The At Wharf Gate (AWG) prices for export logs dropped on average $18 per JASm3 in the higher quality grades and $23 per JASm3 in the lower quality grades. This was a combination of reduced CFR log prices in China and the NZD strengthening against the USD.

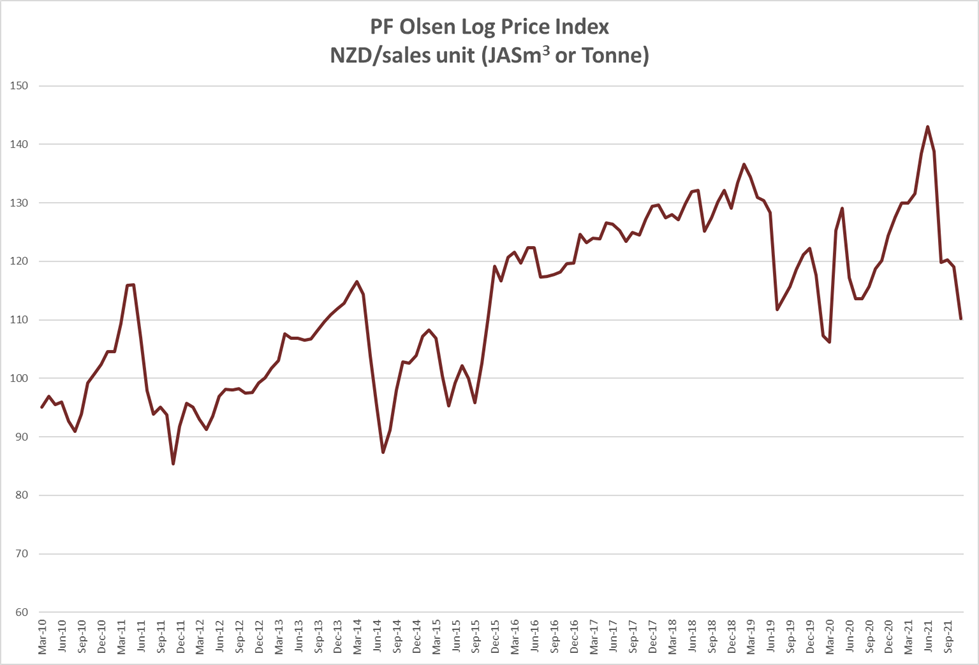

The PF Olsen Log Price Index dropped $9 in November to $110. The index is currently $12 below the two-year average, $13 below the three year-average and $15 below the five-year average.

Although the China log market remains subdued, AWG prices should increase in December due to ocean freight costs dropping 35% in the last month.

Significantly reduced log supply from New Zealand should see CFR prices increase in China in January.

Domestic Log Market

Log Supply and Pricing

Log pricing has generally remained flat as pricing was set last month for Quarter 4. While many harvesting crews are taking a longer Christmas break than normal, virtually all mills report they have sufficient log supply over this period.

Sawn Timber Markets

Domestic demand for sawn timber remains strong across all grades but there is some concern about the viability of building companies and construction projects due to the escalating costs of building materials

Export Log Market

AWG Prices

The AWG price range between exporters and ports remains extremely varied. This is due to varied sales strategies in China and the timing of securing shipping. Some exporters factored in a bigger price drop last month so didn’t reduce prices as much this month, compared to other exporters who held prices higher last month but had a bigger reduction this month.

China

The price for logs in China has dropped about 30 USD per JASm3 (17%) in the last month. The price is still highly variable with some exporters achieving sales for A grade logs at 150 USD while others are 140 USD per JASm3. As mentioned in previous Wood Matters articles there is a structural shift in the Chinese economy with the government looking to slow the property market and reduce debt levels, but as is often the case the market has overcorrected.

Softwood inventory levels are flat at 4.8m m3 and daily offtake is steady at 75k per day. While this is the time of year we usually see daily offtake hit 100k per day, there will be over 2m m3 fewer logs supplied from New Zealand in November and December than usual. This is because many forest owners have slowed or suspended harvest operations, and most continuing harvest operations will be taking an extended Christmas break this year.

The Caixin China General Manufacturing PMI unexpectedly rose from 49.2 to 50.6 in October. This was on the back of a further recovery in domestic demand. Economists note the government needs to further address how to balance controlling Covid19 outbreaks with maintaining economic activity.

If low harvest levels continue in New Zealand, there is likely to be a significant reduction in China log stocks and a shortfall of logs by the Chinese New Year in February. Much will depend on how the China property development sector recovers from its current situation.

India

The port of Kandla that supplies the sawmilling town of Gandhidham is oversupplied. There are reports of over 400,000m3 of unsold South American logs sitting unsold at the port, bonded warehouses, and in inbound vessels. Estimates of nine log vessels arriving in December means oversupply will last into Quarter 1 2022.

Due to the anticipated oversupply situation in November and December, demand is weak and the price for Uruguay lumber has fallen from INR 581 to INR 521 per CFT in the last month. The price for Radiata lumber has fallen from INR 641 to INR 571 per CFT.

Exchange rates

The NZD has strengthened against the USD by three cents over October. This adversely affected the November AWG pricing by about 6 NZD per JASm3. The NZD has weakened by two cents in the first three weeks of November, and this will also help December AWG pricing. The CNY continues to strengthen against the USD.

NZD: USD

CNY: USD

Ocean Freight

Shipping costs from New Zealand to China have dropped by 35-40% in the last month. Shipping costs from North Island ports are now in the low to mid 40’s USD per JASm3. The decline in the Baltic Dry Index is displayed in the graph below.

A softer dry bulk market is forecast for Quarter 1 2022. Iron ore prices have plummeted to below $100 USD per mt causing uncertain forecasts for shipping demand. Natural gas is the primary feedstock for most nitrogen fertilisers. The energy shortage makes natural gas more expensive which reduces fertiliser demand which reduces supramax and handysize voyages.

Source: TradingEconomics.com

The Baltic Dry Index (BDI) is a composite of three sub-indices, each covering a different carrier size: Capesize (40%), Panamax (30%), and Supramax (30%). It displays an index of the daily USD hire rates across 20 ocean shipping routes. Whilst most of the NZ log trade is shipped in handy size vessels, this segment is strongly influenced by the BDI.

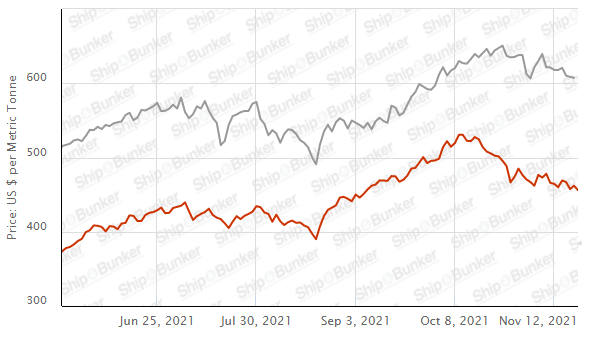

The Singapore Bunker Price has dropped through November.

Singapore Bunker Price (IFO380) (red line) versus Brent Oil Price (grey line)

Source: Ship & Bunker

PF Olsen Log Price Index – November 2021

The index is currently $12 below the two-year average, $13 below the three year-average and $15 below the five-year average.

Basis of Index: This Index is based on prices in the table below weighted in proportions that represent a broad average of log grades produced from a typical pruned forest with an approximate mix of 40% domestic and 60% export supply.

Indicative Average Current Log Prices – November 2021

| Log Grade | $/tonne at mill | $/JAS m3 at wharf | ||||||||||

| Nov-21 | Oct-21 | Sep-21 | Aug-21 | Jul-21 | Jun-21 | Nov-21 | Oct-21 | Sep-21 | Aug-21 | Jul-21 | Jun-21 | |

| Pruned (P40) | 180-200 | 180-200 | 180-200 | 180-200 | 180-200 | 180-200 | 150-160 | 194-200 | 194-200 | 194-200 | 194-200 | 204-218 |

| Structural (S30) | 120-155 | 120-155 | 125-160 | 125-160 | 125-160 | 125-160 | ||||||

| Structural (S20) | 100-105 | 100-105 | 105-110 | 109 | 109 | 109 | ||||||

| Export A | 108 | 126 | 128 | 128 | 163 | 171 | ||||||

| Export K | 99 | 118 | 120 | 120 | 156 | 164 | ||||||

| Export KI | 90 | 114 | 113 | 113 | 147 | 154 | ||||||

| Export KIS | 82 | 105 | 104 | 104 | 137 | 146 | ||||||

| Pulp | 46 | 46 | 46 | 46 | 46 | 46 | ||||||

Note: Actual prices will vary according to regional supply/demand balances, varying cost structures and grade variation. These prices should be used as a guide only.

A longer series of these prices is available here.

Log Prices

Select chart tabs

This article is reproduced from PF Olsen's Wood Matters, with permission.

11 Comments

Rather a generous A grade price for November?

Agree

The key issue would seem to be that log prices are now at a level that makes harvesting unattractive except in situations where there are both low harvesting costs and low transport costs to the port. This illustrates that the log industry is inherently an undifferentiated commodity trade, with forest growers having to take what is left over from a long supply chain. In a matter of weeks prices have declined from being record high to well below the five-year average. This illustrates that forest growers need to clearly understand that the price of cutting rights is highly dependent on ongoing infrastructure development within China. It is very much a boom and bust type of industry.

KeithW

It is an open market - prices climb and South America/Africa enter the market and supply glut forms. Prices fall due to over supply and SA shuts down. Even our most expensive logging locations are still cheaper than our global competitors. Nobody else on the planet produces clear wood with all the old growth gone - so we have a clear competitive advantage here also. Note prices for pruned domestic have not fallen.

Should we form a trading board to keep prices below our competitors or just ride the market. I'm of the latter - be in the market and keep innovating.

Keith your showing your bias !!

Any primary industry is the same in NZ. Wool - say no more, meat prices can collapse as well along with milk, honey, avocados etc etc

Covid, freight have thrown lots of spanners in the works. USD prices are still very high. Shipping has reduced by 50% in the last 3 weeks.

Price will be lower still but still profitable on good sites by end of Jan/Feb I would say. We pay our crews enough to allow for stand down for these periods. Domestic demand is through the roof.

Im still a happy camper and looking forward to a good summer break.

Jack,

You haven't actually identified a flaw in any of the sentences I wrote.

Each of the industries you refer to has its own commodity characteristics. And yes, some of them also have characteristics that can lead to boom and bust.

Your second to last sentence would seem to be very much in agreement with what I wrote, acknowledging that 'stand down' is occurring, that prices will be lower, and that 'good sites' can be profitable by 'end of Jan/Feb'.

One of the interesting attributes of log forestry is that the value of the standing timber is a relatively small percentage of the final landed price in China. Of course another key characteristic is the flexibility of time of harvest. These are two of the determining characteristics of timber. Each 'agribusiness' industry has its own defining characteristics, and this has been a key reason why I have found agribusiness (broadly defined) such an interesting field to investigate.

I have no fixed view as to where lumber prices will be in say three months time. But if I could work out where China's infrastructure industries will be at that time, then I would also be able to predict with some confidence what would be happening with logging in NZ.

In the longer term, I note that we have more timber to harvest in the coming years than we have ever had in the past. So that raises its own interesting questions in relations to the key markets of the future. But I do not claim there are any simple answers to those questions. If I were much younger and just starting out my career I would be tempted to upskill in more depth in relation to some of those markets and the associated issues within land economics.

KeithW

Im not saying we aren't reliant on China - the fact is all our main primary products are.

What Im saying is we are in the same paddock really. All primary industries have different characteristics but we all suffer from boom and bust. We all wish we could reduce this but commodities are commodities. I see Fonterra as a classic example of how they tried to move to higher end products but seem to have retreated to a more classic commodity mix.

I don't know what is going to be happening exactly in 6 months or especially in a year or 5 - no one does that I know in most primary industries.

On the log cut side in actual fact we are near peak production now and in the next 10 years we will see a reduction in harvest - some regions are facing this now - due to a lack of planting between 1998 and now plus forest removed for conversion to dairy. This potentially will cause some big issues.

The % of the price actually landed back to the forest depends a lot on where you are in terms of cost structure and markets. We are still harvesting and making very high returns in places with reasonable costs and a high % of domestic demand. Others in pure export log are poor - especially those in high cost areas. Think carefully where you plant.

At the end of the day the income you get depends upon your sale price less costs. Looking at the He waka eke Noa examples Hill country farming is making between $122 per ha and $400 per ha return before drawings. - $180 - $200k per farm before drawings, tax, debt principal and reinvestment. The last Beef and lamb numbers were at around $120 -$140k so its improved but again a big range.

Even with high degrees of processing etc the bottom line is not that pretty. Dairy is much higher.

We are all believers in our industries and hope for the best - thats why all primary producers keep doing it I suppose. If we wanted certainty and guarantees we would all have left!!

The key I believe is to be honest about what your industry does and plan for events which are likely to occur. Plan for busts to be there for the boom.

Except for investing in houses, that never goes bust. Upward forever.

Enjoy reading the comments.

The housing market makes all us primary producers look like idiots !! We should have just bought a few houses in Auckland 20 years ago, worked for a wage and we would be multi millionaires now. What should I tell my kids to do?

I have five kids. I could never tell them what to do obviously. They seem to have done the impossible, kids, career, OE and houses by mid 30s.

4 own houses or land, all bought realitively recent, in mid to late 20s with no parental help, all highly educated well paid. One didn't do uni but is really practical, truck driving in Aussie, farm manager etc.

The non house owner is ok, but "foolishly" bought 500 cows instead cause it's a productive asset actually producing something. They're well off but no way have they made the rediculouos gains of the other 4.

Not surprisingly that pisses them, all of them, off. They all work hard with hard working partners but housing has made a complete mockery of that.

Im in the same boat. My older ones have partners, all well educated working in Very well paid Tech and Finance jobs. Have houses, shares and travel around, well not much at the moment. None are interested in following after me - their skills are internationally transferrable, they are actually paid by Non NZ companies and their work is around the world - they just happen to be based here.

We are a bit blind here really as Primary products make up such a large amount of area and are in the news, usually moaning. In most wealthy countries these primary industries make up a very small part of the economy and wealth etc is built and sustained off service industries. If we look at GDP figures and trends the same thing is happening here as well - I think many Primary sector types find it a hard pill to take that we just don't matter as much and will even less in the future.

Houses in NZ are a special case though and I have been the doom merchant on this for years saying its unsustainable but Ive been wrong every time. It still makes me nervous but if Im honest the best passive investment Ive had has been just living in my house for 30 years and building a holiday house 15 years ago at the seaside.

But like a lot of primary producers I still like doing my thing on the land though so will keep doing it and suffer through booms and busts, unknowns, regulation, weather, disease risk, staff problems, long hours for zero return - sounds like the definition of madness or is it happiness!!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.