The Reserve Bank (RBNZ) believes it would be counterproductive for it to try to rein in property investors while it’s doing everything it can to stimulate the economy.

The RBNZ on May 1 removed loan-to-value ratio (LVR) restrictions. These required banks to ensure most owner-occupier mortgagors had a 20% deposit, and most investors had a 30% deposit. The RBNZ said it would review its decision in a year’s time.

Asked at a media briefing on Thursday whether the bank would consider applying LVR restrictions to investor lending sooner, given the rapid growth in new (and higher-risk) lending to investors, senior RBNZ officials were unenthused by the suggestion.

Assistant Governor and General Manager of Economics, Financial Markets and Banking, Christian Hawkesby, noted this was a decision for the RBNZ’s Financial Stability Committee.

But he said: “My broad message would be - just remember where in the economic cycle we are.

“Those macroprudential tools and the like - they’re really designed for when you’re on the economic upswing, things are booming, credit growth is very strong, credit growth is freely available. They’re designed to put grit in the wheels of that type of environment.

“At the moment we’re in a different type of economic environment… There’s a big economic contraction and we’re trying to create an environment - by lowering interest rates and making the funding freely available - so we can actually have an economic and financial recovery.”

Investors pile in

The RBNZ has been lowering interest rates in a bid to ease debt servicing costs, and encourage borrowing and spending to boost inflation and employment in line with its monetary policy mandate.

To date, much of its stimulus has come through the housing market.

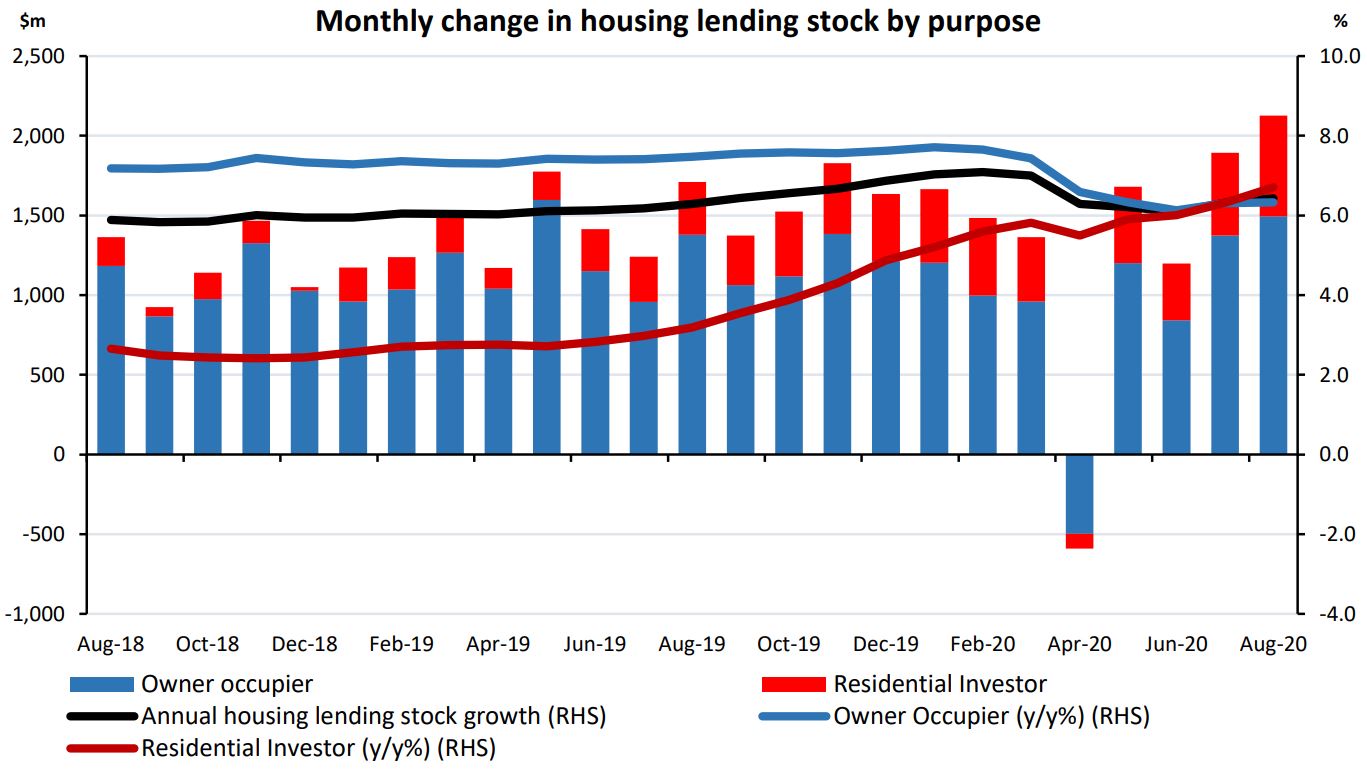

Bank lending against housing is up. While first-home buyers have been active, growth in new lending to investors is out-pacing growth in lending to owner-occupiers:

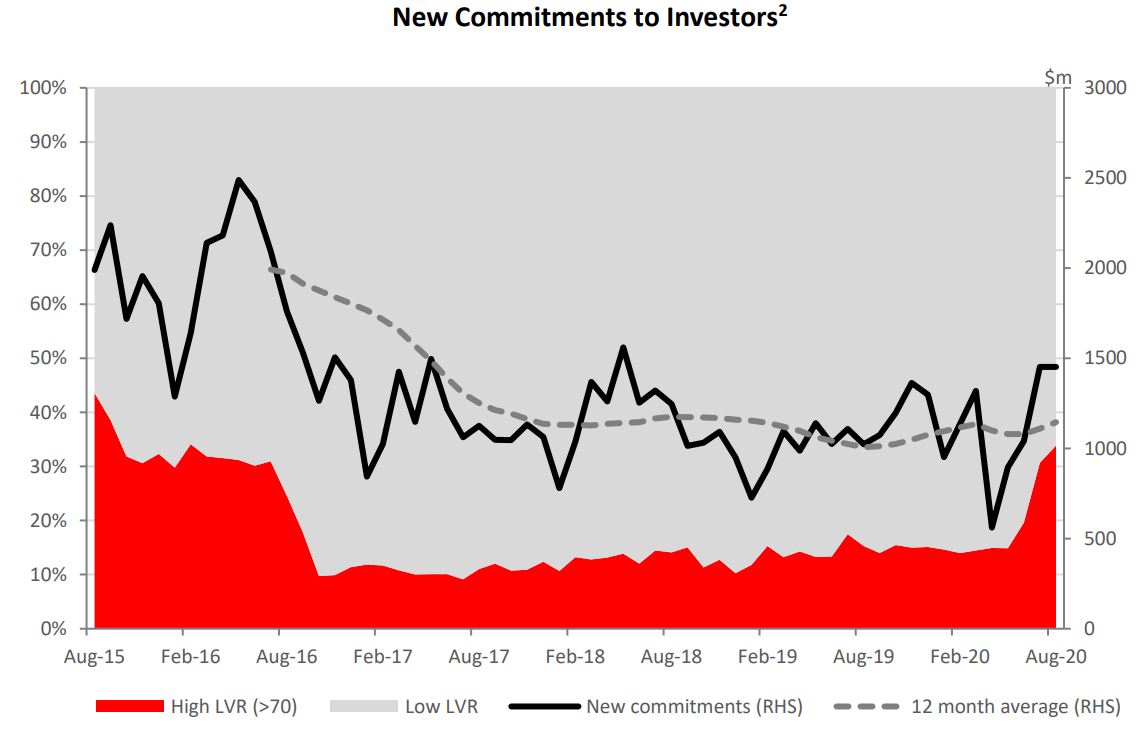

There has been a more than doubling of new lending to investors with deposits of less than 30% since the removal of LVR restrictions:

Lending to investors with deposits of less than 20% was up 32% in August 2020 compared to August 2019.

Already inflated house prices are continuing to increase in value.

Median price - REINZ

Select chart tabs

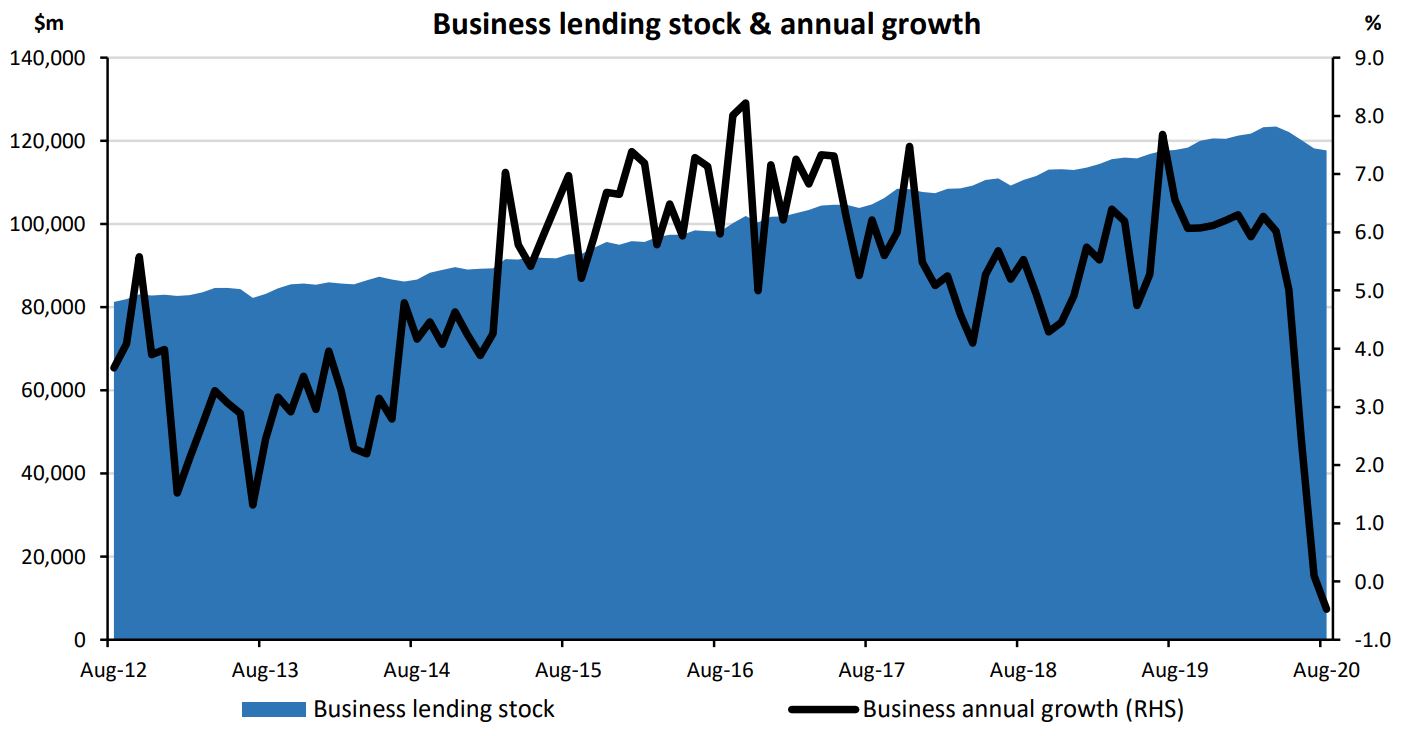

Meanwhile new bank lending to businesses has fallen:

Falling house prices would be a 'worse situation'

RBNZ Chief Economist and Head of Economics, Yuong Ha, wanted people to acknowledge the RBNZ’s view that while lower interest rates boost asset prices, this has a wealth effect, which boosts confidence, spending, economic activity and employment.

From a financial stability perspective, he said: “The worse situation we’d face right now is actually if we had house prices falling.

“That’s always the flipside. You’d be dealing with a Covid recovery and a disruption in wealth through lower house prices.”

Asked to explain how a small reduction in house prices would be bad, Ha said: “We’re conscious of what would be the downstream impact on household and firm behaviour in an environment where household wealth was declining.

“We’re conscious of some of the balance sheet impacts on the financial system.”

Business investment expected to follow...

Ha made the point the RBNZ’s loosening of monetary policy could come through different channels at different times.

He said that while property buyers are borrowing now, businesses might have a greater propensity to borrow once economic growth picks up.

“Investment tends to respond to the state of the economy,” Ha said.

“So the more successful we are supporting the economy through other means… that’s when they [businesses] respond.

“They might not respond directly to the interest rate channel, because uncertainty around the border closure and what-have-you will be dominating their minds.”

It's worth noting that while business confidence is low, but improving, a net 34% of businesses surveyed for ANZ's October Business Outlook Survey had a negative view on the ease of getting credit.

Asked whether there was a point at which high house prices would actually have an inverse effect - IE leave people, especially renters, with less cash to spend on stimulating the economy, Ha said this was something the RBNZ was constantly monitoring.

While he deemed house price growth to be stimulatory in the current environment, he recognised that could change.

Ha also pointed out that in August and May the RBNZ thought house prices would fall, so was surprised by the strength of the market.

91 Comments

"while lower interest rates boost asset prices, this has a wealth effect, which boosts confidence, spending, economic activity and employment."

It might stimulate employment, but the wages we are paid in NZ does not cover the increase in the prices of assets like houses, and the RBNZ doesn't think it's having an adverse affect on consumer spending or well-being.

We're being conned.

Agree we are being conned. RBNZ make out they have all the answers but they and us have no idea.

Nobody knows is the answer if they let the market be the market.

However if zero and negative interest rates and risky loans were a good idea why were they not done all along.

Obsession with saving the debt fueled is a disgrace.

No deposit holder guarantee is a disgrace.

IF not providing additional capital for non-performing loans was a good idea why did we just not allow this all along. With artificial schemes implemented like this deposit holders have no ability to determine the financial viability of their banks. RBNZ prefer pretend and extend.

Deposit holders are being scammed.

As I said on here earlier this year - I used to think that the RBNZ were the 'good guys'. I now disagree and think they're pushing an agenda that isn't sustainable and although its saving us from pain now, its creating longer term pain for us into the future. If you prefer to avoid facing up to the hard truths then that's fine, but they will still find you eventually. You're better to face those up front in my view and get them out of the way then move on. At the moment we're not doing that and the big elephant in the room is going to keep getting restless and make a mess, even if we decide to continue to pretend its no there.

Yeah. I've stopped giving them the benefit of the doubt. They're obviously smart and pleasant people, but their desperation to maintain stability is going to cause absolute chaos sooner or later. Adrian Orr seemed like an independent thinker -- what happened? He's pursuing the most predictable protect-the-status-quo-at-all-costs policy you could imagine. I guess Wellington gets to everyone eventually.

If you have dealt with the rbnz then the last word that would come to mind is pleasant. They have a god complex and it rears its ugly head. They don't care about the ordinary person. A caste system is best how i could think of their culture

Who could have possibly predicted that secluding a bunch of economics and finance wonks in an ivory tower would result in such a culture?

It's about to get worse. The government has confirmed it is in talks with Australia to set up a travel bubble.

The driving force behind this new development is that, as per Grant Robertson, a travel bubble with Australia would free up “an enormous amount of capacity” in New Zealand’s managed isolation facilities (60-70 percent) and allow workers, international tourists and visitors on other visas to enter New Zealand.

Let's turn the entire country into a 5-year MIQ for those intending to backdoor into Aussie!

https://www.stuff.co.nz/business/industries/123027828/travel-bubble-wit…

Spot on! And it's not just the RBNZ.

Anyone whose ever been 'called in' to a Central Bank for a 'friendly talk' so they can quiz a couple of you on "Why are you guys doing XY & Z?" knows they try to intimidate you into disclosing all.

I can recall, like it was just yesterday, being across the table at such a meeting from fellow investment banker Ivan Ritossa, who'd also got the 'call up' and we both knew what the other was thinking "Well I'm not going to tell them! Are you"

Seriously. Regulators are simple-minded, never-weres, or else they'd have been out in the 'real world' putting their skills on the line, every day, like we did.

What they do instead, is put OUR skills on the line every day, and if it goes wrong - keep going at it, in the vain hope that eventually it works.

Perhaps they do since they do not need to get voters support every 3 years?

This is decades in the making - one man vs decades of economic thinking and debt misallocation. It would be like attempting to be a very small Orr, say the size of a spatula, fitted to the Titanic (excuse the pun) and expecting to turn away from the iceberg.

I wholeheartedly agree. Orr is completely delusional and the long term damage of his recent decisions is definitely going to be felt. It is crazy that a bunch of un-elected bureaucrats can wreak so much potential damage to the economy with no accountability for their actions.

Remember they're more or less just taking their direction from the Fed - so I wouldn't blame the man, but more blame the culture and way of thinking.

Mr independent, I'm not sure why you would be complaining that housing is being supported by Govt and the Rbnz ... the spinoff is for those who work in the industry companies like Fletchers .. ie increased employment for workers and better dividend returns for shareholder investors... solution for you: Vote yes to dak and be happy

It’s a bit like the police supporting meth users and dealers.

Well said OC

We're being conned alright. I can't believe what I've just read. We're totally stuffed going forward if these folk are in charge of our economy, may god help us all.

We're being conned

No you're not. The wealth effect has been in play for the last 30 years. Noted behavioral economists have spent much time explaining its relevance to bubbles and political power. The typical Kiwi will probably not want to admit that their behavior has been influenced by their perceived wealth.

Now the RBNZ is stating how important the wealth effect is to our economy. Good on them. The cat's out of the bag. They believe in its power.

The wealth effect is by no means settled science. A few badly controlled studies by economists with an incentive to pump up property markets does not make it a real thing.

https://www.nber.org/papers/w15075

"Once we control for the endogeneity bias resulting from the correlation between housing wealth and permanent income, we find that housing wealth has a small and insignificant effect on consumption. Additional analysis of time-series results provides further support for that view."

The wealth effect is by no means settled science.

You also cannot deny its existence.

What? I'm quite clearly denying it's existence.

As you please. You can deny all you like.

Yes we are. the con has been 30 years long. Its given us what...an economy based on house flipping and immigration.

We should never have taken this option and the end game of this nonsense is in sight.

But as long as the boomer generation can just get through eh!

The socialists used to have a catch cry...eat the rich. Now its the RBNZ... eat the poor.

Entrench a landed gentry, commit the youth to debt slavery just to maintain the status quo...

Can anyone who has studied history tell us what that situation has led to in the past?

Usually the guillotine.

Revolution ! Don’t see that happening in NZ though. Most of the populace are sheep and in adoration with Saint Jacinda, even though she’s not interested in anything concrete for them as the past 3 years have shown.

You just have to read the comments on her Facebook page

Can't believe what I just read? The NZ taxpayer has to pay these people? Do they not realise that money is marely a means of exchange & lacks any real intrinsic value.

You can rob Peter to pay Paul but at the end of the day Peter & Paul collectively have the same amount of money. In this case Peter is a saver, Paul is a borrower.

Ah, but if you increase the amount of money in the system and that money all magically flows into the value of Paul's house, Paul is richer due to manna from heaven and Peter's savings are worthless.

Wile E Coyote used to run off the cliff and keep going at full speed until he looked down. Sure is going to exciting to watch.

If we can get some good unemployment numbers it will change things. As zero rates or negative rates wont help when you cant repay any principal and the tide may turn on house prices. I am keenly watching for this in April onward post mortgage holidays.

What then? Orr may then offer some further scheme to save the debt fueled.

This may sound negative but I would rather face the unemployment, have the country learn to live within its means and deal with the unwinding of house prices than the current BS.

The so-called "Wealth Effect" was propounded by the economists Case & Shiller, who some of you might recognise as the authors of the Case Shiller Index, which tracks the value of housing across markets. They formed a company to publish this index, which was eventually purchased by CoreLogic.

Other studies have since been done on the effects on household consumption of increases in housing wealth, and have come to the conclusion that there is no measurable effect - yet this idea persists as economic dogma and the property industry has made these economists very wealthy.

They should actually give that as an explanation, even the bit about other studies, cause it still makes more sense than what they're currently pushing.

RBNZ do, it's in each monetary policy statement explained as one of the channels by which expansionary monetary policy flows through to higher consumer inflation. The problem is that the science, if you can economics that, behind that channel is questionable at best.

All they're really saying is that gambling with leverage on our housing market is now so extreme that if prices were to fall it would destroy our economy and because we didn't manage that well in the past it means that we now have to support said gambling culture.

You've nailed it. They are so terrified of any drop of the monster they created that anything and everything will be sacrificed to keep the plates spinning.

The reckoning gets ever worse.

'Eat a live frog first thing in the morning and nothing worse will happen to you the rest of the day'....nah, we'll just wait until 11.59.

It's a "Wealth Effect" just for the already wealthy. Banks extend around 60% of lending to one third of households to speculate in the residential property market.

As I noted yesterday :

.. the most important macroeconomic variable cannot be the price of money. Instead, it is its quantity. Is the quantity of money rationed by the demand or supply side? Asked differently, what is larger – the demand for money or its supply? Since money – and this includes bank money – is so useful, there is always some demand for it by someone.

As a result, the short side is always the supply of money and credit. Banks ration credit even at the best of times in order to ensure that borrowers with sensible investment projects stay among the loan applicants – if rates are raised to equilibrate demand and supply, the resulting interest rate would be so high that only speculative projects would remain and banks’ loan portfolios would be too risky. Link

This is why interest rates keep falling - nothing to do with central banks - banks are failing to find borrowers capable of securing adequate collateral and income to meet their lending standards, hence they push interest rates down hoping to entice the already wealthy to borrow against their better judgement. Other than that funding government debt will suffice.

Interest rates are driven by demography.

Other studies have since been done on the effects on household consumption of increases in housing wealth, and have come to the conclusion that there is no measurable effect - yet this idea persists as economic dogma and the property industry has made these economists very wealthy.

Strawman. The 'wealth effect' idea is not dogma. It's supported by empirical research. If you don't like the idea of the wealth effect, you're welcome to share. Furthermore, the Case Shiller Index was not designed to push an agenda nor was it created to 'cash in' on the idea of the wealth effect.

Replied to your previous comment but I will do so here as well, empirical research (https://www.nber.org/papers/w15075) has shown that Case Shiller et al did not account for other factors affecting consumption - once accounted for, the effect of housing wealth on consumption is not statistically significant.

Replied to your previous comment but I will do so here as well, empirical research (https://www.nber.org/papers/w15075) has shown that Case Shiller et al did not account for other factors affecting consumption - once accounted for, the effect of housing wealth on consumption is not statistically significant.

It's a paper that calls into the question of housing wealth on consumption. It does not disprove the wealth effect.

Do you understand what the wealth effect theory proposes? An increase in perceived wealth causes an increase in consumption spending.

Do you understand what the wealth effect theory proposes? An increase in perceived wealth causes an increase in consumption spending.

That is an over-arching explanation of the wealth effect. It also has important implications for behavior such as purchase decision trade offs, which is crucial understanding in the commercial world of products and services. Furthermore, it also has implications on economic self sufficiency. For ex, the extent to which a household holds liquid assets.

You get the feeling we might find out for real J.C. one way or the other.

It's for the wealthy minority as I have pointed out before and will do so again so there is no confusion:

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax. Link

The majority of wealth held in property, is held by owner occupiers. They aren't exactly a minority, it's over half the country

And what percentage produce an income to offset the rising costs of liabilities - I own my own home outright , but it certainly consumes an increasing share of my income.

Sorry but an argument around maintenance and rates is a strawman to say the least.

$8000.00 dollars to paint the roof , ~$2000.00 to insure that roof over its owner's head - all on a pensioner's income That's what my elderly single lady neighbour endures, and yes she does own a house she can ill afford. But not for much longer because the $4000.00 rates bill will take its toll before old age does. And then there is the winter heating bill which is insurmountable hence she remains cold or spends an inordinate amount of time at the public library.

How bizarre - we have some of the worlds most expensive houses but it would make our economy worse if they became more affordable. How insane...

Should OneRoof and RBNZ start a merger?

Should OneRoof and RBNZ start a merger?

All bubbles are supported by vested interests from the ruling elite to real estate offices. It should have not taken this pandemic for people to realize that the housing market is really the be all and end all in the NZ economy.

You decide if they're expensive by making comparisons with salaries and wages. Expensive homes or low pay... take your pick

IO... heard that Adrian is grooming Ashley Church for RBNZ Gov for when he steps down.

Scary thing is that someone so unqualified probably wouldn't make any difference as the status quo!

To avoid a Minsky moment they opened the taps and removed restrictions. But if economic fundamentals decline while prices and leverage increase then the fragility and risk in the entire economic system will have become magnified.

To avoid a Minsky moment they opened the taps and removed restrictions. But if economic fundamentals decline while prices and leverage increase then the fragility and risk in the entire economic system will have become magnified. >

Very succinct explanation

I was hoping that first home buyers would be encouraged by lower mortgage interest rates. However, the dropping of LVRs on investor borrowing seems designed to further embed housing inequality. Now is an opportunity to improve the low home ownership rates but none of the main political parties care and allow the RBNZ to reinforce unfair policies in this regard.

lol "Ha also pointed out that in August and May the RBNZ thought house prices would fall, so was surprised by the strength of the market."

Come on! Don't lie to yourself. We all know it wasn't the strength of the market. You've dropped OCR from 1.00 to 0.25 and removed LVR, plus the government's wage subsidy. Of course the house prices will go up. It shows that RBNZ don't know what they are doing and they don't know what's gonna happen.

If at March 2020, I would have told you that the RBNZ is going to drop the OCR from 1 to .25, remove LVR and there will be a wage subsidy, would you have said house prices would increase by 10% despite all the fear and uncertainty? I doubt it.

Hindsight bias is at work here. A lot of commentators on this site knew and expected the above actions and they were of the opinion that it would not be enough to stop a collapse in the housing market. That it has turned out the way it has, is surprising and defies common sense.

Many commentators say reducing interest cost will increase the present value of cash flows (which is true) thus increases the present value of asset. But what about the cash flows? are you project the same amount of cash flows now (with lower interest rates, no economic growth, falling GDP, rising unemployment etc)? so if you adjust your expected cash flows then maybe the reduction of interest rate should not produce such an increase, it can result in the same PV, it can result in lower PV.

So the increase in all asset prices does not simply show further reduction in already very low interest rates, but the expectation that cash flows will remain at their current level or will increase.

I wouldn't say it would increase by 10%. But would dropping OCR from 1 to .25, remove LVR and wage subsidy be generally pushing housing price up? Of course they would. It is no brainer to know that these policies are favoring housing market. When you have both government and RBNZ's policies favoring housing market and prevent the price falling, how can you say "surprised by the strength of the market"? If the market is strong, I don't think you need these policies in first place. You can comment on the market strength only if you are willing to let the free market to do its work, not pushing out favorable policies and comment "oh the market is strong". That's just bias comments that politicians normally make. We dont want politicians in RBNZ. We want honest people who know what they are doing in RBNZ.

There is no exit plan except 'growth'. But there's also no prospect of growth, as evidenced by the bond markets. So there is no exit plan. Either load up on debt that you know you can never pay off (if you can), or give up on ever participating in favoured asset classes. So in ten years the middle-aged will be in two categories: the mortgaged, who have property of theoretically huge value but little disposable income (incomes not having risen to offset mortgage costs); and the renters, who have more disposable income but never enough to buy security. It's setup for another wave of brain-drain from NZ to any other country that can avoid this depressing senario.

Unelected and unaccountable crooks.

They have no idea what they are doing and couldn't care less about the wider consequences on our society.

New Zealand is firmly on the path to catastrophe. I wouldn't be surprised if this housing bubble takes out our currency or our entire economy within next ten years.

The young have no hope and nothing to aspire to except getting the hell out to make a life for themselves elsewhere.

It's the Pied Piper taking our children (and grandchildren) away.

Caught up with the in-laws recently, their kids have given up trying to get on the property ladder so they are off to Aussie very soon. Better paying jobs and much cheaper houses. The brother-in-law is livid with what successive governments here have done, the sister-in-law is inconsolable her kids and grandkids are being taken from her.

But hey, it's worth swapping our young for higher house prices isn't it.

Forgive me if this is not the appropriate place in which to ask (I am new here, so please be gentle)

Are there any political parties this election who have indicated they will be looking at the Reserve Bank Act and the RBNZ and whether it's current mandate and policies are still pertinent in the current environment? I feel I have had a good dive into the policies of each party, but none appear to have substantially touched on the Reserve Bank act nor the RBNZ's role.

Winnie had a Bill that was defeated.

.

Article should be titled "RBNZ maintains Banks profits in NZ ". Property debt is continuing to be used as an economic tool to enslave most kiwis. RBNZ should promote being debt free and a stop promoting the stupid levels of leverage common in NZ.

Fully agreed, it's the time to put more steroid or fertiliser onto it. RBNZ should modelling the new anticipated FLP into FLP 2.0 high gear full on, add QE/LSAP into the 300billions teritory at least.. then version 2.0 of FLP to be tweaked as opposite to the LVR - This is the only way for NZ at the moment, have to be done before Q1 2021 - Remember, if RE is Cancerous? then Chemo or Radio therapy will just make it worst. So, do the opposite!

I've known for some time that the housing market was being propped up, predominantly by property invested politicians and their corporate buddies, but when the 6 o'clock news reports that the Government and RBNZ are pushing housing prices to spur spending by wealthy asset owners in order to save the economy, I know things are completely out of control.

Successive Governments have turned their back on the 40% or so of the population that don't own property assets while expecting that same 40% to shoulder the majority of the cost of repaying the debt. It's criminal and needs to stop.

Funny coincidence. I used to live in that apartment tower as photographed in the picture for this article. I paid $600 a week in rent for a small 2 bedroom apartment. My partner and I, after much sacrifice, had finally saved enough for a house deposit. Prices had stabilised. Then the RBNZ got involved, speaking in tongues about consumer wealth effects blahs blah ad nauseam. Then the apartment we were living in went for sale, and prices went out of our reach. Again. So with nowhere to go, we hopped on a plane to Aussie. Glad I left with all this new RBNZ nonsense going on. Our deposit will buy us 2x the house here in Aus. I dont think we will be back! This is just my example, but it is probably about to be repeated for many as a new brain drain begins in the coming years...

What do you think, those of us in productive years earning 6 digits figure doing so far? proping up the damp old NZ RE's? C'mon matey - you're welcome, won't regret it - heads to WA or SA, for more options. Check this out, even our lady bozzy VC already pre-empt the moves (despite more than 600k figure here and prop up the dumb FIRE economy ideas): https://www.curtin.edu.au/

Patches, I might be joining you. RBNZ can get high on their house prices, but will lose those with skills to be mobile abroad.

Perhaps they are just trying to dampen migration by having the highest house price to income ratio on the planet *perhaps we already had that anyway

I won't be far behind either.

Take a look at the international news. House prices are rising strongly in much of the developed world.

Investors: to him that hath

Renters: stuff you

FHB: greater fools

OO: staying put paying off debt

Dead are days when central banks knew anything about sound finance, fiscal rectitude and risk management

At least they make no secrets about the strategy going forward.

Welcome to the new normal everyone, house prices can only go up, that is RBNZs sole function now it seems.

Low interest rates equals low exchange rate... yippee farmers make more income, sharemilkers doing well and expanding their herds, farm owners see the benefits through increased yield and want to buy another farm. You haven't said whether or not you agree with the policy JAF

If it all works like that then it sounds brilliant!

Yes now RBNZ is playing on front foot and screw to all FHB.

"“Those macroprudential tools and the like - they’re really designed for when you’re on the economic upswing, things are booming, credit growth is very strong, credit growth is freely available. They’re designed to put grit in the wheels of that type of environment.

“At the moment we’re in a different type of economic environment… There’s a big economic contraction and we’re trying to create an environment - by lowering interest rates and making the funding freely available - so we can actually have an economic and financial recovery.”"

*Dripping with sarcasm* All well and good. Of course we all saw interest rates rise during the 'longest boom in history' that we've just come out of right?

How fast and proactive RBNZ was to remove LVR to boost housing market and notice how they are finding reasons of not reintroducing LVR though knowing that house prices are moving very fast from already high prices..

To support ponzi need no reason and are promot but..........

This shows the mentality of RBNZ, which now they are openly admitting as have no choice as is very evident that their actions are only leading to inflating asset class and if they want low interest rate to boost other economy (not give reason of side affect) can easilt intriduce LVR to curb speculative demand but they too know that this boom is supported by speculators more as FHB are not normally in million dollar category and RBNZ like government is just using FHB to promote speculation.

Real Shame but true as everyone knows what is happening in housing market is not helping FHB but speculators.

If we had a property tax the increased equity would at least be partly captured by the tax system reducing taxes on the productive.

https://d3n8a8pro7vhmx.cloudfront.net/garethmorgan/pages/2959/attachmen…

Who is really in charge of the RBNZ? Not the NZ people for sure.

“The worse situation we’d face right now is actually if we had house prices falling"

Incorrect, the worse situation would be a retail and services sector that get to a standstill since households are already over-leveraged by mortgages on over-priced assets. That will cause growing unemployment and social unrest much worse that falling asset prices which would in reality mostly affect investors.

RBNZ and house prices be like:

https://media.tenor.com/images/5183f1c5b584d08f6068bb1fc4fc35dd/tenor.p…

{kind=link}

If house prices were falling, we would be standing around in shock that the economic forecasts were right.

The thing is every joe on the street knew when lockdown hit, that this was the shock that would finally dent the house market. "Yup the time has come". "Lucky I bought with 20% deposit not 5%" . "Lucky my bank tests me at servicing 7% interest rates not the actual 3.5%"

RBNZ now say that, no no no, we can't have that dent, even if everyone expected and braced for that. We need the wealth effect to bridge the gap before businesses smell a recovery.

So, we were all wrong. There is no dent to the house market possible. LVR don't serve any purpose to protect us from shock, and by the RBNZ logic bank-required servicing rates don't serve any purpose either. RBNZ will protect us, asset owners, always. God defend new zealand property owners.

It would have been nice to have known that the RBNZ were committed to the principle that house prices would never go down. For first home buyers this would reduce a lot of anxiety and investors could add to their portfolios with a high level of confidence.

I didn't know that. Rather foolishly, I realise now, I believed that saving for a rainy day was the right thing to do but clearly it was not. Perhaps because so few of us actually did it there was safety in numbers, because so many people had no buffer, it was simply too big to fail.

By counterproductive RBNZ means that will stop rising high price.

I think I finally figured this out about 3 weeks ago now. Took a lot of banging my head against a brick wall before I just had to change my mind that all the powers that be are propping up the housing market no matter what. Basically its now Armageddon before we see a fall in house prices and by then its going to be too late anyway.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.