By Gareth Vaughan

Four New Zealand owned banks say the fact the Reserve Bank's capital proposals seek to both materially increase the required level of capital for banks and decrease available capital sources, is a combination that's unworkable for them.

Kiwibank, The Co-operative Bank, SBS Bank and TSB have made a combined submission on the Reserve Bank's proposals to increase banks' regulatory capital requirements. A copy has been provided to interest.co.nz. The four say they support the New Zealand Bankers' Association's submission in principle, but highlight matters of specific relevance to them in their own submission.

In principle they welcome moves to introduce a level playing field and a regulatory regime that reduces banking system risk through recalibrating aspects of the current capital framework. However, the four say they are concerned the Reserve Bank's proposed changes could have the unintended consequence of widening rather than reducing the competitive gap between large and small banks.

The Reserve Bank's sole focus on Common Equity Tier 1 (CET1) capital concerns the four. They also argue for greater alignment between banks able to calculate their own credit risk weightings, being ANZ, ASB, BNZ and Westpac using the Internal Ratings Based (IRB) approach, and all other banks using standardised risk weightings prescribed by the Reserve Bank.

"There is no empirical information to suggest that the credit performance of the IRB bank portfolios is superior to that of standardised banks, or that these IRB models make the portfolios any safer," Kiwibank, The Co-operative Bank, SBS Bank and TSB say.

They point to a "significant divide" between the two approaches where IRB banks calculate significantly lower risk weighted assets (RWA) and are thus required to hold significantly less capital. This, the NZ-owned banks argue, has created uneven competition, with the IRB banks enjoying a significant competitive advantage stemming from the regulatory framework.

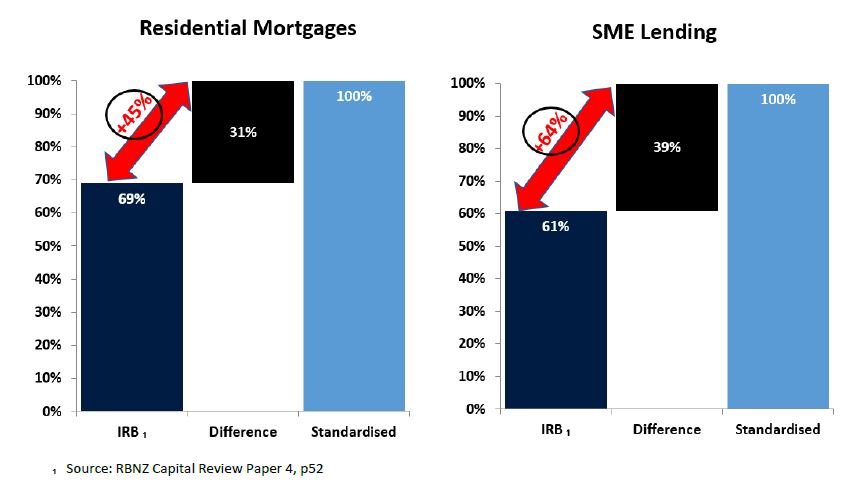

'The standardised banks require 45% and 64% more capital for the same risk'

A Reserve Bank Quantitative Impact Study (QIS) of the four IRB banks that features in the capital consultation paper it released in December, puts average RWA outcomes under the IRB approach at 76% of the standardised approach, albeit with considerable variation across lending categories. What the Reserve Bank has proposed would see ANZ, ASB, BNZ and Westpac increase the assets they use to determine the minimum amount of regulatory capital they hold to the equivalent of 90% of what's held by other NZ banks, up from the 76%. See more on this here.

"The NZ-owned banks operate primarily in the categories of residential mortgages and SME lending. The observed average ratios for the IRB banks in those categories are considerably lower at 69% and 61%, respectively, of standardised risk weightings. This means that the standardised banks require 45% and 64% more capital for the same risk, for residential mortgages and SME lending respectively," the four NZ-owned banks say.

"This illogical outcome is most difficult to justify in relation to residential mortgages where a loan to the same borrower secured by the same house, in the same street requires 45% more capital to be held by a standardised bank."

"For the NZ-owned banks, the requirement to carry extra capital of this magnitude has a significant impact on return on equity (ROE). While smaller banks expect a lesser return than large banks on account of the latter’s scale advantage, the impact on ROE from this regulatory anomaly can be as great, or even greater, than the cost to income ratio differential compared with large banks. For portfolios of similar risk, RWA outcomes should be similar, regardless of which approach is used," the NZ-owned banks argue.

They also argue that the current bank capital regime favours share market listed and foreign owned banks, with the Australian-owned banks having an ability to "flow through" capital from their parents, often with a regulatory advantage from "jurisdictional arbitrage." Additionally they call for a more meaningful difference in capital levels held by banks designated as systemically important to "ensure the system is protected." The Reserve Bank proposes to designate ANZ, ASB, BNZ and Westpac as systemically important with a 1% higher capital requirement than other banks. However, the NZ-owned banks argue this isn't enough given their big rivals represent "substantially all of the market." Thus they say the systemically important buffer should be increased to 2%.

"While not the Reserve Bank's intention, we have concerns that proposed changes will widen rather than reduce the competitive gap between large and small banks...A combination of changes are required to the Reserve Bank's proposals to ensure that a competitive market exists and there is a level playing field."

The Reserve Bank's proposals are based on increases to Common Equity Tier 1 capital’ or CET1. This is a subset of Tier 1 capital and consists of ordinary shares, retained earnings and some reserves. Banks are currently also allowed to use Additional Tier 1 capital, or AT1, and Tier 2 capital. AT1 is capital instruments such as preferred shares that are continuous given there's no fixed maturity date. Tier 2 capital mainly consists of long-dated subordinated debt. Currently banks must have a minimum Total Capital Ratio of at least 10.5% of RWA, with 8.5% Tier 1 capital and 2% Tier 2.

The proposed changes would see a minimum Tier 1 capital ratio of 16% for the big four banks and 15% for the rest, comprised of CET1 capital and AT1 that meets proposed new requirements. The RBNZ proposes to ban contingent debt from qualifying as regulatory capital. The Reserve Bank is questioning whether Tier 2 capital should remain in the capital framework. (You can see more on the different types of capital and what the Reserve Bank is proposing here).

As of December 31 Kiwibank's Total Capital Ratio was 15.3%, The Co-operative Bank's was 17.2%, SBS Bank's was 14.1%, and TSB's was 14.8%.

'It is imperative that the smaller banks have access forms of capital other than ordinary shares'

The four NZ-owned banks argue AT1 and Tier 2 capital should at least remain available to small banks with AT1 instruments callable.

"NZ owned banks also need the ability to meet capital requirements through non-CET1 capital instruments. Without these, NZ-owned banks ' growth will be constrained, limiting competition in the sector."

"The NZ-owned banks already have challenges accessing further CET1 and those challenges are likely to be exacerbated. This relates not only to structure, two of the four submitting banks are mutual, but also scale and illiquidity, given that none of the NZ-owned banks are listed," the four say.

They point out they have "demonstrably lower return expectations" than the big four banks, and that investors are likely to prioritise larger banks delivering higher yields, further compromising NZ-owned banks' access to ordinary share capital.

"A regime with a focus on CET1 will drive competition for scarce capital in markets that primarily reward financial outcomes. Ensuring that good market conduct is not compromised by the pursuit of profits is a principle regulators globally encourage. It is imperative that the smaller banks have access forms of capital other than ordinary shares. A bank should not be disadvantaged from having the ability to compete on account of being unlisted and wholly New Zealand owned."

The four note they pay modest dividends and have ROE of about 6% to 9%. Latest figures on ROE for the four Australian-owned banks show them between 13% and 16%. Adjusted to reflect return on regulatory capital as a proxy for future ROE if all capital is CET1, suggests returns of 6% to 7% for the NZ-owned banks, they say in their submission.

"We estimate the level of lending growth that can be funded from retained earnings generated by returns of 6% to 7% assuming the proposed capital level of 17%, a self-imposed 1% safety margin and a conservative dividend policy of 20%, is less than 5%. After allowing for necessary investments in technology, which result in a Tier 1 deduction, the long run growth prospects are even lower, and this is before having regard for any additional transitional burden."

"The outlook for meaningful growth from retained earnings is very limited," the four say.

'The necessary consequence of materially increased capital requirements must be reasonably practical access to capital'

For Kiwibank and TSB, the inability to call an AT1 instrument will discourage investment by fixed income investors, they argue, and for mutuals The Co-operative Bank and SBS a mechanism to enable Tier 1 issuance would be "helpful."

"The necessary consequence of materially increased capital requirements must be reasonably practical access to capital. The Reserve Bank capital review seeks to both materially increase the required level of capital while at the same time significantly decrease the available sources. As currently proposed, that combination is unworkable for the small bank sector," the four say.

"Ordinary share appetite is likely to be scarce, retained earnings do not represent a meaningful solution, and as it stands there will be limited practical access to alternate forms of capital. The inevitable reality of the forgoing is that small banks will have very limited ability to grow, and increased capital requirements will further restrict already modest dividend policies for corporatized banks relevant to small bank owners. Furthermore, there will be fewer levers to pull to recapitalize a small bank in the event of any significant level of unexpected losses. The consequence of that is an investment proposition that may be unattractive to investors – both current and future."

"The market is currently comprised of large banks with very high expected, and achieved, equity returns coupled with very high dividend payout ratios. Conversely, the smaller bank sector ROE expectations and dividend payout ratios are more modest. As proposed, it is difficult to see how these modest and reasonable expectations can be preserved under the changes. This could fundamentally undermine the economic outlook for the small bank sector," say the four NZ-owned banks.

"In these circumstances there is a risk that small banks are ultimately absorbed by the large banks, competitively in the market or by acquisition. That would only serve to increase concentration on the existing systemically important banks and lessen competition. While we welcome proposed changes that level the playing field, that outcome is moot if the regime does not reasonably allow access to capital to enable growth."

The Reserve Bank proposes a transition period of five years for banks to adapt to the new capital requirements. However, the NZ-owned banks ask for eight years. They say a longer transition period may be necessary "if essentially all required capital must be funded from retained earnings, particularly if there is a downturn in the credit cycle during that period."

"All of the equity of the NZ-owned banks is provided from New Zealand. There are no other markets competing for the use of that capital. It is employed only here and the profits remain within New Zealand. A resilient, effective and efficient market stems from both financial stability and an environment that supports competition. It is critical that the capital changes deliver both," the NZ-owned banks say.

TSB also provided the statement below from its CEO Donna Cooper.

We support the Reserve Bank’s intention to introduce a regulatory regime that levels the playing field and strengthens New Zealand’s banking system and economy.

We do however have some concerns that the proposal as it stands may have unintentional consequences, impacting the New Zealand economy with potentially higher lending rates and reduced saving returns.

More analysis is needed to understand this impact and we welcome the RBNZ’s announcement it is appointing external experts to further review this.

The proposal may also limit New Zealand-owned banks opportunities for growth by restricting the instruments we can use to raise capital.

Under the current regime, the NZ-owned banks are materially and unfairly disadvantaged. In residential lending, we have been required to hold on average 45% more capital than Australian-owned banks, for the same risk.

We support the RBNZ’s viewpoint that this shouldn’t be allowed to continue. However, while not its intention, we are concerned the proposed changes in their current form could widen, rather than reduce the competitive gap between Australian and NZ-owned banks.

The magnitude of the proposed capital increases, together with a significantly narrower range of allowable capital instruments, could make it challenging for NZ-owned banks like TSB to access additional capital. We want to grow, but the current proposals could limit our ability to do that.

Other countries have adopted a more pragmatic approach to this, recognising that some flexibility on allowable instruments is necessary to achieve higher capital ratios.

If the RBNZ is not inclined to increase the scope of capital instruments available for all banks, it should at least allow this for NZ-owned banks. This would facilitate a more competitive market, reflect the approach taken in Australia, fit with the regime which already comprises two separate regulatory frameworks, and the RBNZ’s objectives would still be met.

There also needs to be a larger difference between the levels of capital held by systemically important banks and the rest of the industry, to more accurately reflect the potential risks to financial stability.

TSB believes a combination of changes to the RBNZ’s proposals are needed in order for New Zealand to have a sound, efficient and fair banking system.

*This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

11 Comments

the T1 Capital Ratio Madness Propsosal SUNK by its own small banks. I called it six months ago. The young smart money will go overseas, the older money will go SUM,OCA and ARV, and of course the big R.

These are insightful articles, good journalism.

It is perverse that a big 4 bank is able to carry significantly less capital than the NZ based banks against a loan, yet still be higher rated. That combination of lower capital and cheaper funding explains most of their dominance.

Not sure... not sold I am afraid.

The problem with comparing percentages with absolute capital values is that it does not reflect that size does bring some resilience Let's say Bank A has $5b in assets and Bank B has $100b ... as a straight percentage, would we expect, lets say 20% capital - $1b for Bank A and $20b for Bank B. The likelihood of Bank A needing all $1b is higher than the likelihood of Bank B needing all $20b, as there is more capacity to absorb losses. I am not saying there shouldn't be closer gap, and that perhaps Risk Weighted Asset definition should be closer, but hard to see a case for straight percentage equivalence (or in the case of what the smaller banks want, a higher percentage for Big 4)

Bank B is looking over capitalised with $100m loans and $20b capital. I don't agree with your logic, but I do tend to agree a larger bank is safer due to diversification in loans (a good thing - seasoning, geographical distribution etc), but larger banks also undertake riskier activities like C & I and investment banking. The point I was making is large banks hold 40% less capital against resi mortgages but are significantly better rated. It's perverse and not explained away by size, but explicit rating agency expectation of a sovereign bail-out due to systemic importance.

I'm not sure I've seen like for like comparisons that definitively show the large banks have 40% less capital on an identical resi loan. It could be a mix question. But even if they did, the law of numbers means the smaller you are the higher percentage of your asset base you should be required to hold as capital.

I am not so sure the credit ratings are based on the sovereign bail out perception... it's much more likely based on parental bail out, as OBR would require all shareholder equity to be consumed first and foremost.

The smaller banks have serious risk concentration, not just because slightly elevated losses would wipe out their profits, but also well over weight in resi loans - TSB 83% (9.2% over 80% LVR) , Kiwi 89% (8.6% > 80), SBS 77% (15.9%! > 80) .. while ANZ has 60% resi (5.2% over 80), ASB 65% (7.6% over 80) WPC 60% (8.6% > 80) and BNZ just 48% - way heavy in business - 6.7% > 80

The whole concept of massively increasing capital will just as likely cause drop/rationing in credit, perversely causing systemic risk for an economy propped up (rightly or wrongly) on resi loans. It's all well and good to expect shareholders to accept a lower return, but that's not really how listed companies function right? That may just cause capital flight.

Oh for some proper analysis!

What if analysts like Douglas Orr are correct inasserting that in Australia the household expenditure measures (HEM) to assess loan serviceability were rigged during the boom years so that now an astonishing 40% of the big four's loan books are either not prime or subprime.

This topic hasn't had much air time.... we have been consumed by the RBNZ proposals in terms of the amount of capital as opposed to what this article is highlighting.. what the RBNZ would call the 'quality' of capital.

Neither of the banks mentioned above have access to share capital, so their only source of Tier 1 capital is retained earnings (or a significant further capital injection from Kiwibank's parents in their case)... significantly restricting their ability to grow.

These banks, and the big 4, raise Tier 2 capital by why of subordinated debt and preference shares... an instrument the RBNZ has in the past highlighted their lack of understanding and cited a concern that investors don't understand their position in the capital structure of the bank (which isn't their job, its for the FMA to consider whether investors risks are adequately disclosed).

The RBNZ have given little thought to investors such as myself who think the banks are safe enough and believe subordinated debt offers great value. If I am wrong, I know I am not looking for a taxpayer bailout... so why limit my investing options?

Lifting capital is one thing, but dictating to investors where we can invest in the capital structure cos we 'don't get it' is a whole other conversation. Just because Geoff Bascand has highlighted he doesn't understand doesn't mean we all don't get it.

This is why so many have objected to the RBNZ's proposal, there are far more elegant ways to approach making banks safer than just bluntly increasing tier 1 capital - CoCo's for example. I could buy it if they had produced the research, but they haven't. The cynic would say they don't understand or can't be bothered, who really knows.

Geoff Bascand is a maths man, not a market man, he will take the fall while others sail past .....

Have you even achieved some form of insured savings accounts yet in NZ ?

Talk about archaic

Why does NZ a country of only about 5 million not use the best practices from its greater western cousins ?

So much time wasted & ongoing indecision appears the way

This is a good conversation & hats off to interest.co for hosting it. It's exactly what you should be doing. We're getting into the quality side of things now with a hint of how investors think & invest, especially in a couple of small tinnies bobbing up & down at the bottom end of the Pacific Ocean. I would like to see the banks use this opportunity to re-set their markers & at least make it look like they care about their customers, even if they don't. The banks are looking after the banks. Indeed, the bank looks after the bank. Meantime, the overseas shareholders have taken between 30-40 billion dollars in profits offshore over the last 18-20 years & we can't allow that to continue, if we want to survive into the new millennium as a going concern nation. Struth, we give most of the profits to the bloody government already who wouldn't know how to invest it wisely if it hit them in the face.

The BEOT rules okay! Not while we have breathe.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.