By Jenée Tibshraeny

The Reserve Bank (RBNZ) has been making the case it’s still getting bang for its buck cutting the Official Cash Rate (OCR) further into record-low territory.

Now, it's released a brief summary of some of the modelling done to support this position.

Its analysis found the impact of OCR changes on both inflation and GDP growth have been “relatively stable” over the last 12 years.

So from the global financial crisis and through the recovery, inflation and economic growth haven’t really responded differently to interest rate changes.

The RBNZ is of the view that the same will be the case looking to the future, even though it's in unchartered territory with the OCR now at just 1%.

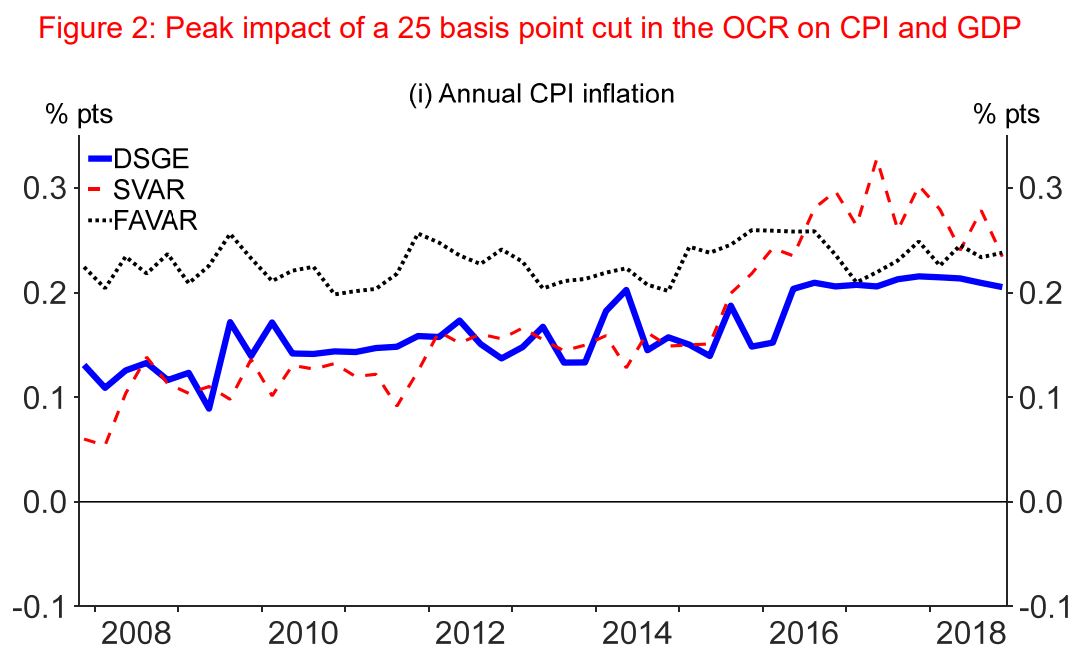

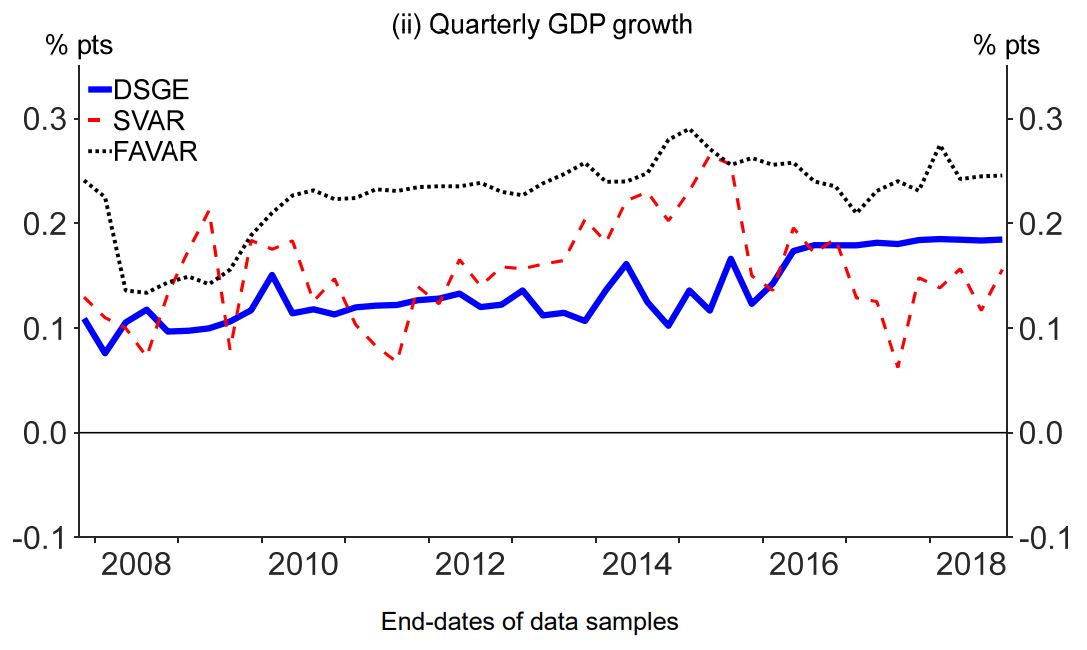

The RBNZ drew its conclusion by using three models that try to isolate the effects of an OCR cut from the other moving parts in the economy. This is what it found (the three lines represent the three models):

Averaging its results, the RBNZ found a 25-basis point OCR cut had a “peak impact” on annual CPI inflation of 0.19 percentage points, on average.

In other words, cutting the OCR by 25 basis points boosted annual inflation by an average of 0.19 percentage points across the time period examined.

A 25-basis point OCR cut had a peak impact on quarterly GDP growth of 0.17 percentage points on average.

With results being relatively stable across time and methodologies, the RBNZ concluded that “the transmission of monetary policy shocks has not changed significantly in New Zealand over the last 12 years. There is no sign that OCR moves have become less effective in recent years…

“This means it is business as usual for the Bank - further cuts in the OCR should boost the economy and inflation, and OCR increases should constrain demand and inflation.

“The significant knowledge and experience we have built up during the inflation targeting era can still be used to guide our monetary policy strategy and achieve our goals of price stability and supporting maximum sustainable employment.”

The quality of the data the RBNZ had access to made it difficult for it to extend its analysis over a longer timeframe, including a wider range of economic conditions.

In more technical terms, the RBNZ explained its approach: “We use an ‘expanding window’ estimation method in order to verify if the transmission of monetary policy shocks to inflation and economic activity has changed through time.

“We first estimate each model on data spanning the first quarter of 1993 to the last quarter of 2007, just before the GFC. At this point, we assess what the model implies about the effect of a 25-basis point cut in the OCR on inflation and output.

“We then repeat this process, adding an additional quarter of information up until the end of 2018.”

For more on the RBNZ’s thinking behind cutting the OCR to 1% on August 7, see this interview interest.co.nz did with its chief economist, and this piece and this one written following the announcement.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

35 Comments

Either there is a recovery, or there isn’t. And if there isn’t, it didn’t work.

I'm with the bond market until proved wrong.

The reason why the RBNZ determines that it is “still getting bang for its buck” is that it systematically eliminates data which indicates the exact opposite.

RBNZ says that “traditional recursive methods for identifying monetary policy shocks in a VAR often produce counterintuitive results, where inflation appears to decrease in response to adecrease in interest rates, reflecting the endogeneity of monetary policy”, but they say that their “methodology removes the counterintuitive price puzzle seen in recursively identified VARs using New Zealand data”.

This seems to be well known. A simple search on the interweb reveals that the "price puzzle" is the association of a contractionary shock to monetary policy with persistent increases in the price level is “an embarrassment to monetarist/ISLM interpretation”

Mmm. I think you miss their point.

Their point is that they are identifying shocks recursively in the SVAR - this essentially means that they have no completely exogenous instrument for estimating structural impulses. They obtain orthogonal impulses from a decomposition of the error terms based on the ordering of the endogenous models. The issue arises where the normal decomposition can produce negative responses. However, using structural assumptions, you can decompose the model in order to guarantee strictly positive (negative) impulse responses without impacting magnitudes.

...it systematically eliminates data which indicates the exact opposite.

No. As above. They don't change the data at all. They simply modify the reduced form assumptions of the model.

It's a question of whether the model is manipulated to fit the narrative. Not whether the data is manipulated to fit the model.

“We first estimate each model on data spanning the first quarter of 1993 to the last quarter of 2007, just before the GFC. At this point, we assess what the model implies about the effect of a 25-basis point cut in the OCR on inflation and output."

Cool! But New Zealand didn't introduce the OCR until March 1999. So how can it have been an influence in 1993!

(This leads us on to - Why did we introduce an OCR in 1999? Answer: Because what we had wasn't working? So the corollary could be - Why do we think the OCR will work in today's environment? Answer: We may need to change again - away from an OCR - to another monetary policy regime.)

Mauldin had a good article at the weekend

"I know this has been a little bit of a Debbie Downer letter. When the consensus is that we are going back to the zero bound on interest rates, we’re literally screwing an entire generation. People who have saved and worked and bled will be rewarded with zero interest rates and the need to take more risk in retirement, exactly the wrong time in their lives to be taking risk."

https://www.mauldineconomics.com/frontlinethoughts/what-i-learned-at-ca…

I have a farm and I'm shocked at the ongoing cost increases, anyone who believes the inflation figures is living on another planet.

As an example in the past month, rates up %18 insurance up %15, road user charges %10 (which will be reflected in my freight charges) and same again next July. Everything is on the move mostly driven by the non-tradable sector.

This means i'm facing reduced profitability, it's putting the pressure on. I can cut the non discretionary, which I actively doing but not these costs.

If my council finds costs are inflating why are we trying to pretend that everything is rosy and CPI is bugger all?

How can I maintain my crazy asset values if im not profitable?

https://brucewilds.blogspot.com/2019/08/the-cpi-understates-inflation-s…

Wasn't it Benjamin Disraeli who said...Lies, Damn Lies, Statistics ?

CPI statistics would fall right in line with his statement, I think.

There is much inflation in prices on ground level, which is being hidden/ignored.

And major, impactful decisions are taken based on that.

No wonder the current monetary policies are not working.

yep. It's simply farcical, this 'game'.

Don't buy them if you think it is theft.

It's funny to think that rates were 8.25 in mid 2008 and they've pretty much been going down since then (with a few minor adjustments up), and now we're close to zero with global storm clouds gathering. They may say that the economy's response to OCR changes has been relatively stable, but has it really been that effective over the past 5 years of so, apart from creating a private debt bubble? Sure, NZ asset prices (property and shares) are high, but they'd have to be concerned about the OCR still being so low. They never got out of the "emergency rates" zone before a new emergency is on the horizon.

Saying interest rate drops are the answer is like preventing a hangover by drinking more. At some point you need to address the underlying cause, and the first step would be admitting you're an alcoholic. Are we ready to be that open with ourselves?

In terms of the analysis they have provided... its all theoretical cos no one knows however savers and spenders behaviour changes when rates are this low. The thing with being in unchartered territory is there is no point in looking at your map.

Regardless of whether you agree with the RBNZ or not I cannot remember a time when the RBNZ has been under so much pressure to justify its actions. Capital rules, OCR cuts, Tane Mahuta indeed!.

The market always took comfort that they generally understood where the RBNZ was coming from.... but there is just too much coming out of left field that has left the market and it has everyone nervous.... yet they want us to go out and spend.

Im trying to think of the last time the market completely mispriced an OCR move.... I think I'd have to go back to Brash in 2001.

When can we shelve the eternal "central bank is facing a dilemma, to raise/lower rates or not by 25/50/x basis points". All pure nonsense. Interest rates follow economic growth & are positively correlated with it. What's driving the economy is bank credit creation 4 real economy Link

The CPI is poorly calculated and is no longer indicative for inflation. The RBNZ should not be using it to set the OCR.

Another disgruntled TD holder.

.. let us say that he is ; how does it make his statement wrong ?

It's a conclusion with no analysis. He should at least know how CPI is calculated (see https://www.stats.govt.nz/topics/consumers-price-index). If it is calculated incorrectly he needs to explain why and what he would do differently.

IMHO he sees TD rates falling = bad for his personal circumstances = CPI is broken + banks are protected by corrupt politicians + home owners exerting political pressure to keep bubble from popping etc........... = whinge on here to other TD holders who are also taking a bath.

Nah - they are neck deep in the bond market anticipating this from the RBA to spill over into NZ:

Bonds are how the government borrows. Here’s how it works in simplified terms:

The government offers to sell a piece of paper that says, “Australia will pay you back a million dollars in 10 years” (a 10-year bond).

Someone buys that for, let’s say, $900,000.

In this way the government just borrowed $900,000 and the $100,000 difference, spread over 10 years, is the return on investment for the buyer. The return on investment in bonds is known as the yield. It is usually expressed as a percentage, and it’s really important.

Yields change constantly in the secondary market as people trade the bonds they buy at varying prices.

When the RBA buys Australian Government bonds from the people who hold them, it is expected to have an effect on bond yields. The reason? Bidding to buy bonds will push up their price. The price of a bond determines the return on it, aka the yield.

The higher the price, the lower the yield. For example, imagine if someone bought that 10-year bond mentioned earlier for $1 million, it would have a yield of 0 per cent. Link

I guess banks have already bought local sovereign bonds (zero risk weighting) after writing up both sides of the balance sheet to emulate the success of their US compatriots without any consideration that they are crowding out the extension of loans to productive endeavours which contribute to GDP:

{kind=link}

The majority of bank credit creation in the UK is not even used for transactions that contribute to and are part of GDP, but instead is used for asset transactions. They are not part of GDP, since national income accountants require a ‘value added’ for inclusion in GDP, not just the shifting of ownership rights from one person to another. When bank credit for asset transactions rises, asset prices are driven up, because the loans do not transfer existing purchasing power, but instead constitute an increase in net purchasing power: money is being created and injected into asset markets. When a larger effective demand for assets is exerted, while in the short-term the amount of available assets is largely fixed, the price of assets must rise. Link

Which Hedge Funds Are Making A Killing As Yields Collapse

How, exactly? By selling the bonds to a greater fool (it's been working pretty well so far).

This is how the rich and influential folks have hijacked wealth in the last few decades.

And the scam still continues, in a larger scale and in the guise of saving economies.

I know one prominent person in NZ who might have spotted this trend and taken good advantage of it.

if you jump to 13mins you can hear Karl Denninger on negative bonds.

https://www.rt.com/business/466760-keiser-negative-bonds-theft/

running out of road to kick the can down

Modeling is a very academic and useful research tool, but falls short in as much as it does not necessarily reflect what is actually happening. It is theoretical and sadly is very flawed and cannot replace practical information generally gathered by 'walking about'. It removes any feet on the street and common sense. It can only look at trends and is highly susceptible to biased entries and interpretations as shown above. Why not run 10 different models for 10 different scenarios.

Exactly. It masquerades as science. But it's not really.

Too many of these economists cling to their theories and models, pontificating in their ivory towers...

Banksters who want inflation...they wants us all to pay more for the same stuff? And they know we won't get a pay rise to counter it.

So next time I go to the supermarket, pay the new rates bill, gas the car, pay the insurance I should be happy if the cost has gone up. Because it means we have inflation! Yehaaaaaaaaa. easy peasy. Let's do this!

Nuts.

What gets me is how obvious the underwrite is.

What then gets me is how many folk don't seem to factor it in.

Yet if you ask why Trump would want Greenland, then ascertain what proportion of the Earth's surface Greenland is, then ask yourself how many doubling-times are left.......

We are indeed in uncharted territory. We are also in journalistically-avoided territory, BTW.....

Wouldn't it be better just to print money? I wonder what would have happened if they also included house prices in the inflation figures, as I suspect inflation over the last 1 years would be significantly more than it is currently . IMO house prices shouldn't be rising by more than inflation and wage growth, because that relies on people needing to borrow more and more, and interest rates needing to be lowered to allow people to service larger mortgages. I just can't understand were the end game is here. In 10-20 years time, where are interest rates projected to be, vs household incomes vs house prices. i wouldn't have thought it was in our best interest to expect our younger generations to have to pay more and more for housing. Having to get a 700k + mortgage is crippling IMO, and it relies on two incomes as well to service it, which isn't ideal for family life and time

But the younger generations always want the latest gadgets, iphones, cars, holidays, $5 coffees, avocado on toast. Why in my day we had 37% interest rates, walked barefoot everywhere in the snow, drank water straight from the garden hose, black and white TV. Today's whippersnappers don't know how good they have it.

That is the probelm with cheap credit, it allows people to buy things now, rather than save. I would rather have 20% interest rates and cheaper priced houses. It means people have more incentive to borrow less and pay off their mortgage quicker.

Rob - almost nobody understands where the end-game is going. That's because we chose to believe a false narrative, peddled by in-house high priests.

The difference between that social narrative and the truth (that we are chewing into a finite planet at an unsustainable rate and are rapidly hitting the Limits to Growth) was big enough to accommodate wikileaks. If there had been no divergence, you would never have heard of Assange. How it ends is almost certainly financial collapse - there being not enough planet left to honour the forward bets, and enough people realising this, then panicking. In existential, ecological and every term except 'financial', we'll be better off. And it was just a self-delusion of a temporary nature.

The economy was humming along fine before the last few OCR cuts. The RBNZ is following trump policy of expanding the economy when it was already going well, forming huge public debt to go with it and wanting interest rates to drop to promote it. Problem is, there will be no room to run when the economy ACTUALLY takes a crap.

I refer to the NZ economy apart from housing prices, which needed to come down substantially anyway as they were extremely overpriced and still are. RBNZ policy is trying to artificially prop up the housing market when just a couple of years ago everyone was talking about having to get housing prices down...Just crazy....

The fact that the RBNZ feels the need to justify its policy suggests to me they are not confident they are doing the right thing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.