The Reserve Bank is delaying its planned consultation on how it could enforce debt-to-income (DTI) restrictions and interest rate floors on banks due to Auckland's Covid-19 Delta variant outbreak.

On August 3 the Reserve Bank announced the signing of an updated Memorandum of Understanding (MoU) on macro-prudential policy between its Governor Adrian Orr and Finance Minister Grant Robertson. The updated MoU adds debt serviceability restrictions to the Reserve Bank's list of tools.

Also in August the Reserve Bank said it planned to consult in October on implementing DTI restrictions and/or interest rate floors in an effort to provide further comfort that home loan borrowing is sustainable.

However, the consultation is now on ice until mid-to-late November with a Reserve Bank spokesman telling interest.co.nz; "Given the disruptions from heightened COVID-19 alert levels this [consultation] timeframe is being revisited."

The Reserve Bank has coveted a DTI tool for years and its most recent formal request for one was made to Robertson last December.

An interest rate floor involves settling floors on the test interest rates banks use when assessing borrowers' serviceability. The Reserve Bank spokesman says this will also be canvassed in the planned consultation. It's currently up to banks to decide what interest rate floor they want to use.

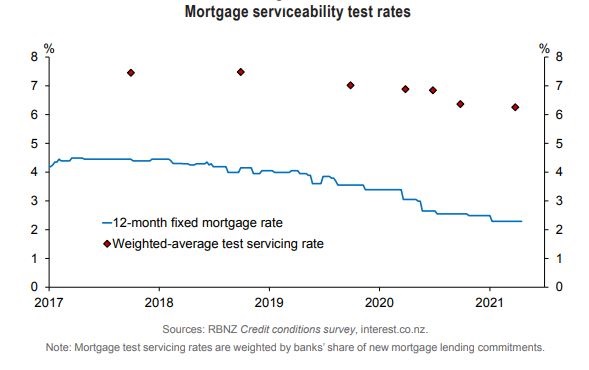

The concept of a test rate is that when considering home loan applications, banks calculate the ability of the borrower to repay the loan at a higher interest rate than current rates. Thus the lender looks to satisfy themselves that the borrower could maintain their repayments if interest rates rise. Lowering test rates increases borrowing capacity and increasing them decreases it.

In June an ANZ spokeswoman told interest.co.nz the bank's test rate, used across all types of homeowner borrowing, was 5.8%. An ASB spokeswoman said ASB's was 6.45%.

The Reserve Bank published the chart below in its Financial Stability Report released in May.

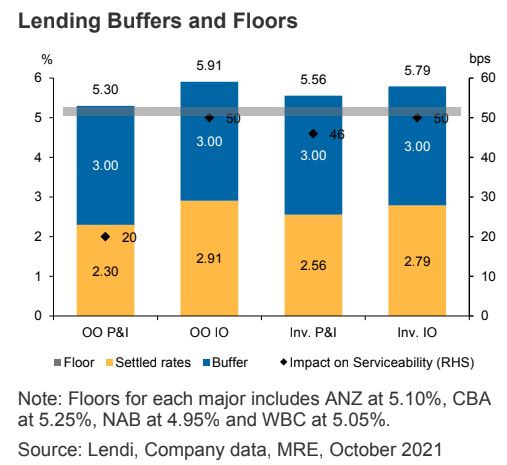

Meanwhile in Australia where the parents of New Zealand's big four banks operate, the Australian Prudential Regulation Authority (APRA) on Wednesday announced an increase to the minimum interest rate buffer it expects banks to use when assessing the serviceability of home loan applications.

APRA has told lenders it expects they will assess new borrowers’ ability to meet their loan repayments at an interest rate that is at least 3.0 percentage points above the loan product rate. This compares to a buffer of 2.5 percentage points that has been in use.

APRA said the decision reflects growing financial stability risks from lenders' residential mortgage lending.

In a report on the APRA move, Macquarie banking analysts suggest it will reduce borrowing capacity by 5% to 6%. Macquarie also notes that 22% of new lending was on done at a DTI greater than six times in June this year.

"The regulator also noted that should the flow of loans at high DTI continue to grow, further macroprudential measures would be considered. While this step is likely to have a modest impact on credit availability, it may be enough to achieve the objective if it weakens confidence and moderate’s property price appreciation," Macquarie says.

The chart below comes from Macquarie.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

39 Comments

"RBNZ's plans for consultation on its debt-to-income restriction tools on ice"

Gareth Vaughan, Why be surprised....do we not know that they have no intent and are looking for reason and will always find one and what best than pandemic / lockdown.

RBNZ is consistent in their action of supporting the housing ponzi..even their inaction and delays are in same direction.

Both the RBNZ and the Labour government have basically used Covid to "Do Nothing" and "Lets wait and watch". So now we are going to come out of lockdown just in time for summer and the usual property market that's pumped and ready to roll.

The only good thing to come out from do-nothing Labour.

It's pathetic. In my job, we are working close to normal productivity, and hey, there's a thing called 'Zoom' that works pretty well for meetings...

We are a free country last time I looked. Why do they need to bring the rules in at all. What right do they have to control the private actions of borrowers ???

None, we are not communist Russia or China last time I checked.

Another opportunity squandered.......

Depends on which side you are in. Home owner or renter.

They know they will work immediately so they are trying to put off.

Great news!

We wouldn't want to fall under the illusion that these morally bankrupt central bankers have any intention of doing anything about the asset bubble they deliberately planned and methodically engineered.

Here is a little throwback to a year ago, not long after the press conference where RBNZ Chief Economist Young Ha was unable to conceal his unbridled enthusiam for blowing an asset bubble.

https://www.stuff.co.nz/business/300131658/reserve-bank-would-rather-do…

The borders can't open soon enough.

What do borders have to do with how they do things?

It means those who don't benefit from monetary policy for the asset rich or from fiscal policy for the iwi or the poor are free to seek better opportunities elsewhere.

New Zealand is not an ideal place to be part of the productive middle.

And you think the same problem doesn't exist any where else? House prices are through the roof all over.

The grass is not always greener on the other side.

Houses are a bit expensive in many other places. But very very few places are as much of a waste of time as here.

Having lived in Australia and the United Kingdom I'm well aware of what the grass is like elsewhere. Maybe you should clue yourself up.

Why don't you shift yourself out of this country if you haven't already?

We won't miss you.

Great argument.

- Look, we have one of the worst vaccination rates in the developed world, should we do something about it?

- Why don’t you move somewhere else?!

Not a housing related analogy, but I’m sure it’s easy to find a data, that imho, shows that the only place within the developed world doing worse than us in housing is Hong Kong.

Is he Don's brother?

When the boarders reopen there will be more people trying to get in than want to get out. I hear there has been a class action lawsuit started re the MIQ and people that are trying to get back in and cannot get back fast enough.

borders..

Worrying about the correct spelling these days is like worrying about all the deck chairs lining up perfectly on the Titanic.

Perfect for some heated summer prices!

Caviar for all!

How convenient.

Pathetic.

What a disgrace. Shameful. Pathetic. Criminal.

Wouldn't it be great if a journo did a really big dig into the whole political class and this property ponzi debacle.

Agree 100% but all are a part of the system - corrupt system

The ineptitude of the RBNZ is eye-watering. I have developed a very low opinion of Orr and his muppets in the last couple of years. but they still manage to disappoint at every step.

They seem to be doing everything they can in order to prolong the housing Ponzi, as long as possible, blatantly ignoring the long term consequences to financial stability and the whole economy; this is also seen by the latest increase of the OCR by 25 bps only, while an increase by at least 50 bps was necessary.

Their tardiness in increasing interest rates will force them, later on, to raise rates higher than what they are currently hoping/planning to do. A peak of the OCR of 1.75% increasingly looks like wishful thinking, and I would not be surprised at all to see a peak between 2.5% and 3% by end of next year at the latest.

Don't agree with this. There's no way the OCR will be anymore than 1.5% by the end of next year.

In fact it might be lower than this as:

- the covid pain on business worsens: a lot of SME's are really on edge now, and are eating in to savings etc.

- China's economy weakens significantly, as it looks like doing. So best case a significant weakening, worst case a financial crisis (and then all bets are off in terms of the OCR)

Also, the construction sector will start to get whacked if the OCR was to go above 1.5%, with resulting impacts on employment (remember employment is part of the RBNZ's mandate)

Why ? If Covid has taught me anything its you can throw logic and reason right out the door. The OCR could be just about anything by the end of next year. Saying it cannot be more than 1.5% is laughable. We are going to get hit with another couple of rises before February.

I'm not saying I AGREE with what I think will happen.

I'm saying what I THINK will happen.

And you are flying in the face of the evidence of the past few years, where the RBNZ has moved in a very cagey manner to tighten things when it has. You allude to a volatile and unpredictable world, which is true, but the RBNZ moves in very predictable and cautious ways.

Why do you think they will suddenly fly in the face of that consistent behaviour?

You also have to keep in mind that CPI is only one part of their mandate. Financial stability and employment are also important aspects of that. Also, much of the inflation at present is supply side rather than demand side.

A rapid rise in the OCR to something at 2% or higher would challenge both their financial stability and employment mandates. It will also lead to pain for the export sector, which is something they won't want.

I strongly maintain my view.

It feels to me that your view is one based on wishful thinking rather than realism.

The RBNZ can essentially do what they want with very little science given the current Dual Mandate.

Like it or not homeowners and the like are enjoying every bit of this endless pie.

A diminishing cohort in NZ - same as US : Link

OUCH! America’s middle class now holds a smaller share of US wealth than the top 1%. Middle-class financial security has eroded in past decades, saw their combined assets drop to 26.6% of national wealth while Top 1%’s wealth jumped to record 27% of total. https://bloomberg.com/news/articles/

Manhattan Apartment Purchases Hit Three Decade High Amid 'Buying Frenzy

Yep saw them talking on the TV about "Getting Americans back into the middle class", wow how bad is it over there that you now have to struggle just to stay in the middle class. Parts of the USA looking really 3rd world now on the streets, pretty shocking with just drugged out homeless people.

I'm starting to think of attempts to slow the decline of the middle-class as a death throw ; we are not heading back there. I was born in the early 60s, so my conditioning is quite the reverse, but the World Economic Forum (you will own nothing and be happy) are probably going to end up right; most of us will be content enough with UBIs and living day to day not earning much or saving anything, maybe making a few extra credits training robots to do day to day tasks.

These last years of rising populations competing and working hard, trying to save and borrow and "get ahead" so they can buy a house (and preferably a few other families' houses), while resources run down, space get's tight and more of us fall into despair, will be seen in the future as an appalling Wild West scenario. An immoral time where those who didn't make it lived under plastic. This is mostly the painful giving up phase, not the fight-back.

Death throes..

Oh, yes, thanks for the correction.

It's essentially irrelevant to homeowners like me. Sadly those with multiple properties like to claim to speak on our behalf.

The only people who benefit from rising house prices are those looking to downsize, and those with more than one property. For everyone else (~90% of the country?) it's at best irrelevant. Sure my net worth goes up, but I still have 1 house and the same mortgage outstanding.

Back to the story - very disappointing and hopefully just a temporary set back - DTI will be a very powerful tool if used correctly and can make the country a better place.

Why not just implement the DTI immediately, then they can do whatever they want with interest rates.

At least with a DTI, the amount you can borrow will be limited so they'll have the ability to go down again in the future.

Begged for it for years. Now goes silent. Yes the speculators will get a hammering. But everyone else would feel the noose of debt/mortgage/rent enslavement loosen off their businesses and personal incomes.

Has Labours war cry changed to "Let's do nothing"...

Yep.

Could limit the extent OCR needs to be raised, which would be helpful for exporters.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.