Governor Anna Breman says the Reserve Bank will closely monitor the impact of the changes announced to banks' regulatory capital requirements on lending interest rates and banking competition.

The Reserve Bank unveiled the decisions from its capital review, announced in March with a consultation paper issued in August, on Wednesday. That's little more than two weeks since Breman officially joined on December 1. Nonetheless she fronted a media briefing, and spoke confidently about the changes.

The Reserve Bank says the changes will reduce banks' funding costs by up to 12 basis points, and boost their lending capacity, which it maintains will result in lower interest rates for borrowers. It's expecting an eight basis points decrease in lending interest rates. Breman says the Reserve Bank will be monitoring closely.

"We will look at trends in the amount and prices of different capital instruments issued, we will look at trends in lending rates also by sector, we will look at banks' profits and return on equity, we will also look at changes in observed risk weights and comparisons between [internal ratings based capital] modelling and standardised [capital modelling] outcomes." (See internal ratings and standardised capital modelling explained here).

"We'll also look at lending trends across the groups [of banks and deposit takers] and the extent to which market share is changing. That's one way of measuring competition, if you can see market share shifting over time. And this will also be published every two years by us," Breman says.

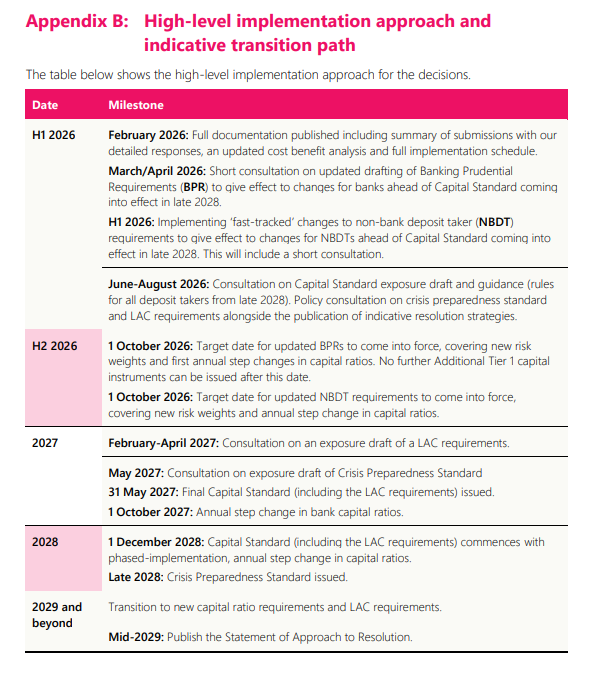

The capital changes will take effect between 2026 and 2029. (See Appendix B below for details). Capital is the form of funding that stands first in line to absorb unexpected losses banks may incur.

Asked about the Reserve Bank's 2019 capital changes Breman says she didn't have a view on them prior to joining the Reserve Bank.

"What I've done is of course I've read international reports, I've had excellent discussions with staff and the board. So when we came to this decision I felt very comfortable that this is the right decision for New Zealand, with the developments that we had, not least in terms of supervisory activity that has been strengthened over the past six years, and also with the new Depositor Compensation Scheme."

"So the key message with this new decision is that we are more aligning with international standards, we are very much adjusting it to the need of the New Zealand economy, and the structure of the financial system here. So I feel very comfortable making this decision together with the board," says Breman.

'We do not operate a zero failure regime'

The Reserve Bank has done away with the explicit assumption included in the 2019 capital review that New Zealand is not prepared to tolerate a system-wide banking crisis more than once every 200 years. Breman described this as "rather uncommon" and "not [a] normal international standard."

"We have a low appetite for events that could create systemic risks, those are events that could materially damage financial stability, but we do not operate a zero failure regime. In terms of the risk appetite, it has evolved so we are moving away from that 1-in-200 approach, but it doesn't mean we have a high risk appetite. On the contrary we do have a very low appetite for events that could create systemic risks," Breman says.

In the paper outlining its decisions, the Reserve Bank says; "We have a moderate tolerance for risks that may lead to the failure of regulated entities where the impact is understood, manageable, and will not materially damage the financial system. This approach supports the efficient operation of the financial system through enabling entry, exit, and expansion of participants."

(Also see; Whilst the push for greater bank competition is good news, it may also come with increased risk).

Too big to fail

The big four banks - ANZ NZ, ASB, BNZ and Westpac NZ - are regarded as systemically important and thus have higher capital requirements than other banks. (See figure 1 in this story).

A systemically important bank is one whose failure might trigger a financial crisis. Such banks are colloquially referred to as "too big to fail." The Reserve Bank has been using the "systemically important banks" term since before the global financial crisis.

OBR still in the toolkit

Breman was accompanied on the media call by Angus McGregor, the Reserve Bank's Assistant Governor for Financial Stability, and Jess Rowe, its Director of Prudential Policy.

McGregor says the Reserve Bank was "still building out" its crisis management framework under the Deposit Takers Act, to expect more news on whether the Reserve Bank is going to develop a bail-in tool next year, and its open bank resolution (OBR) tool "absolutely continues to remain a tool in our toolbox."

The Reserve Bank has previously said it might rename OBR "to better reflect its intended role, to support continuity of access to deposits in resolution."

Bail-in would seek to recapitalise a failed deposit taker by writing down, or converting into ordinary shares, selected capital instruments and liabilities of a deposit taker in resolution. That means bail-in allocates the costs of both stabilising and recapitalising a failed deposit taker to its creditors rather than the public purse.

With some reductions in the amount of capital banks will need to hold against agriculture and small business lending, McGregor says the Reserve Bank expects to see some changes (improvement) in banks' lending appetites in these areas, but isn't in the business of directing where lending should happen.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

2 Comments

On the contrary we do have a very low appetite for events that could create systemic risks," Breman says.

OK, well back that up by charging banks a premium for providing them with a deposit guarantee scheme.

Why should the taxpayer provide free insurance when they're making multi-billion dollar profits.

Company Directors and Boards take note, this is setting risk appetite well, and is half your job alongside strategy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.