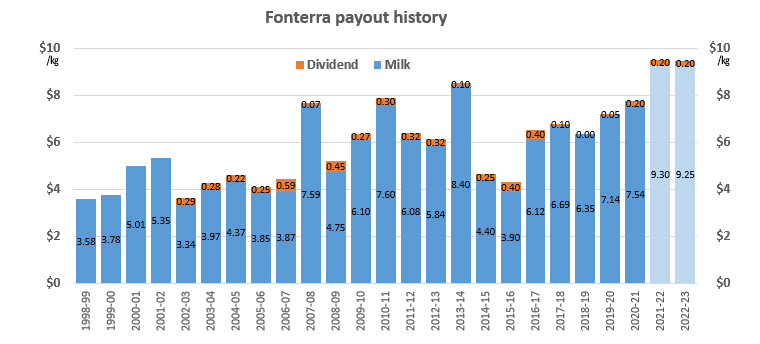

The lowering of the Fonterra forecast comes as a little surprise as the breadth of the earlier forecast of $8.75 - $10.25 looked like it would capture most eventualities. But apparently not with the 25 cent trim from both ends ($8.50 – $10.00).

Given that the last adjustments upwards occurred a little over a month ago (June 23rd) many will be wondering what has changed to bring this review downwards or was that earlier lift perhaps too bullish and the latest adjustment more of a reality check. They shared the earlier view with the banks who generally felt “the fundamentals were sound” with supply down in the Northern Hemisphere and even with the last GDT auction which fell -2.9% were happy to hold onto their earlier projections.

However, it is still early days in the season and no doubt there will be further adjustments ahead and they could go either way.

Among the comments coming out was one from a Federated Farmers spokesman who highlighted the fact that the breakeven point for most dairy farmers was $8.18 per kg MS. Most likely this includes a heavy dose of debt servicing, but it did make me at least blink at that figure. While the prices remain above the $9.00 mark things are OK but if the average is $8.18 there are bound to be a considerable number well above that and they must be in nervous territory.

On the brighter side, dairy debt is reducing with the Reserve Bank being quoted as saying it has reduced by over $5 Billion (a 12% reduction) since its peak in 2018. However, including the current forecast the average for the last 4 years is around $8.30 per kg MS so plenty of downside potential.

The mud forecast

In the meantime, farmers must be sick and tired of having to spend days, weeks, months trudging through mud.

It used to be said that “where there is mud there’s money” but this year has got a bit ridiculous with all sorts of rainfall records broken and the end not in sight yet. Many regions across the country have experienced their wettest winter on record and 5 days to go.

The latest flood events in the South Island has led to many outlying parts of milk collection runs having major disruptions and if the extreme weather events continue to increase, as is predicted, it must make both farmers and processors start to question the economics of these farms in the future. Outlying parts of Westland appear particularly vulnerable and while Bright Dairies made a commitment to continue to collect milk into the foreseeable future when they brought into Westland nothing is infinite and the weather is certainly compounding the pressures on the economics of collecting from far flung farms.

With the heavy costs of floods and slips on both farm and national infrastructure it feels a difficult choice to decide which is worse, floods or droughts. Or at least it feels like that until the next drought hits. I personally always feel there is nothing quite soul destroying as a drought. Floods hit those affected more physically while droughts (to me) are really tough on mental health.

Hopefully, once the season progresses somewhat, the sun will shine and all will have some reprieve from both and long may it last.

Dairy prices

Select chart tabs

4 Comments

Hi Guy,

Westland was bought by Yili not Bright, the later own approx 38% of Synlait.

Great August in Southland ... very good start to the season down here.

Federated Farmers say "breakeven point for most dairy farmers was $8.18 per kg MS." Seems high to me. As well as a heavy dose of debt servicing, does this include drawings?

Dairy farm price expectations going into the coming spring selling season will be interesting. Vendor expectations driven by agents' excessive positivity versus a prevailing cautious/negative mood among the bank managers I know. Five years ago the suggestion of a $9 payout would have had us racing off to buy new tractors and utes. Now the number I focus on is my monthly principal repayment.

Good if wet start to the season here, mostly warm rain so great growth. More than 950mm in June July, normal would be well less than 1/3 that.

$8+ breakeven? Ridiculous

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.