The Reserve Bank (RBNZ) has clarified it wants to put restrictions back on bank lending to both residential property investors and owner-occupiers.

The RBNZ on Wednesday announced it would consult on reinstating loan-to-value ratio (LVR) restrictions in March, rather than keeping them off until at least May, as previously stated.

Speaking to interest.co.nz, RBNZ Deputy Governor and General Manager of Financial Stability, Geoff Bascand, confirmed the RBNZ intended to “reinstate the restrictions we had in place in April before we removed them”.

Specifically, he said this meant no more than 5% of a bank’s investor lending could go to borrowers with deposits of less than 30% (IE most investors need a 30% deposit).

And no more than 20% of owner-occupier lending could go to borrowers with deposits of less than 20% (IE most own-occupiers need a 20% deposit).

‘We’re trying to stop all high-risk lending’

Asked why not only put restrictions on investors to prevent making things harder for first-home buyers, he said: “We’re trying to stop all high-risk lending…

“When we had no restrictions before 2013, we were seeing a lot of lending going at 85%, 90% LVRs. The problem with that is, if the housing market does take a downturn (and we certainly expected that earlier under the pandemic), then people are exposed and they suffer losses and then the banks suffer losses…

“We’re trying to keep those credit standards up for everybody.

“We see a little bit more risk with investors than we do with owner-occupiers, which is why we have tighter rules for them.”

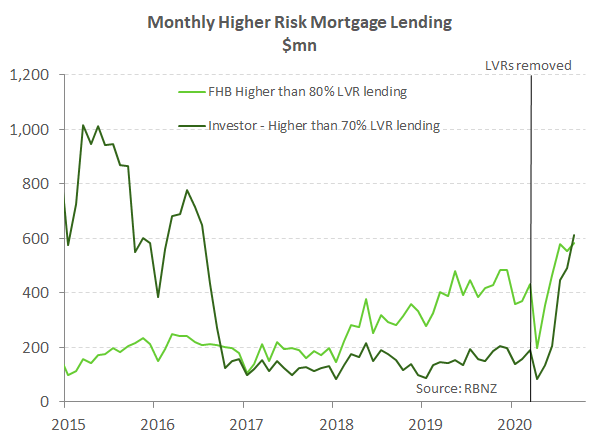

RBNZ data, graphed by Kiwibank economists, shows a spike in high-risk lending to both investors and first-home buyers following the removal of LVR restrictions in May.

The uptick has also coincided with mortgage rates falling on the back of the RBNZ cutting the Official Cash Rate (OCR) to a record low, as well as it effectively pumping up to $100 billion of newly created money through the banking system via its quantitative easing programme, and it planning to lend up to $28 billion to banks at a low rate to help them on-lend at a low rate.

Why can’t the LVR restrictions be put on sooner?

Asked at a press conference on Wednesday why the RBNZ couldn’t implement LVR restrictions sooner than March 1 to prevent buyers rushing into the market before then, Governor Adrian Orr said: "We expect the banks themselves to be the ones who are lending responsibly and managing that capital allocation and avoiding undue risk."

Bascand added: “It’s really as early as it could be done.”

He said a long enough lead time was necessary for banks to know how to handle mortgage applications being processed.

Orr said the RBNZ also had to go through a proper consultation process.

“When we are taking away restrictions, we don’t have to consult. When you’re adding restrictions, you do,” he said.

The RBNZ only left a week-and-a-half between proposing to remove LVR restrictions and making their removal effective on May 1.

No regrets

Orr said he had “no regrets” about removing these restrictions.

“We made sure during the darkest periods of the Covid uncertainty that there was nothing that we were doing… that would get in the way of banks being able to step up and provide confidence and cashflow," he said.

“We had significant concern that the mortgage deferral scheme for example may run up against our own loan-to-value restrictions.”

Onus on the banks too

Fast-forward a few months, and Orr said almost every bank CEO and a number of bank chair people were asking him to put the restrictions back on.

“You’d have to ask the banks why they couldn’t do it themselves. But I assume it’s because of the competitive nature of banks. No one bank felt they could afford to step out… for fear of losing market share.

“So the traditional call came for us to do it to them instead.”

Orr said the decision was made by the RBNZ, which wasn't influenced by Finance Minister Grant Robertson.

Robertson made a point of telling media he brought forward a meeting with Orr on Monday. He then welcomed the RBNZ’s LVRs announcement, saying, “I would like to see the work happen as soon as possible”.

Pulling out the hose while fuelling the fire

Asked why the RBNZ chose to make its LVR announcement on the same day it released its Monetary Policy Statement, rather than waiting two weeks until the scheduled release of its Financial Stability Report, Bascand said: “The later we left the communication, the harder it would’ve been to meet a 1 March date and we would’ve been potentially surprising people very late in the year.”

He also acknowledged that as the RBNZ announced it would provide banks with $28 billion of cheap funding, it would be asked about the impact of this on the housing market.

He said the RBNZ wanted to provide reassurance its monetary policy and financial stability arms were talking to each other.

Bascand wasn’t convinced by the suggestion sky-rocketing house prices were undermining the RBNZ’s social and political licence to conduct monetary policy.

“The concern we have is only about high-risk lending,” he reiterated.

“We obviously don’t have a mandate and we can’t control the housing market. The housing market is a consequence of all sorts of supply and demand factors.”

Here’s a rundown of the questions asked in the video interview, in case you want to skip to bits not covered in the write-up:

Start: Is making it even cheaper for people to borrow the right policy response to the current crisis?

2:00: How much more confidence does the RBNZ need to give the market through looser monetary policy?

3:35: Is the lack of conditionality on the Funding for Lending Programme an admission by the RBNZ the $28 billion of funding will go straight into housing?

5:39: Why has the RBNZ not included building societies and credit unions in the Funding for Lending Programme?

6:51: Why did the RBNZ make its LVRs announcement on the same day it released its Monetary Policy Statement?

8:38: Is the RBNZ worried the focus on house price inflation is undermining its social and political licence to conduct monetary policy?

11:21: Is the RBNZ concerned property buyers will rush in ahead of the LVR restrictions coming in, in March?

12:42: Did Robertson influence the RBNZ on LVRs?

13:23: Is the RBNZ considering imposing LVRs on investors only?

14:48: Why not exempt owner-occupiers from LVRs?

15:58: Should asset price inflation be added to the RBNZ’s monetary policy mandate?

71 Comments

Horrific decision to remove the LVRs. All the worse now they are absolving themselves of all responsibility AND saying they don't regret it. The same as "not having the ability to put a mandate on the 28B of lending". Of course you do - for the good of the financial system, which is your mandate. Duh.

As far as I can see from Bascand and Orr, they will do anything to cover their a$$es, rather than doing what is best for NZ. Ergo pride, arrogance and bad models controls their decisions, rather than wisdom and intelligence.

"We can't control house prices" - even though the correlation of available credit to house prices is pretty clear.

When you correlate credit with house prices do you take into account the new houses built (that where not going to be built without the credit created)? Between Sep 18 and Sep 20, total lending to residential building increased from $271b to $305b. An increase of $34b. There is no accurate information (at least that I know of) of selling value of new builds in the same period, but if use value of issued consents as a rough proxy (and lets lag that by a year so from Sep 17 to Sep 19), as per Stat NZ info, $51b of new builds are consented. So even if not all ended up being built, a significant amount is added to stock. So when you say credit creation increase house prices, you must offset that by the credit creation that has gone to new houses.

This guy acts like he'd rather be doing something else, like playing golf or mowing the lawns on his lifestyle block. He's not interested at all...just listening to him makes me tired. Bring some young people in that can get the job done!

He's actually a spring chicken for a Vampire Prince.

Why am I have this feeling that NZ's housing market is gone crazily unleashed forever?

NZ - Banks, RBNZ, Govt, owners, investors and buyers have grabbed the tiger's tail - it cannot let go for fear of destruction, in fact it has no idea how to let go.

$2.28m PGF loan, now repaid in full, helped Northland berry farm create an additional 56 jobs.

How many jobs has Orr's hundred billion pumped into real estate created (or destroyed)? It would be interesting to see the effect of reintroducing risk premiums on interest rates for recent high-LVR borrowers on household discretionary spending.

https://www.stuff.co.nz/business/farming/123363523/northland-berry-farm…

I suspect it may create more construction jobs as this will likely result in a building boom (although who know for how long). However, it will also destroy a lot of other jobs as people have less money to spend in other parts of the economy and /or invest in export businesses. Overall our economy becomes less diverse and more inward-focused.

It might create the demand for more jobs but the industry is already struggling to retain/increase it's workforce now. Unlikely to lead to any building boom because the there just aren't the companies available. Hopefully there won't be an explosion of "cowboy operators" which lead to the last couple of disasters - the CC rebuild and the "leaky building" saga.. not holding my breath though.

Could they not have just immediately applied the LVR restrictions to new applications & existing pre-approvals remain valid until expiry?

No, you want to give chances to your buddies to get on the train before it leaves the station :)

yet more proof the clowns are running the circus - what a debacle

Bascand says they have to "consult" and give 4 months notice to reintroduce LVRs so there are "no surprises" for banks. But RBNZ just months ago more or less immediately removed the LVRs along with slashing interest rates with zero notice. Absolutely disgusting - these imbeciles need to be sacked.

Agreed on all counts. The consultation surrounding introduction of LVRs has already been done prior to the first application - what's to consult on now?? The justification hasn't changed nor has the mechanism for application - saying otherwise is hubris (or to be blunt straight out BS)

A mortgage broker just sent me this message:

The banks aren't going to wait until March to start applying these rules, they will do it as soon as the consultation is completed if not sooner. I'm telling investors they have three weeks to purchase if they have less than 30%.

If your current bank said no before restrictions are enforced surely you'd go look elsewhere that would. Banks shareholders going to be happy with that?

It's a Lenders market - they don't care if you walk out the door, there's 10 others clamouring to walk in

I'm sure the mortgage advisor cares about that business

Not really. he/she is on a salary - banks have been encouraged/instructed to not pay commissions based on lending totals after the swaps scandal

I think you'll find the large majority of mortgage advisers on commission only

In other words...... Blah Blah Blah tee bloody blah blah :)

Banks are paying commissions, it’s how the model works. It will just be that their boss (with the broker agreement) is keeping the commission and paying a salary

True, but not this renter. I'm just loving the show as avg prices head to $2m+.

I was out of contention in this market long ago, so it's pure entertainment from now on. Come on you guys - stack up those chips!

Bank shareholders should be happy with that, it's their money being recklessly lent out to all and sundry.

Perhaps this broker should also apply the same LVR restrictions to his clients instead of encouraging them to invest before the party is over but I guess his own income depends on it, so who are we kidding right?

Jenée is a superb journo and Bascard cool, calm, and collected with a bit of the ol' Gliding On charm that we should expect from our ruling elite. Sometimes I wish they would be a little more ruthless and say something along the lines of 'It is what it is. Live with it. We're doing the best we can and we're working within the complex that have. Next question.'

Calling Bascand a member of the "ruling elite" is distasteful in the extreme. He is a Public Servant - no more and definitely not an elite. With his and his mate's latest iteration it would seem that the Public are getting poor value for money, not unlike that last idiot that went to the RBoI - Maklouf

He is definitely part of the 'ruling elite'. The policy he and his fellow clowns set has a massive bearing on our economy and social fabric.

Call him "elite" if you want - to me he is a servant. Paid by my taxes

The problem here is he and his mate are answerable to nobody and cannot be voted out. That makes them worse than Grant Robertson, they can make huge calls which are wrong (dropping the LVRs was one), then just absolve responsibility for being completely wrong and retain their massive salaries.

If you think he is our servant, how much power do you think we have to fire him? No need to answer, the fact is the NZ public has zero ability to fire him and Orr, which would mean he does not serve at our leisure. This is why I have been calling them "the worst kind of public servant", because it is a position which has no accountability, leading to arrogance and ineptitude. They could literally do anything they want to the NZ economy and monetary system and claim "but the tea leaves told them to" and carry on without a care in the world. That's more powerful than Robertson or Ardern, which should frighten us all.

Good stuff Blobs. Even Alan Greenspan was wrong and he admitted it. But look at the destruction it has caused. Still lingering today.

It's the disconnect between the enormous pain inflicted on thousands of young Kiwi families who have been robbed of the chance to have stability or disposable income or even a bigger family (if one at all) and the 'that's the way the cookie crumbles' from a guy who likely earns many times more than I do. I can assure you old m8 will have a far easier time making ends meet when he clocks out for the last time than myself or the other people I know slogging their guts out and just waving goodbye to the chance of a prosperous life in the middle, despite doing everything that they were 'supposed' to do.

Granted, it does needlessly personalise things towards one person in particular, but you get the idea. It's not just a spread-sheeting exercise for many people out there and we don't have the buffer of an enormous public sector purse at our disposal.

So he readily admits that they expected house prices to fall earlier this year but, inexplicably, opened the door for people to borrow with less of an equity buffer.

These guys really have no shame.

Honesty is the best policy

When we are taking away restrictions, we don’t have to consult.

really? perhaps that was the time they should actually have consulted. then avoided the problem caused, that everyone else could see plain as day, but not RBNZ

I don't think it would have changed the outcome. All the so called experts picked a downturn - shows how much worth there is in listening to "experts".They all go off historical trends which have no bearing on current events. You'ld think Orr and co could have been a bit more independent and analytical than they've proven to be

We are in hyper bubble so may be by having LVR even on FHB may be a blessing to them and restrain them for falling for FOMO and buying at ridicluse high price by extending beyond BUT Mr Orr by giving window to speculate for next 5 months is not good as house price by that time may go up again by another 10% to 30% as such is the momentum.

Just like in extreme when fear of fall Mr Orr came out to defend fall in house price by mortage defferal, low interest rate, LVR removal than by same logic why Mr Orr not coming out with introduction of LVR asap. WHY ?

So slap 20% on LVR's for FHB's and that somehow solves the issue? The only people that will be able to afford the deposits will then be those with lots of equity..

For FHB to be safe and to give opportunity, why not reduce LVR for FHB to 10% as possibility of negative equity possible at some time and for investors raise from 30% to 40% or even 50%

Yes, exactly! Trying to say the LVR's are there to protect the FHB's from the downturn and to protect banks from high risk lending. When is this magical crash going to happen exactly.

Orr and the RBNZ are full of s..t. and utterly incompetent.

They declared that they could not reimpose LVR restrictions before March, and a few hours later ASB declared that they will re-impose LVR restrictions immediately on speculators:

"ASB says it won't wait for the Reserve Bank to bring back Loan to Value Ratio (LVR) restrictions for investors in March. It is doing it now. ASB will move immediately to increase the minimum deposit required from investors to 30 per cent"(NZ Herald).

It is high time to sack these clowns at the RBNZ and put somebody in charge who knows what he is doing.

Just stop at sacking and see what happens. Maybe markets will spring up again.

Wow ASB is doing more than Jacinda and Orr! I’ll vote for them next election

Good move, but should have been slapped back on about 6 weeks ago.

I feel sorry for the ones who dont have family that can give them 100 to 200k for the deposit.

From what I hear that kind of assistance from

Well off ma's and pa's is quite common.

Isn't it sad that things have gone that way. An entrenchment of inequality.

Keep frowning Jacinda.

3 years of more frowning and trying to summon a human emotion, and she'll be looking like a melted candle

How's her child povvidy statistics going...?

If RBNZ had any interest in reducing speculation on residential property a 50% deposit for investors would be a nice start.

Or no lending on second homes unless it's a new build

A penny for Mr Wheeler's thoughts. Orr appears to be trampling all over his approach to the property market. I note the UK are aggressively implementing CGT across various assets.

I've been skimming the RBNZ Act using a few key search words. My initial conclusion is that the Finance Minister has a lot more power than he either knows and is not letting on, doesn't know what power he has which is my thinking or relies too much on officials advice who by omission don't inform him correctly or choose to inform him according to their own agenda. The US term deep state comes to mind.

Although most on this forum have been holding a torch to Orr there is another lot who I believe are also at fault. The RBNZ board. The also have quite some power to intervene. When viewing who they are they certainly have impressive credentials but if you are more concerned about your cushy job and salary then its best to stay mum. Add the board to people who need a torch taken to them

I'd be interested to hear more on this

The coming property crash is coming. This situation cannot go on. The bubble will burst sooner or later. All round the world, including New Zealand, interest rates are the lowest for 5000 years, share markets are sky high producing microscopic cash yields, borrowing money is virtually free, and we are told constantly to spend and then spend some more. The combination of the devastating Covid-19 and the bubble mentality is akin to the euphoria after the First World War where after years of stress and horror, the world went on a relief binge ending in the 1929 crash which almost collapsed the whole monetary system. In almost happened again in 2008 with GFC, and make no mistake, that shake up is still playing out today. It's not over yet, far from it. Indeed we are in the last phases of the GFC so I caution you all to step back and do the exact opposite to the mob.. As the sheep rush madly through the door, go the opposite way. Do not incur excessive debt, pay off everything, leave at least one years cash in reserve, and cut all necessary costs. If you can afford to buy a home then get the least expensive one that is still decent, and not get carried away. Whatever you borrow, even at almost 0% it still has to be paid back. Keep out of speculative real estate. Bubbles take a while to inflate as people are naturally cautious. But when the crash comes there is very little time to get out of the way. Remember Greed and Fear drive the market but Fear is by far the most potent.

Out of interest BigD, at what point did you go from optimism to pessimism?

I switched when the evidence became overwhelming.

We must face facts or live in an illusion.

It is better to be a pessimist and be wrong, than be an optimist and be wrong. .

So you’re referring to this year?

I picked you to be a property bull but you’re the first to jump ship in any serious way that I’ve come across. Most I talk to over coffee, some are cautious but many appear oblivious to the risk in the system right now/near future.

Around mid year the market did a 180 degree turn to everyone’s surprise. The damage was done by the collapse of interest rates, and the removal of LVRs . This was deliberately done in an attempt to head off a recession in election year caused by Covid-19. This has back fired spectacularly.

What is making it worse is the almost crooked deals by the banks who offer “teaser” loans at super low rates for the first year or two. What happens after that? In other countries 20 year loans can be taken out at a fixed rate for the whole term giving certainty to all parties and still with the right to refinance elsewhere if a better deal is offered. Pay off all debt now and then duck for cover.

Big daddy has been in and around property for a very long long time, has seen booms and busts. Unlike some of the Jonnies come lately's who spruik on this site (you know who they are)

He raises a bloody good point - our mortgage products are simplistic and designed to generate dividends for Australian parent companies, while the same banks overseas offer their customers discounted rates that scale with equity and for longer periods. HSBC's UK mortgage offerings, for instance, are far more interesting than what is on offer here.

Yeah.

Again, a negative of our small size.

Anything that goes up 20% in the blink-of-an-eye has a correction. It felt like a blink-of-an-eye - probably counts. The market might go down 10% then take out all time highs. It really is anyone's guess.

Your salient point of NOT getting carried away was borrowing exorbitant amounts at near 0% rates, seems lost on speculators. The greater fool theory works until it doesn't.

But if property prices drop, how will it affect things? How many people will be in negative equity? Will this affect banks, or will the government underwrite anyone in negative equity? The problem is the governments have allowed this to happen despite years of warnings.

It wont be a property crash it will be a currency crash. Stagflation or Hyperinflation.

Why do Kiwis believe their houses to be so valuable? It's ludicrous.

Since I wrote my last posts, the ASB has brought in LVR;s for investors.

There is no doubt that other banks will follow suit.

This will slow down investors somewhat- which it is designed to do.

As usual there will be unintended consequences.

Investors buy houses to rent them to those who choose to rent or cannot or will not buy.

Hence rents will rise rapidly as investment stock fills up and becomes in short supply.

This in turn will force more controls on rents ( as we seen already) and the merry-go-round keeps turning.

Excellent move by ASB, but why can't the Reserve Bank have this kind of foresight as well?

The RBNZ should be making the LVR's for investors 30% too, investors will be flooding the market again, and crowding out genuine home buyers again.

Maybe because they would have also had to do it for first homebuyers too. IMO banks should also be loaning an amount based on the income of the person. eg a House price to income ratio. If/when interest rates rise, some people could end up in big trouble.

It's a Faustian bargain. I have signed away 30 years of my working life to pay a mortgage so the thing I did it for has to have value to me. If I hadn't had to pay so much, I would care less. However we are all stuck making deals with the devils whether we like it or not.

One reason is because the cost of building is so high. Just work out how much it would cost to demolish and rebuild your house as new, and it is likely going to be higher than what it is worth on paper. My parents house had a rebuilt price worked out by a value of 2 million, yet when they sold it a couple of years ago, they got just over a million, which is what it was worth in the market, and is what they expected to get for it.. Some building companies and tradies are doing very well out of all this.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.