Summary

• RBA joins the tightening club, no longer patient. NZD/AUD falls to multi-year low

• NZD/USD also hits a fresh low, but currently slightly up from this time yesterday

• GDT dairy auction shows big 8.5% fall in prices

• Some slippage in fiscal policy ahead of next NZ election; NZ rates hit fresh multi-year high, albeit driven by global forces

Good Morning

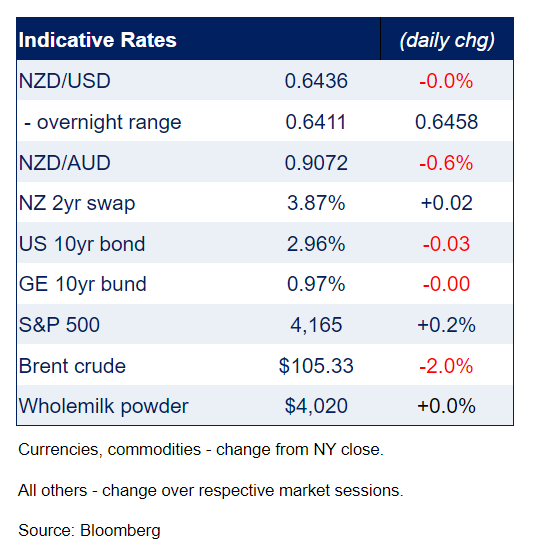

US equity markets remain choppy and currently show a modest gain, following a strong late rally yesterday. The US 10-year rate has pushed slightly lower after returning to the 3% mark. The AUD has been the best major since this time yesterday, although the net gain came ahead of a hawkish policy update alongside the RBA’s first rate hike this cycle. The NZD hit a fresh near 2-year low last night, but now shows a small gain from his time yesterday, while the RBA’s move sent NZD/AUD lower. The GDT auction was very weak.

Equity markets remain choppy, with a strong late rally in the S&P500 soon after we went to print yesterday, taking the index higher and, the index making further gains overnight. In the bond market, brokers report that real money investors bought US 10-year Treasuries after they reached the 3% mark, and they have traded as low as 2.91% overnight, currently down 3bps for the day at 2.95%. There may been some squaring up of positions ahead of the FOMC meeting tomorrow.

A lower US 10-year rate has gone against the grain of a flat Germany 10-year rate, at 0.96%, after it briefly pierced 1% for the first time since 2015, and a 5bps lift in the UK 10-year rate, playing catching to global yields after the May day holiday. Lower US rate spreads have seen the USD weaken a little, with the DXY down 0.2%. It could be another case of some squaring of positioning ahead of the FOMC tomorrow.

Economic data released have been second-tier, but getting plenty of media attention was the US JOLTS report, which highlighted the strength of the US labour market, with a record 11.5 number of available positions while a record 4.5m Americans quit their jobs in March. There were 1.9 jobs for every unemployed worker. The data comes ahead of Friday’s employment report for April, which is expected to show the unemployment rate falling to 3.5%, the low reached ahead of the beginning of COVID19. The combination of labour market tightness and inflation at a forty-year high backs the market’s view of a front-loaded tightening cycle to get the Fed Funds rate quickly up through neutral, and this is the message expected at the FOMC update tomorrow.

European unemployment data were in line with expectations, with Germany’s unemployment rate for April steady at 5.0%, and the euro area’s unemployment rate for March dropping to 6.8%, its lowest level since the euro was introduced. The data comes ahead of what is looking like a very challenging growth period for the region.

Yesterday, the RBA joined the policy tightening cycle, raising the cash rate by 25bps to 0.35%, opting to a take middle ground between the majority who expected a 15bps hike and the handful that expected a larger 40bps hike. The commentary around the move was hawkish, with a significant upward revision to inflation projections and the Bank signalling that this would require a further lift in interest rates over the period ahead. This was a big capitulation for the Bank which, for the first time, finally recognised what the market saw at least six months ago – that Australia was no different to other countries in facing significant inflation pressures and that a significant tightening cycle was appropriate. It wasn’t that long ago that the RBA thought a rate hike wouldn’t be needed until at least 2024 and only two months ago said it would be patient.

Even though the market has been well positioned for a significant tightening cycle, the RBA’s acceptance of this view was still enough to drive Australian rates and the AUD higher. The 3-year bond future is up 13bps in yield terms to 3.16% since the announcement and the 10-year rate is up 8bps. The lift in the AUD to just under 0.7150 didn’t last long and it has fallen back to its pre-RBA level of 0.7090. Still, the AUD has been the best performer over the past 24 hours, but that reflected gains well ahead of the meeting.

NZD/AUD fell from just above 0.91 to just under 0.9040 after the RBA’s announcement, breaking below the 2020 low of 0.9055 to a level not seen since 2018. The cross has since pushed higher, to 0.9070. Last night NZD/USD traded at a fresh low just above 0.6410 last night and it has since edged higher to 0.6430.

The GDT dairy auction price index plunged 8.5% at the overnight auction, more than the 2-3% expected, driven by falls across all product groups. Skim and Whole milk power prices fell 6.5%, while butter was the biggest mover, down 12.5%. The price index has now fallen for four consecutive auctions, taking the cumulative price decline to 13.4% since 1 March. Since that time, the NZD has fallen about 5%, cushioning the blow for prices in NZD terms, and the move comes after an extraordinary surge, so dairy farmers’ incomes will remain very healthy this season. Still, NZ’s soft commodities basket has been underperforming Australia’s hard commodities basket and this has been a key driver of NZD/AUD weakness over recent quarters.

Yesterday morning, Finance Minister Robertson delivered a pre-Budget speech. The key take-out for the market was some slippage in fiscal discipline, with the Government no longer expecting to reach an operating surplus until 2024/25, even though strength in recent fiscal data pointed to surpluses coming earlier than previous forecasts. This suggests a bigger fiscal splurge ahead of the next election and a larger debt issuance programme – adding to the extra debt required as the RBNZ sells its “QE bonds” back to the government.

The fiscal slippage didn’t seem to perturb the NZGB market, with rates up 2bps across the curve, more a reflection of global than domestic forces. The 10-rate closed at its highest level since 2015 at 3.71%. Swap rates were also up 2bps across most of the curve, with the 5-year rate closing at 4.0%, the highest close since the end of 2014, although it did trade above that level intraday last week. The lift in Australian rates since the NZ close could impart a further upside bias to NZ rates today.

The calendar in the day ahead is full. The RBNZ Financial Stability Report at 9am won’t likely be market moving but commentary on NZ’s housing market will be interesting amidst steadily falling prices and rising interest rates. NZ’s labour market reports soon after will be contaminated by the impact of Omicron, so the signal to noise ratio will be low, but evidence of a tight labour market and rising wage inflation should still come through.

On global releases, Australian retail sales, US ADP employment and the US ISM services index are the key releases. All this comes ahead of the FOMC meeting at 6am NZ time tomorrow morning, where a 50bps hike is well anticipated and fully priced, and timing will be given on the start of quantitative tightening, expected to begin soon. There will be more interest in Powell’s Press Conference for a sense how rapid the Fed Funds rate might need to increase and how much beyond neutral it might have to go in light of recent economic developments.

Events Round-Up

NZ: Building permits (m/m%), Mar: 5.8 vs. 12.2 prev.

AU: RBA cash rate target, May: 0.35 vs. 0.25 exp.

GE: Unemployment rate (%), Apr: 5.0 vs. 5.0 exp

EC: Unemployment rate (%), Mar: 6.8 vs. 6.8 exp.

US: JOLTS job openings (m), Mar: 11.5 vs. 11.2 exp.

GDT dairy auction price index (%): -8.5 vs -3.6 prev.

*Jason Wong is Senior Markets Strategist at BNZ. BNZ's full Markets Today report is here.

David Chaston is away on holiday.

90 Comments

Well here's an unregulated industry that's leading to a major crisis that's not making big news - sand extraction.

The world is, believe it or not, undergoing a sand shortage. It's the most extracted solid material in the world, and second only to water in terms of resource usage. It's the basis of concrete, glass and silicon, and we're sucking up 50 billion tons each year, which is enough to build a wall roughly 20 metres thick and 36 metres high...right around the world. In some places farms and forests are being destroyed to get to the sand underneath.

https://www.unep.org/resources/report/sand-and-sustainability-10-strate…

It's almost as if modern life is extremely resource dependent and not sustainable in it's current form.

Then again Apple Airpods are sweet.

And all that sand extraction/transporting/processing is fossil-fueled.

And in both cases we've extracted the best, first.

This will end well.

or....well, this will end.

Well good news, I’m sure given our coastline we have high reserves of sand per capita.

We might be using a lot of sand but what are the proven sand reserves and what is the capacity of erosion to produce sand per annum?

Well a new source of quicksand has just been discovered in NZ.

It's right underneath the property market.

Consents for sand dredging offshore of Pakiri Beach, Mangawhai are currently being renewed to continue dredging millions of m3 over the next 35 years. The beach provides habitat for the critically endangered shorebird - the NZ fairy tern, of which there are only 40 breeding pairs left in NZ. The sustainability of this habitat in the face of continued dredging is uncertain. That said, the dredging provides for much of the Auckland construction sector's concrete and shortages will result if consents are not granted soon.

https://www.newshub.co.nz/home/new-zealand/2022/01/battle-over-sand-dre…

In places like India the 'sand mafia' is a thing.

I also recently found out about the importance of sand and the impending shortage, it is literally being fought over in some regions. I highly recommend this excellent podcast which discusses the issue in a concise and informed way

An acquaintance who bought a house last year for 1.2 million with a mortage of $900000 is worried as his majority of loan comes for refinancing in July and now as per latest calculation he will have to pay $350 - $400 per week extra and if interest rates goes up further will be additional $$$$.

He bought for 1.2 million and same house went uptill 1.3 million (gave him positive feeling, his own words) but today similar house has asking of 1.1 million and as unsold for over two months will be deeply negotiated, so on paper he has lost his deposit by 50%.

As he is home owner, not worried about falling value but worried about servicing the loan as earlier also was not very comfortable but was manageable and now with 45% rise in his outgoing, is concerned.

He is aware of valuation going up and down but in long run will be up but rising interest rate will kill him financially and falling value will only add to his mental stress.

Now that FOMO is dead with housing market as none of the key players in real estate indutry and their lobbyist are able to manipulate to stir up and also their key supporter like government and RBNZ are unable to promote not only now but for some times to come, future looks frightening to all those who over streched under FOMO.

Hope this stops here before the carnage begun.

Frightening perhaps, but end of the day you cant expect sunshine every day. The same fundamentals usually ring true; don't live beyond your means, give yourself buffer and wiggle room, be prepared to work like the devil if you want to retain what you have.

Also, when money is available for around 2%, you lock that in for as long as possible.

Agree but during market frenzy, FOMO was at peak and logic, economy, understanding were all thrown out by greed and for FHB fear of never able to buy the house, if missed now, with the way house prices were going up indoubke digit made them jump and statement from our politicians like house price should never fall only added to FOMO.

This happened not only in housing but more in stock market. Mostly all high growth stocks that everyone was jumping into are down by 40% to 90% and even so called blue chips companies are down by 30% to 50%.

The absolute cheek of lecturing about 'fundamentals' when something as basic as home ownership has been spiked through the roof through speculative lending and aggressive monetary policy.

I keep hearing this statement that politicians said house prices shouldn't fall. Can someone direct me to the source?

I heard Jacinda say that people expected their house prices to rise but that is different to saying they should.

Most people would take any statement from a politician with a large pinch of salt, unless it's vaguely supportive of property prices in which case it carries such strength that it justifies overextending yourself with a million dollar mortgage.

https://www.interest.co.nz/property/108301/pm-jacinda-ardern-says-susta…

Watch the video linked in the bottom of the article if you want to hear it from the horses mouth. Interest's own Jenee called out Jacinda for making such a ridiculous statement. But that's pretty close to a government guarantee that they will do everything in their power to support house prices.

Thanks for link, much appreciated. Will have a listen.

Given the governments track record of not being able to bring house prices down when they have said they want to do so (and actually end up doing the opposite), there's a good chance if they promise to keep house prices them up, they are just as likely to fall than rise.

I listened to the video nowhere does Jacinda say house prices shouldn't fall?

Did you edit your comment Carinanz to change the bit where you said politicians said house prices shouldn't fall?

Bank calls: "Mr. FHB, your mortgage payment hasn't come through this month. What's going on?"

Mr. FHB: "Frightening perhaps, but end of the day you cant expect sunshine every day. "

Thats where working like the devil comes in.

Exactly, the financial literacy of most Borrowers--particularly one like the example above was really on show last year when so few jumped on the 5 year fixed rate of 3% that was on offer for so many months in the first half of 2021. Sure you may not be certain of where your are 5 years out, but one should have known that the likelihood of a consequential break fee was minute at 3%--there was everything to gain, for the cost of less than a point of interest expense short term.

He's got the house he wanted, still there, so value change is no problem.

Rightfully he needs to worry like hell about interest outgoings. Especially as that reduces the opportunity to pay off the mortgage, which is the path to salvation.

This is the lifetime of debt servitude that so many were desperate to sign up for. The bank is the landlord now and the rent is going to the moon and beyond. 🌙🚀

Those who correctly considered it a form of mental derangement to so deeply enslave themselves for the pitiful housing on offer will now be enjoying their freedom to travel ✈️✅ and their ability to enjoy the finer things in life. 🍝🍷💃

I hope that with the recent experiences in tech stocks, crypto and especially kiwi housing we have now learned to recognise the brainless euphoria and other telltale signs of a financial bubble 🫧💥.

The bulk of the lesson on how leverage works both ways is still to come. 💸

Hey but you can upgrade that 3 year old kitchen that the missus don't like ... but then again

The missus will be using it to cook cabbage soup every night until retirement.

Family member had the option of buying a house and sticking with his job....or quitting, becoming self employed an waiting.

He chose the later. He could not comprehend a massive lifetime mortgage that locked him into servitude to a bank bank and employer.

He's feeling pretty good right now.

Sounds to me like you may have got all the brains in the family Rastus. The family member must be on drugs. If you had the chance to get into a house even 18 months ago and didn't you would still be kicking yourself at this point in time. Sure things are looking pretty dire going forward but looking dire and actually becoming dire are two different things as I rapidly discovered with my covid house price crash prediction.

Coming from the guy who believes that Putin appeasement is the correct strategy. Forgive us for not buying what you are selling.

So, what are countries going to do when they can’t afford to pay the higher prices for energy? Well, Janet Yellen, who was the Federal Reserve head and [now] the Secretary of the Treasury says, ‘Well, what we’re going to do is use the International Monetary Fund to preserve America’s unipolar hegemony.’ I think she used almost those words. We have to keep American control of the world and we’re going to do it through the IMF. And that means in practice using the IMF to create special drawing rights, which will be sort of like free money, the bulk of which will go to the United States to support its military spending abroad for all of this huge military escalation. And it will enable the IMF to go to countries and say, ‘We will help you pay your debts and not be foreclosed on and get energy, but it’s conditional.’ On usual conditions: you have to lower your wages; you have to pass anti-labor legislation; you have to agree to begin selling off your public domain and privatize.

The energy and food crisis caused by the NATO war against Russia is going to be used as a lever not only to push privatization, largely under control of US investors and banks and financiers, but it’s also going to lock countries into the US orbit all the more, both the Global South and especially Europe.

One casualty is obviously going to be Europe and the euro. The euro has been plunging in value day after day after day, as people realize that it’s lost its export markets in Russia and much of Asia, and now at home, too, because exports require energy to be made. Its costs of imports are going up, especially energy. It’s agreed to use, I think, now $3 billion to build new port facilities to buy US natural gas—liquified natural gas at three to seven times the price that it’s paying now, which will make it almost impossible for German firms to produce fertilizer to grow crops in Germany. The euro’s plunging.

The largest plunge of all has been the Japanese yen, because Japan imports all of its energy and most of its food and is keeping its interest rates very low in order to support the financial sector. And so, the Japanese economy is being sacrificed and squeezed. And I think this is…you can’t say, ‘Gee, this is an accident.’ This is part of the plan, because now the United States can say, ‘Of course we don’t want your yen to go down so much that your consumers have to pay more. We will, of course, give you SDRs—special drawing rights—and we will give you American aid. But we do want you to rewrite your constitution so that you can have atomic weapons on your soil so that we can fight against China to the last Japanese. Just like we’re doing in Ukraine, let us do it for you.’

And, of course, the Japanese love that. The government loves that idea. They love sacrificing the population, which is what they’ve been doing ever since the Plaza Accord and the Louvre Accord of the 1980s that basically wrecked the Japanese industrial economy from this huge upswing to just a mass shrinkage.

So, those are the economic effects of the war. And in the newspaper, you think the war is all about Ukrainians and NATO fighting Russians, and it’s really a war by the United States to use the NATO-Russia conflict as a means of locking in control over its allies and the whole Western world, and in Janet Yellen’s words, re-establishing American unipolar power. Link

It says ""the NATO war against Russia"". But Russia says it is not a war. Whose troops are where?

What an absolute load of Bo****cks.

Sure is Brock or die trying to change it, the choice is yours but my pick is you would be running away with the women and children and not staying to fight. You couldn't even handle NZ so you had to run to Aussie so forgive me for not buying what your selling.

Lol Neville 67,

You know collaborators were shot by their own people back in the day right?

If you had the chance to get into a house even 18 months ago and didn't you would still be kicking yourself at this point in time - Carlos it is you me thinks on the drugs with that comment?

“Ultimately there’s no natural income streams to be able to service and repay loans. What you have is capital gains which are contingent on the game continuing. So it’s a Ponzi scheme. says Werner. - https://wire.insiderfinance.io/richard-werner-qe-infinity-707e2c627e03

Good anecdote and there will be many in that situation.

our mortgage is just over 500k, and we will re-mortgage in November. It won’t be too bad for us - our mortgage isn’t too high, and I will have paid off a couple of loans by year’s end. Our net financial position will be similar to now.

I am expecting quite a nasty recession, global and local, and my view is that the OCR will start being cut by mid next year.

Therefore my plan at this stage is to float for a while late this year, before fixing again in 2023.

But with things so volatile I will of course keep an open mind.

Why do you have a mortgage and loans? Surely the mortgagae rate is lower than the loans.

New car loan, 3 year term, at 0% interest.

So you purchased a new car when you had a mortgage? Wow.

Yup ...Kiwis love cars and status symbols

You're going to have a mortgage for 15-30 years most likely, so upgrading cars at some point in that timeframe is pretty much a certainty. And with prices the way they were/are no reason not to go new when 2nd hand is selling for the same price as new anyway. Hopefully it was an EV if that works for HM, the fuel savings make it a no brainer if you do a reasonable number of kms a week and can charge at home.

Exactly, thank you. And second hand cars can be very costly in terms of maintenance, repairs etc.

What’s your point???????

You do realise the "zero" percent interest is a scam right? You pay more for the total car price due to added fees than if you bought with cash

Yawn.

And I put 50% down.

The less personal details you share on here HM the better!

I have some sympathy. People should have been prepared for 4-5%, 2.3% was never going to last forever. But I’m surprised at the speed at which things have changed and that we seem to be heading into the 6-7% range.

Yes we all should have sympathy for FHB. The price of housing has been in some form of bubble since the early 2000's. Remember Morgan/Hickey/Equab were warning of a 30% crash coming even then. But the last 15 years has shown that market forces no longer applied as interest rates were forced down. How long can a FHB sit on the sidelines renting waiting for the correction so they didn't risk putting their family into negative equity, all the while being ridiculed by their friends who did hock themselves to the eyeballs.

Will those that have sat it out for the last 10+ years ever own a home now? Nobody really knows but probably not unless they move to somewhere *cheap*.

We should also fell for those who can't buy a house at all. Big big group.

And a decade or two ago they could.

Indeed, can't blame recent FHB for disregarding fundamentals when the governments and Reserve Bank regimens have worked incredibly hard to make fundamentals irrelevant and house prices sure-to-rise.

A certain Warren Buffett quote springs to mind...

I had a similar conversation with a couple in there late 20's the other day. they went all out and for their first home brought a new build (no landscaping-they are going to try and do that themselves) for 1.1 million with 20% deposit, they said a no brainer as they had a interest rate 3.2%, it comes of this year and they seriously concerned now. (I did ask them why they did'nt buy a lesser house for their first house and work the way up the property ladder, but the wife could'nt see herself in a house with just one bathroom...sigh). .

I mean mortgage repayments will have effectively doubled havn't they? You were getting money in the early 2% in 2020 now you can't get under 4%. I believe one bank (can't remember which) even had a 1.89% special.

The FHB's who brought in 2021 have effectively already lost there deposit due to the price decline and have had there disposable income destroyed by increased mortgage costs and an increased price of necessities such as food and gas. They are getting a triple whammy. In effect their net worth is probably no higher than what it was when they had there 18th birthday 10 years ago..... The lucky generation!

Friends of one of my kids went one better. Bought the $1m house but didn't like it or the school and the sister in laws was way better. Up graded to $1.4m house with bridging finance but haven't been able to sell the first house.

Thats ok, SIL has a big house.

Wonder how much bridging finance there is in use out there cause that's going to be a real b345h

FCM - not often we agree but that had me smiling. Our first place was an old crib (bach) 16ft by 25ft, half of it a walled-in verandah complete with sloping floor made of old packing-crates. No insulation, a busted No1 Shacklock, two rain-tanks, one cold tap, no bathroom.

But no debt......

Yup, kids aspirations these days is way out of league. Many people love to slag off the boomers but we sacrificed big time to get into our first hovel, although most of us did have debt, and for me at least it was big! We couldn't afford to pay other people to do the work on our houses or cars so learned to do it all ourselves. We didn't get the OE trips or the new cars or other toys. cheap and second hand was all we could afford. We didn't have kids until we could afford them and so on. that was just the world we lived in. We didn't blame others for what it was.

Yes back when homes were 3X a single income - Uni was free, and shops were closed on a Sunday. Would you vote to bring it all back?

Damn right I would! I believe the current situation is a condemnation of generations of governments. I do not believe homelessness is acceptable in any democratic society.

I probably wouldn't want it to be so onerous, but i do believe that people need to be realistic about what they can afford.

And who demanded no CGT and no higher taxes ...and brought investment houses hand over fist...???

Investors primarily. But think about it; CGT as it was discussed was to be on the theoretical change in value of a house. With no change in real income, this would have put many home owners on the street. And ultimately as international evidence proves, it would have had negligible effect on house prices.

Don't blame Boomers Baywatch, look at the politicians. they have shafted boomers as much or more than later generations, and utterly failed to understand the consequences of their actions. When peoples saving and preparations for retirement are undermined by politicians, they go wherever they can to compensate. We are now two to three generations past boomers now with little change in attitude from the politicians, so your generations of voters are having the same effect the boomers had - Sweet FA! politicians follow their own agenda once they are in power, and today be warned, they are trying to entrench their power and reduce their accountability even further.

Especially the shops on Sunday.

Yep we were the same, two bed, one bath, spent weekends painting, sanding floors just little things that could add some value, only brought what we could afford and did'nt want to stretch too much, one TV, second hand furniture including cutlery. We did that process 5 times, whilst having kids, to get to where we are now, then I see these young ones trying jump straight into this market carrying huge debt, with interest rates heading back up to where we started, that's not going to be good for the mental health side of things.

Pa1nter - your friend is the start of an avalanche of people with little to no equity and are concerned about their ability to pay higher interest rates .

The RBNZ financial stability report will no doubt admit that their reckless policy choices have put the financial system in a perilous rate where a huge amount of debt is concentrated in a single overvalued asset class, with a high number of very highly leveraged borrowers, in a rising rate environment.

Who am I kidding, they will pat themselves on the back for another job well done, and blame international conditions

In a way it IS overseas conditions

but they are the ones who failed to read them.

Wrong tools......

No regerts Orr...

And Orr will admit that the "wealth effect" plan to prop up the economy was really stupid in hindsight.

Mr Orr will probably resign in a couple of months and let someone else clean up his mess. He will probably go and hide in Europe for 10 years with some cushy job in Luxembourg

... I wouldnt have minded if they'd flooded the productive sector with cheap money ... financing for construction firms , small businesses , exporters , infrastructure funds , medical research ... St John's ambulance ...

But no , they allowed it all to pour into houses ... OMG ... how fricking stupid ...

All this comes ahead of the FOMC meeting at 6am NZ time tomorrow morning, where a 50bps hike is well anticipated and fully priced

...rrrrB?

Money printer goes BRRrrrrrrrr-clang-crunch-bang.

Hope you are right but its still too little too late - a Hallmark of RBNZ.

Little anecdote of the geared up 2020 house buyer is very widespread. I don't think people have a handle on how bad this could be because few making debt decisions were round in the 70s and early 80s. We've got a simular combination of uncontrolled govt spending, over-full employment and wage growth, and falling confidence leading to a weak currency. None of those are going to change in the foreseeable, so inflation is going to have real momentum, and will only be brought under control by aggressive ocr increases.

Agree that OCR has to move up and cannot have emergency measures in place forever. Earlier the better as one bad downturn (whatever one may call it... Recession.... Stagflatioon....) is unavoidable and rbnz could kick the can as much as but not anymore as has come to a deadend, so is not an optionfor Orr.

We're well and truly up shit creek with an orr.

The falling AUD/NZD could have a few consequences

1. A large amount of packaged food in NZ is made in Aussie- this will only add to inflation. Australia is NZ's second biggest importer after China

2. A $100K salary in AUD is now worth $110K NZD. A falling dollar will only make Australian wages look more attractive.

3. Selling your NZ house and moving to Aussie will mean less buying power over there ie the $1M house will now only be worth $900700 in AUD

With this AUD/NZ exchange rate, I really need to chase up and try and hurry up my Aussie super provider in transferring my Aus super balance to KiwiSaver.

Leave it in Aussie. With the falling dollar it's appreciating in value anyway, and to bring it here will just expose you to the taxman.

NatGas surged back above $8, to its highest level since 2008...

{kind=link}

How is Biden going to explain shipping it all to Europe to Americans facing soaring energy bills?

He can't.

Nor can any energy-exporting country keep exporting energy, if it's citizens want it first. And there is less and less to be exported, but more and more demand. So not many exporters left, and getting fewer by the day.

"... a larger debt issuance programme – adding to the extra debt required as the RBNZ sells its “QE bonds” back to the government."

Total Crown debt won't actually change of course. The net result of winding up QE will be billions less in institutional settlement accounts (one form of debt) and billions more bonds held by the private sector (an alternate form of debt). Oh, no wait, one thing will change. Treasury will end up paying an extra billion dollars per year or so in interest payments to the private sector. Great.

But the RBNZ won't be paying OCR to the QE participant bank settlement account owners.

Furthermore, As a sidenote, based on average Treasury yields at the various points that the Fed (RBNZ) has expanded its balance sheet, we estimate that the Federal Reserve’s $9 trillion balance sheet is now underwater. If the Fed was an actual bank, and if banks marked their assets to market value, the Fed (RBNZ) would be insolvent. Link

The billion is a rough estimate of the net figure - assuming a 200 pts spread between OCR paid on settlement balances and bond coupon rates.

"a bigger fiscal splurge ahead of the next election and a larger debt issuance programme"

Or....

"a yuge bribe to buy the next election funded by new debt foisted on you, your children, and their children's children"

There, fixed it for y'all.

It worked for Key and he got a knighthood out of it.

Reagarding Sand

Surfer Magazine did a great article on Sand in their January 2015 issue. They mention "Sand Wars" a documentary by Dennis Delestrac. It was on youtube but I failed to find the link, great watching and a revelation. From memory the Burj Khalifa in Dubai was poured from sand imported from Aussie.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.