National Party leader Judith Collins isn’t particularly keen for the Government to enable the Reserve Bank (RBNZ) to restrict bank lending to residential property investors seeking interest-only loans.

Asked whether she would give the RBNZ this tool if she were in government, Collins said: “No, I don’t think so.”

Her reasoning was that government policy on housing shouldn’t be offloaded to the RBNZ.

“That seems to be what the current government is doing,” she said, also saying that most developers use interest-only loans.

Collins didn’t mention the fact that one the RBNZ’s main jobs is to regulate banks and promote financial stability.

She said removing impediments to increasing the supply of housing was National’s focus.

Finance Minister Grant Robertson on February 25 asked the RBNZ to provide him with advice on the risks interest-only mortgage pose to financial stability and whether restrictions - particularly on investors - could be applied.

Robertson on Tuesday couldn’t put a date on when the RBNZ would report back, but expected a response within weeks, not months.

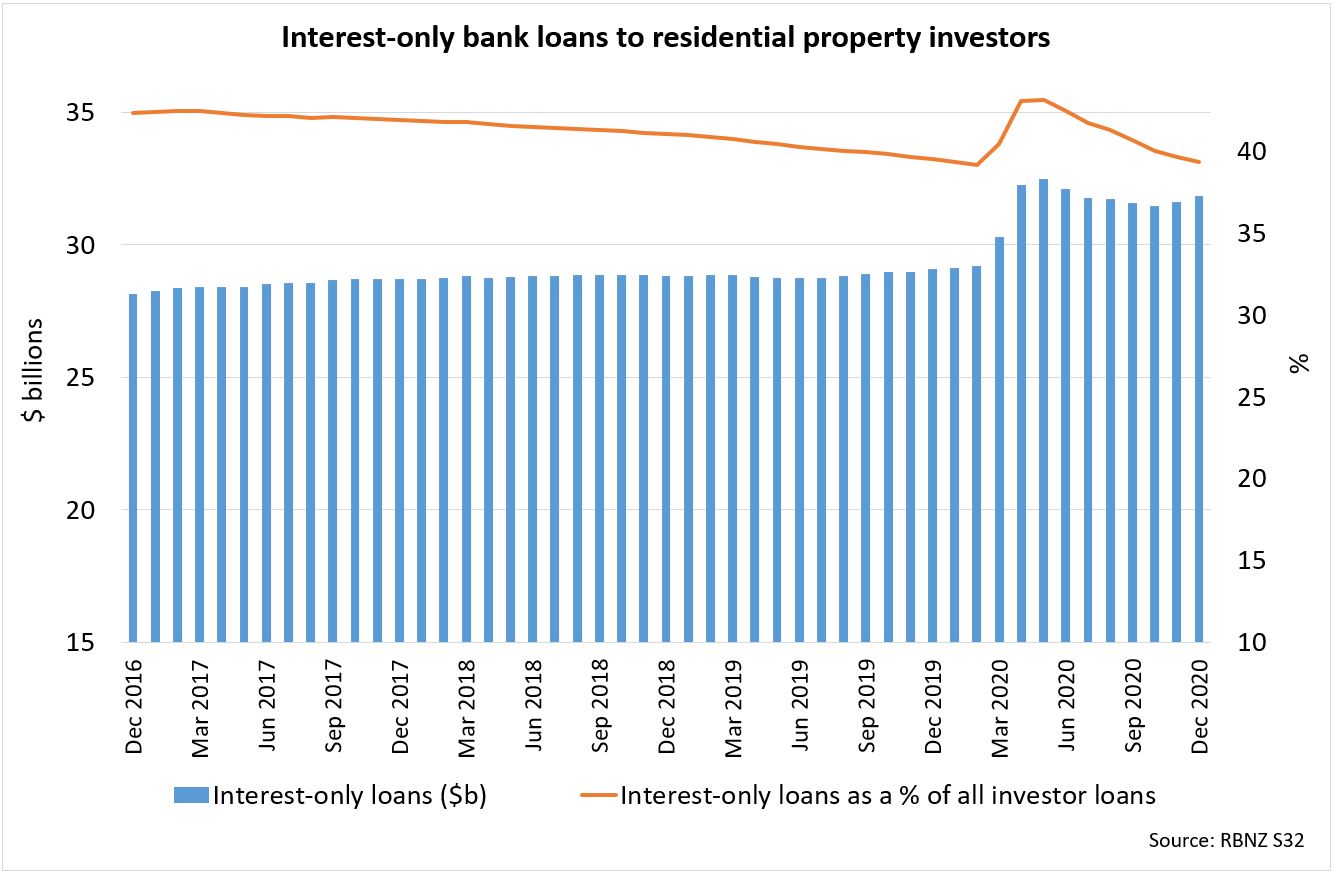

As at December, 39% of bank lending to residential property investors, worth $32 billion, was interest-only. This portion was on par with where it was pre-COVID-19.

Yet because borrowing against housing surged during 2020, the value of interest-only mortgages taken out by investors plateaued at a level about 10% higher than pre-COVID-19.

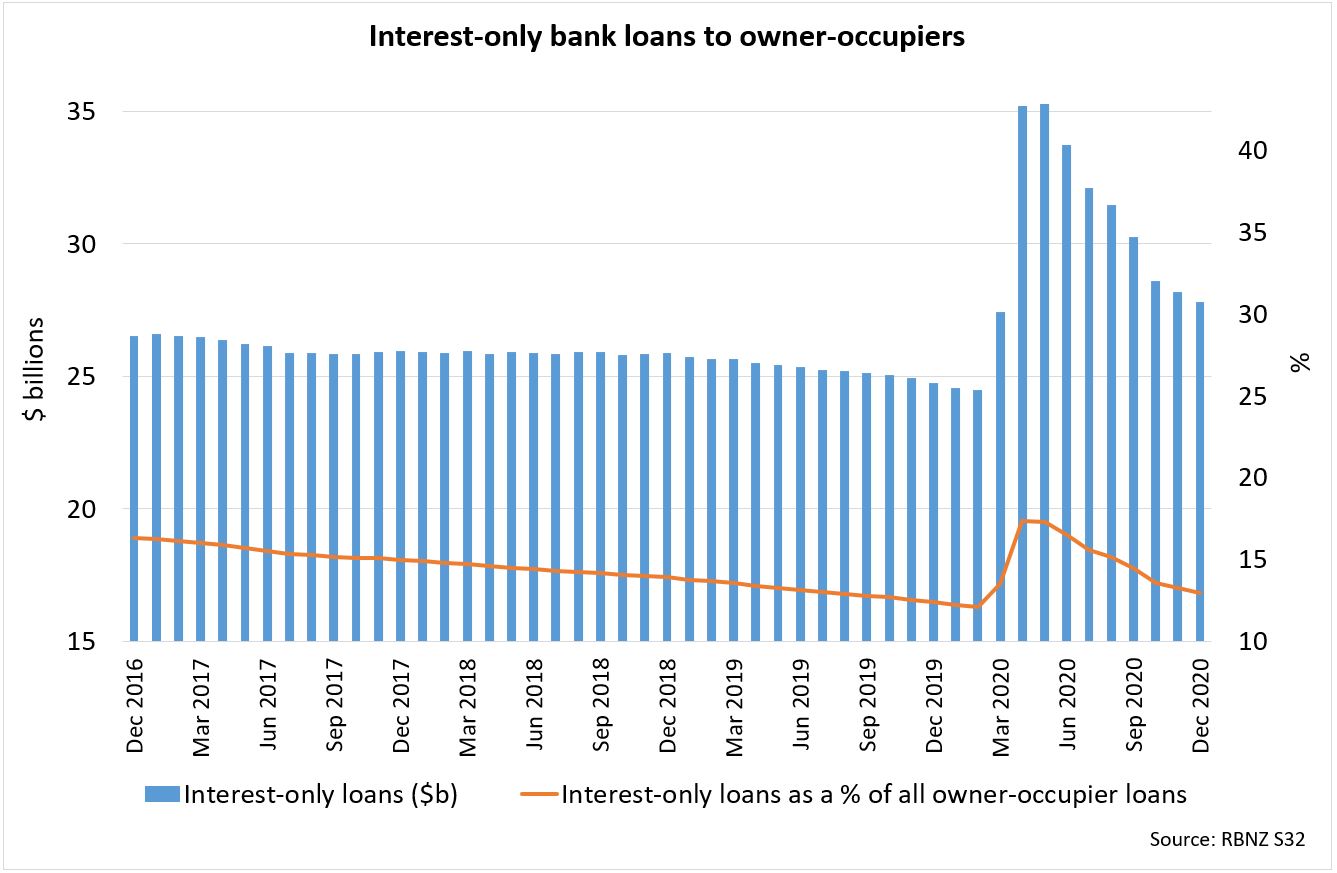

Only 13% of owner-occupier lending, worth $28 billion, was interest-only as at December. Yet the value of interest-only mortgages held by owner-occupiers was about 12% higher than it was a year earlier.

Note interest-only loans spiked for both investors and owner-occupiers during 2020 as the RBNZ relaxed bank rules to make it easier for banks to offer struggling customers mortgage repayment deferrals.

The Australian Prudential Regulation Authority put a cap on interest-only residential mortgage lending between March 2017 through to the end of 2018.

In December 2018 it said the temporary measure led to a “marked reduction” in the proportion of new interest-only lending, which fell to below its 30% threshold.

RBNZ Governor Adrian Orr last week told interest.co.nz the RBNZ hadn’t yet formed a view on whether it should restrict interest-only mortgages.

The RBNZ has also been tasked with reporting back to Robertson on whether it could apply debt-to-income (DTI) ratio restrictions to property investors.

The RBNZ has long wanted the Government to add these DTI tools to its macro-prudential toolkit.

124 Comments

Judith who?

Judith who?

[comment deleted by Ed]

Hi David and team,

again encouraging you to take a stance against value-less appearance based insults.

I just realised, this is the first time it hasn't been JA/GR/AO where I've seen it, good on her for getting into the news!

Officebound

Nice rebuttal. But I suspect the likes of the Herald cartoonist, Emmerson, is quivering in his boots.

Takere, you're responsible for this. An apology is in order.

Lol... National who..? you mean the disarrayed minority party?

National not keen for a single demand side measure as far as I can see

In the past I've noticed a strong correlation between National Party supporters and property investors - so no surprises really in Collins saying this.

Io... you do not have to look far to see that the property crisis could, believe it or not, be even worse than it is if National had won the election. Thier stance on immigration is no better either.

Yeah fully believe it. Cracks me up how National are nothing without Key, English and Joyce. They were the brains trust of the previous government - yet others like Collins/Bridges etc all thought they were key contributors to the winning formula. Clearly not.

The Key Government's policies were massive immigration to keep property prices rocketing up. This Government is not much better. When the borders are open again, the immigration doors will be wide open again to help the Ponzi housing market.

House prices have risen faster under Arden than they did under Key. In fact house prices rose faster under Clarke than under Key. It is almost like key had policies that actually worked but did not sound fancy whilst Clarke and Arden make policies that sound cool but don’t actually work!

They have ALL been hopeless. Key acknowledged the housing problem then went about enabling rapid rises in immigration, along with property speculation, to further dramatic increases in prices. Dont pretend he was any better.

Key went in to govt proposing to solve housing, and yes I voted for him, saying he was bought up in a state house. So what he done nothing.

It's all about Jacinda Ardern now, she has shown that she can out-National Judith Collins and drive prices higher much faster.

Not sure that's an accurate portrayal. Many property investors have gained millions under various Labour administrations. Most of the ones I know in Wellington quietly support Labour. Why bite the hand that feeds you? Among the propertied classes there is a sense of immense gratitude towards the current Govt. There is little doubt Jacinda can count on their votes in 2023.

One of Judith's properties was reported to have been rented to Brian Tamaki. I'm not sure if that means anything, but I find it creepy.

.

.

.

geez!!.. I'm really sticking my Orr in today lol

I hope she tithes 10% straight back to him, but not so he has more...

Different snouts same game, OPM for free....

Yep Zack that is creepy.

Nope

OK. So the banks are already privileged enough to lend money into existence. And Judy also believes that the principal repayment of debt is a secondary concern. All this while the taxpayer is implicitly on the hook for any largesse and while the currency is being debased.

What a clown. This is not 'laissez faire' or 'free market.' It's essentially crony capitalism where the ruling elite sets the rules in their favor and bugger anybody else.

That's incorrect!

Banks only lend money that mum and dad depositors put in the bank. And currently the banks are awash with customer deposits..

Second time you've written that - but given your pen-name I'm assuming it is that a p--- take?

Fiat lending, backed by things which wouldn't be of value ex fiat lending - a ponzi it is.

I presume you’re taking the pee? Anyone who thinks money is a scarce resource - or that loanable funds theory didn’t die 50 years ago - is not paying the slightest bit of attention.

PonziKiwi,

Read this. "In the April(2017) edition of their monthly report, the Bundesbank has belatedly joined the Bank of England in explicitly stating that the treatment of banks and money creation in most textbooks is wrong: banks are not intermediaries; they create money ex nihilo".

One more quote: "This refutes a popular misconception that banks act simply as intermediaries at the time of lending-ie that banks can only grant credit using funds placed with them previously as deposits by other customers".

Apparently the IMF confirmed this many years ago.

https://youtu.be/fOj_xp2jHl0

Sigh....they are all hopeless cronies!!!

Ha ha.. wait until many of them, have to be in gruesome Healthcare waiting list. Apparently, health can be super expensive to quickly drain those wealth.. many seeking 'tax payers' funded scheme

This Government is coward and inept when it comes to housing and monetary policy.

J. Collins has just reminded me that National is at least as bad.

And many people have the audacity to criticize me when I tell them Ii have never voted. I spent hours researching every single party last election and realised I would be ashamed to vote for any of them.

Fair enough. I voted - it was a prioritisation of the policies in order of the things I felt most important. Even though the party I voted for had one main plank that I strenuously disagree with, on balance the strength of feeling on the other policies I agreed with overruled that. Now I am free to criticise that party on the policies I disagree with and back them up on the things I agree with.

I wish other people would do this too - I'm sick of the binary good/bad criticisms of parties. For example, Collins makes a good point (if true) that developers rely on interest only during construction, so any "ban" would need to take this into account e.g. no IO loans on existing housing. She also makes a good point that the Government could approach the problem differently instead of relying on the RB to do the heavy lifting. That she's avoiding demand side solutions is just plain wrong.

All fair points. IMO the rules around new builds should be different and encourage new houses to be built. I wouldn't even have a problem, for example, with interest only loans for any new build as well as other incentives to build. But I think there should also be huge and numerous disincentives introduced to discourage investors from buying existing homes eg no interest only loans. We need to ensure, in the overall interests of NZ, that the process of being an investor/landlord always begins with building a new house.

With you on that.

I have built and bought new builds, the bank always applies the investor LVR regardless.

Good one karl, always thought new builds be incentivsed wether that be through interest free loans or tax incentives. Anyone buying family homes for rentals should not be able to claim on interest.

National simply don't 'get it'. Interest only loans should be restricted by the RBNZ - it is their job. Judith appears to be out of touch. I thought National were serious about looking for reasons why they lost the election. They are not listening.

They're struggling to see past their own self interest and narcissism as a political group. Therefore doing the right thing for the future stability of the economic system doesn't come into consideration (admittedly Labour are just as terrible...)

Blow out.

Judith has lost a good chunk of National voters to ACT and I am sure many more will follow. Phrases like “yes it requires historic debt” - from the election canpaign - aren’t a rejection of the current government; more like an endorsement. I can’t vote for political parties who support a property Ponzi scheme and ballooning national debt, sorry.

Bring it on. I'd love to see ACT as the opposition - they may not be the best, but at least there's a clear choice. Seymour is too principled to have policies that the masses will love though, so we'll be stuck with reddish purple and bluish purple for the rest of history.

Like many long term Nat voters, I'm completely disillusioned with them. Voted ACT last time not so much because of some of their zany policies but because I was so p...ed off with the Nats. They just don't seem to get it anymore & don't listen to their base. Terrible policies, lack of depth and ability in their MP's & more interested in infighting/leaking etc. Worst thing is if I looked at policies I should have voted NZ First, if only it wasn't always Winston first. At least I didn't vote for the current useless lot in power.

As I just wrote to reply to another comment, while this Government is coward and inept when it comes to housing and monetary policy, and against their very core of voters and supporters, J. Collins has just reminded me that National is at least as bad. The ongoing lack of attention by National towards the wishes of the majority of Kiwis is, sadly, quite clear. They simply are not learning.

Collin's isn't as intelligent as she thinks she is and National are going to be a train wreck as a party until they get rid of her as leader.

Collin's isn't as intelligent as she thinks she is and National are going to be a train wreck as a party until they get rid of her as leader.

It's downright reckless. The GFC was caused by the conditions that she appears to be promoting.

Isn’t “removing impediments to increasing the supply of housing” their policy from their previous 9 year stint? When can we call that idea a failure?

Labour:

Labour is like a Sisyphean stone, you really have to push them up hill - even then they just roll back down on issues like cannabis and housing. Sisyphus never quite got the stone over the other side now did he.

National:

Refuses to even try to try.

which makes National much smarter of course , on the basis of the analogy.

Agreed but we are working on the basis of 'like' aka simile. Well done for knowing your Classics though. U get a like for that lol :)

I agree you have to pick the battles you know you can win, but as it turns out that doesn't win votes does it ? Better to tell the masses what they want to hear if you want votes. Works for at least two terms in government as it turn out.

"Collins didn’t mention the fact one the RBNZ’s main jobs is to regulate banks and promote financial stability."

So true, that line fully made me lol

I enjoyed that line too. As usual Jenée is in fine form.

Start a party Jenée. Give us someone we can vote for.

"Jenée for prime minister"

We really need one now that we have National team A and National team B. It appears both have forgotten the young and the old - they are the puppets of the investors.

Surely most interest only loans are purely for tax purposes?

A better change would be to subtract inflation from interest tax claims (both interest received and paid). It is pretty unfair and the only justification to not do so is that it would be difficult as inflation changes. Why not assume a fixed inflation rate of 2% which is the RBNZ target? In almost every year in history that would be a better estimate of inflation than 0% is.

That's a bloody good idea JJ. They have kind of set the precedent for taking inflation into account with the likes of depreciation deductibility, so it's not such a big step to apply it to interest.

Tough position she's in,

Massive opportunity to tear strips out of govt for blowing up the bubble, while having policies that on balance would be worse...

What about residential new build construction loans by owner occupiers? This discussion is a bit more nuanced than “interest only = bad” and I say that as someone concerned about the level of IO loans to residential property investors.

It's just a blip in the March quarter but the overall trend for interest only loans are going downwards for both owner occupiers as well as investors.

The Market is wise to preserve their cashflow during a time of great uncertainty. The March quarter was when the virus problem became a mainstream concern coupled with intensive and extreme public policies.

Anyone who wants to make any good money should learn to read a graph, have a reasonable mind and stop reacting to blips in life. It helps too not to bark at the wrong trees.

Surely if you are a mum and pop investor and you have a mortgage on your own property it is best to have interest only on the investment property to claim as an expense. It sucks that you can claim what is mostly inflation as an expense but it’s hardly a worry for the RBNZ if there is enough equity over both properties.

Jimbo the problem is a lot of rents don't cover the interest,loan repayment and costs. So a lot of landlords are very exposed if interest only is taken away...and it has to be taken away because the problem keeps getting bigger.

Watching our pollies deal with the housing situation is like watching a ten year game of jenga... boring and you know what's going to happen...just not when!

When they go back to 40% LVR I don’t see a problem. If those investors lose out that’s their own problem, providing the banks can foreclose and get their equity back (which they should at 40%) then who cares. Unless RBNZ are worried about greater than 40% falls? If so investors probably the least of their worries.

hate to give you bad news Jimbo but the last governor wrote a paper where he discusses the return of house prices to the long term mean....

that would be 70% and greater falls...when real interest rates rise

that's why he introduced the lvrs

Interest rates rise with inflation. Inflation means rent increases.

What happens if we have stagflation - costs increase but wages don’t. You could try putting rents up but productive economy isn’t profitable under the economic conditions to provide meaningful wages increases to offset the increased general price level.

The last thing any lender wants to do is realise the collateral it has over any loan. Especially so in a market where 'the last price is the new market price' of all other security backing the whole loan book.

The lender might get its 40% back on the first fire sale, but what about the second?

That might be true but I doubt interest only has much affect. Even if you can afford the repayments would you want to if you are more than 40% in the negative? I’d declare myself bankrupt either way. (By the way I don’t have an interest only loan or investment property)

Well said.

But they're not 'investors', for the record. That suggests some kind of input. All they put in was debt, and they expect someone else (the tenant) to repay it. Then they expect a 'profit'. That's not an in-vest, it's an out-vest.

I watched some paint dry today just to liven things up a bit

Jimbo in the end the equity in a lot of investors homes won't help because it doesn't create an income.

Have a look at this video to explain how and why interest only loans have been used to screw the market...

Judith All Along

Who's been messing up everything?

It's been Judith all along

Who's been pulling every evil string?

It's been Judith all along

She's insidious (Ha, ha!)

So perfidious

That you haven't even noticed

And the pity is (The pity is)

Pity, pity, pity, pity

It's too late to fix anything

Now that everything has gone wrong

Thanks to Judith (Ha!)

Naughty Judith

It's been Judith all along

AND She KILLed Sparky TOO :(

About what's expected from Nationl the bank debt speculation party. Big question is... will Labour sell out to that agenda as well or not

Pretty much already have, no?

Judith's mates are property investors, of course she doesn't want to restrict I/O loans. The party must go on...

So investors are lending money (interest only) and buying investment property? That can’t possibly be right; Ashley told us they would all be selling up with the recent changes to tenancy laws!

JJ...he also said the vast majority of investors had interest only loans. Amazing that anyone would take any notice of anything he says.

Even been kicked out from opposition role have not learnt or may be so pressurised by their speculators supporters that forced to speak.

National party and it's supporters of speculators are trying to put pressure on government through opposition just like they were saying that legally cannot ban foreign buyers but was banned.

Shamefully corrupt as interest only is major contributor if not the only.

Making noise indicates that must have inside information that government is trying to restrict interest only loan and rightfully.

Has National party ever tried to cornered government on current housing ponzi - NO but when it comes to taking action to control the ponzi, though late are showing their true colour.

They did manage to put jacinda Arden in a corner to declare come what may will not put CGT but will they succeed now in trying to destruct any meaningful action to tame the rising housing ponzi.

So much of issue if Jacinda Arden skips an interview to some Mike ....really. It issue like this that media should take with Judith or whoever tries to derail action on housing ponzi.

Yup labour & national are both all in on the property ponzi. The only way this ends is via the TOP or the greens picking up enough votes. It may happen but probably 2026

Act will hopefully become the new opposition. National's voter base is really down to die-hard-oldies and speculators? I wouldn't vote Labour but I certainly wouldn't vote National~!!. As far as youth perspectives go, they vomit up Simeon Brown. Even Ilam, Ilam I SAY~!!, they don't even what National (Gerry Brownlee)!

I would like to see Act become the main Opposition. National are catering to their investor friends while the young and the old are squeezed. Labour are still thinking about what to do about the housing crisis and they have yet to ban plastic produce bags, straws (the small stuff), which could be done overnight, even though they declared a climate emergency. Lots of ammunition for Act.

“That seems to be what the current government is doing,” she said, also saying that most developers use interest-only loans.

I thought these were called "development loans", where the interest portion is due when the loan is settled. I can't imagine a developer just walks into the bank and takes out an interest only residential mortgage to fund their project.....

Er... that's exactly what they do. For cash flow purposes. Why is that a surprise? Developers are actually the enemy of "investors" by adding supply.

Actually I stand corrected. I see Westpac offer "construction loans" which are interest only lending, paid out in stages with interest bearing on the drawn down amount and principal payments owing on project completion. Not quite the same as a development loan, which is what I thought developers were utilizing.

Interest only loans are cancer.

Get rid of them!

They have their place, but NOT at the levels they currently exist~!! That's for sure~!!

Yes, as non-performing loans. Interest Only being a last resort to prevent an impaired loan. Mind you, one could reasonably suggest that plenty of investor lending would be deemed as impaired if rolled over to P&I earlier than anticipated.

I think they are quite sensible, you are basically using inflation pay it off. If you’d taken one 30 years ago you would be pretty happy about it I imagine.

Interest only loans are wonderful, they are a great way to build wealth

Judith should be playing the role of the opposistion by raising and talking about rising house price but what she does was enjoying the party/ponzi and the minute she came to know that government is plaining to control speculative demand, panicky and even on Sunday gets active to put pressure on government to avoid controlling speculators .

Not really surprised as every knows knows she supports rising house price for biased vestetd interest.

"Father, forgive her, for she does not know what she is doing." INFACT SHE DOES.

Yes showing her true colours

Judith has already been beaten badly. I am guessing she's being kept in position for now to make Labour complacent

Both parties are far too right wing to do the right thing.

Fritz, you might want to move to China, I believe they are significantly more left leaning

What is your point?

The Labour Party are centre-right in many of their actions, if not their rhetoric. A shift to the centre left, along the lines of many northern European nations, is a long way from authoritarian communism.

What you, and to be fair most people, don't get is that the neo-liberal ways of the past 40-50 years have failed society as a whole.

Only by the government massively lifting it's house building programe, including building a lot of shared equity housing, will the issue be addressed.

One should keep in mind Einstein's quote about insanity...

China is looking reasonably appealing and given the absolute cluster that western economic leadership is turning into, moving to China for work might actually be a wise move for young people (if allowable). Prospect there are probably much better than in NZ or anywhere else in the anglosphere. China likely calling the shots on the world stage for the next few hundred years while the USA implodes the next few decades (and us along with them).

Interest only mortgages are wonderful for accommodation suppliers, leave them up to the choice of the mortgagee

Yvil...like a wild tiger, a wonderful thing but very dangerous and unpredictable.

Just in case anybody thought there was any hope for our young peoples future you can now be sure there isn't.

I feel thst way Karl - and I'm old.

I am not young either but it should be our kids (and other young people) we are worried about.

Yeah you have to think the prospects for young people in this country might be the worst they ever been (in the country’s entire history).

Severely overpriced houses, disfunctional two-faced politicians, and central bankers acting like a type of rogue mafia who protect only their mates with assets already. All while the young people are trapped in the country and can’t leave because most borders are closed. Rent slaves in their own country.

And the definition of young has also changed quite a bit. Many of my friends in their early 30s are renting with not much hope of owning a house. One generation ago, people in their 30s had already been thinking about upgrading from a 3br house to a 5br one with a nice deck.

In our early 30s we're the backbone of the economy, we're supposed to be having kids and a house and building wealth.

Yet we are still being treated as misbehaving kids by landlords and politicians (including those in their 30s). We're getting sick of everyone telling us that they know it better...

yes this is often ignored. people love to run the numbers as say "houses are just as affordable as ever, due to low rates". But what that fails to factor in is that previous generations were not delaying home ownership due to student loans, having to spend 10 years saving for a deposit.

I find in fascinating talking to my parents about their journey to homeownership. They both finished higher education with no debt. In their first jobs they spent 18 months working full time, smartly took a 6 month contract in another city (which had accomodation paid for). This allowed them sufficient time to save enough for a 30% deposit on a house. In their mid 20's. Allowing them to pay of a sizable portion of the mortgage by the time they were 40~

The reality for young people now is they will likely leave higher education with some debt (up to 50K) delaying the window for home ownership. Then the big hurdle is the deposit. It is now estimated that it will take a decade for people to save that money (assuming they can save faster than the deposit requirement increases). They will then purchase with a fraction of the deposit (risky) at a later point in life, anywhere between 10-15 years later.

Instead of paying off 66% of the purchase price over 30 years, they realistically need to pay off 80% of the purchase price in 15-20 years.

Ah yes, I love stories from the previous generations. Especially when presented with a fake concerned face (a la Jacinda), or in a condescending tone.

The other day my coworker (in her early 50s) mentioned how it was very difficult for them too back then, they "had to save so hard" when they were paying off their mortgage and "barely had any money left at the end of the month". The caveat: she was 23 at the time.

Yes, I think this is a really important point. You often hear people say things like 'it's always hard to buy your first home.' Well yes, but that's true because the majority of people tend to try to buy their first home as soon as it is economically feasible. if every individual buys first home at a point in their life when buying a home is a stretch for that individual, then it will be true that it's 'hard for everybody.' But objectively speaking, having to save hard for a few years before buying a home in your early 20s is a lot different than having to save hard for 10 years in order to buy a home in your early 30s. Just like I get annoyed when people say things like 'it was hard for us, our first home was a run down place and we had to sit on beer crates etc.' Sure, that sucks. But having to do that for a few years in your early 20s is one thing. Having to live in run down dumps with flatmates for over 10 years and then moving into (yet another) run down place if you are lucky enough to buy in your 30s is a whole different story.

Well now we know what the labour demand side policy is going to be next week. Whilst its been mulled over - labour has not officially asked the RBNZ to limit interest only loans - but with Judith already opposing the policy- sound like next week Labour will announce that policy.

It will be the right thing to do.

Interest Only fuels housing ponzi.

Some people here seem to love interest only....

Be interesting to see how quickly banks stop interest only lending if/when prices start falling.

Even if at 40% LVR.

First few days into March, +1k on the border arrivals vs departures. Should help to reverse the 127k net loss in 12 months. With the amount of building going on, shouldn't take long for any demand to be mopped up.

Interesting to note in Dec FHBer # of borrowers was up 20% and Investors up 30% YoY according to C31. If more people are buying their first home i.e. moving out of rented accommodation then there could be a rental glut on the way?

E.g. Dec 20 - 3338 FHB's took out mortgages @ $1.69b versus 4995 Investors @ $2.45b. Assuming the FHB's are couples, and investors buy 3 bed houses, the loss of tenants from the rental pool could equate to approx. 1112 properties. This is while investors have potentially purchased 4000+.

Kudos... Only Jenee could highlight...

Exposing.... as if Judith does matter !

Both Lab & Nat, use the same song sheet.. the focus of their delaying=time=cost money is that technique of bickering/blaming each others with relate to supply & demand, both tweaking and distorting when the balance set look to change, both a short term thinker, gainer.. the long run cost is not in the equation. Leave it to RBNZ.

All others regulatory means? just good for discussion; LVR, DTI, Bank CAR, Stress test of 80%, TD deposit, Rental freeze, Bright line test, CGT..

It feels to me like both parties are just playing a game. They are hardly different at the end of the day, perhaps the whole childish nonsense in parliament is just a charade.

Both parties are so heavily invested in the status quo

They have to play the the childish game to get paid and enjoy the perks.

Politicans as breed flock together - NO one is different and may be this democratic system has run its course and time for revamp for Good or for for bad but system will change and may give rise to new evil.

Felt sorry for Kiwis, they need to ask PM about the ideal DTI number for NZ. Here's a thought:

- NZ needed more Healthcare professionals.

- Young graduates, still have to pay student loan, resides mostly in big cities, attend hospital for further training.

- Be a couple, start family.. difficult chance without leveraging from Bank mum & dad.

- Salary grow slowly, housing cost? one word: wow, imagine for the next year graduates, without abating.

No wonder, OZ banks started to show Kiwis to eat tomatoes all years to get to 'the ladder', some suggesting to coupling without a kid/s, some banks even (may be try to be inclusive)..give an idea to switch their own gender preferences if necessary, eg. as long as partner is rich, all in order to secure loan. Sweet nectar of NZ.

From Marketwatch:

The (US) administration’s tolerance of higher long-term interest rates is all but certain to arrest the stock market’s advance and send share prices lower. Long-term rates already have started climbing. It is also likely that short-term rates will rise in an effort to arrest possible inflationary trends resulting from fiscal expansion and a weakening dollar.

What does this mean for investors? The famous 1987 and 2001 Alan Greenspan puts, and the 2008 Ben Bernanke put—Fed policies that effectively set a floor under stock prices—have ceased to exist. Powell most likely will be replaced by a progressive Democrat when his term ends next year. But even if he remains Fed chair, the Fed put is now kaput.

What Judith thinks only matters if Jacinda keeps letting the Property Investors Assn. dicate the tax and monetary policy of her government.

RE is and has very powerfully lobbying access to ministers, experts, media and people who matter.

Best example is Judith lobbying for speculators as gets their bread and butter from them. Need leaders and not politicans like Judith and may be also Jacinda Arden, who thinks about country than themselves.

Jacinda Arden and her team when came to power had some freshness but now are trained hard core politicans, in fact now better than Judiths of the opposition as have mastered the art of denying and avoiding by lying and manipulating.

Mr Robertson's delayed announcement to control speculative demand next week will expose them as will turn out to be toothless tiger.

Removal of Interest Only Loan and DTI just like LVR and that too in in timely / QUICKLY is the key and not by giving window of opportunity to speculators to ramp up before the deadline.

Most probably will only talk about supply and RBNZ and some promise for future - journalist should ask them that will have future only if they act now and do not screw up the present.

Wait and Watch.

Thanks Jeneee for the article so can have discussion on the same and government if plaining to act and taking feedback, will know that doing right thing just as they did by banning foreign buyers and silenced all those who said was not possible or predicted doomsday if banned - similarly landlords tried to put pressure initially when laws / policies were been framed to protect tenants that many landlords will dessert or not rent but after the event nothing happened - tried to blackmail but didn't work SIMILARLY restriction on interest only loan and DTI will work not allow to be blackmailed.

With majority Jacinda Arden has got an opportunity to do right thing, for ince.

"She said removing impediments to increasing the supply of housing was National’s focus."

Again words with no detail or any action plan. Standard Collins, just doing it for the sound bite.

Time for her to step aside.

Interest-only loans are a non-issue.

What do you think the first 5 years of a principle and interest thirty-year mortgage look like?

We should be more concerned about why the length of mortgages have to increase.

Both interest-only loans and longer mortgage terms act as house price accelerants in a restrictive supply market.

Focussing on interest-only is only piddling and fiddling while house prices burn.

What do you think the first 5 years of a principle and interest thirty-year mortgage look like? - there's a pretty significant difference between interest only and interest and principle when you're looking mortgages based on todays prices

I'm saying leave them. It's a distraction in the bigger picture. They, like extending the term of a mortgage, have an inflationary effect on house prices when you have a restricted supply market.

If you are going to remove them, then you should also fix the length of term as well, if the reason for doing any of this is to control house price growth.

OR we could focus on the real problem which is removing the restrictions to supply, and then what they would find is finance terms and length of mortgage has very little impact on house price growth, just like it does in jurisdictions where supply restrictions are low.

Of course they are not keen, it is their main line of business.

Please do it ! We don't want interest only mortgages.. this could be only used as temporary emergency fall-back; when they r in financial difficulty ...

The 'interest' itself is soo minimal - and now they want to pay only that minimum interest.. crazy bloodsuckers !

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.