Waning farmer satisfaction with their banks underlines that a government Farm Debt Mediation Bill would be "a useful tool in the tool kit," Federated Farmers says.

Federated Farmers latest banking survey shows farmer satisfaction with their banks at its lowest level since the survey began.

Although 73.7% of the farmers who responded to the survey said they were satisfied or very satisfied with their bank, that's down 5 percentage points since the previous survey in May. And as a group, more farmers, 11.6%, reported feeling "undue pressure" from their banks than at any time since August 2015. That's up from 9.6% in May. The average increase in a feeling of undue pressure from dairy farmers went up 2.4 percentage points to 16.2% from 13.8% in the six month period, and for sharemilkers the increase was even higher, rising 6.5 percentage points. It means 20% of sharemilkers now feel they are under undue pressure, Federated Farmers says.

"The results show a need for renewed efforts to improve relationships between farmers and banks," Federated Farmers' economics and commerce spokesperson Andrew Hoggard says.

"It also underlines the fact that farm debt mediation - voluntary ideally, but mandatory if necessary - would be a useful tool in the tool kit. We look forward to the Government advancing a Farm Debt Mediation Bill after the original NZ First Member’s Bill was withdrawn a few months back for improvement," Hoggard says.

The survey is conducted for Federated Farmers by Research First. There were 749 respondents. It's the tenth iteration of the biannual survey dating back to 2015 that's typically conducted in May and November.

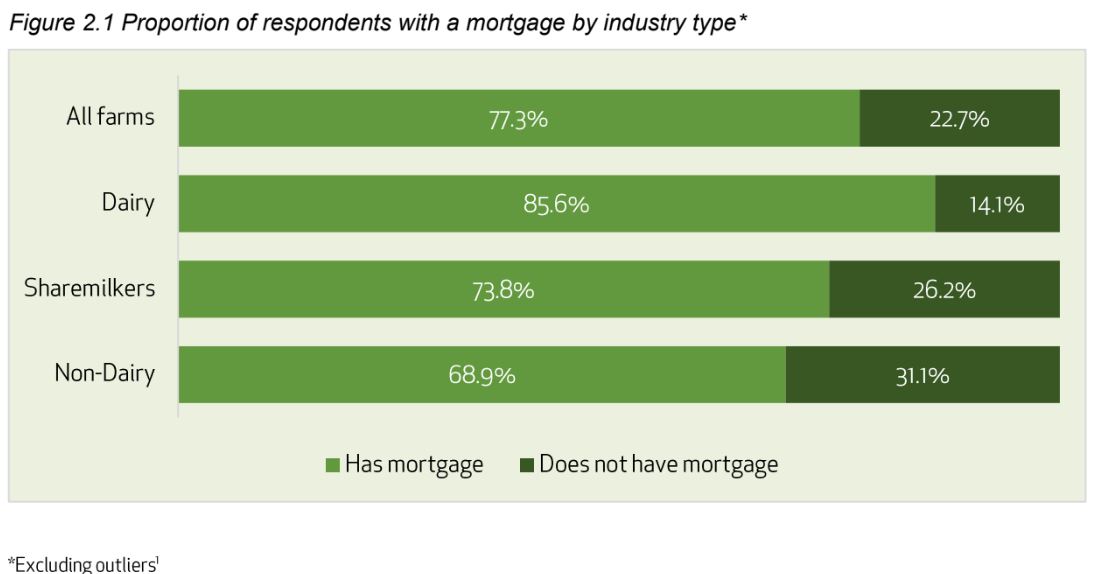

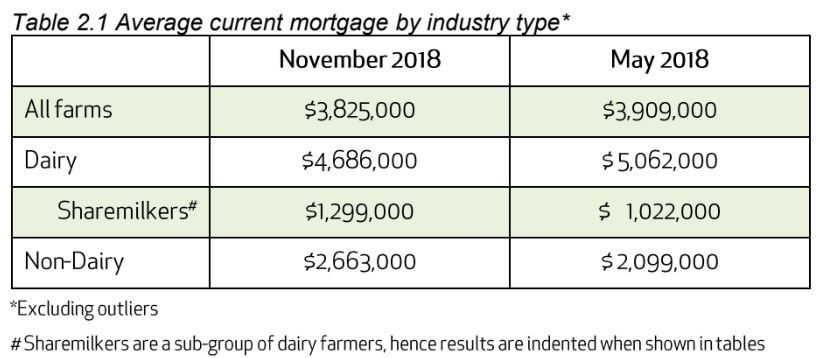

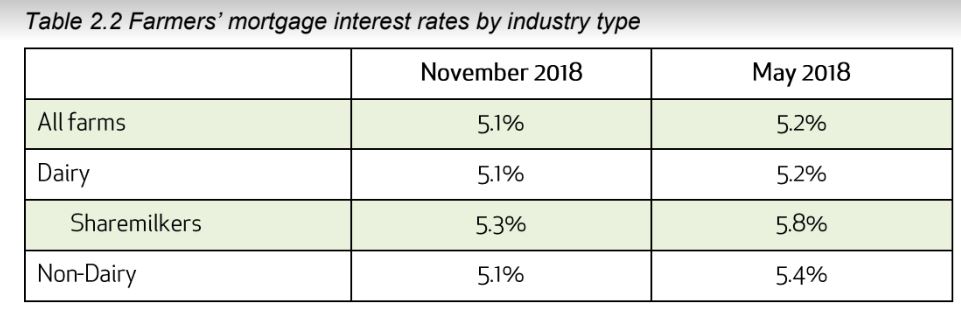

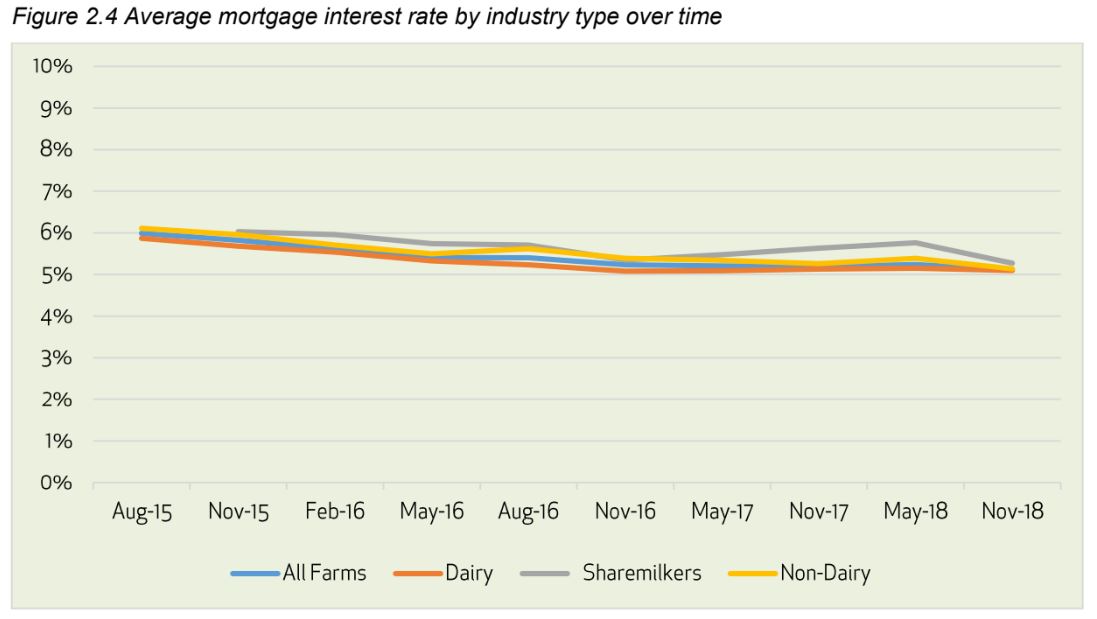

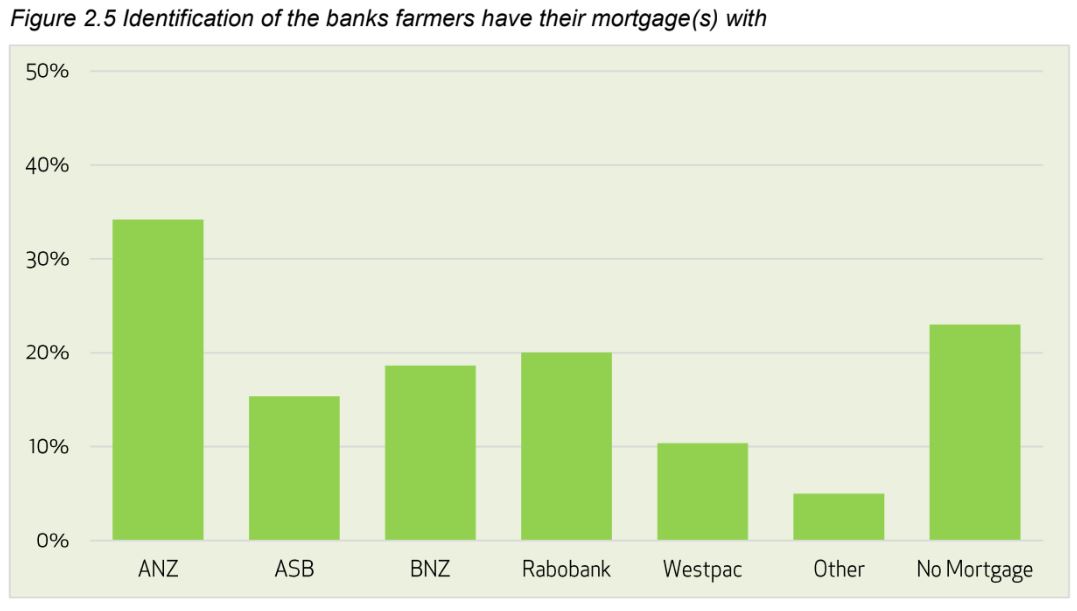

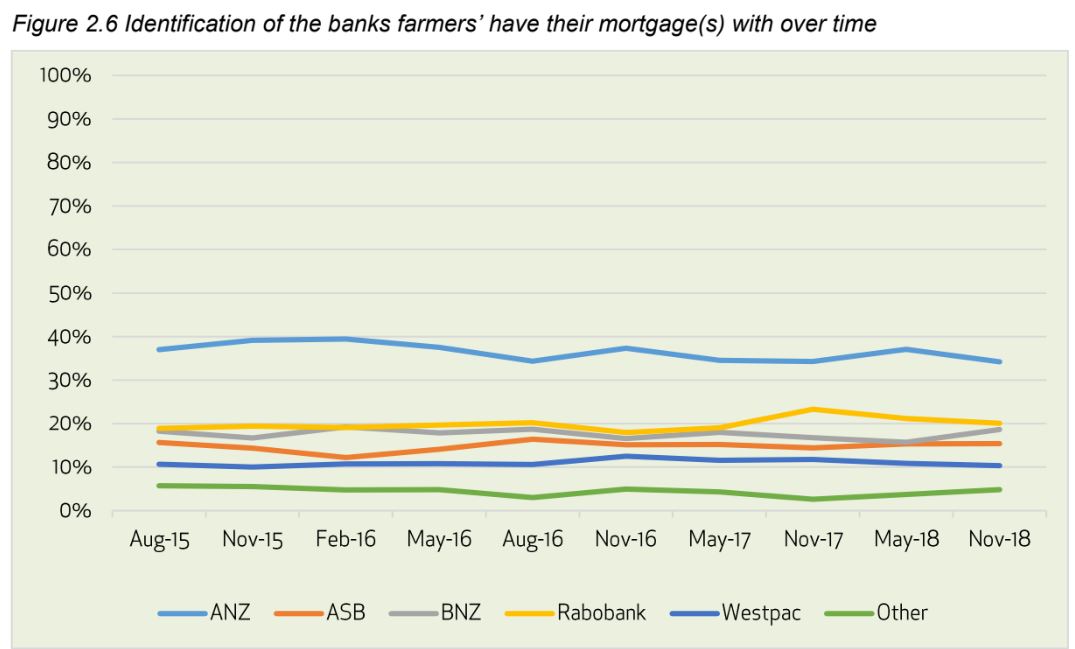

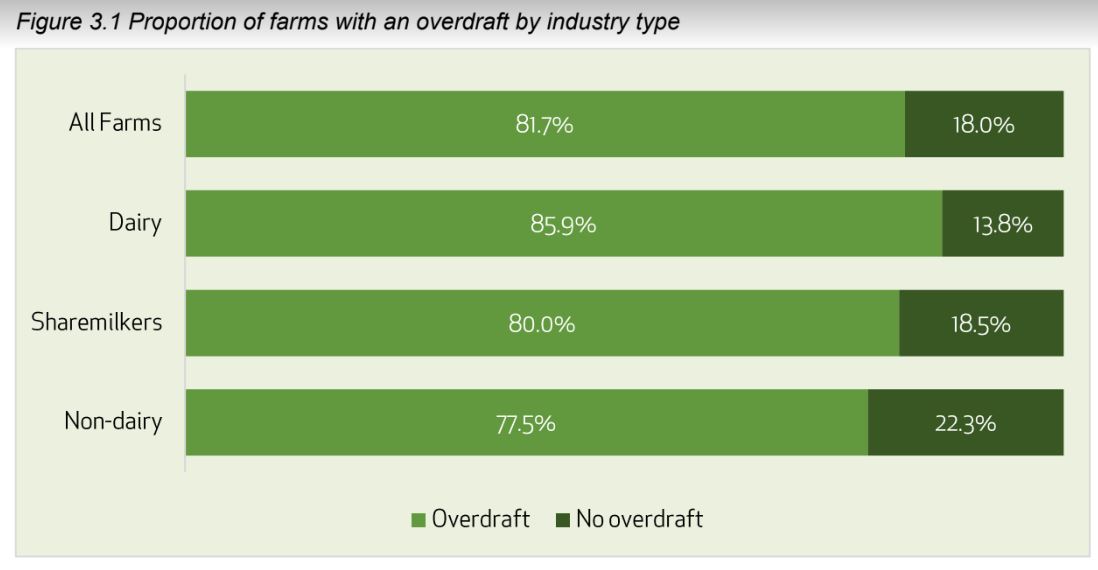

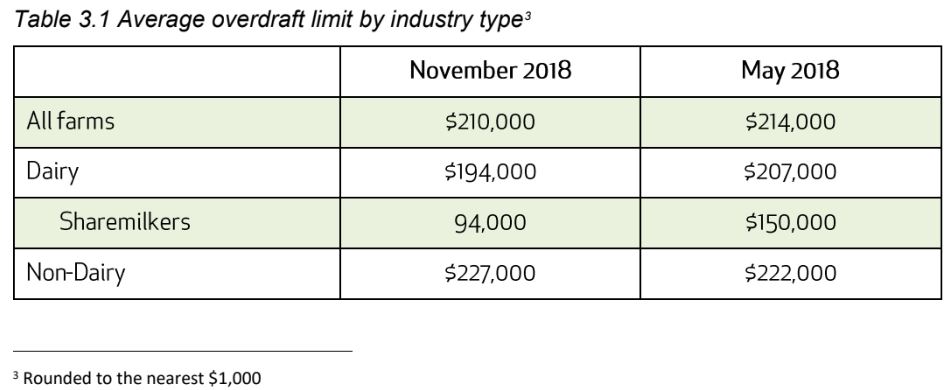

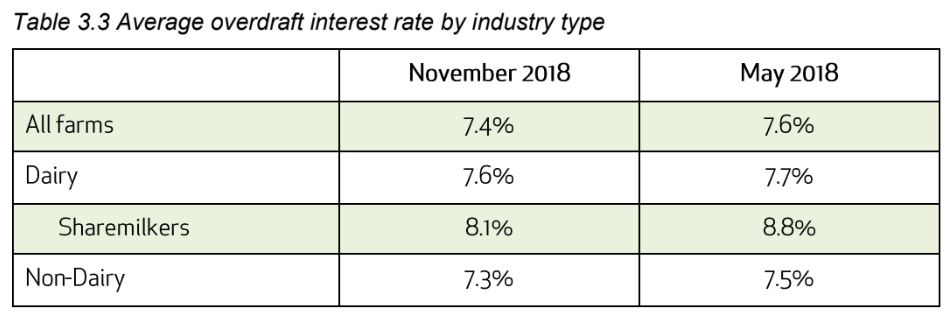

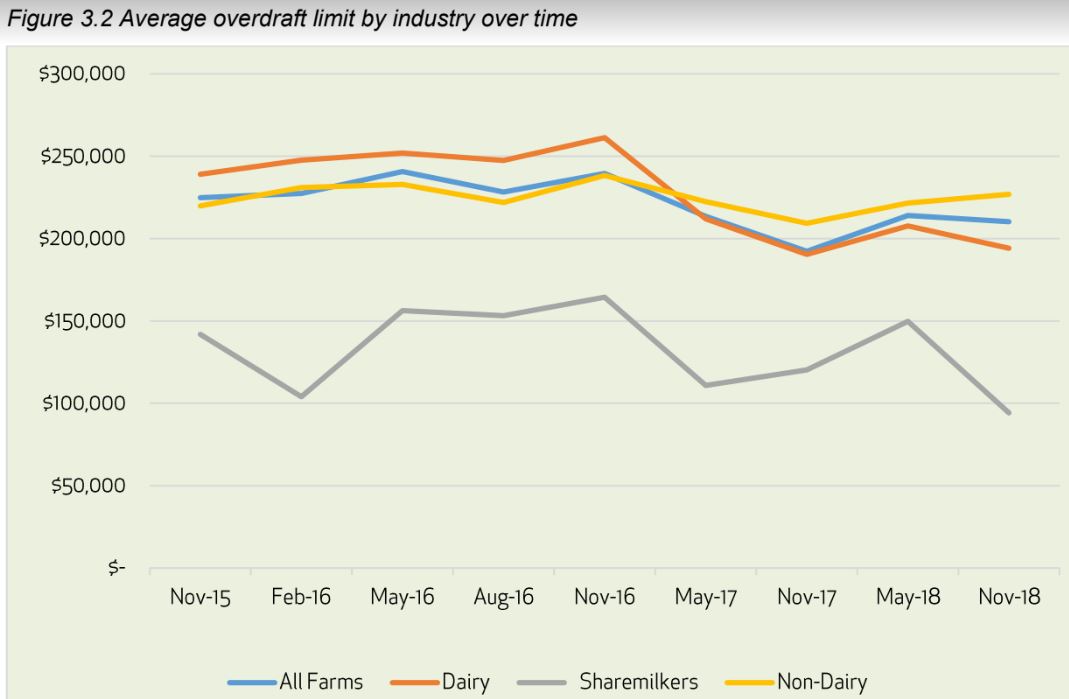

The charts and tables below come from Federated Farmers' November 2018 Banking Survey.

18 Comments

Those numbers are phenomenal. No wonder the farmers satisfaction is waning, they're being milked dry by the banks.

It would be interesting to see what the average ratio of mortgage to total assets is for NZ farmers and how this has moved through the years. My brother in law in Aust is mortgaged to the hilt but this reflects the number of adjoining properties he has purchased over the last 3 decades similar to what his father did. He now controls approximately $80-100 million of dairy, beef and cropping land but all I hear from him is low milk prices. They have 4 children who are all engaged on the farms - I suspect there will be some punch ups at will time.

Are dairy farmers somehow shifting some debt burden onto sharemilkers?

Yea thats a huge change in 6 months, including o/d thats $300,000 plus, 25% increase. Must bea reason somewhere.

No. Sharemilkers are self employed with legal contracts setting out the terms of who pays for what. Initial contracts are usually for 3-5years and if parties are willing, renewed for anything from 1yr - upwards. As the terms are negotiated the robustness/fairness varies according to the ability of the negotiators however there is a standard Fed Farmers contract that can be used, which is the result of Fed Farmers Sharemilkers and the Owners with Sharemilkers sections and their members having input. Capable sharemilkers ROI is around 20-25%.

Thanks for the insights there. A bit hard to make much sense from just 2 data points and only being 6 months apart (so no idea what seasonal influences are driving this). Just seems odd that the average mortgage amount goes in different directions for farmers and sharemilkers.

It's only a small sample - 65 sharemilkers. The report also states that sharemilkers with mortgages decreased 7%. There are >2000 sharemilkers in the industry.

The report that states "....volatility in mortgage rates between iterations could be a reflection of those who choose to take part in the survey......."

There's some big numbers there on all sides, it would appear, and they look to be in better shape than 2-3 years ago, which is a plus. What i find interesting is that they are generally charged more (mortgage rates) for their productive asset where-as we (townies) get charged slightly less for a non-productive asset (our home). Part of me thinks this should be the other way round, but I'm not grumbling believe me. One of the more sobering moments in anyone's life is the day we sit down & work out how much money (in interest) we paid the bank manager over our whole life.

The average dairy farmer mortgagor paid nearly a quarter of a million dollars in interest last year. At $6.50 a kilo milk price that's 38,461 kilos of milk solids. "The average dairy cow produced 4,259 litres of milk in the 2016-17 season, containing a total of 381kg of milksolids (kg MS)," (from DairyNZ) Pretty much 100 cows milk production to pay the interest for the year...

Assume 400 cows and $ 250,000 interest. That's $ 625 / cow - say $ 6.25 / kg solids or 100 kg solids / cow just to pay the interest on the debt out of total per cow production of 380 kg.

That's a really scary ratio !

Costs, Depreciation, Capital repayment and Drawings - Doesn't seem to stack up ?

These are averages - Half better - half worse. Would love to see these #'s by decile of indebtedness.

I think part of the dissatisfaction stems from the reality slowly sinking in of just how long it's going to take to pay off. It didn't seem like a long time on day 1. Debt like we have will stick around for a long time yet...

That could go some way to explaining the high suicide rates for kiwi farmers

Quite worrying considering that is our key export industry

Finance targets the productive sectors of all economies and ours is no different. I do worry about the relative naivety of my Countrymen when it comes to dealing with banks, this sort of protection is long overdue.

I just can't understand the constant bank-bashing. The banks didn't determine the price these guys paid for their farms. The banks didn't force them to borrow the money. The average interest rates look fair. If they're unhappy, they only have to look in to the mirror to see the person that got them into the position they're in.

The banks didn't determine the price these guys paid for their farms. Well they kind of did actually.

Guess you missed banks being trashed for upselling rural customers on complex financial products a few years back.

All the banks have done is set an upper limit of what purchasers could borrow which added to their equity is what farmers COULD pay for a farm - not what they SHOULD pay. Farmers make that decision themselves. My issue is with the influencers that impact on the farmer's thinking. This category includes over enthusiastic bank managers looking to build their lending book to the point of over cooking the figures to get loans approved, Fonterra over promising and under delivering on forecast payouts, unrealistic production goals by farm advisors, peer pressure and family expectations.

Fascinating - farmers are business men. they own and operate a business. Why are they being treated different to other business men who own and operated their own business's? If they are not smart enough to figure they are being ripped off by their bank, or being given bad advice, why are they in the business?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.