The At Wharf Gate (AWG) prices for export logs in June increased an average of $5 per JASm3 from May prices. The sale prices for New Zealand logs in China are now at record levels.

The global shortage of logs and sawn timber is becoming more evident by the day.

The PF Olsen Log Price Index increased $6 to a record $138 in June. The index is currently $18 above the two-year average, and $14 above the three and five-year averages.

Domestic Log Market

Log Supply and Pricing

Early indications from Quarter3 price negotiations are increases in log prices, particularly in structural logs. Immediate log supply is fine, but mills in some regions express concern over longer term supply if forests are being overcut or cut down early to take advantage of high export log prices.

Sawn Timber Markets

Despite the risk of repetition in this report the demand for wood products in New Zealand remains very strong. Wood product manufacturers in New Zealand are enjoying the strong demand as they can sell more product domestically and avoid excessive ocean freight costs to export markets. The mills that were exporting clear sawntimber to the US and Europe prior to Covid-19 have continued to supply these solid markets.

Global shortage of World Products

You do not have to look too closely to notice the extent of the word-wide shortage of wood products. Just a few of the recent headlines are noted below.

- More than 90% of US homebuilders report a shortage of timber.

- Turkey has started to limit export of some timber products.

- Production of about half of Germany’s furniture manufacturers is restricted due to material shortages. There is a particularly tense supply situation for chipboard, MDF and HDF boards.

- Prices for wood products in France are up 50% since the start of the year as the industry is struggling with a new law that requires half of the materials used to construct public buildings to be wood or other natural substances. The law is part of the country's drive to become carbon neutral by 2050.

- Sawn timber prices have doubled in the Netherlands in recent months.

- Lumber futures in Japan topped US$1,700 for the first time in history and lumber prices are about three time higher than what they were a year ago.

It seems New Zealand users of wood products have got off lightly so far.

Export Log Market

China

The price for A grade logs is now in the mid 190’s range. These are unprecedented price levels, and while log buyers are grumbling, the markets are adapting to the higher price levels.

Softwood log inventory has stabilised at just over 4m m3 and while daily port off-take has dropped slightly it is still around 60-70k m3 per day.

The Caixin China Manufacturing Index hit an unexpected five month high of 52 in May. The index was 51.9 in April and market consensus was for a drop in May. New orders rose the most since December 2020 and export order growth was at a six-month high. Rapidly rising commodity prices have started to distort the market as some companies begin to hoard goods, while others suffer raw material shortages. This is evident in the log market.

India

Many states in India are relaxing lockdowns and commentators are optimistic normal activity will resume by August. If there was a return to normalcy in August, then there will likely be a log shortage. Liner services are not supplying containers to India citing Covid-19 and port congestion in Singapore and Colombo. Current log supply has reduced to two ships from Uruguay and one from Australia per month. Some Uruguay suppliers have also agreed longer term supply deals to China.

Due to a shortage of sawn timber the prices have increased to INR 581 per CFT in Gandhidham and INR 625-650 per CFT in Tuticorin.

Exchange rates

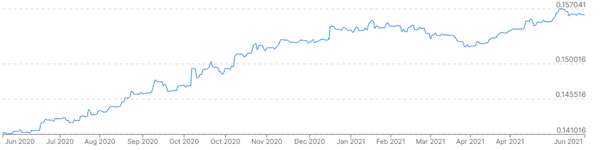

The exchange rate had no impact on AWG prices in June. The NZD was the same strength against the USD at the end of May (0.724) as it was at the start of May. The CNY continues to strengthen against the USD, which assists the Chinese log buyers purchasing logs in USD.

NZD:USD

CNY:USD

Ocean Freight

The Baltic Dry Index was sitting at 1200 in November and is now at 2857. It has dropped from its peak in May as the heat has been taken out of other commodity markets.

Trade data shows that iron ore imports in May were down 8.9% from April and steel exports were down 34%. The recent removal of export rebates by Beijing is likely to reduce iron ore demand in the coming months.

Source: TradingEconomics.com

The Baltic Dry Index (BDI) is a composite of three sub-indices, each covering a different carrier size: Capesize (40%), Panamax (30%), and Supramax (30%). It displays an index of the daily USD hire rates across 20 ocean shipping routes. Whilst most of the NZ log trade is shipped in handy size vessels, this segment is strongly influenced by the BDI.

The Singapore Bunker Price has continued to edge upward.

Singapore Bunker Price (IFO380) (red line) versus Brent Oil Price (grey line):

Source: Ship & Bunker

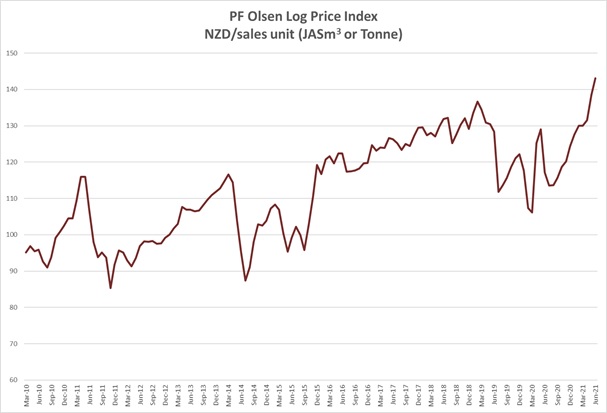

PF Olsen Log Price Index – June 2021

The PF Olsen Log Price Index increased $5 to a record $143 in June. The index is currently $22 above the two-year average, and $19 above the three and five-year averages.

Basis of Index: This Index is based on prices in the table below weighted in proportions that represent a broad average of log grades produced from a typical pruned forest with an approximate mix of 40% domestic and 60% export supply.

Indicative Average Current Log Prices – June 2021

| Log Grade | $/tonne at mill | $/JAS m3 at wharf | ||||||||||

| Jun-21 | May-21 | Apr-21 | Mar-21 | Feb-21 | Dec-20 | Jun-21 | May-21 | Apr-21 | Mar-21 | Feb-21 | Dec-20 | |

| Pruned (P40) | 180-200 | 175-195 | 175-195 | 175-195 | 175-195 | 170-195 | 204-218 | 200-214 | 184-192 | 180-190 | 180-190 | 170-185 |

| Structural (S30) | 125-160 | 125-139 | 122-136 | 118-132 | 118-132 | 115-130 | ||||||

| Structural (S20) | 109 | 109 | 108 | 108 | 108 | 105 | ||||||

| Export A | 171 | 165 | 150 | 148 | 148 | 138 | ||||||

| Export K | 164 | 158 | 142 | 140 | 140 | 131 | ||||||

| Export KI | 154 | 150 | 134 | 134 | 134 | 120 | ||||||

| Export KIS | 146 | 142 | 125 | 125 | 125 | 115 | ||||||

| Pulp | 46 | 46 | 46 | 46 | 46 | 46 | ||||||

Note: Actual prices will vary according to regional supply/demand balances, varying cost structures and grade variation. These prices should be used as a guide only.

A longer series of these prices is available here.

Log Prices

Select chart tabs

This article is reproduced from PF Olsen's Wood Matters, with permission.

3 Comments

According to the WSJ people who hoarded timber in the past are now selling as the price falls.Contractors etc hoarded timber as the price rose as they feared running out of timber.

Yep that’s the risk they take on. Even though prices tumbled they are still over double what they normally are, so they probably contributed to a price level that was not sustainable.

Nothing can stay that high - back to long term average like all products. Best cure for high prices is high prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.