Summary

• Higher US wage and European inflation data triggers further increase in global rates

• Fed widely expected to raise rates 50 basis points this week but the market is now pricing an almost 50% chance of a 75bps hike in June

• Aggressive central bank tightening, underwhelming earnings outlooks, Chinese lockdowns, Ukraine war make for a long list of headwinds for risk assets

• US equities tumble on Friday (S&P500 -3.6%, NASDAQ -4.2%)

• Amazon crumbles 14% after providing disappointing revenue guidance, says it has over-invested

• Bloomberg reports that EU is preparing to phase out Russian oil imports by end of the year

• Chinese policymakers promise more support for the economy - Chinese equities higher but commodity markets unimpressed

• USD lower on Friday but still has its best month in years

• NZD falls to fresh YTD low amidst rising risk aversion; down over 7% in April

• Big week ahead: Fed (+50bps), BoE (+25bps), RBA (+15bps) all expected to raise rates. NZ Household Labour Force Survey (HLFS) expected to show fresh multi-decade low in the unemployment rate.

Good Morning

Global rates moved sharply higher again on Friday, following upside surprises to US wage data and European core inflation. The Fed is almost universally expected to raise its cash rate by 50bps this week, but the market has moved to price an almost 50% chance of a 75bps hike (!) in June. The prospect of aggressive central bank tightening and underwhelming earnings outlooks from Amazon and Apple saw the S&P500 and NASDAQ plunge by around 4%, capping off a dreadful month for risk assets. The NZD and AUD were weaker on Friday amidst weaker risk appetite, the NZD ending just above 0.6450, a more than 7% fall on the month.

The Employment Cost Index (ECI), considered one of the most comprehensive measures of US labour costs, was much higher than expected in Q1, reinforcing the market’s heightened inflation concerns. The ECI surged 1.4% q/q in Q1 (1.1% exp.), its largest quarterly increase since the survey was established in 1996, in part due to a jump in benefits payments (such as pensions). On an annual basis, the ECI is now running at a 4.5% pace while private sector wage growth is even higher, at 5% y/y. The data corroborates the elevated readings coming from other wage measures, such as the Atlanta Fed’s Wage Growth Tracker, which is tracking at 6% y/y.

With the US labour market exceptionally tight and wage growth running above levels consistent with the Fed’s 2% inflation target, markets expect an increasingly aggressive response from the Fed. Markets are fully pricing a 50bps hike at this week’s Fed meeting, given it has been well telegraphed by Fed officials, including Chair Powell. However, the market is now pricing an almost 50% chance of a 75bps hike in June, as well as another 50bps hike in July.

The last time the Fed raised (rather than cut) the cash rate by 75bps was in late 1994, towards the end of that tightening cycle. Market pricing is consistent with the current tightening cycle being even more aggressive than the one in 1994, which famously caused another brutal bond bear market.

In Europe, headline inflation was in line with expectations, at a post-euro high of 7.5% y/y in April. But market attention focused on the much higher-than-expected core inflation reading which, at 3.5% y/y, is now well above the ECB’s 2% inflation target.

ECB Chief Economist Lane confirmed that rate hikes are coming, telling Bloomberg TV “the story is not the issue about are we going to move away from -0.5% for the deposit rate, the big issue which we do need to still be data dependent about is the scale and the timing of interest-rate normalization.”

The lack of pushback against market pricing for ECB rate hikes from Lane, who is usually considered one of the most dovish members of the committee, is notable. Lane added that the weakening in the euro would be an “important factor” in determining their forecasts.

In contrast to recent cycles, where currency strength has been a constraint on policy tightening, EUR weakness is exacerbating inflationary pressures in the current cycle. The market is now almost fully pricing a 25bps ECB hike in July and 3.5 hikes by the end of the year. The 2-year German rate was 6bps higher on Friday, at 0.26%, close to its highest level since late 2013.

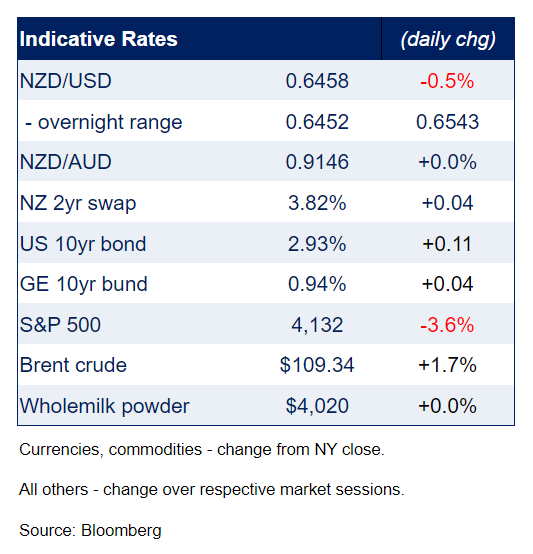

In some ways, the price action in equities and rates on Friday was a microcosm for the month of April. Bond rates surged higher as the market braced for more aggressive central bank tightening with inflation concerns top of mind. US Treasury rates were 10-11bps higher across the curve, with the 10-year rate ending the session at 2.93%, just below the psychologically important 3% mark.

The German 10-year rate was 4bps higher, at 0.94%, closing near a seven-year high. The 60bps increase in the US 10-year rate during April was its biggest one month move since January 2009. The Bloomberg US Treasury index is now 12.3% lower than its peak in mid-2020, by far its biggest drawdown since at least the early 1970s.

Talk of 75bp Fed hikes is hardly doing the equity market any favours. Investors are coming to the realisation that the so-called ‘Fed put’ is quite some distance away, and the Fed is not going to bail out the equity market by deviating from its hawkish path while inflation remains so elevated.

The NASDAQ was down a huge 4.2% on Friday, ending a miserable month for tech stocks.

On the month, the NASDAQ was 13.2% lower, its worst month since October 2008, while the S&P500 didn’t fare much better, down 8.8% on the month (-3.6% on Friday).

Shares in Europe weren’t hit as hard, despite the proximity to the Ukraine war and spiralling energy prices, with the German Dax down only 2.2% in April and the EuroStoxx 600 index 1.2% lower. The outperformance can partly be explained by the differing composition of the indices, with European benchmarks typically more heavily weighted towards the likes of industrials and banks, while US indices have far greater exposure to interest rate sensitive tech stocks.

All sectors in the S&P500 were in the red on Friday, with Consumer Discretionary (-5.9%) leading the way as the market factored in a weaker revenue outlook and more cautious guidance from Amazon. Amazon said it had overinvested in both its warehouse space and labour force and now had excess capacity. Amazon’s share price crumbled 14%, weighing on both the S&P500 and NASDAQ given its chunky weights in both benchmarks.

Meanwhile, Apple’s share price fell 3.7% despite beating analysts’ earnings estimates, with the company warning that supply disruptions, including those related to the lockdowns in China, could hit revenue by $4-$8b in the current quarter. Consumer discretionary stocks on the S&P500 underperformed staples by a whopping 15% in April, a sign that markets expect consumers to rein in discretionary spending as real disposable incomes get hit by rising inflation.

Notionally, ~80% of companies have beaten earnings estimates this quarter, but investors have focused on more cautious guidance from companies ahead of what is likely to be a much more challenging macro environment ahead.

The Ukraine war remains another major headwind for risk appetite. In news over the weekend, Bloomberg reported that the EU would propose a ban on Russian oil, to be phased in by the end of the year, although such a move would require unanimous support and some countries, such as Hungary, have been resistant to this point.

Meanwhile, the UK’s defence secretary warned that Russia could formally declare war on Ukraine on May 9th, when the country celebrates the end of WWII. A formal declaration of war, rather than the ‘special military operation’ term that Russia has used to date, would enable it to call up reservists and replenish front-line forces, likely signalling it is preparing for a drawn-out conflict.

Chinese policymakers continue to make more noises about providing support to the economy. A statement from the Politburo on Friday vowed policies to meet the country’s ambitious 5.5% annual growth target while promising to “strengthen infrastructure construction in an all-around way.”

The statement also said policymakers would “support healthy growth of platform firms”, seemingly signalling a shift away from the regulatory crackdown on tech firms. The announcement sparked a 2.4% increase in Chinese stocks on Friday while the Hang Seng rallied 4%, bringing its two day move to almost 6%.

There was less obvious enthusiasm from commodity markets at the possibility of an infrastructure-led fiscal stimulus, with big question marks remaining around how this might be achieved if a significant proportion of the country is locked down. Copper was up only 0.8% on Friday while Singapore-listed iron ore futures were down 1.2%, suggesting the market isn’t expecting a ‘big bang’ stimulus like that seen after the GFC.

The Chinese PMIs released over the weekend reinforced the case for policy support for the economy. The Manufacturing PMI fell to 47.4 while the Non-Manufacturing index, which covers services and construction industries, tumbled to 41.9, well below market expectations. The market remains concerned about the impact on global growth (and supply chains) of prolonged Chinese lockdowns as the country pursues its zero-Covid approach in the face of Omicron outbreaks.

Turning to currencies, the USD lower was on Friday (DXY -0.6%, BBDXY -0.3%) but it still recorded its best month in years. On a DXY basis, the 4.7% increase in April was the biggest increase since 2015, while the broader BBDXY index’s 4.5% gain was its best since 2012. The sharp escalation in Fed rate hike expectations and increase in risk aversion during April has been a potent combination for the USD.

After falling sharply the previous day, the CNY stabilised on Friday, with USD/CNH edging back down to around 6.64. Likewise, after breaking above 131 on Thursday night in the wake of the BoJ’s renewed commitment to its Yield Curve Control policy, USD/JPY nudged back below 130 on Friday.

Meanwhile, the EUR rebounded 0.4% to 1.0545, helped by the higher-than-expected European core CPI data and more hawkish comments from ECB Chief Economist Lane.

Commodity currencies remained under pressure on Friday, even against a weaker USD backdrop. The NZD and AUD were both around 0.5% lower while the CAD was off 0.3% amidst the sharp falls in US equity markets. The NZD was off a massive 7% in April, its worst month since mid-2013, ending just above 0.6450.

NZ rates were 4-7bps higher on Friday, reversing the previous day’s falls, with the 2-year swap rate ending at 3.82% and the 10-year rate at 3.92%. Volatility remains extremely high, and liquidity strained. Aussie bond futures’ yields have increased 8-10bps since the NZ market close, which will set the tone for the local market when trading reopens this morning.

In domestic data, the ANZ consumer confidence index rebounded in April although, at 84.4, remains mired at levels below those seen during the depths of the GFC. Confidence is facing multiple headwinds including sharply rising mortgage rates, falling real incomes due to high inflation, lingering Covid uncertainty, and now falling house prices. At face value, consumer confidence is at recessionary levels.

Big week ahead

It’s a big week ahead. The Fed is almost universally expected to raise its cash rate by 50bps and announce the start of Quantitative Tightening (‘QT’) at Thursday morning’s meeting, while the RBA and Bank of England are also expect to lift their policy rates. The US nonfarm payrolls report takes place on Friday, with the market looking for a 390k increase in jobs and a fresh low of 3.5% in the unemployment rate.

The domestic highlight this week is the HLFS labour market report, where we (and the market) are looking for the unemployment rate to nudge down to a fresh multi-decade low of 3.1%. (It was 3.2% in the December quarter).

In the session ahead the ISM Manufacturing index is expected to increase slightly, to what would be a still healthy 57.6.

*David Chaston is away on holiday. Nick Smyth is Senior Interest Rate Strategist at BNZ Markets. BNZ's full Markets Today report is here.

69 Comments

How do you maintain productivity, let alone increase it, when skilled workers head offshore and nobody is allowed to come in to replace them?

Long term you offer to write off 1 year of higher education debt (Uni/Polytech/Apprenticeship) for every 5 years full time equivalent work in NZ.

You charge interest on student loans if you start working overseas which stops accruing on your return. You work with international governments to take student loan payments out of overseas income.

Short term?

pass.

Tinkering with student debt peanuts 🥜 will only keep the monkeys 🐵 around.

To retain skilled professionals you need to first understand why they are fleeing in droves and then meaningfully address why it's increasingly such an undesirable place to live and work.

Until then the human capital flight is only going to accelerate. ✈️✅ The best and brightest are smart enough to see where this country is presently headed. ⤵️

There is something in abundance abroad that is very scarce in New Zealand. Life opportunity.

Yes, nothing to do but just wave them out the door.

This is what is going to happen. We've already seen lardboy dismiss the issue as "kiwis have always left and then they come back to have families".

Except they now won't, because raising a family in New Zealand is no longer economically viable for most people of child making age.

And nobody of sound mind wants to live in their racist co-governance utopia.

Yes, I think Covid showed the wording has changed...

Kiwis aren't coming back to "Have" families.

They are coming back to "visit" the family that remained.

Lol yes millennial kids coming back to catch up with boomer parents who are cruising the country in the RV, with the e-bikes, sipping lattes, collecting rental income and superannuation and telling the kids to stop eating the smashed avocado so they can afford a house!

Just plain wrong Brock. Breeding fatherless children is extremely economically viable. But don't stop at one or two. Have at least 6, that will get you a great income and a decent sized house.

Forget house flippin.

Looking after a couple of small children even with two parents is relentless. I could not fathom six as a single parent. This strategy is not a good one.

Once again I find myself agreeing with you Brock. I worked most of my life overseas as a successful manager of large projects (much bigger than those seen in NZ). All my projects were bought in on time and under budget. To test the waters as to whether I could survive in NZ in a working environment rather than simply planning on retiring here, I got a job at my local Council. The job was way below my skill level, however, I dumbed down my resume and gave it my best shot. You guessed it, I lasted two weeks. My problem was that I wanted to take a contractor to task for doing poor quality work and demanded the job be fixed (told to stay quiet and leave the contractor alone). I spent three hours per week sitting in meetings where everything that was said was repeated in Te Reo (even though there were no Te Reo speakers in the room). I had members of my team sitting for hours playing on their computers and once again was told to let it be. With an "A" type personality, the slow pace of of work and the acceptance of poor quality workmanship and budget over-rides (that rate payers would have to live with), was a step too far.

You did well to recognize the problems and get out quickly.

NZ councils are a perfect example of Parkinson's Law in action.

NZ was so lucky to have an inexorable talent such as yourself grace our fledgling backwater for such a fleeting time. We are eternally grateful that you were able to withstand our naivety and puny budgets for as long as your superior intellect could manage. We are far worse off without your demi god like vision and management, and your universal understanding of time and culture will be sorely missed.

You failed to repeat this in Te Reo. Your career is doomed already.

Don't you just write it on your CV? You don't actually have to know how to speak it..

What did the guy you were ridiculing just say about what happened in the council meetings?

Councilperson Jobsworth says everything must be repeated in Te Reo to comply with virtue legislation.

The young and the skilled are leaving because they can see the writing on the wall. NZ is spiraling down the path of an socialism/communism and is dominated by a 16% minority. Democracy is being subverted by a government that is replacing elected reps with centrally appointed officials. They are creating duplicate bureaucracies with 50% of those appointed coming from the 16% with family ties. If you're young and talented then there is no point sticking around unless you're one of the 16%.

y/n - bollocks.

We need to be along. long way further along in the discussion than that - 1958 is past, OK?

1840 is past powerdownkiwi, OK? Biculturalism is backward thinking. We're a multi-ethnic, multi-cultural society now, in case you hadn't noticed? Centralisation and twin bureaucracies based on race will only create division and send us bankrupt.

Disagree -

The opposition leader, outlining her economic ideology to RNZ in a lengthy interview, was asked if she agreed with former Prime Minister Jim Bolger's assessment of neoliberalism in New Zealand: that it had failed.

"Yes," she replied.

"Neoliberalism" traditionally describes the political shift in the 1980s towards privatisation of government services, a focus on individual freedoms over collective good, and a general glorification of market principles.

But she offered no solution right?

Politicians these days have neither vision nor courage to effect the change required. They're too afraid of the big money. And shallow commenters like YeahNah, above, apply emotive terms such as 'communism' or 'socialism' to changes necessary to ensure everyone gets a chance to participate.

When officials are appointed any not elected then only the appointed and their cronies get a chance to participate. Our PM is a former President of the International Union of Socialist Youth. Their policies are taking us down the road to socialism. Wake up and smell the coffee!

The label is too emotive, the undermining of democracy is the problem. If they were true socialists they would promote the voice and participation of the people. But like all ideologies it is about power and privilege. Socialism is today, a derogatory term about those who would take wealth from the rich and give it to the poor which is an ideology that would be doomed to fail before it begun. As Maggie Thatcher is famously quoted; "The problem with socialism, is all too soon you run out of other peoples money". So Adern by action, is not a socialist. None of the Labour leaders in my time have been. But they are all anti-democratic, because they all seek to extend their terms, reduce their accountability to the people and increase their privilege. So the path they are on is not socialist. To push you words back on you, wake up and try thinking about it!

Yer Nah

Teh application of the word "socialism/communism" undermines your credibility. it is not socialism to ensure everyone gets a chance to participate in the economy. The issue is, all over the world, is that democracy is being undermined by elites. In small countries such as NZ, the effects are more readily apparent, but it is happening everywhere.

I do wonder how long it will last. History suggests we hit a tipping point and the walls get torn down (and occasionally heads are removed).

If everyone is participating then why are they leaving in droves? And creating a 16% elite where membership is based on family history is not undermining democracy? See comment above on socialism. https://thestandard.org.nz/ardern-to-lead-iusy/ Nice happy snap of Hipkins there too.

I'm not sure I understand your point? People are leaving in droves in part because of what I said in another post; "The issue is, all over the world, is that democracy is being undermined by elites. In small countries such as NZ, the effects are more readily apparent, but it is happening everywhere."

I view the desirable state to be that of democracy; where Abraham Lincoln's words at Gettysburg are the fundamental principles, and the Government is fully accountable to the people. As I has said the trend today is to undermine democracy, but that is not socialism it is authoritarian, which Trump wanted, but the US is more like a Plutocracy, ruled by the wealthy, and we due to a lack of courage by our politicians are getting very close to that too.

But enough about property investors fleecing the young for their wealth...

Though it's a fair point. Young and skilled are leaving rather than having their wealth transferred to older asset owners via silly tax, economic and housing policy that penalises hard work and rewards sitting on assets.

With socialist central bank and direct welfare policies seeing >$4 billion in landlord subsidies and another $14 billion in universal pension welfare benefits, plus many more billions in transfers of wealth from wages and savings to assets...all this ridiculous socialism for the wealthy is making NZ a poor offering for younger, talented people.

Student loans <$1b per year. Superannuation >$14b per year.

Reduce public sector employment by 5% every year for the next ten years.

So fewer teachers, nurses, police etc?

no thanks.

unless you mean the Wellington bureaucracy, with which I would agree.

If it's Wellington? REDUCE 30% a year for two years. Then look at the rest to see who benefit New Zealanders.

It's that principle that it's needed "if it makes the boat go faster"

Well productivity increases usually come by increasing investment in technology, rather than simply hiring more people. See the fruit picking industry which chooses to rely on cheap foreign labour rather than investing in automated fruit picking machinery.

tech for farming has been around for decades, but we have had politicians that rather that help them advance the industry bow down and let them import cheap labour instead. time after time i hear we need to import diary farm managers from india or the phillipines, please explain to me again how is their diary industry even comparable to ours and where did they gain this experience. that and the other one kiwis are lazy, no they will question a request if they see a better way. ie go hand dig that fence line while the tractor and drill sit in the shed or hire a post hole borer for a day and get the whole fence done , where as an immigrant will just toddle off and do it. and this from me that is a shareholder in two farms who rolls his eyes when i hear this , i also have had family work in the industry that have now moved on to better pay and conditions in other industries

Perhaps we could think about whether we should be importing more skilled labour or actually training it locally? It's about time Kiwis woke up to the reality that it's not just migration at the unskilled level that pulls down wages - many occupations are on 'skills shortages' despite thousands of them graduating from our universities a year.

I mean the answer never seems to be: pay locally trained skilled workers enough to actually make ends meet. Maybe that's the actual problem, not the closed borders?

Skills shortages are areas expecting growth and need for skilled people in the future. It just means universities and polytechnics are able to sell qualifications that aren't valued or needed by employers. Especially when we can just import "experienced" professionals. High levels of people studying also make unemployment figures look good. Tertiary education is a booming economy in NZ at cost of students and tax payers.

we used to train all a big proportion of our trades people through our government departments ie MOW , mechanics, electricians, carpenters, painters, NZ Rail, fitters and turners, welders, Air NZ same, etc etc and when we sold those off or privatised them all that went out the window. and it took decades for the government to realize what they had done and start the apprenticeship scheme. instead they focused on sending as many as they could to university and ignored the rest of the workforce that is needed.

To pay people more the money needs to come from somewhere. It would be better to have prices come down.

But central bank policy curb stomps that from ever happening. Prices must always go up.

You improve competition in the market by removing regulatory hurdles that keep those market hard to penetrate breaking up duopolies.

Free education is another long term strategy. It's beyond me why the world hasn't figured that one out long time ago. The more free and open-sourced knowledge there is, the more productive and skilled people will be.

Intellectual property and paten laws, copyrights and all that garbage have one single thing to do, protect the financial interest of whomever came first (even if they have never built/invented a real thing!!!) and hamstring innovation and progression of humanity.

Wow a good chance of a 75bps rise at the FED, who would have guessed ? I might be right with the next MPR on 25th May after all. Looks like another 50bps is a given.

Yeah I agree. I am ready to concede I was wrong on the OCR. It is likely to be lifted 50 BPs next meeting, and it’s likely to go to at least 3%.

Employment is holding up more than I expected, so there’s no reason not to raise quite aggressively.

The housing market isn’t really a reason.

but a warning. Things are eventually going to get even uglier than I thought later this year in terms of the economy, once the lagging effect of a rising OCR really hits.

And I really struggle to reconcile how people can reconcile the OCR at 3% with only minor falls in house prices.

So I hold to my view that the OCR will be pulled back quite a lot by mid next year.

Right when half my mortgage rolls over. A selfish "yes please", but with one eye on the housing market's future for my kids "no thanks"

Yes you look back at when the level of unemployment has been this low...it is often followed by the Fed raising rates into a recession/crash.

The rumours about a building company here in Welly today.

One of the biggest of whats left.

If true, it's going to hurt.

Should be out today

Interesting….commercial or residential?

well I have been calling a construction bust.

Don’t know the Wellington market well.

Commercial

Can you tell me the first letter of the name?

A

I'm not surprised. A lot of contractors priced work at a labour rate of $50 per hour with 10% on marterials in 2020. Now with massive labour issues you need at least $55 per hour on labour to break even & materials have gone up 50%?! You you end up taking a massive hit on materials... You might as well just fold at that point. Its the only way to get out of the loss generating contract.

Ar_______ Do____

* ding ding ding *

There will be plenty more…

Out today. You were correct.

Great summary Nick.

Disagree.

Much minutae about the goings-on on the upper three decks.

Nothing about the iceberg.

RBNZ will be dancing to the FED's tune come what may.

OCR up up and away - housing market and residential construction now stuttering.

The last time the Fed raised (rather than cut) the cash rate by 75bps was in late 1994, towards the end of that tightening cycle. Market pricing is consistent with the current tightening cycle being even more aggressive than the one in 1994, which famously caused another brutal bond bear market.

Hmmmm ..- this didn't turn out well. Currently, US interest rate swaps are hovering above breakeven for term maturities Link

{kind=link}

ECB Chief Economist Lane confirmed that rate hikes are coming, telling Bloomberg TV “the story is not the issue about are we going to move away from -0.5% for the deposit rate, the big issue which we do need to still be data dependent about is the scale and the timing of interest-rate normalization.”

Not that rate hikes or lack of rate hikes would make a bit of difference either way. More QE won’t get the European economy going any more than past QE’s didn’t, just as hiking rates at any pace in between nonchalance and ultra-aggression won’t be able to supply more energy to the constituent countries in place of lost Russian flows.

In at least, possibly, realizing economic (and financial) results and outcomes are not closely connected to monetary policies (QE doesn’t create either inflation or recovery), that would be a good first step even if it has taken this long for anyone to have taken it.

Assuming they have. For once in the modern world, a policy obsession that isn’t totally at odds with increasingly worrisome reality. Link

The Employment Cost Index (ECI), considered one of the most comprehensive measures of US labour costs, was much higher than expected in Q1, reinforcing the market’s heightened inflation concerns.

Inflation-adjusted (constant dollar) private wages and salaries declined 3.3 percent for the 12 months

ending March 2022. Inflation-adjusted benefit costs in the private sector declined 4.0 percent over that

same period. (See charts 3, 4, and tables A, 5, 9, and 12.) Link

Chris Luxon is giving a pre budget speech in Orc Land ... live , according to Stuffed who're covering it ... well , he'd have to be alive to deliver it ... it helps ...

... anyhoo , hoping Gareth or someone will cover it off here at interest.co.nz ...

Then we can spend the afternoon picking over his entrails ...

Be interesting to see if Luxon puts his beliefs in policy and charges his Botany constituents the full cost of their public transport and the Eastern busway.

.... ha ha haaaa ....oh , you are a wag ...

His speech , for what I saw of it , was warm fuzzy waffle ... rather vague ...

.... but , as someone said today , Luxon doesn't need to release lots of specific policy ... Labour are shooting themselves in the foot so often , you could use their feet to strain your spaghetti ... they're gifting an election victory to the Gnats ...

Does seem like he's hoping to be able to avoid giving specifics or real direction on policy if at all possible. Hoping to slide into the job...

Although, does one really want to slide into a job of dealing with cans that have been kicked down the road for 20 years? Just to spend years blaming the previous government and pretending it was nothing to do with one's own party's actions either? Nick Smith was still blaming Labour 8 years after National came to power, and this current government are heading in the same direction...what chance Luxon is just more of the same?

The current PM stepped into the leader of the opposition role about eight weeks out or so from the election, so I'm not sure what standard people are holding Luxon to or how relevant it is. Besides, she arguably made most of her policy direction changes after they got elected. Holding Luxon to something over and above 'abjectly spitting in the face of a democratic mandate' seems hardly consistent...

Key, Ardern, Luxon (possible). Three similar approaches, then.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.