Reserve Bank Governor Adrian Orr says the bank regulatory capital increases put on hold during the COVID-19 pandemic remain very much on the regulator's agenda.

Speaking to media after the Reserve Bank issued its latest bi-annual Financial Stability Report on Wednesday, Orr said the capital increases were parked rather than binned. However, he did indicate the timeframe for implementing them, set at seven years, could be lengthened and the start date that has already been pushed out for a year might be stretched further.

"It's an idea that has proved critical and incredibly useful," Orr said.

"We were very pleased that a lot of banks had already moved pretty close to where we wanted them to get to anyway in advance, they were pre-empting our decision and our timetable. But what we've said to them is we will put it on hold for one calendar year, that was back in March, and at that point we will come back and reimplement that."

"What we'll have to do at that point is to say we assume you're going to be starting at a lower level of capital so we'll think about the transition period that we want banks to be working back towards a higher level of capital," said Orr.

"Of course come March next year we have to observe what is the economic environment around us. But [they're] far from shelved," Orr added.

In March the Reserve Bank said it was pushing out the start date for the increased bank capital requirements by a year to encourage banks to lend, meaning banks would be required to start their seven-year transition to meeting the new requirements on July 1 2021 rather than in July this year. The details of the new capital requirements are here.

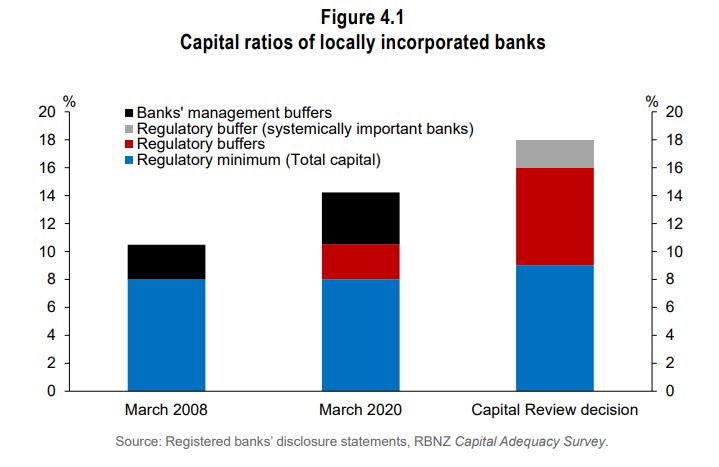

In the actual Financial Stability Report the Reserve Bank says its modelling showed banks would be able to meet the new capital requirements through retaining most of their earnings for a seven year period, while continuing to provide new credit to customers.

"Given the negative effect of COVID-19-related credit impairments on banks’ earnings, the Reserve Bank does not want banks to seek to achieve higher capital ratios through reducing credit availability in the current environment. As such, the Reserve Bank has deferred the implementation of its Capital Review decisions for a period of at least 12 months, with a future decision to resume the transition dependent on economic conditions. It is important to note that this decision is purely focused on the timing of the implementation of the Capital Review decisions. All Capital Review decisions remain in place, and will be important to help support the stability of the financial system for the longer term."

Figure 4.1 below comes from the Financial Stability Report.

*This article was first published in our email for paying subscribers on Wednesday. See here for more details and how to subscribe.

5 Comments

The banks dont need to be told what to do they are already bracing for maximum impact by restricting lending. Your ability to pay the mortgage is now front and center they will be minimising their risk exposure going forward and building reserves in preparation for defaults in a few months time.

Building reserves?

I've always been suspect of what they use as backing. All 'values' (besides food, water and shelter) are cranially-held constructs and thus liable to any alteration. But digitally-held ones and 'paper', would seem more suspect than most.

Nonsense which needs to be addressed by the adults left in the room and certainly depositors who carry the most exposure to a reduction in the soundness of the banking system.

As I noted yesterday:

by Audaxes | 27th May 20, 11:38am

Without any sense of irony the RBNZ has undertaken actions to undermine measures of banking system soundness in order to save banks and their customers.

{kind=link}

..the Reserve Bank has delayed increasing capital requirements, relaxed rules on how much of banks’ funding needs to come from long-term sources, and temporarily removed restrictions on low deposit loans. This helps to free up banks to continue supporting customers

In reality:

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

ANZ shareholders were impressed. One can only conclude they thought there were greater fools elsewhere underwriting their future.

Must be music to banking sector ears. If I was a bank I’d want to minimize my skin in the game right now. Who cares about negative equity when you can hold the government to ransom using voter deposits as leverage? Would Jacinda Ardern really let thousands of grandmothers and grandfathers take a financial hit, or would she take the ostensibly painless medicine bailing out the bank. Bear in mind that the title of Ben Bernanke’s GFC memoirs was “The courage to act”.

How is any confidence left in the system? What a joke. The rbnz tells us a few years back, "banks need their reserves for protection in hard times, and they were already caught playing by their own rules, some years ago."

Now it's all smiles and smooth talking heads, "yeah, we needed them to increase capital reserves, but hard times have come now, so we'll get them to work on that later". What utter bollocks.

ANZ shares then go up over $2, to $19+.

When they have been prevented from paying dividends? Who was buying? Investment funds have been doing nothing but seeking higher yields for over a decade, and suddenly we are supposed to believe that a non-yielding share is worth buying?

How is this not complete manipulation?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.