By Roger J Kerr

One of the arguments against a cut in the Official Cash Rate next week by the RBNZ is that lower mortgage interest rates at this time would fuel the already over-heated residential property market even more and cause increased inflation down the track.

For inflation to increase from rising property values, the transmission mechanism has to be that of households borrowing/spending up large on their enhanced values and that consumer spending driving demand-push inflation i.e. prices increases occurring because the sellers can get away with it and the buyers do not care and pay up.

Certainly over recent years there is no evidence of inflation coming from house price increases (the opposite in fact).

However, building and property maintenance costs have increased with the increased house building activity levels to address the supply shortfall.

Inflation in the NZ economy always comes from the supply side, not the demand side.

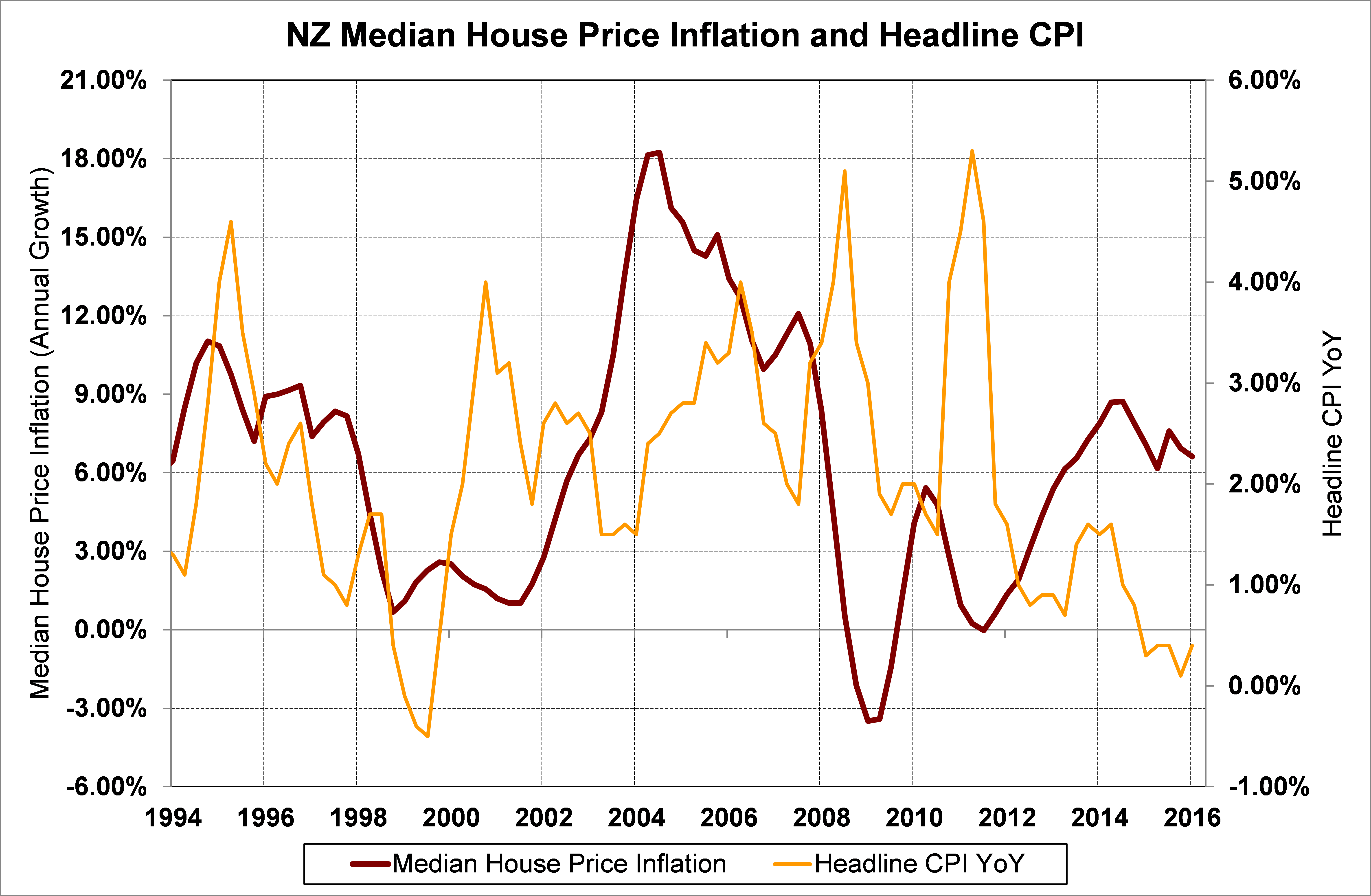

The chart below that plots the relationship between house prices and the CPI inflation rate does not suggest any great cause and effect correlation.

House prices and inflation did fall together in 1998/1999, however that was due to the external Asian financial crisis and plummeting commodity prices at the time, not domestic economic reasons.

Many commentators believed that the RBNZ did not cut interest rates in late April as they were spooked by the resurgence in house prices in March/April, which was contrary to their own forecasts.

The dairy industry desperately needs to the RBNZ to look beyond such an introverted response to getting their own forecasts on house prices wrong.

As more dairy farming debt is put on special monitoring by the bank lenders, the banks’ lending margins will increase due to the higher level of credit risk.

The RBNZ need to cut the OCR base interest rate to off-set those credit-related interest rate increases.

To subscribe to our daily Currency Rate Sheet email, enter your email address here.

Daily swap rates

Select chart tabs

Roger J Kerr is a partner at PwC. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

61 Comments

Wow, I'm surprised to see in the graph that house price inflation was much, much higher between 2003-2008 than it is now and over the last 3 years

I suspect that the current bubble is (or has been) an Auckland story, the mid 2000's; more widespread.

With credit growth now hitting double digits, further easing is unwelcome and potentially dangerous. Is this the same Roger Kerr from last year?

Captured by his masters?

Dairy is in the state he claims because of cheap credit in all the markets NZ producers compete. Delaying creative destruction to eliminate the marginal, but nonetheless, weak, underwater, over producers is not a solution.

agree Stephen...why should we all subsidize dairy with lower rates...what about retirees income from deposits, the housing bubble, savers are rewarded, normalising interest rates so there is a proper price for money...the longer this historically low rate environment continues the more mal-investment we'll have

For there to be any significant improvement for the dairy industry payout the NZ dollar would have to collapse. The problem is that the milk prices of the past are just that of the past. It was a once in a lifetime event , most likely not to be repeated and farmers need to get over the fact that the suck investment costs are gone - destroyed by an over supply. Let those that need to die....

I think they need higher value added products like organics to lift returns but have been to slow, riding the commodity cycle which they foolishly didn't realise goes down. I read a little while ago that nestle were making record profits, as cheap ingredients now from dimwit companies like Fonterra

And do you note how the always talked about CPI is almost in opposite step to HPI? It shouldn't be IF the CPI was a credible index! Instead, this graph highlights a total fraud which the RBNZ play to keep banks profits at record levels in boom and bust times

And it highlights how Labour not only were the precursors to ignoring this house price issue which clearly started about 2003, but also total hypocrites now to complain about the same issue National have exploited for votes. Labour also played the 'lets keep the homeowners and landlords rich' at the expense of everything and everyone else.

The CPI is not really a cost of living index.

Don Brash said recently that it wouldn't hurt the economy to have low inflation for a while...Having said that I did notice petrol has increased in price - maybe we are importing inflation a again.

You are talking 'cost of living', I'm talking house price inflation in direct relation to the consumer price index which is used as a major component of inflation targeting. Why should CPI inflation be at record lows when house price inflation is at record highs, or vice-versa?

This is why to keep a stable economy you should lift the OCR as HPI lifts. You don't lower!

But, due to our economies being hamstrung by needing perpetual debt consumption (particular now around housing) You get a warped scenario we are now stuck in.

Reserve banks (including our own) all admitted that from 2001-2008 they left OCR's way too low for far too long. That would not of happen if they had used HPI figures as a real reflection of overall inflation IMHO

Well that's what I mean. The CPI isn't reflective of most people's cost of living.

Yep big failure by both previous govt of twits and current govt of twits....but the biggest bunch of twits were the various councils and ARC pre amalgamation that were hopeless

Wheeler got a special mention by a currency trader on cnbc for consistently missing his inflation target. It was suggested that the result will be possibly more cuts than otherwise the case as he now has to pay catch up. AUD was suggested to rise against NZD as wheeler plays catch up as opposed to AU reserve bank who's been much much more proactive

Probably from the same carnival barking stable that persistently parades the lower rate story to enrich themselves in the Australian sovereign bond market.

The top forecaster for Australian bonds, the world’s best-performing debt this month after Greece, sees further gains as the central bank cuts interest rates.

“We have, of all the developed countries, perhaps the clearest view that the official interest rate can come down,” said Stephen Roberts, an economist at Melbourne-based advisory firm Laminar Group Pty, who was the most accurate in forecasting the nation’s benchmark yield last year. “The bond market has plenty of potential to perform Read more

These traders never tire of capitalising today tomorrow's taxpayer bond coupon payments which sucks much needed capital from the productive sector and in the process exacerbates deflation.

Meanwhile, NZ lies second in the sovereign bond return stakes, but probably first for the subsequent wealth transfer to foreigners since ~ 65% of NZGS is owned offshore.

Got to keep that Foreign Investment flowing in, so House Prices keep rising, the NZD stays high, exporters struggle, domestic savings are discouraged, we don't get to full employment, wages are kept down and the workers are kept in their place.

Did you see my link here?:

http://blog.mpettis.com/2016/05/the-titillating-and-terrifying-collapse…

Interesting statement in there:

It turns out that foreign investment is only good for an economy if it brings needed technological or managerial innovation, or if the recipient country has productive investment needs that cannot otherwise be funded. If neither of these two conditions hold, foreign investment must always lead either to a higher debt burden or to higher unemployment.

So what happens next?

Are you basing your DIRA submission on this?

Are you emailing each MP (outside of Auckland at least)?

What would Donald J Trump do

https://youtu.be/1FJ6WYtLgbo

I would think that the dairy industry is secondary to the trading of houses now. However, Kerr is suggesting that the beast cannot be contained and there's little point bothering. I tend to agree with him. Actually, the property crash in Ireland has done great things for their dairy industry and their food industry in general. They're a lot more focused on exports at present.

I remain astonished that nothing was done by Bill English to address the housing crisis .

Where are the restrictions for foreign buyers ?

Where are the taxes to dis-incentivise foreign buyers from speculating in our market ?

Why are we not following other OECD countries in quelling the overheated housing market ?

And how is a foreign buyer identified? With beneficial ownership of NZ Trusts and companies as opaque as a mud pool? NZ is too naive in this area. Thus causes the attraction of those wanting a safe haven for funds.

Easy, Force all banks and REA's to take Passport info in regard to all housing loans. Done. See, its not hard.

Banks already do that. RE agents don't even know what day it is in that respect.

Then why is NIck and others having such a hard time (not) getting some "reliable" info? Banks have it all in regards to loans! They have to incase of any defaulters. And they have details of ALL 100% cash buyers of properties as bank accounts transactions can/are all be/being traced.

It is a matter of defining source of funds. Skip a pebble across a pond enough times, it becomes very difficult to determine where it actually originated.

Wait for the election bribes/lies Boatman. They know its still too far out from the next election to start the real BS to the 45.4% gullible.

So true once again Justice. They should have spent big on housing but are holding back a tax cut looky scramble for next year. Sick

Interest rates once they drop below around 2.5% become ineffectual in influencing house prices as other countries have found out.

Will the RBNZ ever again meet their PTA target?

Households simply won't spend the economy into any kind of demand-led inflation, as they sense that the economic system is vulnerable.

Households are short of disposable income to do so whatever the collective inclination.

How about we start with Fonterra restructuring, reducing their costs and returning more profit to their dairy farmer shareholders. Once that's done then lets talk about lowering interest rates.

a good start would be to move the head office out of Auckland to Hamilton or Tauranga

cheaper running costs and cheaper wages. the only reason it moved to Auckland was because the first CEO lived on waiheke island

how much has that cost farmers over the years

Edendale.

And they can do the night shift if necessary.

Nightshift. Brilliant. Headoffice could run 24 hours on each workstation.

12 hour shifts like the Tiwai workers and maybe Edendale.

you're onto it delboy...can't hold economy hostage for a poorly performing company

While I don't agree with Interest rate cuts, they will not impact the property market. It is clear the vast bulk of buyers out there are not borrowing from NZ banks, and are not impacted by the OCR or its impact on Wholesale Mortgage rates.

I am looking for a family home in Wellington. All documents sent to me come in English and Chinese, apologies for not being specific I don't know if it is Cantonese or Mandarin. However, last I checked neither is an official Language of NZ.

So it is truly amazing the level of service offered by real estate agents for what amounts to only "3%" of buyers.

Generally Mandarin script is used by both Cantonese and Mandarin speaking people, especially in foreign countries. You can't really go wrong guessing it is Mandarin as it makes sense to use it for both communities (also Shanghainese) although simply saying Chinese characters is not offensive.

I know the ASB has (probably all major banks have) a Chinese department catering for these borrowers so many mortgages for them are actually sourced locally.

Cheers for the script tips.

My instincts tell me that even if the mortgage is sourced locally, its not the interest rates that are the crucial factor (this applies to local citizens as well). I am yet to hear anyone say;

"Oh the mortgage rate has dropped - I should buy a house".

The 20% LVR seems more of a cap to what people are willing(able) to spend. I am hearing a lot of people complain;

"I have $100k the bank will lend me $400k - that's not enough I guess I keep saving - oh great the interest rates dropped, now it will take even longer to get the $200k deposit I need"

So if anything Interest rate drops should be lowering the price of houses as people can't get to the magic 20% mark.

Investors may be in a position to buy more as a result of low interest rates - but the more intelligent ones I have met seem to be refraining from expanding their portfolio due to the ludicrous prices.

Which brings me back to foreign money - clearly they have far more money behind them. They may even be using foreign mortgages as a deposit? End result is that NZ interest rate changes will not impact domestic house prices.

Asian people often use the bank of mum and dad too although it is more like a dowry, often from both sides, which gives their young people a bit of an advantage. However, on average, they take better care of their old parents as well. This is a bit of a problem with multiculturalism as certain communities have very different attitudes to money and education which can give them certain advantages. These advantages can be self magnifying as Asian kids at school often form nerdy, studious cliques with parents who go to great lengths to give them an edge. For example they will take their kids to tutors who will train them to pass specific exams. Various differences can have big real world impacts. For instance Indian people like to collect gold and precious stones while Chinese prefer real estate.

Europeans have created a fantastic infrastructure for anyone who wants to apply a bit more energy and focus to get ahead. Trouble is many Europeans are a bit blasé about this and don't take advantage of it. Other communities give up before they even start and are destined to fill the lower echelons of the workforce.

Huge generalizations i know but evolution teaches us that it is small differences across a community or group that mean the difference between survival and extinction in the long run. It surprises me that this is not well understood.

If Asians want to live in NZ ,then charge them accordingly.

If they can afford it at the current asking price, then up the price to 3 times as much as that.

If they can then afford that, then say, "Well Maybey I'll think about it."

Market Forces Rule.

"Market Forces Rule."

That's the whole issue, they are setting the market. Problem is I can't keep up.

Absolutely agreed.

Distributed wealth is very powerful but its hard to understand what happens if it fails..or an arranged marriage fails.

Someone may end up doing life..

People may not consciously understand it, but subconsciously everyone is aware of people different to themselves. That in itself is an evolutionary trait.

NZ (the West) would be quite a different place if we were less independently minded and more family orientated. I think it is starting to head that way slowly - maybe not for altruistic reasons of love and happiness. Rather finance playing a big part. Pooled resources and cost savings abound.

When I was living in Dublin in 2008 - the only way a lot of people could afford a house was too join up with all their siblings. Same thing now seems to be happening here - hopefully the impending crash isn't as bad.

That is the real lack of understanding, NZ was barely touched in 2008. We are only just starting to have issues now. A real crash like what happened in Ireland, and we would be toast.

Yes, im from a County Mayo family myself.

Care for your own.

As I read my own post, it just struck me how many similarities NZ today currently has with Ireland of 2008.

Housing has gone through the roof.

Unemployment - while not bad, is not secure.

Companies downsizing via natural attrition - which isn't picked up as readily by the media.

Talk about tourists only dealing with tourists as offshore labour floods the minimum wage jobs.

Talk about the negative impact of tourists, rather than just the economic benefits.

Talk about foreign citizens played down as being tax residents.

adjusting labour laws to encourage foreign companies - particularly for film/tv

Barely taxing foreign corporates,

Younger generation looking at options offshore.

Economy almost entirely at the mercy of bigger players.

Government worried about popularity rather than actual welfare of the citizens they represent.

Media and average joe not picking up/questioning policy until after it has gone pear shaped.

Lack of opposition, whereby the leader is the guy that lost by the least, rather than won by the most.

I could go on, but I am starting to scare myself.

My family were building houses for the first time in 200 years and working at the local factory and farming the commons

Hope it worked out alright.

At this point in time we are led to believe the banks are in a stronger position. The banking system in Ireland really was over leveraged in 2007/8 and most the money was lent to about 15 individuals. I am very surprised that interest free mortgages remain over here as that is where a lot of risk remains. In the UK they are almost impossible to get since the GFC.

....."take advantage of it" being the operative comment. Or put it another way..." Grab all you can for yourself and to hell with everybody else" .

Yes noncents. In Melbourne apartments about sixty percent of purchases are cash or purchasers own arrangements. ie: no mortgage in Australia.

Mandarin is compulsory in schools, they may not be speaking it at home.

Auckland housing market has peaked. Speculative , easy credit, sub prime mortgages, expectations of ever rising prices . Aucklanders will be lost in space in the unwind. The RBNZ may bring forward the inevitable, but as investors jump ship the decline will become historical.

it hasn't peaked and will not, at least not while Jonkey has the immigration floodgates wide open. All you require to get residency here is to buy one residential rental property - the only country in the world where you can slip in that easily and wash your cash eh! The Chinese Mums and Dads have their secret agent student children in a frenzy in the auction rooms of Auckland. The IRD data showed 35% of house buyers are foreign students - who is funding them - Mum and Dad back in China. The lawyers and the Barfoots agents and the valuers and mortgage brokers/bankers all know what's really going on but keeping it under cover as they are making a fortune from this immigration scam. Twyford was right - 39% of Barfoots buyers with Chinese names = a connection to family back home with the students fronting the house hunt in NZ. Not racist simply fact!

Offshore buyers make up an insignificant amount of Auckland home owners. Immigration is not the problem ,it is providing a little smokescreen as you do not need to migrate to purchase a property. Speculation and expectation of future rises is all that is in issue. If the RBNZ puts in mortgage/income restrictions , and it should do , its game over , but the reality is , it is already game over. The Chinese or other do not need to hide their money in Auckland real estate, many other ways to store ill gotten gains.

Most of the Chinese money is not ill gotten. Where is a better, safer, place to invest than Auckland, Vancouver, Sydney, Melbourne for a people that love real estate? There simply are too few of these unique cities. Where do you think they will invest, Lagos, Caracas? Do you think they will trust foreign shares?

The trouble with people like you is that you have no real appreciation of what we have here. It's a bit of a Kiwi tradition to mock ourselves and show contempt for our own culture and heritage. To many outsiders the environment we have created is rather special.

Sadly true. Without a change of government NZ as we knew it is toast.

No Rodger. As John key says dairy is just 5% of the economy. So who cares. Let it collapse because jk and b.e. are right. Ha ha ha.

I find it hard to understand why interest rates should be cut to help dairy farmers. Aren't they in the same boat as anybody else who pays too much for a business and has the terms of trade turn against them. Indeed it was Federated Farmers who lead the charge for the free market paradise we now live in which has seen so many workers lose their jobs.

Why should young NZ couples be forced out of the housing market by the cheap money available to investors but not them to save farmers who have made bad investment decisions.

Was cowpat serious?? Have a think about it cowpat. 3 years in a row we have raised our population by a city the size of Whangarei. Three Whangarei's in 3 years. Auckland council needs $17 billion to service the needed subdivisions for the population growth. Cowpat, if we have 1 million taxpayers, $17billion is $17,000 from each taxpayer and thats not even counting medical and needing more energy generation. Immigrants aren't a smoke screen, they are NZ's unfolding financial disaster.

and our government services have gone backwards, have a look at the education and health increase in spend in the last five years and compare with population and it is standing still.

it is twisting of facts again to say we are spending more on government services, we have to as there are more and more requiring them, and they are struggling to keep up, visit a hospital or school sometime and check with your own eyes

I cant agree Sharetrader.

My experience has been that both the health and education sectors have had a massive improvement in the last 5 odd years.

An immediate family member contracted a terminal debilitating illness 10 years ago.Back then there was no end to the number of counsellers ,phsychiatrists available ..but if you wanted to see an actual doctor or specialist then you waited months.National has had a clean out in the top heavy bureaucracy and hangers on ..and now things have improved markedly .The last 2 visits to A&E we actally had doctors that speak English as their first language which was nice.

If you visit a school now you will find them much more friendly/ modern than 10 or so years ago.

There has been plenty invested in technology/classrooms facilities(some of which has been community supplied ) but to say that it has gone backwards is rubbish.

However I wouldn't say the calibre of teachers has improved..something the govt needs to work on.

I want the old Roger back. The one who repeatedly warned that cutting the OCR would bring a veritable tsunami of inflation in its wake. This would come from the lower dollar raising import prices,all of which would be immediately passed on to the buying public .Of course, he was wrong every time, so perhaps he is now trying to improve his hit rate.

I am pretty sure that there will be further OCR cuts despite the significant oil price recovery, but what will that mean for borrowers? Precious little I believe, whether for mortgages or business loans. I rather agree with Ransome above. Why should dairy farmers be treated differently from so many other businesses which don't get bailed out if they get it wrong?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.