By Gareth Vaughan

Ten years ago, on September 15, 2008, Lehman Brothers collapsed. A financial world where US sub-prime mortgages were already spooking people, lurched into full blown panic as what became known as the Global Financial Crisis (GFC) took hold.

Down here in New Zealand we reacted, nervously, to the events unfolding in the global financial capitals. Some New Zealanders, however, had front row seats in these capitals. One was Antonia Watson, now managing director of retail and business banking at ANZ New Zealand. Another was Christian Hawkesby, now executive director and head of fixed income at Harbour Asset Management.

Watson, who worked for Morgan Stanley in Hungary, was visiting New York. She recalls watching the news of the Lehman collapse unfolding over the weekend with her husband, followed by the bailout of Merrill Lynch by Bank of America.

"To me - naively - it felt like Monday morning was opening with things largely sorted out," Watson says.

"We happened to eat breakfast on the Monday morning in a diner across the road from Lehman’s state-of-the-art head office building. It had been purpose built for Morgan Stanley but we had never moved in, selling it to Lehman after 9/11 when everyone was reducing concentration risk in Manhattan, and Lehman needed new office space having lost theirs in the attacks. My main memory from sitting in the diner was that the whole area around the Lehman building was strangely quiet."

"As it turned out the action was a couple of blocks away outside the Morgan Stanley headquarters at 1585 Broadway. That’s where all the news trucks were, hoping to see us all walking out of the building with our cardboard boxes, because after Lehman and Merrill, Morgan Stanley was next on the list of not being likely to survive in its current form. My husband went past Lehman again later in the day and did see people leaving with cardboard boxes," says Watson.

She recalls Morgan Stanley's share price was hit hard that day and over following weeks.

"My observation as I watched my colleagues’ reactions in the office was the lack of a 'plan B.' There was a lot of fear and uncertainty. So many people had 20+ year careers and much of their wealth invested in the firm."

"There was no doubt that 'RIFs', reduction in force - our code for job losses, would be on the horizon as well. The interesting thing was that amid the fear and uncertainty there was also the odd colleague who took the opportunity to buy Morgan Stanley shares rather than sell in a panic - they would have done very well," Watson says.

"Morgan Stanley did survive largely intact. But in doing so it became a traditional trading bank, regulated by the Fed, and had a significant capital injection from Mitsubishi UFJ. I exercised my own plan B in early 2009, returning to NZ to work for ANZ."

A view from London

In September 2008 Hawkesby was on the other side of the Atlantic working at the Bank of England (BoE).

"That weekend of the Lehmans collapse I was shifting roles from running the Deputy Governor’s private office, where I had been involved in the Northern Rock rescue and measures to save HBOS, RBS, and Lloyds TSB, to being chief manager, sterling markets where I was part of the crisis teams advising how to buy the assets for the BoE’s QE [quantitative easing] programmes," Hawkesby recalls.

"The big lesson to central banks and regulators is the difficulty for markets or the public sector to predict when exactly a financial crisis will strike," says Hawkesby. "The Bank of England had been writing for years about the risks that ended up crystallising during the GFC."

He points to two articles written in 2001 that "seem prophetic" with the benefit of hindsight. The first, on page 137 here is entitled Risk transfer between banks, insurance companies and capital markets: an overview. The second, on page 117 here, is entitled The credit derivatives market: its development and possible implications for financial stability.

"But when markets, even in the face of large imbalances and vulnerabilities, continue to perform strongly for years on end, then the warnings from places like the BoE, Fed, IMF or BIS [Bank for International Settlements] start falling on deaf ears," says Hawkesby.

Wide ranging impact

Here in New Zealand the local response to the Lehman collapse and onset of the GFC included a dramatic reduction in the Official Cash Rate from 8.25% in July 2008 to 2.50% in April 2009, with the Reserve Bank making 150 basis point cuts in both December 2008 and January 2009. There was also the collapse of dozens of finance companies that began in 2006 and gathered pace through 2008 resulting in significant losses for tens of thousands of depositors.

In reaction to events in Australia, the Labour-led government cobbled together the Crown retail deposit guarantee scheme over a weekend, as then-Finance Minister Michael Cullen details here. It cost taxpayers' the thick end of $1 billion largely due to the demise of South Canterbury Finance. There was also a Crown wholesale funding guarantee scheme covering overseas bank borrowing that was used by ANZ, BNZ, Westpac and Kiwibank. There was also new Prime Minister John Key's Jobs Summit in February 2009 that spawned the idea of a national bike trail and a little used $1 billion job creation fund from ASB.

Overseas the Occupy Wall Street movement sprang up after the US Government bailed out banks rather than homeowners and failed to jail bankers. We learnt all about collateralised debt obligations, or CDOs, and credit default swaps. There has been billions of dollars of QE, or money printing, from central banks, and a European sovereign debt crisis resulting in unprecedented attention focused on Greek and Italian government bond yields.

We also got an entertaining explanation of the US housing market crash courtesy of The Big Short, a movie based on Michael Lewis' book of the same name.

What has changed?

Ten years on is the financial system less risky?

Here in NZ Watson says banking's in good shape.

"We have enough capital and liquidity to buffer us against external impact, and most importantly we make money by lending to people who we believe have the capacity to pay us back, through a series of simple products. And we are acutely conscious of the trust our depositors have in us to do the right thing with their money. Things seem to go wrong when complex, niche products are introduced where no one really understands the full set of risks. I hope banks learned their lesson on that front," Watson says.

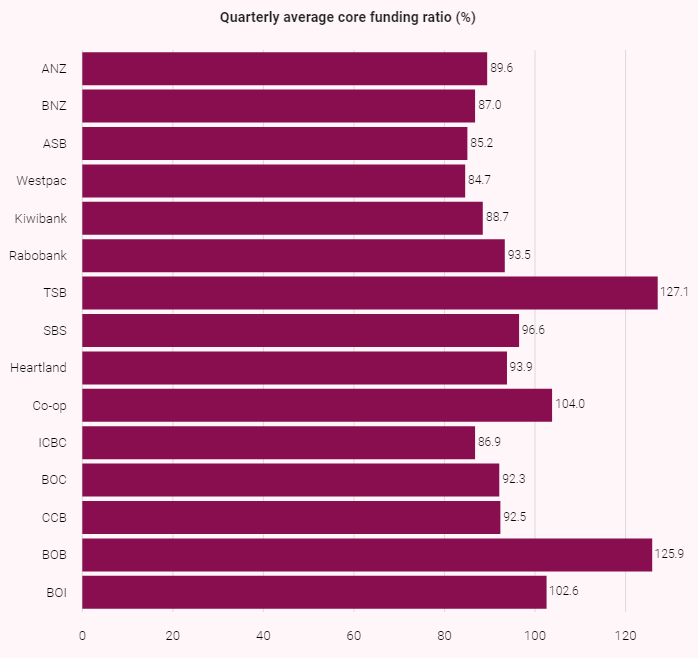

Following the Lehman Brothers collapse and subsequent drying up of international credit markets, the Reserve Bank introduced the core funding ratio (CFR) in 2010 to reduce NZ banks' reliance on short-term offshore borrowing/funding. The CFR requires banks to meet a minimum share of their funding from retail deposits, long-term wholesale funding and/or capital. The minimum CFR for each bank is 75%.

The idea underlying the CFR is a comparison between an estimate of a bank's funding that's stable and can be assumed will stay in place for at least one year, and the core lending business of the bank that needs to be funded on a continuing basis.

The CFR means our banks are less reliant on short term, offshore funding than they were as demonstrated by the Reserve Bank chart below. This shows key banks' core funding ratios as at June 30.

Shift in focus

Hawkesby points out there has been a big shift in focus from central banks and regulators, with them moving away from trying to predict crises and provide warnings to market participants, to a new focus on ensuring the financial system is resilient for when the next big shock eventually happens.

"This is what has motivated all the additional requirements for banks to hold bigger buffers of capital, more sticky and reliable sources of funding, and larger holdings of high-quality-liquid assets. In a local context, while many commentators see the RBNZ’s loan-to-value [ratio] restrictions (LVRs) as a way to control or manage house prices, in fact their main purpose is to ensure that borrowers have enough equity in their homes that they, and the bank that lent the mortgage, can withstand a house price crash if it ever occurred," says Hawkesby.

"Measured on the basis of capital, funding and liquidity, both global and local banks are undoubtedly in a much stronger position than before the GFC."

"However, there are still plenty of risks and imbalances that loom over financial markets as vulnerabilities. One is high debt levels, which was at the root of the GFC originally. Normally after a crisis there is a period of austerity where consumers and government tighten their belts and get their balance sheet back in better shape. That hasn’t happened to the same extent this time around," Hawkesby adds.

"When you look across the Western world, the United States is one of the few places where household debt-to-income has fallen after the GFC, whereas in places like New Zealand and Australia it is still very elevated. And even in the case of the United States, while households have been more prudent, it has been offset by growing fiscal deficits and government debt."

New risks emerge

Meanwhile, Hawkesby notes new risks and new unknowns have also emerged.

"One of these is that, as part of trying to reduce their exposure to market risks, banks hold much smaller trading books. As a result, the amount of market liquidity, ie. secondary market trading, has reduced in many pockets of the financial markets. This means some markets may be more vulnerable and volatile in the face of shocks, as market trading is likely to be thinner with fewer market liquidity providers."

Another new risk Hawkesby points to is the rapid growth of Exchange Traded Funds, or ETFs.

"These funds are designed to replicate the returns of different equity and fixed interest indices and sub-sectors of markets. However, given they are now making up a large portion of many global markets, there are concerns that they may exacerbate sharp moves in markets, particularly if these ETFs are tracking asset classes with already thin market liquidity," says Hawkesby.

Donald Trump & the next crisis

As you'd expect, the world's financial press has been writing ad nauseam in recent days on the Lehman collapse to mark the tenth anniversary.

In The New York Times Andrew Ross Sorkin nicely summarises the broader impacts of what came to be known as the GFC or Great Recession. He points out the impacts are still being felt in the economy, culture and politics, suggesting President Donald Trump’s election was a direct result of the financial crisis.

Here's more from Sorkin;

The crisis was a moment that cleaved our country. It broke a social contract between the plutocrats and everyone else. But it also broke a sense of trust, not just in financial institutions and the government that oversaw them, but in the very idea of experts and expertise. The past 10 years have seen an open revolt against the intelligentsia.

Mistrust led to new political movements: the Tea Party for those who didn’t trust the government and Occupy Wall Street for those who didn’t trust big business. These moved Democrats and Republicans away from each other in fundamental ways, and populist attitudes on both ends of the spectrum found champions in the 2016 presidential race in Senator Bernie Sanders and Donald J. Trump.

The depth of financial despair during the Great Recession and the invariably slow recovery have unleashed a sense of bitterness that dominates the political landscape, culminating in Mr. Trump’s electoral victory.

John Cassidy in The New Yorker reviews a book on the crisis by economic historian Adam Tooze.

In “Crashed: How a Decade of Financial Crises Changed the World,” the Columbia economic historian Adam Tooze points out that we are still living with the consequences of 2008, including the political ones. Using taxpayers’ money to bail out greedy and incompetent bankers was intrinsically political. So was quantitative easing, a tactic that other central banks also adopted, following the Fed’s lead. It worked primarily by boosting the price of financial assets that were mostly owned by rich people.

As wages and incomes continued to languish, the rescue effort generated a populist backlash on both sides of the Atlantic. Austerity policies, especially in Europe, added another dark twist to the process of political polarization. As a result, Tooze writes, the “financial and economic crisis of 2007-2012 morphed between 2013 and 2017 into a comprehensive political and geopolitical crisis of the post–cold war order” - one that helped put Donald Trump in the White House and brought right-wing nationalist parties to positions of power in many parts of Europe.

“Things could be worse, of course,” Tooze notes. “A ten-year anniversary of 1929 would have been published in 1939. We are not there, at least not yet. But this is undoubtedly a moment more uncomfortable and disconcerting than could have been imagined before the crisis began.”

Roubini, who has expended a fair bit of energy railing against and warning about cryptocurrencies and blockchain over recent months (see his tweets below), argues that given changes in the structure of financial markets since the GFC, once a market correction occurs the risk of illiquidity and fire sales is now more severe. He says there's less market making and warehousing activities by broker dealers, and the growth of high frequency trading has heightened the risk of flash crashes.

Here's more from Roubini;

Now factor in US domestic politics. Donald Trump is already attacking the Fed when economic growth is above 4%. What will he do in 2020, an election year, when growth stalls below 1% and job losses start? The temptation will be to create a foreign policy crisis, especially if he is boxed in on domestic policies by a Democratic House.

Since he has already started a trade war with China and cannot attack a nuclear North Korea, the only feasible target would be to provoke a military confrontation with Iran. That would trigger a stagflationary geopolitical shock as was the case in 1973, 1979 and 1990, leading to a spike in oil prices. Finally, once this perfect storm occurs in 2020, the tools available to policymakers will be constrained. Fiscal policy is hampered by higher public debts, but returning to unconventional monetary policies may be thwarted by the bloated balance sheets of central banks. Bailouts will be run up against the populist mood and less solvent sovereigns.

Unlike a decade ago, once the next economic and financial downturn occurs the policy tools available to reverse it will probably be less effective.

Below are a couple of tweets Roubini sent out this week.

And since last December the average crypto-currency has lost over 95% of its value while the Top 10 have lost only 90% of their value. Crypto-Apocalype in Crypto-Zombie Land. That entire asset class is essentially dead! https://t.co/afN6KoOBYK

— Nouriel Roubini (@Nouriel) September 12, 2018

As I said repeatedly: Blockchain is the most over-hyped technology ever! Crypto-currencies area total scam but blockchain is biggest baloney BS ever... https://t.co/9ATQP9P1qV

— Nouriel Roubini (@Nouriel) September 12, 2018

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

19 Comments

Concerns in 2008? How about 10 years before that - 1998! Brooksley Born warned of the catastrophe that could engulf the OTC Derivative Markets, years before that came to pass, and yet those wise heads that we still revere today ( for some unknown reason!) dismissed her concerns as fearmongering.

"...regulation was strenuously opposed by Federal Reserve chairman Alan Greenspan, and by Treasury Secretaries Robert Rubin and Lawrence Summers. On May 7, 1998, former SEC Chairman Arthur Levitt joined Rubin and Greenspan in objecting...They argued that the imposition of regulatory costs would "stifle financial innovation"... Greenspan brushed aside the substance of Born's warnings with the simple assertion that "the degree of supervision of regulation of the over-the-counter derivatives market is quite adequate to maintain a degree of stability in the system"....The derivatives market continued to grow yearly throughout both terms of George W. Bush's administration. On September 15, 2008, the bankruptcy of Lehman Brothers forced a broad recognition of a financial crisis in both the US and world capital markets....Born declined to publicly comment on the unfolding 2008 crisis until March 2009, when she said: "The market grew so enormously, with so little oversight and regulation, that it made the financial crisis much deeper and more pervasive than it otherwise would have been."

And today, "We have enough capital and liquidity to buffer us against external impact, and most importantly we make money by lending to people who we believe have the capacity to pay us back " etc. Just the view that was held back in '98?

Here the PBS video on how Brooksley Born gave her warning.

Very good analysis.

The Warning

https://www.pbs.org/wgbh/frontline/film/warning/

Great doco that people should take the time to watch.

Thx for that. I'll try to get it to load and have a watch.

But 1998 wasn't when the first worries surfaced over OTC Derivatives. I can recall another 10 years further back, '88, and the real worry from Boards of Directors/Credit Committees (who actually still had some sort of idea what banking and simple derivative trading was all about!) baulked at increasing counterparty/trading limits for fear of default on settlement. Sadly, that caution was overwhelmed by the "Well if you don't want the business Banks, X,Y and Z will do it". It's all easy and obvious, looking back!

It's all easy and obvious, looking back!

Yes, if you take the time to understand it; however, most people don't and simply accept the cliched explanations about what happened. In NZ and Australia, we simply spend the time explaining why we are different from the rest of the world and why we're immune to bubbles.

Maybe we are immune? Australasia might be uniquely resilient.

BW exactly right

World debt is exponentially higher today than at any time in history

We are merely awaiting which cork will pop first from the debt dam for GFC2 predicted to be far worse

People lost their homes in the USA , and the Govt bailed the banks out. They could have bailed the people out , who could then pay the banks . At least the ones that weren't in the worst junk bond catergory , but still affected. Places like Detroit and Troy just starting to recover now , it didn't need to be so hard.

Solardb it’s the American Dream

Bank bailouts but no mortgage bailouts

Let hedge funds buy up foreclosed homes & rent them

to the same poor souls the banks kicked out of their homes.

Then sell the rentals when market has ticked up for easy profit$

Keep the working class on low wages until the Ai robots take over the jobs

Vote in fake saviour Trump who promises tax cuts then gives most to the wealthy

American fake dream continues

There's a very good analysis of the entire saga here. It focuses primarily on the myth that the 'removal' of Glass-Steagall safeguards led directly to mayhem. not so....

The conclusion is worth quoting in its entirety:

The 2008 financial crisis had precious little to do with Glass-Steagall, one way or the other. It was caused primarily by bad lending policies, which in turn led to the growth of the subprime market to an extent that neither the lawmakers nor regulatory authorities recognized at the time. The commercial banks and parent holding companies that failed—or had to be sold to other viable financial institutions—did so because underwriting standards were abandoned.

Yes, these banks acquired and held large amounts of mortgage-backed securities, which pooled subprime and other poor quality loans. But even under Glass-Steagall, banks were allowed to buy and sell MBS because these were simply regarded as loans in a securitized form.

Yet by focusing the public’s anger on “greed,” “overpaid bankers,” and so-called “casino banking,” politicians have been able to divert attention from the ultimate cause of the financial crisis, namely their belief that affordable housing can be provided by encouraging— or even obliging—banks to advance mortgages to homebuyers with low to very low incomes and requiring government-sponsored enterprises to purchase an ever-increasing proportion of such loans from lenders.

If politicians continue to believe that affordable housing can only be provided in that way and act accordingly, no one need look any further for the causes of the next financial crisis..

95% lending for KB - This Time is Different......

Glass-Steagall kept savings banks apart from the riskier side of banking

That alone kept savings safer than they are today

All your insured savings protection is worthless if your derivatives trading banks & insurance cos go bust and many will in GFC2 coming sooner than we think.

Check out the US deficit inflated further by Trump tax cuts

There are many reasons for a GFC yet we have all the seeds planted for a next big one

Indeed Waymad, it's not an ideal lending scenario. The maintenance of a debt for equity swap to the elderly is the other thing that is holding up the 'Beveridge' Ponzi. Without more immigration, more debt and more hype of housing, most Western economies cannot fulfil the obligations made to the post war population spike. They can't fund it from tax receipts so it has to come from the debt for equity trade to allow the majority of the retired to remain independent of the governments books. It's the biggest swindle of the last two centuries but no 'elected' government has the power to implement the necessary changes because they'd never get voted in again whilst the voting power resides with the 'beneficial' generation of boomers. Even the policy makers, as we've seen with our recent tax review committee are scared of the consequences that adjustment will have on the dependency ratio of asset holding classes....if assets slow even the slightest signs of correcting downwards. It is what is best described as a 'Buggers muddle.'

Great article which should get wider viewership

Have you tried the Washington Post & NYTimes ?

This site has long been a great source of info & entertainment

You should be proud of yourselves

GFC legacy: households with heads down, paying off the mortgage as quickly as possible, & refocusing on careers & work longevity, - if it all collapses, what is your personal plan of survival? Always a useful question for people to ask themselves.

So a core funding ratio of 75% is required by banks against deposits and most of the lenders have healthy ratios in the 80%'s which is great.

But. and it is not a little BUT, with our banks lowering deposit rates whilst other international markets are raising theirs, how immobile are those deposits to maintain CFR's? I'm currently thinking about moving cash out of NZ , primarily because I think the exchange rate will continue to weaken at a far greater rate than any slightly higher interest benefit on my cash. I would presume that I'm not the only person who might consider this as an option. How quickly could that impact on Banks Core Funding Ratios if cash (which is pretty liquid) decided to do the same? Already in Australia we are seeing their banks having to raise mortgage rates because of a shortage of deposits, anyone any idea what percentage of our deposits are held by NZ citizens? Any ideas how many of them might or could move their cash away if the interest rates don't compensate the exchange rate falls? I I'm also a bit anxious about the lack of profits at the major NZ companies and how that will be viewed by the currency markets... Is anyone else thinking the same as me?

Yes. That's why I quote the BEFU Budget Assumptions which underpin the Gubmint's financials, every Friday. NZD is dropping quietly but consistently, which raises input costs (think, fuel) right across the board. Yes, it raises export revenues when converted back to NZD, but if most inputs are imported, there's little net benefit. For non-exporters, but still with most inputs imported, it's all cost, less profit. Which won't do much for tax revenue, employment, or business confidence.

And your example of cash moving away from what is increasingly perceived as a cul-de-sac to better yields offshore, could be one of those little trickles out of the dam face....

It's the old Hemingway quote (The Sun Also Rises):

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

Debt in China at 300% of GDP is the really worrying take from this little news clip. How much of that debt ended up in our housing market?

https://www.youtube.com/watch?v=n3UJ6yMaM4A

Interesting take on impact of Chinese debt on Western housing markets. Someone gave a blank cheque book to a populous who love to gamble.

Another fascinating article from the always-Interesting Yves Smith at NakedCapitalism

The lede:

A financial industry safety net enriches bankers and their shareholders — at our expense

When the collection of forward bets is grown exponentially, there will be times the expectation overruns the underwrite, That is when moves are made like repealing the likes of Glass-Steagall - by politicians who just want to kick the can down enough road to see out their tenure.

But ultimately the increased bets run into physical limits - 2008 reflected that. Since then we have avoided that debate, preferring to smear blame. The next iteration probably doesn't have a fix, given that fixes require mass faith in the fixers.

I'm sure Govts here and there know this - our is using the words 'resilient' and 'sustainable', neither of which describe endless growth. .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.