The Reserve Bank (RBNZ) says the financial system is in a “solid” position to weather the impact of COVID-19.

Its stress testing suggests banks are “resilient to all but the most severe scenarios”.

“Loan losses for banks will rise materially from current low levels. This could weaken banks’ capital positions,” the RBNZ said in its biannual Financial Stability Report released on Wednesday.

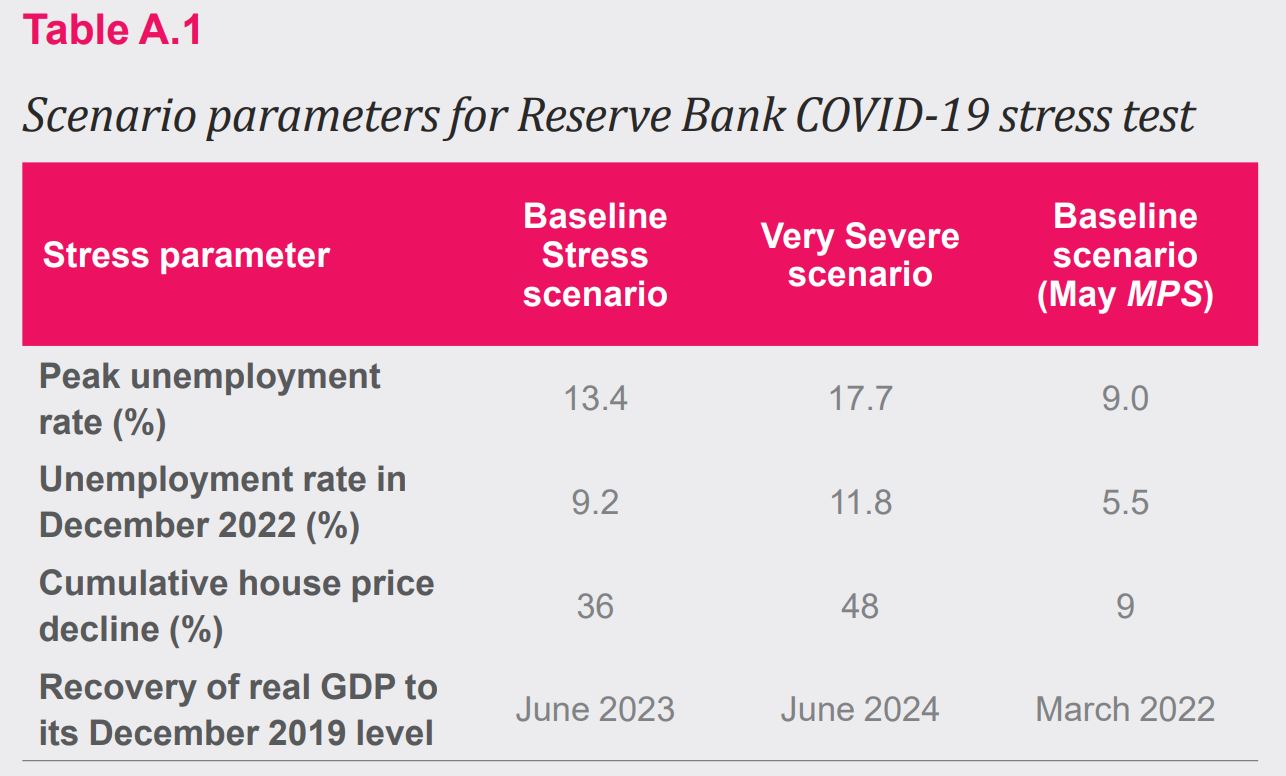

“Preliminary desktop modelling suggests that, under a scenario featuring a larger increase in unemployment and a slower recovery than the most severe scenario published in the [May] Monetary Policy Statement, banks are likely to maintain capital ratios above minimum requirements.

“However, there remains considerable uncertainty about the future trajectory of the pandemic, and how this will affect the New Zealand economy.

“Under severe enough scenarios, the viability of banks would come into question.”

Under this kind of “severe enough scenario” unemployment could rise to 18% and house prices fall by almost half.

In this scenario, “Without significant and timely mitigating actions, banks would fall below minimum capital requirements under this scenario,” the RBNZ said.

“The Reserve Bank is working with industry to better understand the impacts that these scenarios would have on banks and to assess appropriate mitigating actions.”

Easing borrowers' debt servicing burdens buying time

Governor Adrian Orr reiterated: “Banks have a critical role in supporting customers who are facing short-term income declines. Maintaining the flow of credit to financially sound customers also contributes to the long-term profitability of the banking sector, by avoiding unnecessary defaults and disorderly corrections in asset markets."

"Banks have supported mortgage and consumer credit borrowers with options to switch to interest-only terms or defer payments for up to six months, allowing them time to adjust to temporary income shocks without entering into arrears," the RBNZ said.

"As at mid-May, banks have reported granting payment reductions or deferrals on 13 percent by value of total household lending.

"However, by shifting loan repayments to future dates, payment deferrals ultimately increase households’ debt servicing burden over the remaining term of their borrowing. If current pay reductions and elevated unemployment persist for a longer period than expected, households and banks may find that more substantial loan restructuring or remediation is necessary when deferral periods end."

The RBNZ said banks' efforts to ease debt servicing burdens "helps to buy time for both banks and borrowers, on the basis that the borrowers’ incomes will return in the future, and the additional debt burden will be sustainable".

"However, if the present economic downturn turns out to be deeper or more prolonged than banks and borrowers expect, banks will need to exercise caution not to ‘extend and pretend’ if the prospects of full repayment are diminished."

Consolidation among NBDT expected to continue

Turning to non-bank deposit takers, the RBNZ said some firms in this sector entered the COVID-19 crisis in an “already vulnerable position”.

“Some non-bank deposit takers (NBDTs) have low profitability and are operating with low buffers. There has been consolidation in this sector in recent years and this is expected to continue,” it said.

“Resilience could also be boosted by seeking operational efficiencies, asset sales, and additional capital.”

Some life insurers made to increase capital buffers

As for insurers, the RBNZ said, “Some life insurers have also been operating with low solvency buffers, some of which have been adversely affected by falling interest rates. In the past six months the Reserve Bank has applied licence conditions to these insurers to require stronger capital buffers, to mitigate the impacts of further reductions in interest rates.

“More generally, COVID-19 is likely to affect insurers in a number of ways. For now, containment measures have been effective in limiting the disease outbreak in New Zealand, reducing the risk of significant life claims for insurers.

“However, a number of insurers are exposed to investment losses as a result of movements in interest rates, bond spreads and equity prices. Further, some providers of credit insurance appear vulnerable to a significant increase in unemployment.”

155 Comments

Safe as long as house prices are going up. That is the model isn't it?

I'm struggling with the concept that more debt is the answer to ones inability to afford their current debt. Perpetual increasing house prices...the sacred cow of NZ along with universal Super.

Bit like alchoholism...its easier to keep drinking in the short term but harmful in the long term vs going sober and suffering in the short term in order to prosper in the long term. Read the comments on this site - people don't want that short term pain and we're avoiding it at all costs (including the stability of the whole system).

As long as the bubble doesn't burst during Orrs watch then whats the problem? JK had exactly the same idea. Disgusting and should be criminal.

Older folks who rely on their savings get pretty antsy when figures of responsibility sacrifice their savings to enrich a few: http://www.stuff.co.nz/business/money/3106541/Angry-investors-rough-up-…

Wow you have been saving that link for over a decade.

Exactly....

That's the problem when the western banking system is run by the gangster elite. Once they have theirs hooks into your country, its very hard to extract them. He who controls the money sets the rules. Lebanon is but an example of what happens when you become too indebted to those crooks; aid and abated by ex politicians who have been nothing more than plants to sell their wares. All these plants have been doing is pedaling a private tax system for the global elite, who could never hope to spend what they have already.

NZ inc has had an income deficit on international investment for 30 years or more, and taking on more debt sponsoring overseas interests is only going to compound the problem. I would have liked to have seen the reserve bank print money direct to the local people, but you can be sure this will be met with trade embargos from the gangsters pulling the strings of the US government in response.

The only solution is to invest local, creating more competition in the essential items, and spread your business with other countries wider; so you are not dictated to by these big bullies. Any smart business person will tell you that. Unfortunately its going to be a long road to achieving this; no thanks to Roger Douglas incompetence and Jonkey arrogance who have pampered to the banking elite.

My house could be worth $0 and I'm still OK. Remover my super and I starve. Until I apply for some other benefit. Start Super later, reduce the rate being paid, remove winter heating allowance and keep on applying income tax however keep it universal otherwise the accountants and lawyers will have a field day and the govt will end up saving very little.

The lesson of universal Super is the good sense of universality - it should be applied to child benefit. Along with WFF and accomodation benefit, the means test to child benefit is distorting how people choose to live to the detriment of our children.

You are basically advocating for a UBI without saying as much. That may actually happen as the gubbmint will likely have to continue the wage subsidy scheme for another 8 weeks... then another 8 weeks... then another 8 months... then another 8 years...

Well if i thought it could be done I would go for a UBI. The small experiments have not be greatly successful. Think of it in a different way - we all of us have provided by the state a health service, an educational system, a massive collection of universal access parks, beaches, roadways, a justice system, a corrections system and a defence force to protect us one and all. That is like having a generous UBI.

I might further means test Super (nb Income tax is already applied) if I thought it would work. Just as I might have low GST on fruit and veg but higher on alcohol and sugar - however I've written computer code for varying rates of GST - (a) variable GST is a recipe for rorting (b) who is entitled to determine sugar = bad but cabbage = good - I prefer autonomy.

Your are right in your first paragraph. Tax expenditure in theory is UBI, you pay for stuff collectively that you probably couldn't afford by yourself. You then choose whether you use it or not, regardless it is there if you need it.

The benefit in theory, is that all current welfare payments are removed, everyone gets a UBI, and there is a net saving to all. But I see two problems

1. Much of the current welfare is more than any potential UBI.

If I get $750 in current benefits, but UBI is only $500, I am not going to be happy.

2. Who is left to pay the tax?

If I pay $500 a week in Tax, but get $250 a week in UBI - who is paying the difference?

The only way UBI can ever work is if you tax the companies to ensure you have enough to pay everyone a UBI high enough to live on (if required). Which is akin to aknowledging the current system is not just corrupted, but utterly shattered.

Everyone is struggling with that except the folks who set our monetary policy apparently.

You'd be mad to have any significant amount of cash in a bank account right now.

Housing absolutely must remain severely unaffordable for our Banks to remain solvent

Headline..."should" be ok.....in "everything but the worst scenario"...…...we should be good, everything is peachy right now.....If those words by RBNZ don't make you sweat...….

Quite.!?.

Quite relevant.

Quite apparent.

Quite appalling.

Quite likely.

Quite significant.

Quite substantial.

Quite obvious.

Quite disastrous.

Quite like 1987.

More like 1929 on steroids

Why here, why now.

I suspect he has picked up on the change in thinking, change in heart of the banks. Change in tune from 8 weeks ago.

For more context hear what these same banks are saying & doing in their home market.

The real world unemployment rate is already over 18%. I think the wage subsidies make sense but a large number of these people will not have jobs to go back to or will lose them shortly after the business that employs them fails to re-open successfully.

I have been looking at businesses to buy and the pre-covid books are just awful. People have clearly been running their businesses by borrowing against real estate to make things work.

There is no getting away from the fact we were in a slow-down pre-Covid. Many will have used up cash reserves or chipped in their own money already, before this even reached NZ. The worst case scenario is that not only do businesses fail, but people who put more of their own money in pre-Covid to get through a quiet time no longer have the capital or credit to start over again.

You are correct, and the real life evidence 860 people apply for 30 supermarket jobs. The unemployment rate is going to 18% plus...GR is all talk when he says they will create jobs, it's just like they going to build 100k houses. The only stat they are interested in is the covid free days, so they can go to the WHO and say look at us little old NZ we had 30 days in a row with no covid cases, we had to reach 20% unemployment to do it and totally wreck our economy, but look at us, look at our stat.

The US has about 25% unemployment and they don't have COVID under control so at least in that respect we a more positive outcome. But yes I'm quite worried that unemployment will rise and government intervention won't be sufficient to pay everyone's bills/mortgages/rents - and all roads lead to Rome (the banks and mortgage debt).

There is a difference - a really determined govt can build 100k houses but it cannot do much about productive jobs. OK it should do what it can but don't expect success except at propping up a few businessmen and creating jobs where half dig ditches and the other half fill them in.

Have I got a deal for you... It would be interesting to see how much of the real economy is propped up against housing - making it part of the unreal economy, or mortgages.

A lot of friends who own businesses were barely wiping their behinds pre covid, they are really struggling now. There are a lot of breadline lifestyle businesses out there, and everyone who owns one thinks they are worth a mint.

It's really odd talking to business brokers. They want you to hand over seven figures for something that is losing money and they act like that is normal.

Every time I see that picture of Orr I see flailing dreams of affordable home ownership and desperation to keep people borrowing at any societal cost

Well luckily for banks, they don't pay out on term deposits anymore, or not in amounts that matter, so once they cover the CEO's salary package they're fine.

ANZ's TDs rates right now are a disgrace.

There needs to be a savers revolt.

We're just catching up to the rest of the world aren't we wrt TD rates?

Move money to kiwibonds if you don't like the banks - but then you're only getting 0.75% or so.

Indeed. Savers rates in the UK are trash. However, the rest of the world also has deposit guarantees. Now that NZ banks are also earning pittance, you may as well stick your savings somewhere safer for a while. That's what I did.

Thanks for the advice - I have an old moribund account in Scotland and an honest French son living in France with various french bank accounts.

last time you checked (a while ago) he was honest!!!

Might have to do the same with my son in the UK and bear the currency risk. Asked RBNZ for official information about "Banks: Liabilities – Deposits by sector ($m) - S40. Which of these deposits is NOT subject to claims under an OBR event?" Pre-condition was it was readily available so I didn't have to cough up some unknown amount for the research. Withdrew the request a week later. Trying to do my own research from docs I can locate on RBNZ's website.

I'm yet to figure out if non-citizens of countries where bank accounts are held would still be covered by a deposit insurance scheme. Does anyone know?

Absolutely correct. That is what I have been doing too.

"ANZ's TDs rates right now are a disgrace."

Most people enjoy sunny days, as they get to go outside and enjoy the weather. On days when the weather is raining, some people choose to become unhappy and complain that it is raining. Others choose to adapt to the changed weather conditions.

In the military, there is an adage used - "adapt or die"

Many people in NZ are facing reduced household incomes (through lower salaries, fewer hours worked for wage earners, lost jobs, etc) and are being forced to adapt to changed conditions. Those who are relying on incomes from their investments might also consider choosing to adapt (however some will choose to complain, which is really unproductive, and doesn't change the situation).

I'd love an alternative. I can't find what I consider a sane place to put money anywhere on earth. This really has been the Everything Bubble.

Without all the government intervention, I wonder what our unemployment rate would be? Based on the US, they look like they're around the 25% point so I could see NZ matching that this year.

And that figure is well above what Orr is saying banks can handle - matched with a 50% fall in house prices (a possibility in my view based on previous property bubbles around the world).

I have money in TD's with NZ banks so will be watching this space closely this year and may move those funds into kiwibonds until the dust settles. Made a risk based assessment a during lockdown and moved some funds into kiwibonds then...perhaps more to follow.

Valid thoughts.

But all of this 'move money about for safety" etc could be so easily overcome if any tax-paying NZ citizen could open plain vanilla; at call, savings account with the RBNZ.

The RBNZ would get some liquidity to refinance the banks, and our funds would be safe to meet future tax payments etc - or just move back to a commercial bank(s) when 'things' stabilise.

Comes back to my view of why do we need commercial banks again? Other than to pay high private sector wages?

We need them so that all the profits can head offshore and buy yachts and ferraris ?

Well, if I take a perfect market view: so that we have competition driving innovation and new banking products & services......but that almost seems like sarcasm given the near-oligopoly we have in NZ.....

Totally agree and yes, we need a drop in house prices of 40 to %50 to get things back to where they should be. Look what Ireland did after the GFC, just let things melt down slowly over a 4 or 5 year period. Then house prices will be at affordable levels again. What worries me is what a lot of people on here say, is that the RBNZ will do whatever it takes to keep things the way they were. Isn't it about time we just all take our medicine.

Ready to start the next bubble!

Is there another property bubble? The housing market in 4 charts

https://www.irishtimes.com/business/personal-finance/is-there-another-p…

Thanks for posting

Next month will be interesting, the 12 week subsidy runs out mid June. Will be some lay offs then.

Been extended 8 weeks, no?

Yes . From the RBNZ May report

The largest fiscal response has been the Government’s Wage Subsidy Scheme, with more than $10.7 billion having been paid to employers by mid-May. To date, the scheme has helped to cover 12 weeks’ worth of wage costs for 1.7 million employees. An eight week extension to the scheme is available to employers whose revenue remains low following the move down from Alert Levels 4 and 3.

Have to show a 50% revenue loss. Many businesses even with a 10-20% loss are unprofitable & they won't qualify.

We showed a 90% loss yoy in April, but that has bounced back this month. Compared to a lot we are in a priveleged position. Customers that I have been helping with their financials for the government sponsored loans are struggling to get anything out of the banks, everything is stacked against survival of so many small businesses.

It is not the unemployment rate but the under-employment rate that matters. Way back last year NZ had lowest unemployment rate for decades but we still have over 1 in 8 looking for more work. You only need to work for one hour per week to be registered as 'employed'

What is so heretical about an overvalued market trying to correct itself?

Oh don't you DARE talk about free markets to these free market economists... hang on...

A fifty percent drop in house prices would be lovely.

So long as we can keep it that low, yes. A temporary fall to allow a new cohort to enrich themselves would be a disaster.

That's why we need a CGT and other changes to the way the banks lend, especially to investors. If the correct changes are made we could keep the growth at realistic levels. Just need someone with big roundies to do something about it. But I'm not holding my breath though.

Yeah! Bring in a CGT as soon as possible! I'd love to be able to claim a tax credit for the declining value of my assets. Soften the blow and all. :-)

I can't imagine they would make it retrospective.

Who said anything about righting off loss's? Just a tax on the gains from the proponents. You thought this would be fair? Even in the USA where theoretically they have a more open market system (although not in the last few weeks of buying up the stock market)...you can only write off $3000 of capital loss's against income in any one year, but they are quite happy to tax the entire gain in the year it is realized, possibly bumping you up to the highest tax bracket at the same time. If you have a significant loss it can drag on for years before you get to write it all off. This is on personal income..don't know the corporate rules.

And this is where they will waste the crisis.

A fall to the level he is saying is exactly what the price could have been prior if the non-value added speculative rentier monopolistic waste was removed from the system.

But to whatever level it falls to, all they need to do is remove the monopoly restrictions afforded to land bankers and council both in the way of land restrictions, and the restrictions afforded to councils for consenting and infrastructure provisions.

This would set the price at its value-added level and prevent any speculative behaviour going forward.

Your comment is exactly right. The generational property is the only way game, is so ingrained in so many that barring an absolute tear it to the ground blood bath, I cant see it happening. Unless they all lose their real jobs and there is are mas mortgagee sales.

It would totally financially ruin most of the millennials who had to put off buying houses for years until they were more established in careers. But then again, they have been acceptable collateral damage so far, why stop now? If you think our suicide rates are bad now, you should see what a 50% drop in house values would do.

I agree with you but there may be no choice in the matter. The other point to remember too, is these people bought into the ponzi scheme, or should I say, were sold the scheme.

or...alternatively, they were just buying houses to live in? Young New Zealanders have already had to stretch low wages to meet massive deposits on hugely inflated house prices through no fault of their own. At each and every point they got told 'tough, that's just how it is'. There is no moral reason they should bear the brunt of negative equity in the event house prices collapse.

or... they were told by all and sundry that house prices never ever fall, only go up.

I don't see the problem, those who bought a house to live in will still have the house to live in and the mortgage that they agreed to take on.

There has to be consequences for overpaying, even if only to serve as a warning to others.

Why should those who chose not to drink the kool aid bear the brunt of the housing bubble being kept inflated?

Yes from me

Funny, there hasn't been any consequences for the people and massive profit-taking that got us into this mess. I guess that's how it is though. Someone has to be taught a lesson, there has to be someone you can wag your finger at, as long as you have a seat when the music stops, who cares what happens?

Glad to see you find some positives in the wave of suicides, divorces, family breakdown and financial ruin that will hit my generation harder than most others, for the heinous crime of buying a family home to live in.

It sucks that some people got sucked in. It's not like I haven't been warning them as long as I've been on this website.

But at the end of the day it was their choice and they can still sell now if they choose.

It's my generation too. Plenty of us refused to overpay, while others kept bidding up the market.

I appreciate that people have 'refused to overpay' and have had the options or flexibility to pay rent instead, but this correction has been long overdue and wasn't on the cards until a bat virus sprung up. You could have conceivably been sitting on the sidelines for another five or ten years - no one was showing any real interest in reform, the party was just going to keep on trucking no matter what. I would say expecting people to put off something like buying a house for a potentially infinite amount of time is almost as unreasonable as letting house prices get to where they got to. Yet here we are.

Seems to be a financial crisis and major recession about every ten years. This one came a touch over schedule.

It's a bit like the property clock ;)

But I still think they will engineer for house prices to not fall much.

Most of the generations alive right now, are entitled or soft for one reason or another. We're arrogant enough to forget that for the most part life is a hard grind. I could give two hoots about any generation other than Generation Alpha who are born starting around the early 2010s. They're the ones who are going to bear the brunt of this, and will never know anything different other than poverty, austerity and war like we've never seen before.

GV 27,

A reminder, that all owner occupiers (some of who are highly leveraged) are free to choose to act today regarding their owner occupied house:

1) hold on to existing house

2) sell existing house and rent accommodation (and potentially buy at a later date)

3) other?

Those owner occupiers however are not free to choose the future consequences of their choice.

FYI, a property investor sold their property last week and received a price that they were very happy with.

I sold my 2 bed rental unit one week ago, in Auckland city, and it sold under a multi-offer situation, and price achieved was inline with the market pre lockdown.. market could take a while to correct..

I agree with you GV 27 - its just terrible that so many have been put in that position. Foolish, short term, self interested behaviour in my view that was always going to lead to this type of situation.

Yeah but what's worse? To have 50k of them thrown under the bus now ending up with say 10% negative equity on average, or once the can is kicked down the road a bit more, have 100k with 20% negative equity on average? The band aid needs to be ripped off and the wound disinfected or else the limb needs to be removed later.

By all objective measurements, housing in NZ has been in bubble territory for a decade or so, getting much much worse in recent history.

When you look at our housing bubble in inflation adjusted terms, it makes the US bubble look like a baby. I lived through that when I was over there during the GFC and it caused a lot of pain. What we could see could be multiple times worse.

Both comments above are spot on, couldn't agree more if I wrote it myself.

"If you think our suicide rates are bad now, you should see what a 50% drop in house values would do."

This is the reason that a number of commenters on interest.co.nz have been highlighting the elevated property price vulnerabilities and elevated property price risks to enable owner occupiers buyers to make a fully informed decision.

People can choose to ignore those warnings, or people can choose to heed them. That is entirely their choice.

Given we have been waiting over a decade for this corrective event, how long should one have waited until it happened? What's a reasonable time-frame, do you think, for people wanting a stable roof over their heads for things like families, all the while paying rent that can't be gotten back once it's gone? 15 years? 20 years?

Sorry, send the bill to the people who created this mess. I've had enough of being the wrong age at the wrong time gag, it's getting pretty old.

" I've had enough of being the wrong age at the wrong time gag, it's getting pretty old"

It is terrible that some recent owner occupier buyers have chosen to purchase at high prices recently.

This is nothing to do with age, or the year that people were born in. There have been recent owner occupier purchasers who have been upgraders - they are older, yet they face the same potential property price risks as younger owner occupier buyers who purchased recently.

This is all about people making a life choice. For instance, people may choose to take a job, only to find out that they don't like the job and it was a bad choice for them. Some people can choose to change that situation, whilst others choose to stay.

Some recent owner occupier buyers chose to purchase a house at high prices. People can choose to change their current circumstances or they can choose to stay in the same circumstances. It is entirely their choice.

Everyone has made some poor choice at some point in their lives. It is how they choose to deal with the situation that they have got themselves in that really matters.

Previously, people had a choice about whether there was meaningful reform in land supply or urban planning or taxation or migration or all these other wonderful things. They chose not to do those things. They managed to feather their nests at the expense of the people who came along after, who didn't have input into those decisions.

Those people are insulated from any consequence. Funny how that works. Yet suddenly, when the mess they created comes to a halt, it's suddenly about choice and how people are the arbiters of their own destiny, and the choices of people born into a set of circumstances they had literally no control over.

I would feel more charitable about this had I not endured years of lectures from people who managed to buy houses for less than what I had to stump up as a deposit about how it was just a question of 'hard work' or 'less takeaways' while houses went from 4x household incomes to 9x household incomes. These same people, by the way, are now assured a non-means-tested pension for turning a certain age.

So with all due respect, now five years and counting older than my parents when they started their family, and still with a student loan, and having watch some friends spend less than 12 months in a rental before their landlords sold out from under them, this is entirely about age, and the idea that people enriching themselves at a future generation's expense is something that future generation is just going to be OK with and there won't be any consequences whatsoever.

But sure, choice or something.

GV 27 - exactly. And if you hit said generation up about this behaviour you get the 'oh that's nice dear. Do you know how tough it was in our day?' response while they sit there in their million dollar home receiving superannuation payments.

I am taking this personally, I_E, bear that in mind. But that's only because while I am unlikely to starve to death on the streets or be totally financially crippled, some of my friends will not be so lucky. Statistically, some of us will not make it out the other side alive. I am scared for them and NZ as a whole. It is sad that this is a reality in NZ, but it is what many are facing. Some will be wondering why suddenly the honus has fallen on them to make sound, selfless choices that their fore-bearers got away with totally ignoring to their own benefit. Some will be angry about that.

I got angry about 2013-15 period when I could see what was happening especially just after living through the property bubble/mortgage crisis in the US. The thoughts that regularly go through my mind are ‘how could be so continually stupid to put our country in this position?’ But then you look at all the inputs and it’s beyond any individual factor so there is no real point in playing the blame game or getting angry. The ignorance and denial frustrate me but what can one do?

I can feel your pain. I understand why you are so worried and bitter about this. I'm in my early fifties and haven't, sadly, made huge gains out of property due to relationship issues etc etc. I've been saying to anyone that would listen for the last 15 years that the existing system is broken. No political party has had the balls to do anything about it in those years. It's been apparently, political suicide to even mention a CGT or any other measures to soften the market. If someone had at least done something we wouldn't be where we are today. The elephant in the room is immigration, its been out of control over the last decade. Just look how quickly we've gone from 4 to 5 million people living here. Some thing some how needs to be done. I don't have too many answers but like you, I'm worried where this country is headed. That's why I've mentioned earlier that we need to take our medicine now, yes, I know that will hurt a lot of people, I will feel some of that myself by the way. If we don't take it now, when will we take it, when house prices are 15 times the household income. I know there will be a lot of collateral damage along the way but isn't it better now than in 5 years time. I don't know really, I don't have the answers. I just wished that the government would take advice, even from some people who write here. They seem to have a very good understanding of how it all works. Better than I do anyway. I just don't know how we get the powers that be to listen. Maybe it will come to marching down to parliament in our tens of thousands to make them listen. I really wished I had an answer.

And yet people are still saying how amazing Jacinda is. She may have bought the 60+ crowd time with COVID by locking down the country and saved a few folks who were at the end of their best years. But she's thrown everyone under 50 under the bus to do it. There'll be thousands more deaths thanks to poverty because of her. And they'll be young healthy people who had their whole lives ahead of them.

Yeah. This. Kiwis are so busy gushing with slavish worship for Jacinda they don't yet realise the consequences of her virtue maximizing strategy. Idiots.

I absolutely hear you and like many other commentators have been yelling at anyone and everyone that housing is out of control and will likely cause massive social and political upheaval. And that looks like it's just around the corner...

You are obviously a smart one GV. Get organised, take the consequences, but when it happens, take to the streets. I really mean that, I will be standing right beside you.

If the system has shafted a whole section of society, there will come a reckoning.

they can cope with everything but whats coming.

Yes. Not that long ago they told us they had stress tested the banks and they were sound, now they are adding a 'BUT....' to the statement.

Comment of the month.

I could not help but laugh.

scarfie...well, I laughed and gave you a thumbs up....and then started to sweat a little....RBNZ comment from headline above .....Banks 'should' be good under 'all but the most severe scenarios'.....good to know we are not close to that severe scenario at present...……..

"Banks have supported mortgage and consumer credit borrowers with options to switch to interest-only terms or defer payments for up to six months, allowing them time to adjust to temporary income shocks without entering into arrears," the RBNZ said

There is no TEMPORARY in this condition. Allowing them to kick the can down the road and cross their fingers.

"However, if the present economic downturn turns out to be deeper or more prolonged than banks and borrowers expect, banks will need to exercise caution not to ‘extend and pretend’ if the prospects of full repayment are diminished."

Banks need cut there house valuations by a hell of a lot 30% to 50% and decrease the borrowers income hard as well.

Under this kind of “severe enough scenario” unemployment could rise to 18% and house prices fall by almost half.

So Orr is suggesting that house prices could fall by approx 50%. And that is not a worse case scenario.

So where is the so called RBNZ "stimulus" failing to stimulate?

Liquidity trap in my view. More debt can't generate the earnings required to service that new debt created. Death spiral...

I can see unemployment at 18%, I can't see house prices halving. The govt will never stand for this & will keep printing money in larger & larger quantities to keep housing from falling in value.

What happens if we keep printing money donny11? Inflation...then what happens if we have inflation..? Higher interest rates? And what happens if we have high unemployment, high unemployment, no or negative wage growth? We'll we have stagflation. And how do we service high debt with low wages and high interest rates?

Inflation doesn't necessary cause higher interest rates if you go down the financial repression road. Not that I recommend this. But you are right, NZ is going to face "monetary system" problems in the medium/long term.

Are you saying the Reserve Bank will now opt our of inflation targeting now that it might impact house prices?

Can't have it both ways in my view.

I would bet money that's exactly what they do.

Absolutely agree. If inflation picks up, the RB knows the risk, so will let it run wild for a few years. Reason? It's the inflation we should have experienced from a decade of dropping interest rates. "Pent up inflation" will totally be a thing.

We'll end up with millennials with $600,000 mortgages paying 15-20% interest in a few years time.

This will never happen. The system now survives on low interests rates. It dies without them. In an inflationary environment interest rates will naturally rise to compensate for inflation. This is not desirable as it will cause economic collapse. So what you do is "force" private money to buy government debt to keep interest rates low. For example in an inflationary environment of 15% no one in there right mind would want to own govt bonds that pay 2% as you lose 13% per year. However the govt will issue a directive that all kiwisaver funds have to buy govt bonds. That's 56 billion to buy their debt. If you complain they go "listen buddy we are doing this for your own good, you know how volatile the stock market is, we are helping you out by directing you to buy our nice & safe govt bonds". They will then look at the superannuation fund of 44 billion & make them buy govt bonds also & so on and so forth. Hence you go down the road of financial repression.

Yeah, but inflation affects income as well. So they will be earning 100k a year each instead of 50k before too long. Don't make the same mistake as the boomer argument of "But but but in the 80's we paid 15% interest rates" without seeing that they also had comparative pay rises. Sure it's temporarily painful, but it will inflate away the debt. Of course you need to have these people in jobs, or be paying off their mortgage for them via a Universal Debt Reversal Income. People have mistaken a UBI for this, the D and the R were accidentally squashed together, it's actually a UDRI. :-p

Not necessarily under stagflation. Rising prices but stagnant wages.

They won't be able to long - otherwise we'll have a repeat of the 1970's and 1980's and the baby boomers always tell me how bad that was...

Yeah my folks could only do a 3 bedroom extension rather than a 4 bedroom extension while servicing their mortgage at 20% on a salary of $20000 in the mid eighties. Horrible I know.

Which suggests if they're just going to end up giving people free housing like that then they may as well build a bunch more houses and give a bunch more Kiwis free housing too.

Well ASB "ASB expects 6 per cent house price decline, rapid ... - www.nzherald.co.nz › business › news › article

Apr 27, 2020 - "We expect the unemployment rate to rise from 4 per cent to just under 9 per cent and wage growth to slow sharply....

If banks expect a 6% house price decline from unemployment increasing by 5%, 18% unemployment makes for a 15 to 20% drop in house prices possible..

I live in a million dollar house. I'm quite content to live in the same place but worth $500,000. Of course if I was a property investor I might feel differently but who cares about them?

Sounds comfortable... but if you could sell your house for $800,000 and buy another one next door in 3 years time for $500,000, wouldn't you feel more content?

Yes. I do have an investment property; it is the house next door; it has a mortgage on it. And my economic self was desperate to sell it last year because even I know a bubble when I see it. However the tenant was pregnant and wanted to stay. And she is my step-daughter. Birth was in Feb - what you couldn't call a million dollar baby but certainly a few hundred thousand. Cute baby.

Good on you Lapun!

Does increasing the minimum wage help?

Might increase unemployment - businesses wouldn't be able to keep as many staff on their books.

I think it's really irresponsible not to have a bank deposit insurance scheme in place now, and for more than the $50k being looked at. The very severe (and the next level which they don't show publicly) scenario could very well play out. Perhaps the govt + RBNZ see it as less expensive to pay out for mortgage payment relief for an extended period, rather than have to bailout out a bank or two, if they get into trouble from being over extended in the mortgage market - which they surely are.

What do you think any Deposit Guarantee payout would be worth if it was ever called?

The exchange rate would be close to zero, so shipping whatever nominal amount you get will be worthless.

Moving it to another bank would be just as pointless.

What is it that you think you could do with any 'money' dished out under a payout situation?

(ie: Would you take money from someone in exchange for anything if it could be devalued to zero by a banking failure?)

No major bank with an RBNZ license is going to 'fail'. Whatever circumstances they might find themselves in, would be dealt with by a merger or acquisition.

The point is, every other developed economy has substantial bank deposit guarantees (including Australia with $250K guarantee per bank - same banks!). Putting aside what it would be worth if ever called, it would stop a run on the banks as the news breaks of trouble afoot. We do not want that, ever.

I've already run to Bitcoin. Even if it goes down to $5K I can hold it long term and not lose the asset value of my savings. It's a value store system designed for the very circumstances we're in now.

Currently the merger or acquisition would be after an OBR event so depositors would still take a haircut. I'm fairly certain this is what happened to a Cyprus bank after the GFC. The mostly Russian depositors took a haircut and some Greek mainland bank took the Cyprus bank over. With a deposit scheme of $50k per bank and you ran out of Banks, say 6*$50k, would result in any deposits over this total subject to a haircut.

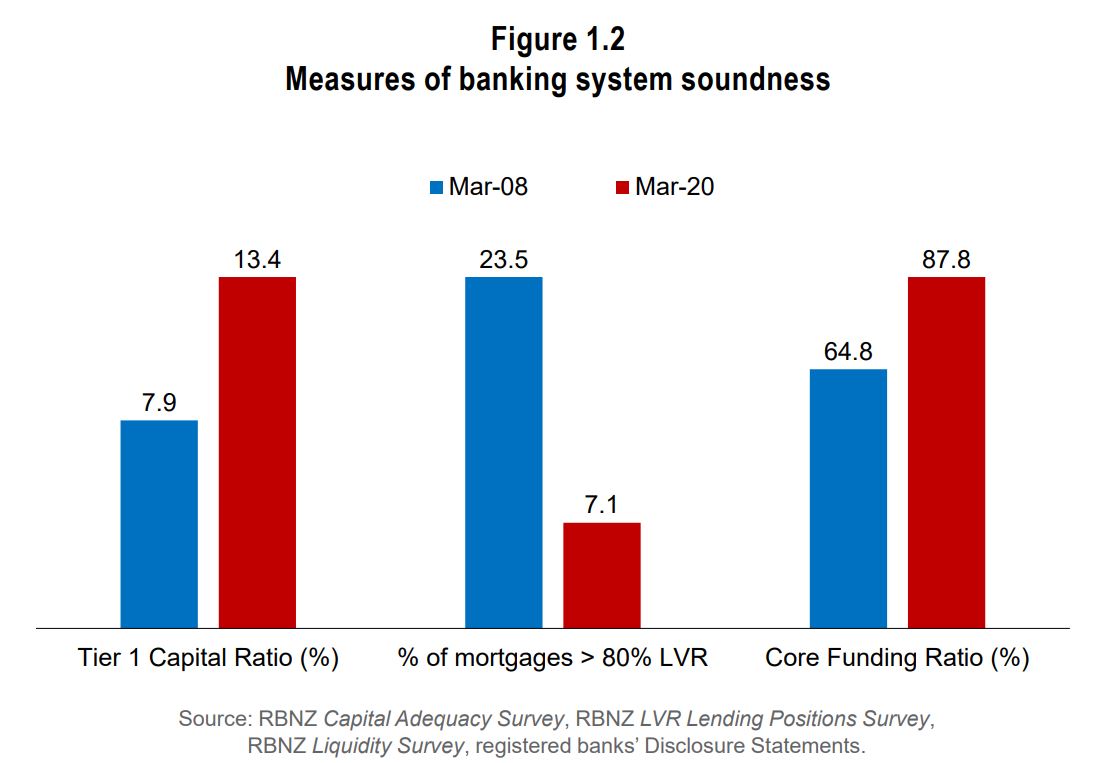

Without any sense of irony the RBNZ has undertaken actions to undermine measures of banking system soundness in order to save banks and their customers.

{kind=link}

..the Reserve Bank has delayed increasing capital requirements, relaxed rules on how much of banks’ funding needs to come from long-term sources, and temporarily removed restrictions on low deposit loans. This helps to free up banks to continue supporting customers

Yes, it's completely bewildering. Just like the LVR removal which is marketed as being a major factor in ensuring the soundness of the financial system.

Now on all the property spruiker blogs/emails what do you hear? "With the removal of the LVR limits, we expect house prices will take off again!"

RB is asking for disaster. Don't worry though, Orr will leave just before the writings on the wall...

Is this the same Orr bloke as what was, only last year, all fired up to double (IIRC) banks' capitalisation to 'cope with a 1 in 200 year event'? But is now saying - move along, nothing to see here, everything's a Box of Fluffies?

Conspiracy theory alert: are we in fact being addressed by an animatronic facsimile, and the real Orr is locked in a vault at 1 The Terrace?

"'cope with a 1 in 200 year event'"

Is the current economic environment, THE potential one in 200 year event?

"Even accounting for an expected recovery in the second half of the year, this year’s projected decline in annual GDP is the largest in at least 160 years (figure 1.1)." - page 2

Yes exactly.

To cancel the more stringent rules which were going to be put in place and to allow the banks to run at lower levels of capital adequacy right at the beginning of a downturn where the trajectory is completely unknown seems rather ummm, imprudent to me.

We all understand that existing morbidity issues make you more susceptible to CV19 complications.

We all knew our economy had existing morbidity issues prior to this and was not fit for purpose, it was hardly surviving in the good times.

One more bat favoured wafer Mr Creosote. https://www.youtube.com/watch?v=gdJcWvxEULQ

No one has even mentioned the elephant in the room re insurance - income and/or mortgage protection.

A lot of claims about to come in for that.

I mentioned this in a thread a few weeks back. Love to see some analysis or a story on it.

And a lot of column inches about how insurance providers won't pay out for whatever reason...

Wow spoke about 20% unemployment and 20% house price falls months ago and got nothing but criticism and DGM comments. How things have changed, now I'm looking like the optimist on here ! Little doubt the effective unemployment will hit 20% now before Christmas if its not there already. Cannot imagine 50% house price falls in New Zealand so sticking with the 20%. By the time the banks are in trouble we will be like Lebanon, there will be riots in the street and people throwing petrol bombs, its not going to happen. What could come out of this is a new digital currency where everything is "Reset"to a new value.

A new currency backed by at least partly by gold. It has to be backed by something that is solid, no one has any trust in the banks.

Or it has to have the mechanisms that ensure it's management is out of our hands - scarcity, distributed open ledger, private keys to prove ownership, quantitative hardening, highly portable, easily transferable, globally accessible, and pegged to something real - like the cost of energy.

Oh, that's Bitcoin.

I will still be able to access my PM's in a sun flare or an electromagnet blast.

Pick which news story is correct.

China, Russia and reserve banks are stacking PM's.

Or

China, Russia and reserve banks are stacking Bitcoin.

???

Ah yes, because in the event of a complete electronic meltdown the banks have all those massive warehouses full of paper records and aren't reliant on digital info at all.

So everything except PM's could get potentially get smashed. Even more of reason to go PM backed.

You are all missing the most important part!

"In this scenario, “Without significant and timely mitigating actions".

Money printing, negative interest rates, helicopter money etc etc.

lol, exactly.

Translated into simple english I am pretty sure it reads as: "as long as we do everything possible to keep them afloat they will be fine"

This could be phrased alternatively as: "if we don't do anything, then they are stuffed"

My thoughts: https://www.youtube.com/watch?v=--hMJPUBwMc

I'd imagine that part of the reason that the banks have a higher level of so called "soundness" from 2008 and 2020 are changes such as the new rules regarding breaking term deposits. 28 days I think is the shortest notice period that the banks now allow. And also to reduce the interest payments on so called "savings" accounts which discourage people putting money there.

NB. These savings accounts now have interest rates very similar to kiwibonds..

Not entirely true you can break at even shorter notice than 28 days with a House Sale & Purchase agreement, banks love you to take on more debt.

and the 30 day rule is exactly why I have considerable money in cash right now. The markets are too fluid to be putting money in such low interest, uninsured TDs right now.

Governor Adrian Orr reiterated: “Banks have a critical role in supporting customers who are facing short-term income declines. Maintaining the flow of credit to financially sound customers also contributes to the long-term profitability of the banking sector, by avoiding unnecessary defaults and disorderly corrections in asset markets."

By avoiding unnecessary default and disorderly correction in asset markets...... Now also have not learnt the lesson but will go to any extend to support the ponzi instead of allowing the economy cycle of up and down run its course.

Support is good and needed but not at the cost of banks going burst.

First time such a fear is shared by Governor Orr, so is worrysome.

More problem for FHB as their saved deposit in banks are not safe and may lose it at the same time now cannot buy house also, as may lose equity/deposit with fall in house prices which is now very much imminent as all news/data/experts/agencies are predcting to be prepared for worse downfall in housing market.

Moral Of The Story : FHB is damned if they buy now and damned if the keep the deposit in bank.

Diversify.

My savings are spread across stocks, bonds, gold, crypto, NZ cash, foreign cash and some other investments.

Leaving all your money in the bank just encourages them to lend on housing.

Indeed. To explicitly state this stuff implies to me that he is very, very, worried.

There is a big move towards zero cash. The USA recently moved to have zero cash backing held against lending. The Chinese are now moving real fast towards digital currency and will probably get there first which will force the USA to respond. The ultimate Chinese goal is to displace the USD from being the worlds reserve currency, at which point the USA is no longer number 1 in the world. Plenty of info on the net already just Google it. Cash is "Dirty Money" in more ways than one and governments are now using Covid-19 as the perfect excuse to get rid of it.

The surveillance this will provide governments will be unacceptable to anyone with any sort of libertarian bent. It will also rubber stamp cryptocurrency as an universally accepted solution. Fancy paying for a prostitute on the government ledger anyone? What about the govt ledger recording where your donations go? Anyone smart enough to see this will at least be hedging with what's available now alongside the likes of Paul Tudor Jones.

ANZ's share price flying after Orr's comments. The market seems to interpret it all as a green signal.

Talking up the market is working out well everywhere, right up until the point there is a total loss of confidence when reality finally hits home.

another day with zero covid cases and an extra 1500 unemployed. Tracking along nicely

Another 100 going at Fuji Xerox announced around 5 PM

https://www.stuff.co.nz/business/121647589/fuji-xerox-to-axe-100-jobs-a…

Bank equity is made up of loans that they call an “asset” and then leverage 10 to 1

The “modelling” always says no problem.

Just like sub prime was no problem

Why do you think ANZ share price was 38% down in first 3m of 2020. Does that sound to you that market thinks ANZ is safe??

ANZ share price more than halved from $30.96 in Oct 2019 to $14.62 in March 2020, that's an eye watering fall. However they're up more than 11% in today's trading, so I guess the recession is cancelled!

No rhyme or reason

Don't these sort of crisis events always end up being fair worse than projected early numbers? Eg Look at the Christchurch earthquake and the increased costs of that.

Yes its about trying to stabilise the market and prevent panic. Giving bad projections can be self fulfilling so its best to play it down and hope for the best.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.