent inflation"

"While inflation can be volatile month to month, monetary policy influences inflation with a lag. Our most recent estimates suggest it takes about 18 months to 2 years for the peak effects of monetary policy to flow through to inflation"

Neither of those quotes are really setting the tone for a rate hike

Agreed.

It is useful to look back at the length of 'peak OCR' durations.

Using another of interest.co.nz's excellent graphs here: https://www.interest.co.nz/charts/interest-rates/ocr

- July 2014 - 46 weeks

- July 2010 - 32 weeks

- July 2008 - 51 weeks and 6 days (when central bankers imploded the global economy!)

- July 2002 - 42 weeks and 1 day

- May 2000 - 43 weeks

And we've now had 'peak OCR' for 38 weeks.

However, it's been longer as the RBNZ signaled they were quite happy to create to create a recession when they started the fastest and biggest rate rise in our history back in October 21. ... A full 123 weeks ago! Yes. Over two years ago. (Note that retail banks immediately hiked rates at the outset way beyond what the OCR was.)

By the 28th Feb it'll be 40 weeks.

And by the 10th April it'll be 46 weeks.

And by the 22nd May it'll be 52 weeks. The longest ever! If their intent is to cripple NZ Inc for years to come there are going about in the right way.

A far, far better approach is to start easing now. But do it ... s l o w l y.

Maybe 0.25 in Feb. Skip April. And another 0.25 May. (Although by May I expect, if they follow that timeline, NZ Inc. will be demanding 0.5 as even an OCR at 5% is seriously contractionary and will cost a fortune.)

I am sure they know some people are hurting. The problem is the second they stop talking tough and start to loosen things the economy will go straight into fomo again.. everyone readying for growth vs our 'now' positon

But they cant have growth til unemployment actually goes down, immigration slows and inflation drops . Right now everyone is in a holding pattern praying it all goes back to how it was.. hanging onto staff, keeping businesses running on leas hours etc.

I still reckon they may hike it and give a talk about more rises to try to get businesses and people to actually change habits, close down if needes, let employees go asap. . So they can get into a position where lowering in a few months is possible .

Globally Uk has entered recession now, japan is in recession i think... we probably have to take quite a bit more of a pounding before green shoots are allowed

I find it hard to see how the economy will go back into FOMO mode if we drop the OCR to 5%.

Concur. And let's not forget it'll be yonks before retail banks pass 0.5% on. (Rocket & Feather pricing). There's also a remote possibility that wholesale markets disagree and rates stay high in spite of the OCR for a very short period.

Say you are a business - and i know 2-3 large ones in this situation.... revenue and profits are down and some units are working at a loss.. high paid consultants dont have sufficient work to do and are idle.

HOWEVER - if they get rid of those consultants now and the market starts to come back they fear the competitors will snag their ex- skilled staff and their customers, and they wont have resources to deliver a growing number of projects,

so - they wait and pray the budget brings work and the ocr changes sooner than expected. so for now nothing has actually chnged and as soon as money starts to free up... people will spend and hire.

I suspect MANY businesses are in that mode. people still have money to spend and IF the ocr starts to drop then the businesses will see it as a sign of change and stock with their current plan.

What the economy needs is the certainty that the market ISNT coming back as it was and businesses need to restructure accordingly.. prices, staff.. everything. when job losses start to mount and business profits take a tumble THEN the economy will start to align and the the ocr can drop.

Hense hold the line untill Dti arrives. This will stop people borrowing way to much to spechlat on gains. Perhaps a lower dti for second house would be good?

re ... "But they cant have growth til unemployment actually goes down, immigration slows and inflation drops."

And yet the US economy has falling inflation with growth while employment remains robust and immigration continues as always. Weird huh?

And unless someone has changed the RBNZ's remit again - their only consideration is inflation within range. Increasing unemployment from where it is currently, which appears to already be in the neutral zone, isn't necessary.

Whilst increasing unemployment isnt in their direct remit.

... but unless they do that the as soon as they drop the ocr businesses will immediately start to hire and try to retain staff. As their is no pool to hire from (without increased unempoyment) that means immediate wage growth and spend starts and demand spikes. Inflation continues.

Tis the same issue as housing. If immigration continues and wage growth returns.. with a housing shortage then prices will rise.. people feel richer and spend.. demand spikes. Inflation continues.

To quell inflation relies on breaking the cycles that drove it.

To break a wage/price spiral (if that is what is actually driving inflation) then it is enough to bring employment markets back into equilibrium, i.e. where employers need not pay higher to get the same work performed. If unemployment results by going past that equilibrium then it's being pushed too far.

Are you saying that you want unemployment to rise so far that there are so many unemployed that workers can be found that will do the same work for even less pay? If so, and employers actually pass these savings on in lower prices, then they'd have a deflationary effect. But don't worry, employers seldom pass on lower labor costs. They usually pocket them as larger profits.

The latest unemployment reports from Stats NZ have graphs on the LCI (Labour Cost Index) that split public and private wage costs. The private LCI has been falling for almost a year and is almost back to neutral. The public LCI will likewise be back to neutral soon as the NACTF start culling and the pool of public servants increases dramatically. My view is we're back into equilibrium. Thus further rises in unemployment would be a fail on the part of the RBNZ.

re ... "Tis the same issue as housing."

It is indeed. It is about supply. The more dwellings we create, the greater the supply, and house price rises will moderate to the rate of inflation. The problem is though, the high OCR is causing a collapse in the creation of new dwellings. (But if you're a house owner, or owner of multiple houses, I guess you'd be happy with that as house prices will indeed go up. Me, who is more concerned with the wellbeing of NZ Inc., isn't happy with this outcome at all. )

re ... "If immigration continues and wage growth returns."

Um. Why would that happen? We've just seen that the recent influx of immigrants (plus a contracting NZ economy) has in fact stopped wage rises in their tracks.

re ... "with a housing shortage then prices will rise"

Yup. Because the high OCR has the effect of stopping the building industry in its track.

Read between the lines...

Could you point out the lines you're referring to, please.

Fair enough, insisting on lowering inflation, but it will come at a price of deeper recession and higher unemployment.

It will create the lesser of two evils.

Agreed, but I can see Yvil cringing

Possibly JJ, time will tell.

Really? Why do you say that?

Please reference these two facts in your reply. 1) inflation is already heading down and tradeable inflation will (re)turn to deflation. 2) Even at 5% the OCR is still contracting the economy.

The lesser of two Yvils

Since I can't give you a smiley face, have an uptick HM.

Whilst we're humouring on each other's names. Have you been visiting a Dunedin supermarket recently house mouse.?

Yummy cheese they stock there

and the delicatessen section!

but that is what the government wants why else take away a secondary focus on employment.

the whole point is to lower wage inflation, that is best for businesses that is why ACT have forced through a whole range of repels to lower wages

I think you're confusing the Government and the Reserve Bank. The Government has nothing to do with setting the OCR or with the article above, that's the RBNZ's job.

No - The government changed the RBNZ’s mandate which impacts OCR settings

✅ Nice one Mouse.

Indeed. But by how much? From Orr's speech notes:

This primacy of the inflation target helps to anchor inflation expectations. Well-anchored inflation expectations are particularly important to an economy facing frequent or significant shocks that impact on inflation. If households and businesses expect inflation to return to the 2 percent midpoint, price and wage increases are more likely to be set around 2 percent, helping ensure that transitory shocks do not lead to second-round effects and more persistent inflation.

Our mandated Remit Review did not explore whether the objective to support MSE should be removed. This is a legislative matter for Parliament to determine, not the Reserve Bank. However, the recent change to remove supporting MSE as a primary objective aligns with the general push towards a simpler and clearer Remit that emphasises the primacy of the inflation target.7

While the removal of the MSE objective does provide some benefits in clarifying the MPC’s priorities, it does not mean significant change to the MPC’s task. The labour market is a key driver of inflation for any economy. The supply of labour and worker skill sets are critical to determining the productive capacity of the economy – how fast the economy can grow without generating inflation.

I smell a rate hike

I had ruled that out, but it is getting a bit whiffy.

I taste a rate hike 😁

ABSURD

The RBNZ has no control over non-tradeable inflation.

a) e.g. local government proposed property rates increases of +15%

b) The RBNZ also has stuff all control over monopolies and oligopolies raising prices as they are effectively untradeable inflation as well.

c) The RBNZ also has no control over the very high net immigration rate which is driving up rents (in CPI), new building costs (in CPI) and house prices (not in CPI but should be as a house is the main consumer product).

So the RBNZ has to overtighten on tradeable inflation to get average inflation back down to the target band & push the unemployment rate even higher screwing over the average New Zealander who gets thrown on the scrap heap.

This is simple insanity and does nothing to improve NZ's productivity.

The Government needs to get its A into G and legislate to:

a) force local government to restrict its property rate rises to the target inflation band as local government is an arm of government and has a responsibility to help meet the inflation target band. (NZ is now a poor country and cant afford the service levels being provided)

b) break up the major monopolies and oligopolies so that they become price sensitive and dont simply jack up prices to the shareholders benefit.

c) set a sustainable population strategy that seeks to maximise wellbeing (economic + social + environment) per capita rather than dumping additional inflation into NZ

d) overhaul the tax system so that it is focused on the productive use of capital (not lazy tax free capital gains in the property market) further driving up inflation

No one was complaining when rates were artificially low for a decade due to imported (tradeable) deflation.

a) I doubt property rate changes have ever been below the average inflation or tradeable inflation rate

b) If they were then its simply a reflection of local government failing to fund depreciation properly - a reflection of the 3 waters funding issues we currently face.

I was complaining.

The fake extra low interest rates blew asset prices sky high.

This is the reason average house prices should have been kept in the CPI (houses are the biggest consumer purchase).

Interest rates went much lower than they would have had house prices remained int he CPI.

The same is true now. With interest rate increases house prices are slowing/reducing in some areas. This would reduce the CPI and need for such high interest rates.

We have simply made a sword for our own back following the US and removing average house prices from the CPI.

Nice narrative. Echoed frequently. But could it be wrong? Consider the following ...

Between 2016 and RBNZ inspired covid madness house prices flatlined in Auckland (see REINZ stats). According to your narrative, they should have increased. But they didn't. Why? The best answer I can find is that Auckland's Unitary Plan of 2016 allowed for a massive increase in dwelling supply. Or put another way, a massive and artificial supply constraint had been removed. Likewise, Christchurch prices also rose at a sub-par rate once rebuilding got up to speed circa 2014 until RBNZ inspired covid madness. Graphs here: https://www.interest.co.nz/charts/real-estate/median-price-reinz

There are plenty of studies confirming supply is a major problem in cities all over the world and all studies identify restrictions placed upon what can be built, and where, by Councils. (Council's get elected by property owners and most property owners see nothing wrong with dwelling prices rising faster than inflation.)

With regards the CPI ... I'll say it again. The only organisation that should be using the CPI is the RBNZ. It is specifically for their purposes as it intentionally strips out certain costs that are affected by RBNZ actions. It is a massive con-job pulled by right leaning politicians that it is used for anything else as it does NOT reflect the cost of living correctly.

Tying benefits to the CPI - or any other inflation adjusted measure - is nonsense. I'd love to see what those on super in NZ would say if it was suggested their entitlements were tied to the CPI. The howls of outrage would be deafening.

Eh, the aspiring First Home Buyers sitting on the sidelines because house prices were rising faster than they could accumulate a deposit were probably complaining?

"a) e.g. local government proposed property rates increases of +15%"

Clutha District Council is proposing a 95% increase in Rates over 3 years, tip of the iceberg stuff I'm sure.

Kiwi - I’m afraid big local government rate increases are likely to be the reality for most parts of NZ due to a lack of investment in infrastructure going back many decades (ironically caused by pressure to minimise rates increases). Many Councils are now faced with a pressing need to deal with aging infrastructure. For example, sewerage in the streets and massive water leaks in Wellington. High net immigration into NZ also requires investment in new infrastructure in areas that are experiencing growth. Councils are also needing to spend more to make existing and new infrastructure more resilient against our future of more extreme weather events.

Those clamoring for an increase in the OCR should take note of these paragraphs from the speech notes:

These realties make achieving 2 percent inflation with precision today or on any specific date effectively impossible. Attempting to do so would create large swings in interest rates, output, and employment in response to temporary fluctuations in inflation. And even then, central banks would fail.

Instead, monetary policy should be set such that future inflation can be reasonably expected to reach 2 percent over the medium term. This allows for a more considered response to noisy data, with the focus on the balance between supply and demand and core inflation pressures.

A credible, forward-looking, and flexible approach to inflation targeting is the best contribution monetary policy can make to long-term economic prosperity, while avoiding excessive economic volatility.

While a medium-term focus does not prescribe a specific ‘time-to-target’, we always aim to get inflation back to the 2 percent midpoint in reasonable time to mitigate the risks from inflation expectations becoming unanchored.

An OCR at 5.5% is already forcing a contraction in NZ's economy. There is no need for it to go higher.

In fact, if cool heads prevail, the OCR at 5.0% would still be forcing contraction. But not only would it help those younger people with larger mortgages, force the rentier class to reconsider rent increases, it would also save NZ Inc. the considerable sums of money that is needed to hold the OCR high.

If the RBNZ really cares about our 'long-term economic prosperity" (as they claim!) the time for a cut is now.

I tend to agree with what you are saying, but if they drop the OCR to 5% at the next meeting, the NZD will likely drop significantly, and that will certainly give inflation a boost?

A 0.5% drop at the next meeting is extremely unlikely and, yes, it would definitely freak out the FX markets (amongst others). Central banking policy should avoid big changes except in exceptional circumstance. It makes planning exceptionally difficult when they're behaving erratically.

Woah woah woah. The 'rentier class', if they were smart, will have saved their money. And are now earning interest from it. So they don't need OCR cuts.

At the moment, property owners pay the renters (savers) via interest rates. Which is the opposite of what you probably think, that owning a home makes you wealthy. So why would we want OCR cuts?

I like how they refer to inflation as if it's something they didn't themselves create during their COVID response....

Guess we're still going to pay for their mistakes for a while longer....

Probably need a commission into it?

Councils, central govt, food retailers, wage slaves take note.

Orr has a problem in that his credibility is shot. He should be fired

You can jawbone inflation down but only if people believe you - raising rates is only a tiny part of the impact the biggest is emotional

and despite the noise from the retailers the people paying the price in NZ are the primary producers

I just had a quick look at reported annual cpi since he started.

2018, 19, 20 every quarter report of annual cpi was within target range.

2021 he had 1 quarter in range. Since then every quarter report has been above target.

Can we fire this guy? He made the problem by ignoring economic reality.

Difficult, Labour re-appointed Orr in 2023, for another 5 years.

Is that an iron-clad contract? Pay him out and move on. Cheaper than canceling the light-rail

Labour did so while breaking Paliamentary convention & previous precedent by not consulting & confirming with National.

All part of their losers poison pill

Talking of losers.

The Bolger government caused the leaky home crisis by allowing untreated timber. The Key government destroyed our roads when they increase the axle weight limit for trucks and this lot have so far destroyed our conversion to locally powered and non polluting EV's, killed Aucklands public transport and will probably cause another Wahine disaster.

Clutching at straw men...

Apples...Oranges

man

Key destroyed NZ with the failure of the health and safety law reform bill. This put small business out of business to the benefit of big business and traffic cone deployers.

Yeah, but you know, the whole world did that. All the whingeing and moaning about Adrian. Come on, get real. He’s on track. Bit of pain for some along the way but that’s life. Harden up.

Yep. Suck it up specucake.

Our goal posts are just a couple of school bags chucked on the ground. We can move them whenever we like. As long as it benefits our team and makes it harder for the other team.

How about we agree to use M2 money supply as the rate of inflation? Oh, wait, we don't get M2 statistics anymore.

M2 on its own doesn't really tell you much. It needs to be evaluated alongside other factors affecting inflation and what's happening in the real economy. Growth, or contraction, of M2 is completely normal and of itself tells you little. (Those who rant on about fiat money and how great crypto currencies are will have a different story to tell.)

Imports cost rising 25% due to freight costs and insuring that plus oil price rising

High interest rates draining mortgage and gov debtors will not reduce this cost. Meanwhile tourism income is 20% down on 2019 and China is in deflation funk

Recession inevitable

Shocks will not go away

World has changed. But the stupid finance models continue their masochistic policy

As inflation falls the OCR doesn’t

So real rate is going up while this applies

Tightening not cutting

Suicidal

It’s going up twice. Just read between the lines.

govt changes rbnz to sole inflation targeting.

Orr comes up with this commentary saying he’s serious about inflation..

If it was going to be the same, why say anything at all… after all if this was the top, he’d be chilling quietly till November. Job done right, all going down from here.

yea rite..

How long do we have to pay for the mistakes of the Reserve Bank?

Their job is to control inflation but they actually created it with artifically low interest rates and carrying on the funding for lending programme right up to Dec 2022 which was 18 months longer than Aus who realised free money to the banks was actually causing inflation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.