By Keith Woodford*

In New Zealand, we have yet to come to terms with the reality that the future of our dairy industry is highly dependent on China.

America does not need us. Europe does not need us. The oil producing countries can no longer afford us. Africa has never been able to afford us.

So it is all about Asia.

Our dairy products can have a place in many Asian countries – Thailand, Singapore, Malaysia, the Philippines, Sri Lanka, Vietnam, Korea, Japan, and so on. All of these countries can and will make a difference to overall demand. But without China, it won’t be enough.

Further west, Iran my well open up, particularly if oil prices recover. India is the other big one, but for the foreseeable future, India will largely meet its own needs.

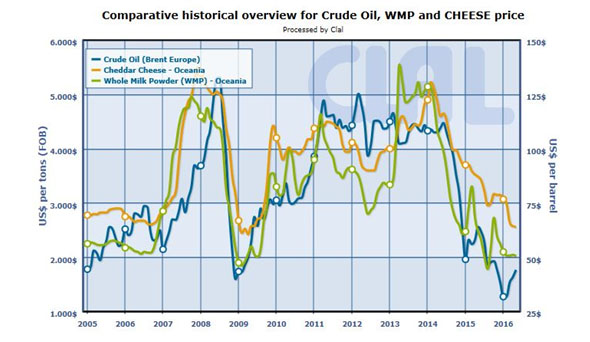

In the past, our dairy industry has benefited greatly from high oil prices. This sounds counter-intuitive, but for the last ten years, apart from China, it has largely been the oil-producing countries who were out there using their oil income to buy milk powder. There has been a remarkable correlation over this period between oil prices and milk powder prices.

Source: http://www.clal.it/en/?section=petrolio

There were even a couple of years when oil-producing Venezuela was our largest purchaser of whole milk powder (WMP). But Venezuela is now in turmoil and any recovery will be slow.

So the key reality, is that regardless of what happens elsewhere, and even with an oil rebound, the numbers can never stack up without China in the mix.

The idea that China ever left the market is considerably misplaced. The 2015 calendar year was indeed a quiet one for China’s milk powder imports, with whole milk powder imports declining to 347,000 tonnes after purchasing 619,000 tonnes in 2013 and 671,000 tonnes in 2014. Nearly all of this WMP came from New Zealand.

Despite this step back, China was still by far the largest importer of WMP in 2015. Next came Algeria with 210,000 tonnes, much of it purchased from the adjacent EU.

Algeria tends to be a buyer that comes in and out of the market, buying mainly when prices are low. However, in the early months of 2016, and despite low dairy prices, it seems that Algeria is largely absent from the market. Algeria’s problem is the same as other oil and gas-producing countries – they no longer have the cash flow needed to purchase WMP.

In the last few days, the EU Milk Observatory has published global import and export data for the first three months of this calendar year. What is evident, is that China’s WMP and SMP (skim milk powder) imports are recovering, although there is still some way to go to reach the 2013 and 2014 figures. So far, WMP volumes are up 24 % and SMP volumes are up 29% on the same three months last year.

A key note of caution is that although China’s milk powder imports are increasing again, the increases are lower than for most other dairy products. There is emerging evidence that WMP will be a declining component of the Chinese dairy industry in future.

For example, latest statistics from industry analyst CLAL in Italy depict how liquid milk consumption per capita in China increased 9% between 2013 and 2015. However, milk powder consumption per capita dropped 17% during this same two-year period. Over a longer five-year period, liquid milk consumption per capita is up 35% but WMP consumption has essentially been static.

Over the most recent two-year period from 2013 to 2015, China’s cheese imports increased 60%, butter imports increased 36%, infant formula imports increased 57% and liquid milk imports increased 150%. It was only WMP and SMP that went down.

So far this year, China’s liquid milk imports (mainly UHT) are running at 80% up on the same months last year.

In 2015, China’s largest category of dairy imports was whey at 436,000 tonnes. This largely comes from the world’s big cheese producing regions, these being Europe and the USA.

The final destination of all this whey powder is unclear. Some will be for human consumption, and some will be ‘sweet whey’ containing a mix of whey and lactose, which probably ends up in animal feeds.

One of the interesting statistics is imports of pure lactose. The most recent statistics for the first three months of this year show that China is only number two for lactose imports.

So who beats China on lactose imports? The answer is good old New Zealand!

So why do we import so much lactose into New Zealand? The answer is that our cows produce milk in which lactose is a lower proportion than the international standard. So each year we import up to 100,000 tonne of lactose, largely from Europe and the USA, which we then mix in with our NZ-made milk powder.

Lactose is typically one of the lower value components of milk powder. So not only does its importation to New Zealand give us an internationally standardised product; it also bulks-up the milk powder and hence is a nice money-making venture.

Within the trade, the presence of imported lactose in New Zealand milk powder is no real secret. However, it is an issue to be thought about by those who argue that we could get more mileage from our so-called grass-fed products.

Turning back to China, the overall evidence is very clear that China’s demand for imported dairy products is increasing. However, the future demand for WMP is less certain. If China does want more WMP in future, then it will be following a pathway different to other countries that have travelled from a ‘developing’ to a ‘developed’ economy.

A big part of the equation is working out how much milk can China produce for itself. The answer is that China struggles to produce the feed for its growing herds. Hence, milk production over there is expensive.

If it were just a case of simple economics, then China would import much or even most of its dairy products. But these things never come down to simple economics. Food security, plus the politics and welfare of rural development, also come into the equation.

In a simple world of open borders and totally free trade, then China would import most of its cheese and butter. It would also import much of its UHT (long life) milk. And with emerging technologies for extended shelf life (ESL) refrigerated milk, it would also import increasing quantities of ‘fresh milk’. In that simple world, as internal chilled facilities improve, the demand for both local and imported WMP could be expected to decline.

Estimates of the proportion of China’s dairy consumption that is currently imported depend, to a considerable extent, as to how the imported whey is allocated between human and animal uses. However, as a working number, I estimate that total dairy imports for human use are about 15% of total liquid milk equivalent (LME) consumption. My expectation is that this will increase. But in reality we don’t have quality ‘on the ground’ research to make sound estimates of what is happening to China’s overall industry.

So how should we be responding in New Zealand?

The first point on which agreement should be easy to obtain – if logic is the basis of our judgements – is that we cannot have a vibrant dairy industry without China. The second point of agreement –although I have not had time to develop this argument here – should be that wholesale conversion of New Zealand’s dairy land back to sheep and beef cattle is no solution. It is very easy to show that the economics of that do not stack up.

The challenge we face in New Zealand is that over the last 15 years we have developed an industry that is highly dependent on WMP. This is a very different industry than the butter and cheese-dominated industry that we had throughout the 20th century.

Since the turn of the century, the WMP strategy has worked very nicely for us until the last two years, built on oil-funded purchases by the oil producing countries, combined with the unique trajectory of China’s economic growth.

There was a very good reason why we went the WMP way. Quite simply, for a seasonal industry that produces most of its product in spring and early summer, and given the price signals of the time, it was an apparently obvious way to go. Seasonal production and WMP go hand in glove.

But what we have is a one-trick pony. To take an analogy from another industry, we have nearly all of our dairy eggs in the same basket.

If we want to reduce our risks from a highly volatile product, then we are going to have to restructure our industry. Unfortunately, our industry has yet to come to terms with what that means. It won’t be an easy journey.

Keith Woodford is Professor of Agri-Food Systems (Honorary) at Lincoln University and a Senior Fellow (Honorary) of the NZ Contemporary China Research Centre. His archived writings are at http://keithwoodford.wordpress.com

33 Comments

And thoughts that on BAU terms we compete price wise at the global marginal costs area (different to average costs).

This thinking is further on from Goldman Sachs of 24 mths ago seeing us pass the swing producer title to USA. Its because volume can now move as price does.

Prof Gow.:

http://www.radionz.co.nz/audio/player/201801098

payout of $4 something/starting with a 4 for years

Henry,

Hamish Gow and I are on the 'same page' to the extent that we both believe that the global dairy market has indeed changed,. But predicting a price of less than $5 for 'several years', as Hamish has done on RNZ, is somewhat 'brave', and in my opinion under-estimates volatility and the associated short term unpredictability.

Marginal costing issues are important, both globally and in NZ.

Here in NZ, fixed costs tend to be high and 'sticky'. Hence reducing feed inputs can easily result in reducing revenue by an even greater result because most other costs are indeed 'sticky.

In this current year, most of my dairy mates have actually increased production and spread their fixed costs over more production. Cost of production has gone down - aided by a good weather year and reduced input prices with lots of sharp deals available. Any feed deficits have been met with PKE plus in some cases early culling of cows, and both of these have made economic sense. They are sailing along nicely, and some are even pressing the 'go button' for further development at good infrastructure cost prices. But that is only possible for those who have positioned themselves in past years.

Next season will be interesting, with national production likely to be down somewhere 6-10%. Cost of production will be down for many farmers, but this will be more due to sharp input prices than moving down the marginal cost curve. For many, moving down the marginal costs curve, as supposedly taught in Economics101, will actually have been counter productive because of the specific structure of the MC curve, such that even at low product prices, MC<MR. The economic 'sweet spot' ( as taught in the correct version of Economics101) is where MR< MC, not, as some in DairyNZ seem to think, where MC is a minimum.

My mates will largely hold their production next year. As one farmer said to me in this last week, if he can get a milk price of $4.50, then after adding in the Fonterra dividend and livestock sales, he can pay a dollar of debt per kg MS, and still have very considerable free capital for living and further development.. By my calculations, a milk price of $3.90 next year will still give him a good living, but with no room for capital expenditure. But of course many are not positioned in that way as a consequence of a different set of historical decisions.

Keith W

Keith, it is well known that men bullshit. And in my experience dairy farmers do it a lot. Suddenly its the thing to be able to make money at these low prices. So everyone is bragging how they can do it. Its kinda amusing.

Belle,

Yes, some dairy farmers are like fishermen in the tales they tell. However, I like to see the numbers and where they are coming from, and I certainly don't use pub talk. At the moment, it is tough for everyone - not helped because there were no residual payments early in the season, and this year's residuals have still to come. So the cashflow milk income is considerably lower than the headline $3.90. But some farmers are still managing to run cash flow positive this year after interest repayments, with a range of contributory factors. But for most farmers, there is nothing they can do in the short term that will eliminate the negative cashflows. It is all about survival until recovery occurs. And there is nothing amusing in that!

KeithW

Oh I dont know Keith...It all got out of hand didnt it. Like housing at the moment. Now the farmer is desperately trying to justify his/her existence.

Yes, there seems less chance of surprise to the up side

But more and different risks (aside from "predictions farmers will do it tough for another three years)....

Ultimately, Fonterra's Oceania chief Judith Swales' argument – which has triggered almost more of a backlash than Murray Goulburn's profit warning and price cuts (Keely says farmers are "filthy" with Fonterra, even more so than MG) – seem to ring true: the global dairy market is in a slump, and Australia can't be immune.

"The fact is that, for some time, the price paid to Australian dairy farmers for milk did not reflect the reality of the international market," Ms Swales, who runs the country's second largest milk processor, told The Australian Financial Review this week.

"A global over-supply of dairy and softer demand has weakened global dairy prices.

"The Australian dairy industry has to get real about milk prices and find ways to adjust to the new lower milk price environment that we expect is likely to continue next season."

Read more: http://www.afr.com/business/agriculture/herd-mentality-why-the-dairy-in…

Follow us: @FinancialReview on Twitter | financialreview on Facebook

And a little on price discovery

"They genuinely felt they hadn't done anything to hurt any individual dairy farmer and there was a lot of frustration about some of the claims that were being made," one former Coles source said.

"But it took a lot of money out of the profit pool, leaving little for farmers or processors."

Five years later, consumers have embraced $1-a-litre private-label milk and Coles, Woolworths' and Aldi's house brands now account for about 63 per cent of drinking milk sales, according to Dairy Australia.

But dairy farmers are still up in arms, saying Coles' strategy has permanently devalued the price of milk in the eye of the consumer and accusing Coles of stripping more than $220 million a year out of the milk profit pool. The fact that Aldi is selling private label milk for $1 a litre rarely rates a mention.

The average price of white milk is now $1.34 a litre, taking into account private label and branded prices, cheaper than bottled water and soft drink.

Read more: http://www.afr.com/business/retail/coles-1-a-litre-milk--masterstroke-o…

Follow us: @FinancialReview on Twitter | financialreview on Facebook

Henry, this is the one where Miss Zhu let slip about the Chinese economy

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=116…

Rod Oram latching on to the concept of the Bonlac Supply Agreement

http://www.radionz.co.nz/audio/player/201801848

http://www.radionz.co.nz/national/programmes/ninetonoon/audio/201801848…

When you as small as NZ the accusation of 'all the eggs in one basket' is almost a structural necessity. So I don't see that as any kind of failure as such. If we didn't focus our limited resources as much as we do we wouldn't get as far as we do.

It is inevitable that change comes and that time seems upon us.

I think exporters in NZ need to be like the All Blacks. Centrally organised, everyone in the industry playing with one goal, all focused on the national (central) result.

Ralph, you raise an excellent analogy. New Zealand's most successful organisation is a product to a large degree of central planning. The likes of the English and French unions with far greater resources are a disparate rabble seemingly basing their model on the NZ Red Meat Sector and getting the same result!!

The likes of Zespri have proven that it is a business model that can work here when the strategy is right. Unfortunately, as Keith highlights, Fonterra got sucked down the commodity path. In fairness to them it was the inevitable outcome of the DIRA and being played like a violin by China.

From President Xi from his November 2014 NZ visit:

President Xi said people here in New Zealand should not be worried by the free trade deal between China and Australia.

"On the contrary, possibly, New Zealand will have to worry about the fact that there is more Chinese demand than you can possibly supply. We have a very stable market there and the market will continue to expand in the future".

Keith, and others, have highlighted on a number of occasions that NZ needs to do much better differentiating our pasture fed/free range products. Progress has seemingly been non existent and we have now been overtaken by the Irish and their "Origin Green".

http://farmersweekly.co.nz/section/all/view/green-kiwi-story-sells-food

As you say Keith, next season will be interesting. One of the interesting parts will be the market share changes and a upshot of that will fit nicely with the need to move from WMP. Simplistically Fonterras share will likely be down and with it WMP production but others producing other products will rise. Despite being the biggest I can't see Fonterra directing the need shift in production.

Differentiating our milk from competitors by promoting the nutritional superiority of natural NZ pasture derived milk is where it's at. Provided that processing WMP can retain the nutritional distinction and superiority of pasture derived milk, there is value in that, as discerning customers in China, Europe, USA....are becoming increasingly aware of and demanding nutrition that can be derived from such product.

Unfortunately Fonterras 3V strategy seems more in line with your vision Keith, in that our milk is no better than that of our competitors.

Omnologo,

In regard to our milk 'quality' I have no 'vision'. I simply go where the science takes me. In regard to 'pasture fed', there are market opportunities just like there are opportunities for organic milk. ( Note Bellamys in Australia and Organic Valley in the USA, both big success stories.). But the science in regard to pasture fed is not compelling. However, I agree that a number of small scale manufacturers are making it work for themselves in specific markets. And here in NZ, with Munchkin and Synlait working together, it will be interesting to see the market penetration that Munchkin can achieve. As for the 3V strategy, I find that to be just words with no great meaning. But apparently it does resonate very much with Fonterra's CEO, who I am told, invented the term himself. So within Fonterra, it makes sense for staff to climb aboard that cause.

KeithW

Interesting comment Keith. And brave of you. The volume bit is sure resonating in the depths of hell somewhere.

Belle, how are the bulls going? Beef price in California for angus steers is the worst price for 10 years. Last year $2.49 a pound, last week $1.25. The halving of the price in the States hasn't affected us yet as China is now taking most of our beef. Just keep a eye on Brazil, if it starts to dump it will be the event required to collapse prices as the huge beef numbers in the world look for a consumer.

http://finviz.com/futures_charts.ashx?t=LC&p=m1

http://www.thebeefsite.com/news/49673/cme-meat-availability-continues-t…

http://www.beefcentral.com/trade/does-brazils-rapid-export-expansion-re…

Andrewj

I agree that there are some very real risks for NZ beef prices in both the short and medium term.

I work with colleagues from the Brazil beef industry.

I don't see Brazil as 'dumping' but I do see scope for production increases from Brazil.

And new market access for Brazil beef in the US and China will compete directly with NZ beef as they fit into the same category (grassfed, lean).

At some stage - when time allows - I will write about their industry. Particularly in the south, there is scope for earlier turnoff and higher productivity. And market conditions are now favouring those technologies, whereas previously, with market access problems, the economics were much less attractive.

Keith

Keith, you do a great job, thank you for the input. I was amazed to find that dairy bull calves California went from $15 a head to $500 in two years, so the beef industry is in a state of restructure with both new technology and new entrants. Thanks for the heads up on the impact of sex selection, you were way out front.

Frome Brazil

If you keep farming like you have for the last 40 years you will go out of business.

http://www.abiec.com.br/eng/news_view.asp?id={5D7D1422-104D-4F1D-8824-EB687CC29025}

Hmmm, have to play with that link. try this and click on sleeping giant

I will read your links when time prevails Aj. I have been slowly killing all my older stock and not replacing with r2s to fatten over winter/spring. Replacement cost is eye watering so I am not bothering. I have a great crop of r1 bulls and their fate is up in the air. Might take the ridiculous dosh now and run for the hills. So Keith is seeing the warning signs. Anzco had a warning in their newsletter. And I heard Susan Kilsby on the radio saying the same. The saleyards tell a story of desperation and ignorance. Excema looking 150kg heifers easy making $550.

Belle, we are in a bugger of a drought but we had good rain last night which should help and it's still very warm for this time of year.

I have the last of my 18mth bulls going on Monday and then I have found a local with a feed crisis and he will graze my farm till December. So I am out of the cattle market from Monday. Talked to my bank manager , he has a small farm and is out buying 2y steers, I lifted an eye brow at that and he wanted to talk about why.

That BRazil link i sent to Keith sums it up.

quote,

'If you keep farming the way you have for the past 40 years, you will go out of business'.

http://www.abiec.com.br/eng/news_view.asp?id={5D7D1422-104D-4F1D-8824-EB687CC29025}

That link is hopeless, try to cut and paste or look at the link and go to sleeping giant.

Tried it, i can get the gist of it. Like reading without glasses.

Glad to hear you had rain. Looks like lots more coming. And pretty warm here too.

Belle, here are some stats for you

http://beef2live.com/story-world-beef-cattle-statistics-0-108033

That link doesnt like mobile either. But I got most of it. It would be interesting to see at what point the crash in fish stocks determines the level of beef being eaten.

If New Zealand cows produce milk in which 'lactose is a lower proportion than the international standard', perhaps there's a global - or largely Asian - market for 'low lactose milk'.

Having no better information at hand immediately than wikipedia, I see that 'Most mammals normally cease to produce lactase, becoming lactose intolerant, after weaning, but some human populations have developed lactase persistence, in which lactase production continues into adulthood which likely developed as a response to growing benefits of being able to digest the milk of farm animals such as cattle. Research reveals intolerance to be more common globally than lactase persistence... The frequency of lactose intolerance ranges from 5% in Northern European to more than 90% in some African and Asian countries.'

If low fat milk products can make a market, why shouldn't low lactose? One of the greatest lessons in business as in life (for they're inextricably related) is 'start with what you have'.

Yes, we could produce both low lactose or lactose free milk. There is, however, an issue with taste. Most lactose-free milks therefore add other sugars. But the big step forward with lactose and lactase issues is A2 milk. Although this has the same amount of lactose, the fermentation thereof is less because, unlike A1 milk, it does not get delayed passing through the intestines. Here is a recent paper from China, with these effects now being assessed in the West in current clinical trials.

https://nutritionj.biomedcentral.com/articles/10.1186/s12937-016-0147-z

product innovation, its all there in front of us..

Dairy products are versatile. In most instances, they can be consumed as is, minimally processed in both foods and beverages during any eating occasion. If there is one thing dairy suffers from, it is being pigeonholed into traditional consumption roles: milk and cookies, milk and cereal, cheese on pizza, yogurt eaten in the morning, milk in coffee, ice cream and cake.

These are valuable roles for dairy products and ones that need to be protected. However, the industry can capture new volume through new uses and occasions. In order to compete in the snacking occasion, the industry needs to innovate. Innovation beyond flavored milk, beyond snack cheese, beyond spoonable yogurt, beyond new ice cream flavors, beyond whey-based sports beverages, and, very possibly, beyond the refrigerated dairy case.

To compete in the snacking occasion, the dairy industry needs to look past the usual competitive set and take a broader view. It needs to compete in new categories and go after new consumer segments. By capitalizing on the versatility of dairy products and using the snacking market structure outlined in this white paper as a roadmap for innovation, incremental dairy volume could come from the snacking occasion.

http://www.thinkusadairy.org/Documents/Customer%20Site/C3-Using%20Dairy…

but with big food, I've a feeling we're not in Kansas anymore...

http://www.amazon.com/Salt-Sugar-Fat-Giants-Hooked/dp/0812982193

Sugar Identified as a Top Cause of the Global Cancer Epidemic

http://www.wakingtimes.com/2016/02/24/sugar-identified-as-a-top-cause-o…

Thank you, Keith. Surely it would be fair to presume that, with the majority of global populations being lactose intolerant and with the points made by Henry Tull and Andrewj, that the development of palatable reduced lactose or lactose-free dairy would be a priority among dairy industry strategies. When it is said that this or that country doesn't need us, it is more usually the fact that they just don't need what we produce.

In China, for example, an annual growth rate of 10 percent is forecast despite the fact that a large part of the population’s disposable incomes are not yet sufficient to allow dairy products; especially lactose-free products, to be affordable

http://www.apfoodonline.com/index.php/bf/item/723-asia-pacific-lactose-…

In addition to these benefits, Fonterra’s scientists are able to precisely control the hydrolysis to make hydrolysate ingredients with a range of different attributes, which enable a variety of product characteristics including ............... lactose-free and Halal, or Kosher status.

http://www.fonterra.com/wps/wcm/connect/Fonterra_NewZealand_en/Fonterra…

Greetings Keith.

Although you claim the science on nutritional distinction and superiority of milk derived from cows fed exclusively pasture is not compelling, I would suggest that a google search suggests otherwise, and more importantly, increasing consumer insight, awareness and perception in response to the effects of industrialised food production and delivery. Ironically having followed your argument for breeding cows that carry the A2 gene and selected sires accordingly, it’s been in resistance from advice to the contrary, based, believe it or not, that the science is not robust enough. In this day in age it increasingly seems science takes you in the direction you pay it to.

As a farmer trying to cope with the roller coaster of so called market volatility, I find the strategy of supplying undifferentiated milk to global consumers uninspiring, particularly when governance and management continually fall back on the corollary excuse of ‘market volatility’ to justify poor returns.

The assertion that to add value to NZ milk requires massive capital investment, beyond the capabilities is also frustrating, as it not only ignore the unrealised value inherent in pasture derived product, it’s also an excuse to further undermine the cooperative structure which has served farmers so well, in favour of selling out to corporate investors who are repatriating that grass fed value offshore, e.g. Synlait and Danone. Meat and wool industry here we come.

Omnologo,

Although Google is a great place to start, it also picks up all of the assertive material as well as the genuine science. It is true that pasture fed cows will produce more omega 3 fatty acids, but these are the shorter chain omega3 acids, with very low translation through to longer chain omega 3s which give the supposed health benefits. In contrast, fish contain the longer chain Omega 3 fatty acids. The evidence in relation to fish-derived Omega 3 fatty acids remains controversial but I find it to be moderately persuasive. However, the clinical evidence for documented health benefits from milk produced by pasture-fed cows is, to the best of my knowledge, non-existent.

As for the science around A2, I came to that as an 'agnostic' and indeed initially a sceptic. But once I got into the detailed science I soon changed my mind. You are right - there are some who claim the evidence is not robust, and they are people and organisations for whom the A2 issue (or more specifically the problems with A1 beta-casein) is a threat. As the infamous Mandy Rice Davies said so long ago ( at the time of the Profumo scandal), "they would say that, wouldn't they". Interestingly, those same people are unwilling to engage in a one-on-one debate with me on these matters. At times it is somewhat like a tidal river - with public debate ebbing and flowing - but the overall direction of the river of science is only flowing one way. More science is on the way.

As for co-operatives, I have always been a supporter of co-operative principles. but co-operatives - like investor orientated firms - only prosper when they are well managed and well governed. And the Achilles heel of co-operatives is the difficulty they have in investing to meet new challenges unless they have a war chest all ready to go.

KeithW

Thanks for your feedback Keith.

Perhaps the science on superior properties of milk derived from pasture is controversial or non-existent as far as you know. However the properties of milk derived from pasture are distinct to that derived from grains, and other concentrates including PK. In fact Fonterra has recommended limiting the amount of PK used by suppliers during lactation, as it imparts properties which inhibit certain manufacturing processes. A comparable observation can be made to eggs either derived from factories or free range, and the respective hen diets. People prefer free range and are prepared to pay more, not just for ethical reasons, but also taste and quality.

I agree that cooperatives only prosper if well managed and governed, but therein lies the rub. If tried and true cooperative principles are respected and adhered too, it mitigates the risk of substandard governance and management. A well-managed cooperative will always have sufficient to meet needs of long term intergenerational sustainability, as illustrated by the balance sheet of Tatua, and the NZ dairy industry prior to DIRA and Fonterra.

http://agrihq.co.nz/section/dairy/view/brownes-cuts-farmers-loose

Fonterra are suddenly not looking so terrible in comparison to Australian dairy companies that are refusing to pick up milk from some suppliers in an effort to reduce milk supply.

It seems that most companies are saying that milk prices are going to continue to be very poor for a while yet, while I wonder where Fonterra is hiding all of the product that they have not sold through the GDT to try and boost prices.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.