BNZ economists are forecasting that economic growth in New Zealand will stall completely next year and "the danger is that the wheels well and truly fall off".

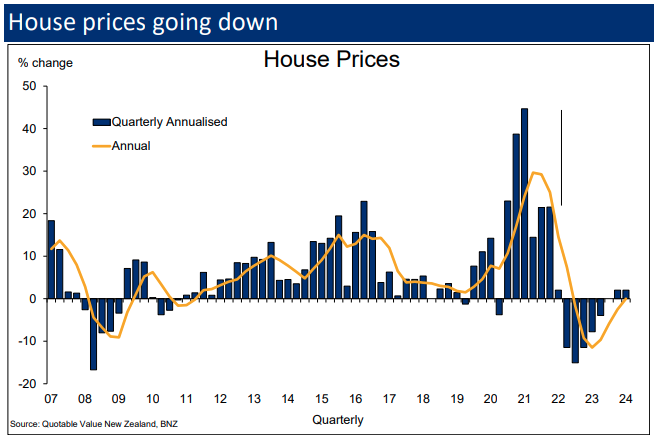

And they say the house price falls that have started will get worse.

In the BNZ's latest Economy Watch publication, the bank's head of research Stephen Toplis says the chances of the New Zealand economy moving into recession are "rising by the day".

"New Zealand’s economic 'imbalances' continue to be exposed at a time when the global economy is increasingly coming under duress," he says.

"The policy measures taken to 'fix' these issues are getting more and more aggressive.

"The chance of a soft landing is fading."

Toplis says the fundamental issue the country faces is that the economy has suffered a series of massive supply shocks. Domestically, the biggest impact has been felt via the labour market. Those suffering with Covid and\or isolating have left businesses short-staffed and needing to employ swathes of temporary staff.

"This is costly and, eventually shows up in selling prices. As if this wasn’t bad enough, closed borders imposed an additional constraint on the supply of labour. And don’t forget labour was already in short supply pre-Covid. Consequently, not only have businesses been forced to take on more labour to cover shortages but they have also had to compete, via rising salaries, for the diminished pool of labour which remains available to draw on."

The labour market has, therefore provided "a major general inflationary pulse" for the economy.

"But labour supply constraints have not been limited to New Zealand. Many of the same issues are being faced across the planet meaning the cost of imported goods is also rising."

And, in New Zealand’s case, the freezing of international supply chains has further reduced the capacity of the economy to produce goods and inflated prices as an auction market for goods in short supply develops, Toplis says.

"As if all this wasn’t terrible enough: the Russians decided to invade Ukraine, and the Chinese decided to impose one of the most severe lockdowns seen on the planet. The former added to supply chain issues and resulted in massive upward pressure on energy prices, food, fertiliser and some base metals costs, amongst other things. The latter simply dropped demand further.

"To cap things off, more recently, the New Zealand dollar has fallen sharply pushing up tradables goods prices even further."

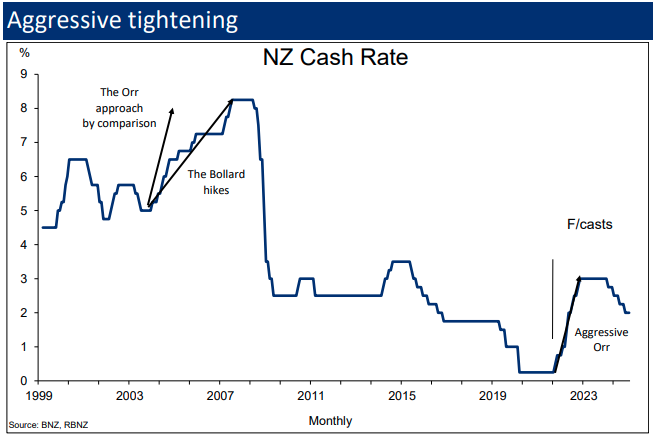

Toplis says in terms of a response to this, the Reserve Bank is faced with doing the majority of the heavy lifting.

"But with inflation and the unemployment rate so far from their respective targets, and supply unlikely to lift markedly in the near term, the only available option is to crush demand to meet the new levels of supply.

"From the RBNZ’s perspective, this means getting CPI inflation down from an expected annual peak of around 7.0% in the June quarter of 2022 back to near 2.0% and seeing the unemployment rate rise from its current low of 3.2% to something of the order of 4.5%. Realistically there are only three ways that this can play out:

- There is a sudden positive supply response both domestically and internationally;

- The economy goes through a relatively protracted period of low growth;

- The economy goes into recession.

"We accept that supply conditions will start to improve. Already, fewer people are isolating because of Covid, border controls are being reduced and global supply chains are starting to ease. But there is a very long way to go.

"Our central forecast, currently, is that New Zealand’s growth stalls completely in 2023. The danger is that the wheels well and truly fall off."

Toplis is expecting the RBNZ to hike the Official Cash rate by a further 50 basis points in the next rate review on May 25, (bringing the OCR up to 2.0%).

And he believes there will be a further a series of rate increases until such time that the OCR reaches somewhere between 3.00% and 3.50%.

"This will represent the steepest increase in the cash rate since the Reserve Bank began inflation targeting, and its magnitude will come close to matching the [then RBNZ Governor Alan] Bollard era tightening cycle which ultimately ended in the 2008/2009 recession, albeit that it wasn’t just interest rates that generated that recession."

On the currently falling house prices, Toplis says, "that is most definitely going to get worse".

"The REINZ’s Stratified House Price Index is already down 4.2% from its peak. And the consensus view is that prices will eventually correct between 10 and 15%. The risk is that they go even further than this. In 2008 the peak to trough house price decline was 10.9%.

"Falling house prices constrain household spending via the wealth effect. Spending on big ticket and discretionary items normally take the biggest hit. This at a time when increased spending by New Zealanders offshore will also constrain domestic spending."

Toplis says whichever way you look at it, "the planets are aligning in such a way that a recession seems difficult to avoid".

"We should note, that when we talk the possibility of recession, we are referring to some time in 2023 when the full impact of rate increases and falling asset prices hits home."

Toplis notes that when/if the recession does eventually arrive, there are a number of factors, this time around, that should moderate the pain that might be felt. In short:

- There is such a strong excess demand for labour in New Zealand currently that the first stage in any economic softening will simply ameliorate the excesses rather than drive the unemployment rate higher.

- Hopefully, an increased supply of offshore labour, albeit modest, will mean that some of the increase in the unemployment rate is more to do with an inability to absorb supply rather than wholesale layoffs.

- The peak in the unemployment rate should be lower than in previous recessions.

- The government’s coffers are in decent nick so extra fiscal spending can come to the rescue if things begin to look dire.

- While there will be fallout from falling house prices, such declines will help make housing more affordable.

- The banking sector is well capitalised so the risk of a financial meltdown is very low.

- New Zealand will benefit from a pick up in tourism as international travel accelerates.

- The emergence from all that Covid-19 has thrown at us will provide some tail wind to the economy.

"There is, of course, the chance a recession does not eventuate but we think, given the way the world is evolving, households and businesses would do best adopting a prepare for the worst, hope for the best strategy.

"Whatever the outcome, we can say with some certainty that growth can only be moderate at best. If demand constraints don’t put a cap on the expansion then supply constraints definitely will."

164 Comments

Good analysis from the BNZ. I have said it before - he’s not flashy, but Toplis is by far the best bank economist in the land.

You're just emotionally attached to his DGM sentiment. His narrative was probably completely different 6-12 months ago.

Yes I imagine he was much less DGM six months ago. So it’s still lagging analysis, the likes of myself were calling this more than 6 months ago.

He’s still the best bank economist though, in my view.

but that’s not saying much!!!

... he's got far & away the best surname ... d'yer reckon he gets sick of guys in the pub saying " hey , I wanna see your wife , Toplis ! " ...

Perhaps he takes the Hyacinth Bucket approach, and claims French pronunciation.

"It's toe-PLEE!"

Like a street in Masterton. Cockburn street. The residents like to pronounce it "co-burn".

Or the old Republican speaker John Boehner (aparently pronounced bayner)

cos that's how that surname is pronounced?

No it's not! Don't ruin it.

Sorry, but Kiwi mangling of foreign names really triggers me.

Actually it is pronounced that way - without the ability to place the German umlaut over an O in English it is spelled oe.

Sorry Falsie spelling and pronunciation are important!

EN

I'm confused, are you saying it's pronounced co burn or cockburn?

went to school with a few kids and they were definitely Co burn and the Port is called Co burn too

Of course you were . Repeatedly

He’s still the best bank economist though, in my view.

And what's your 'benchmark'? Be honest with yourself.

The benchmark is set by the mediocre economists at all the other banks.

zollner is Ok, but nowhere near as good as she thinks she is…

What is your basis for evaluating them? Are you close to thier daily activities?

They are employed by a company who probably evaluates them by different criteria than yourself...

I evaluate them by:

- the rationale behind their views and forecasts

- the accuracy of their forecasts

on both measures they are poor.

Chart looks like a roller coaster just the last part will continue down and if housing market survives it will stay down for a good few years.

I have to agree but to be fair there were quite a few on here prediciting 6 months ago it would all hit the fan in 2023. Next year is shaping up to be the perfect storm, pretty much everything comes together even an election in which Labour will be in total disarray by then.

Yes indeed….

To be fair, there are always a lot of people on this site, predicting a crash. Same as it ever was. It's 50/50 you are going to be right.

To be fair, the chances of either houses increasing or decreasing are based around the economic conditions globally or for the particular country.

At this point given there are clear problems globally and NZ has led the world in asset prices appreciation, it's probably more like 75/25 and that's a glass half full prediction

So Labour will be back to their old tricks of flooding the country with low quality immigration right as recession hits. Brilliant.

Correct but as already posted below before I read this, I think we are in the crapper this time round.

Labour ? ... in all fairness to them , they were slowing immigration prior to Covid breaking out ...

... it was John Key , the Gnats , who flooded the country with unskilled immigrants for 9 years ...

Statistics NZ rejects the premise of your assertion. https://www.stats.govt.nz/topics/migration

Yes. National and Labour are two sides of the same turd.

Nice link.

When the borders were slammed shut in 2020, long term net migration was at its highest level since records began.

This 3 years after Labour campaigned on a platform of reducing immigration.

It was quite public that Labour campaigned on reducing immigration. So what specific action did Labour not perform to decrease immigration?

Last time I checked Immigration NZ were responsible for signing off on Visas. While I do point the finger at Labour, secondarily why couldn't Immigration NZ take heed of the announcement and follow through? Do Governments really need to mollycoddle the highly paid unelected departments into meeting the desired outcomes?

Just because they campaigned on reducing immigration doesn't mean they actually wanted it to happen. Or perhaps they wanted it, then changed their mind once they got into power.

What action did Labour take that indicated they were trying to reduce immigration?

That's what I would like to know. What action should Labour have done to reduce immigration and did they attempt it?

What if the bulk of the movers and shakers of Immigration NZ are largely staunch National supporters and are doing their bit to sabotage the big bad reds? Yes it's rabbit hole stuff, but not an out of place assertion in the current political landscape. Maybe they have performance KPI's based on immigration volumes hard coded into their employment contracts?

They could have done something like they did today (https://www.interest.co.nz/public-policy/115750/green-list-occupations-…), but with a more restrictive set of rules. I don't recall any such announcement. I'm sure Immigration NZ have their issues, but I suspect they were just following the (government controlled) policy over the last few years.

Something sure is off in the immigration Dept. We know foreign doctors and specialists who came here with the hope of gaining residency. They have been stymied at every turn so that now, that, combined with the crazy house prices they are leaving.

On the other hand I recently met a nice young Indian chap and his wife and got talking. He came here from India as a low level hospitality worker and his wife, a seasonal laborer. He got into the country 21 months ago???? What??? I thought that the boarders were closed to all but returning Kiwis.

What the hell is going on? Smells more like corruption to me.

but kept inflation in line, unemployment at the agreed target levels --- and well those house price graphs suddenly make the Nats look like geniuses in that space -- sadly National 2023 is way way short of National 2008 and 2011 - and its hard to see any improvement in the situation !

Immigration tends to drop when there is a recession so this tactic won't save them (or National who follow the same playbook)

Brock,

Look at Gummy Bear's post-he's quite right.

https://www.stats.govt.nz/topics/migration

My memory may be hazy, but Lie-bour were elected on a platform of cutting annual immigration to around 30k per annum in September 2017?

Little was saying that while he was leader, but they seemed to go quiet on it once Ardern got in. I suspect it comes down to the fact that neither major party has a real economic plan beyond more housing debt and more immigration.

Pretty sure everyones best mate, Winnie wanted it cut to 20K P/A. Things sure have worked out well for everyone who voted for this lot.

He is writing a new book..Winnies day out with the protesters

NZ first and Greens had numbers -- Labour skirted around the % drop -- instead saying significant reduction to more appropriate levels ...... and then kept them much higher than the greens or Winston wanted! so rejected the premise of the question and the value of measuring things even before they were elected!

"Falling house prices constrain household spending via the wealth effect. "

Such a sad indictment when so much of our economic activity has been reliant on living off debts others must pay rather than our own productive efforts.

The smell of fear is in the air, Labour are in full panic mode and the borders are fully reopening early. Not sure that this is going to save us this time, the problems are now to entrenched because they have simply been ignored for years.

I think they said October was a 'worst case' end date and always indicated that an earlier opening was on the cards if covid didn't thow any more curve balls.So I think it is hardly 'panic mode', just an abundance of caution,other wise know as common sense...always better to under promise and over deliver.

Wait a minute..are you seriously suggesting that this Govt of ours is capable of demonstrating common sense? Sorry but I don't think so.

but its not like Fields of Dreams --- we can open -- -but in this case people wont be coming -- some yes -- but large scale numbers of tourists -- i think not - NZ has been way too slow to capitalise on the great initial response --- and in the last year has looked more and more out of touch with reality to the rest of the world -- in the same way China's lockdowns are looking to us. Net result huge numbers are not going to chance coming here in case of lockdowns / border closures and tighter restrictions that mean they cant actually do anything whilst they are here -- after all only a couple of months ago we were still in red --- when in the UK and EU -- even Omicron positive people could go to the pub !

I agree, NZ is no longer a field of dreams. My FIL arrived back home from a fishing trip yesterday. He had visited NZ years ago and remembered his time fondly. This trip he stayed in a modest motel (NZ$250), purchased a small bottle of water at the local store (NZ$3.90) and so he continued showing me receipts for meals, etc. His comment about ripping off tourists stuck with me as I'm a Kiwi and I have to pay these rates all the time.

BNZ has a 60 Billion dollar mortgage book. They would have access to swathes of data on the spending habits of those mortgage customers who are fully banked with BNZ. They could see what is coming long before anyone else. The purpose of articles like this are to try and maintain confidence and prevent a recession starting in Q3 2022. Not predicting one in 2023. A monkey with an abacus could do that.

'A monkey with an abacus could do that' : Westie AJ, I laughed out loud!

I love it that some comments here don't grasp that this is essentially a pr piece. What we want to happen mix in with some current data.

This is our opportunity to take our medicine and address the critical flaws in the way our country has been run.

There should be little or no immigration. Further immigration just compounds our problems. We will flood our country with extra people to build the housing and infrastructural shortfall. This may help, but it just increases the shortfall also. We have been saying this for years and the problem just seems to get worse, so is it really getting us anywhere. It is a case of the old story. Insanity - continuing to do the same thing and expecting a different result. (There is a lot of that in the way our country is managed)

House prices need to be allowed to crash. a price to income ratio of 3.5 to 4 is considered as sustainable and reasonable. Ours is 11. something. Supporting this crazy house market is an enormous burden that is born by every employer though wage demands and people though housing cost and all the other social deprivation that follows. How much of our taxes can be attributed to crazy house prices? -

-Working for families

-Housing supplement

- Mental illness

- Health

- Crime

- Increased environmental pollution

- Infrastructure and services shortfall. - Did I not read recently that this was so huge that the government cannot afford to address it and it is going to have to find some other solution. If all these immigrants were such an economic boost for the country then surely you would expect them to have generated more than what it costs the country to accommodate them? They should generate a surplus over and above these costs. May be the best solution to the costs that the government cannot afford, is to reduce the demands on them by reducing the population? An awful lot of the immigrants are low wage workers and as such contribute very little taxes to the government. Net of their cost to the country they represent a loss.

We need high wages to correct our low wage low productivity economy. People need to be rewarded and relocated to employment that is the the most productive and contributes most to our economy. This will not happen if we continue to import cheap labor to prop up the status quo. Those parts of the status quo that cannot cut the mustard need to fail and disappear.

IIRC, 40% of our doctors are immigrants. Our stellar education system is not really producing the goods...

Rubbish. As a multiple repeat customer of the NZ health system, mainly Auckland Hospital's Oncology and Gastroenterology departments, and living with a retired nurse with many friends as senior nurses in the same institution - we train them but they leave. According to the aforementioned sources about half of graduating doctors and nurses already have jobs in Australia and elsewhere on graduation. Similarly, as an UBER Driver who has covered the Greater Auckland area for the last 5 years or so, I can tell you that nearly all young males from high school students through to university graduates are already in the process of leaving or are looking to, especially if they are heterosexual white or Asian. They know, like my two MAGS and Auckland University graduates sons that this country does not want them - and they don't like younger NZ women. As my sons said, "there is no place for us here dad." The elder one runs SONY's New Products Division global supply chain, ironically in the same building his father used to train SONY's managers) and the younger one, the traitorous little bastard, as peirsonal assistant and interpreter for the Australian Ambassador.

Two interesting observations yesterday that lead me to believe that the Labor Govt are going to replace tertiary institution education for nurses with an apprenticeship education. I.E. hugely degrade the nursing profession to a trades skill type vocation.

Chris Hipkins was saying in reference to apprenticeship subsidies, that on the job teaching is far better than classroom based education and that soon they will be moving more in this direction. Nursing is the obvious candidate.

I suspect that Paul Goulter, the nursing union representative is a government plant and that the whole back pay thing is just a fake battle that he will win to get the trust of the nurses. His real task is to make the transition away from a degree training to apprentice style training. He obviously has strong links to the government as is revealed by their appointing him to the board of Air NZ.

hugely degrade the nursing profession to a trades skill type vocation.

I was an early BSc trained nurse in the US many, many years ago. Prior to 'my time' all nurses were trained on-the-job in hospitals.

Typically, a hospital first year student did: bed-making, personal hygiene, feeding patients unable, or lacking appetite/motivation to feed themselves, vitals taking, cleaning up unpleasant things, and walking around with/talking to/comforting patients (i.e., bedside manners). Also, call button answerer in the first instance.

I never got that first-year type experience in my degree programme. To this day, no matter how we train nurses - whether by university degree or polytechnic - I think the first year ought to start at the coal face with all those basic jobs.

Patients would get better care; our registered nurses would not be run off their feet and future nurses would really understand whether or not the profession is for them in the long-haul.

My point, I do think nursing is a vocational calling first, and a higher education/profession second. We should structure its teaching in that order and first-year (and even second year) students should (to my mind) be hospital (as opposed to classroom) based.

Yes, it was the same in NZ till the 90s.

Nurses used to be mainly trained in hospitals. I know because I used to be in hospital a lot in the 1970s as a child and I remember asking what the different coloured epaulettes meant. Most nurses wore pink ones, which meant hospital trained, whereas the staff/registered nurses, who were degree/diploma trained wore blue. Not sure about anywhere else in NZ, but in Nelson we had a nurses home where all the these nurses stayed while they trained.

I'd say 90-95% of nurses were hospital trained back then.

Nurses back then never had anything like the skills, autonomy and responsibilities. The world has moved on a long way since then. Would you want a nurse from back looking after you now without the upgraded skills and closer medical oversight? Would you want to pay for all the extra doctors that they would have to employ to fill the skills gap?

Not true.

We are training enough nurses and doctors for NZ, but after completing their training they are evacuating to Aussie for much more pay, less system pressure, and much CHEAPER HOUSES. This last bit is the number one factor. A close family member has been training specialist in their medical area for the last twenty five years, and in the last ten years this is the number one factor cited by newly minted, or final year, Medical Consultants in leaving for Aussie.

After investing circa 25 years of tax payer supported education and medical care to create these people, and when they have a potential of 40 years of serious contribution to kiwi healthcare and the tax system, we are sending them to Aussie ....essentially for free.

We must support protect the property ponzi owners, who have grown fat on a culture of tax avoidance at all costs...

A blind man can see the problem. If he can pay for private medical he can really see the problem.

Yes, houses should be cheaper in NZ to make up for the lower wages.

But guess what happens when they are cheap, they get bought up by investors or foreigners.

But to be fair the only path the average NZer has to wealth is through property, because we produce bugger all of value to the world.

We nick medical professionals from other countries so only fair they can take ours.

Alfa is sort of right as some medical students we produce don't stay in this country but are replaced with immigrants. I don't have a problem with this so long as the medical people have the expertise required. Maybe the exchange is a good thing as the new arrival in their chosen country perform better than if they had stayed in their existing surroundings.

Cutting immigration would turn us into Japan, with emptying out cities, not into some kind of utopia.

Japan has a declining population. I haven't yet heard many people saying that NZ should have a declining population. It is the big increases that stretch resources.

KeithW

100% we should not be increasing our population.

The falicy of growth for growths sake, whilst societal, fiscal and natural/environmental imbalances continue to grow.

Though I'm of the opinion that we won't need to cap population limits, the cost of living and physical constraints will do it for us.

I thought nz already has a declining birth rate less migration?

Sure is a spectacular corner that central banks have backed themselves into!

The $ 64 dollar question ... will Jacinda " read the room " and abandon Labour prior to the 2023 election ... or , will she lead them into the Valley of Political Death ... volleys of poor polls to the left of them , a booming recession to the right of them ... she leads her cavalry into certain doom ...

Please...and good riddance forever.

I can't think of any group that would have voted for her who are better off except consultants

It's generally the other way around. When National are in there's a freeze on permanent staff numbers so contractor and consulting numbers soar. Then when Labour get in ministries start hiring and many contractors start hitting us up (in the private sector) for better paying full time jobs.

Yep. When I was in government we transitioned from a Nat govt to a Lab one - and the first thing Lab told Vote managers to do was to slash our consultancy budgets.

The weird thing is I despise Labour but my financial situation has strengthened phenomenally over the last 5 years. Look at how your assets (houses, shares etc) have performed. The financial upside isn’t worth the social issues resulting. Cluster F of epic proportions. As Bernard Hickey described, the wealth transfer is staggering benefiting largely older/wealthier kiwis.

I played Monopoly last weekend with my 7-year old granddaughter. Wanting to make the game faster so that she wouldn't get bored - I made a new rule. Every time someone lands on a property that is owned - regardless of whether one has a 'set' of those properties - the property owner not only collects the rent, but he/she also gets a free house (even if it is the property owner themselves who lands on their own property).

Well, what an exercise in today's reality that was! One could accumulate houses without the money to pay for them - just because one had been lucky enough to own one in the first place!

Try it - it's a whole new perspective on the game.

The only realities there Kate are the next generation cannot wait for a house and then just expect one to be given to them.

Preach! Lazy self entitled FHBs expecting anything less than having to pay hundreds of thousands on a deposit for crippling life-long debt.

Not sure who is being referred to, last I checked a roof over your head was a basic human right. That is, a realistic pathway to having a “home”. Anybody who thinks differently is the one who is truly pocketing the welfare cheque…

Virtue signalling drivel.

Property investors

be kind...and stay off Telegram..

Pregnancy announcement and subsequent "stepping aside for more time with family" coming soon to a lectern near you!

Agreed I'm just awaiting some reason that appears "Justified" to the NZ public.

Yep my prediction at the start of the year was Jacinda will be gone before the end of 2022 and I still back that (Labour were in a much better place then!)

I’m wondering if next month she’ll resign and a snap election will be held in September.

She gets out before the recession really bites.

https://thedailyblog.co.nz/2022/05/11/theres-no-way-nicola-willis-will-…

excerpt;

Many blokes have walked away from Labour and the Greens and are voting National because they are sick of Jacinda and our ever triggered woke hysterical activists.

There are 2 things everyone flirting with voting National need to recognise right now.

1: Luxon can do the 45 second CEO soundbite but he has zero intellectual curiosity, he is a devout evangelical Christian whom believes his wealth is proof positive that Jesus loves him. His policies will make things far far far worse in this country in terms of housing, inequality and poverty so don’t pretend voting against Jacinda for him makes you radical or edgy, it makes you a f**kwit

2: Luxon is such a boofhead, he’ll let David run rings around him in terms of pushing through crazy ACT Party policy because Luxon isn’t interested in philosophy, he’s interested in God’s love of him being the best he can be. Policy is something the little people do, and Christopher don’t do little people stuff. National are selling Luxon’s certainty to you, and that’s all.

Something something... what BrockLanders said regarding green checked airplanes... ✅✈️

It would be easy to sympathise with any young person wishing to make tracks with the country hurtling towards economic uncertainty and no clear and obvious leader who will be able to pull through it.

7 houses Luxon has an ulterior motive.

Yes.

there's no way I will vote National, or Labour.

She's getting a bit old for that tho?

Misogyny is alive and well in here...

Yawn.

My great grandmother had five children in total, the first when she was 41, the last when she was 45. She was 15 years older than my great grandfather but lived for a further 22 years after his death. She died just before her 95th birthday. If a woman born in the late 19th century can manage that I'm pretty sure a fit, healthy, pampered woman born in the late 20th century could as well.

It's quite amazing that many commenters on this site, see likely economic outcomes, months before bank economists do

You forget that bank economists aren't university economists- their job is to provide information to their lending operations to ensure income is maximised for shareholders. As such, they only say what's required when they can't avoid saying it, then they tone down the effects to manage the income streams of their employer.

Yes they're only ever going to predict relatively mild house price declines since they'll lose their jobs if they predict a crash and in doing so, help hasten one.

Exactly.

And that explains fundamental inconsistencies in their opinions.

Such as ANZ’s farcical forecasts in late 2021 - that the OCR would increase to more than 3% yet miraculously house prices would only fall 3 % (then changed to 7%, then changed to 10%, then…)

if the economists were any good -- they would all be in private enterprise and cashing in big time on their ability to predict the markets and economic factors ---- but they are not - governments are the same --- hell i have no real idea about high finance and most of the technical talk on here -- but after 18 years of 2 yr, 18 month and 1 yr fixes -- i have a 2.99 5 year fix from march 2021 ---- NO i am not a genius -- but blow me -- it was so so so obvious that things could not go lower than that -- and that it was going to head upwards in a hurry that it was a no brainer!

I also moved all the savings / kiwi saver etc i have ( again for the first time since it started) from high growth to the lowest risk fund i could find -- during the olympics -- hint you never start a war when there is a global media circus !

I am sure heaps of the way smarter people than me on here did exactly the same -- or made better choices than that -

If you want to know what inflation is --- go and ask anyone earning under 60K -- they can tell you instantly what is going up and by how much - not MP's Bankers or economists who simply dont worry that milk went up 50cents or cheese $3 a block -

It was so obvious that even I fixed for 5 years back around then at 3.05%. Unfortunately not so obvious to my wife, who twisted my arm into trading up in December. But happy wife, happy life, location location location, etc.

Haha. Any man who has been in a relationship long enough knows that woman are not happy with what they have. So good luck with that.

It’s impressive ey Yvil

"Reckless bus driver predicts crash"

Lucky I'd just finished my coffee.

Another bank softball trying to maintain confidence. What is the bet the banks have completely cut lending to the bare minimium to avoid eating enormous losses on these overpriced mortgages and going belly up? I suspect at least one or possibly two of the big 4 banks will go broke in the wake of this enormous recession we are about to enter.

There are one or two banks who have been a bit risky over the last few years which immediately spring to mind. Diversify your cash...?

I am getting that feeling, that this majority of commentators stating that the sky is falling or about to fall in NZ, likely in 2022, but definitely will occur in 2023 - will not occur. This relates to a 30% decrease in house prices and significant increases in unemployment. NZ has been resilient during Covid, and I think this resilience will continue over the next few years. The reasoning for this is our current reasonably strong position, and now the messaging and action, albeit slow that NZ is opening to skilled and highly skilled workers. Going to a simple immigration system will help greatly, however, they do need to follow through and resource the Government ministry/agencies involved.

Dreams are free I guess

Not a dream, an opinion.

Having some resemblance of financial literacy is hard in NZ. People like to go by gut feel and the age old saying "house prices always go up".

Works until it doesnt.

Well, as a couple, we bought our first house in Papakura for 120k, and used an additional 30k to renovate it, in 2007. Later we moved and bought into another region in the NI, but kept our first house as a rental. For me, that 150k house has at least doubled every 10 years since we have owned it and it is likely to continue to do so, well into the future.

This will be the year that it halves in value.

Like the fable of Taleb's turkey.

"Consider a turkey that is fed every day," Taleb writes. "Every single feeding will firm up the bird's belief that it is the general rule of life to be fed every day by friendly members of the human race 'looking out for its best interests,' as a politician would say.

"On the afternoon of the Wednesday before Thanksgiving, something unexpected will happen to the turkey. It will incur a revision of belief."

Every decade your rental has doubled in price, reinforcing your belief in the general goodness and upward trajectory of house prices. A sudden inflationary spike is going to cause many Kiwis to experience a sudden revision of belief.

Halve in value? Absolute bollocks and plain wishful thinking - as much as my belief are, as they're all subjective forecasts. I reckon that House prices will decline somewhat (and some seem to be - but certainly not the ones I'm looking at), but it'll be very patchy with the crap out there badly affected but the desirable properties generally maintaining or even increasing. As always, it'll be a supply and demand issue - whilst there'll be a lot of affected people out there, there's still a large number of peeps who've done really really well out of Covid and are well cashed up and able to leverage the situation - you know, the usual rich-get-richer poor-get-poorer caper.

In real or nominal terms?

Either, as a wholesale collapse in current dollar value term swill be highly unlikely (we have a Govt in power with fish'n'chip shop experience who're quite happy to print money and throw it at any problem, especially with an election coming up) and as wages sure ain't going up in a hurry for many, so houses will get more expensive in nominal terms.

What is the likely outcome of more money printing in an environment of stagnant production of goods and services?

They will decline as much as interest rates increase, where servicing is maintained at current levels. It's purely a numbers game, anything else is just trivia.

e.g. Calculated on 30 year mortgage:

- $800k mortgage @ 3% = $778 per week.

- $550k mortgage @ 6% = $760 per week.

30% drop in borrowing power. Maybe compensated slightly by wage inflation. But then what's a loss in sentiment worth?

Loss of sentiment is worth 13%

Inflation is worth 7%

Add it to your 30% drop in borrowing power and...

Badababoom! 50% drop in real terms.

Easy as falling off a log.

I will take the bet.

“This will be the year that it halves in value.”

At any time this year (2022) where the mean value of a NZ house is 50% of the peak from that year.

REINZ data from early next year to validate.

Yvil can adjudicate. $500 to a bonafide medical charity of the winners choice. Donation made in winner’s name. Proof of payment sent to the Editor.

Accept the bet?

Clarifying the terms of the bet:

1) the drop is in real terms, not nominal.

2) the fall is over the next 12 calendar months.

3) I'm not betting you, or anyone else $500. Internet bets for money are a fool's game.

Also, to be clear, we are talking about an older house in Papakura, that has been a rental for many years. Sounds like it had a bit of work done in 2007, and has been left to rot in the rental pool since then. Just the kind of place that is hard, or downright impossible, to sell once the magical liquidity well runs dry. To compare values (and catastrophic price drops) you really need to do a like-for-like analysis.

Cheers

Crickets 🦗🦗🦗.

Looks like cheetah dosen't want to take the bet.

There are a ton of manky, run down old rentals that have been held for many years by the mature generation.

They have been cash cows, and a great source of pride. "Look at how wise we are, with our rentals that keep doubling in value."

Well now that the magical, wonderous, fairy tale liquidity tap has been turned off, we will start seeing these dilapidated old rentals, with their dated kitchens and old carpets, tired paint and leaky (rotten underfloor) bathrooms in a new light.

Nobody will want them. Yields are far too low. FHBs won't have enough borrowing power to do them up, and house flippers will be going the way of the dodo.

So, yeah, I pick 50% falls for those old ex-rental wrecks in 12 months. Take the bet or leave it, Cheetah.

Aha. Now it is a specific house not the NZ market in general. Groan silently….

Do you see the irony of offering a gambling bet on the outcome of a highly speculative housing market that will be determined by people who have gambled with debt?

If one person wins, many FHB's who purchased last year may well be ruined financial (potentially for their working lives).

If the other wins, poor FHB's who can't afford to buy, will likely be in an even worse position.

Either way, your $500 gain or loss, might be compared with $500,000 gains or losses for FHB's either in, or trying to get into the market.

In real terms or nominal terms?

.

nzb - this is the kind of ignorance I cannot understand:

"and it is likely to continue to do so, well into the future."

Where t f is the rationale for that?

Astounding.

Historical data, of what has occurred to date generally for all areas of NZ. However, buying in the areas that have the infrastructure, good schools, shops and businesses...basically area's that are likely to have high growth. Ensuring you get a discount at purchase, also helps. When I bought in 2007 in Papakura, I had already attended multiple property investor seminars and 3-day events, spending $300-400 and the time to take on board the learning. RE agents told me that I would not be able to buy any property in Papakura under 300k, however, we searched and searched and eventually got a do-up on a good street, for 120k spending 30k to do it up. So a property doubling every 10 years using the initial investment of 150k in 2007, 300k 2017, 600k 2027 and 1.2M in 2037 is very much doable. By no means am I a full-on property investor, far from it. But it has helped me and my family to trade up family homes as I moved locations within NZ for employment. I hope that respectfully answers your question.

For some perspective of what you're experiencing, watch a youtube documentary of the roaring twenties and the great depression.

It's been a great welfare scheme, hasn't it.

My New Year's prediction for overall national NZ house prices was a rise of 9 per cent this year. This was not a prediction made on the basis of what looked likely to happen at the time but a feeling I had. Right now all the graphs are showing us heading toward quite a large decrease in house prices for the year so logic is winning over gut instinct.

For any kind of house price rise this year to happen the dip in the middle of the year will have to be savage enough and fast enough for the US Fed to reverse it's rate rises and go back the other way within 6 months. Also our Reserve Bank will have to follow suit and the NZ govt will have to make major changes to the CCCFA. The Americans can and will do anything in the blink of an eye so the first part is possible, the same is true of Adrian Orr, but the likelihood of the Labour govt being able to get out of it's own way and do what is necessary to save it's own election prospects is remote.

I dream of them functioning as well. Recent calls asking to get involved in chasing skilled workers was responded to with "ring back in three-six months" or "use the old system". We did try that but it requires humans at their end to do their job, which they did not. So sorry to say any dream of the Immigration Dept saving us is actually more a nightmare of Govt Dept incompetence.

#dontbetthefarm

NZ Billy - The Kiwi $ is falling rapidly so imported inflation will arrive shortly, historically interest rates need to be 2% more than inflation to tame inflation which is already close to 7% - so double digit interest may be a possibility, Orr could do too little too late as usual and kick the can down the road and then perhaps we will see 15% and a 40-50% asset crash. The market is usually right in fact it is always right and currently it is losing confidence in NZ as are voters with open eyes and and IQ above 100.

I don't think there is a REAL appetite for RBNZ or the Government (red or blue) to make those hard economic decisions, either in NZ or with our Five eyes partner countries. Going hard to reign in spending that directly addresses inflation will not occur, instead, the overall negative world economy may do that itself. Instead, the narrative is 'we are spending to sort out infrastructure issues that have not been addressed over generations', and we will do whatever it takes to keep the economy going (not necessarily high GDP growth, rather neutral-low/medium levels). Labour today, has made a politically astute move with its "Opening NZ to the world", even stating that the settings pose some form of 'competitive' advantage over its partner countries. I suspect this will just one of the many lollies that will continue to the next election - at the same time National has already stated that it will wind back changes that support Property Investors and state that they are better at keeping the economic engine of NZ humming. NZ continues to be an attractive place to live, bring your family and start a new beginning - a global niche for others of the world. I did not hear anything with number restrictions with how many can come in, however, I suspect that the high bar of wage limit (just under $28 hr) and control measures embedded in the design with 'accredited employers', a progressive model that allows some industries to come in under the wage-setting with a year or 2 to meet the target - will help control the flow of workers at various low, middle and high value needed in NZ. Again, political parties and the government are showing their hand, of which the NZ economy is still strong (2 pair Aces high). The war will one day stop, supply and building materials in the logistic chain return to some form of normal (but stronger after Covid), technology enhancements continue, and within the NZ economy the māori economy is rising.

Well the Reserve Bank seemed pretty confident they could engineer a soft landing when they let inflation run away for a year.

Also no economist seems to have a good handle on the New Zealand economy, their estimates have been widely out generally and so not very useful.

Sqishy - I doubt the RBNZ with help from Robberson could engineer a fire if they had a cu metre of paper and 20 litres of diesel plus two boxes of matches.

Be Kind. At least shout them a flamethrower....

Those dips are looking generous, watch this space..

I am getting a bit sick of seeing economists lazily blaming the price of labour for price increases - this speaks to their bias rather than the facts, and it makes it easy to push 'solutions' that basically involve putting people out of work and stopping wages rising enough for people to afford to pay their bills.

What is happening is that increasing prices are putting pressure on wages - NOT the other way round. People need higher wages because the prices they are paying in the shops, the rent they are paying their landlord, and the amount of money they are paying on their mortgages is going up. Employers are going to find it hard to say no to some wage increases when every other news story is about the 'cost of living crisis'.

The solution here is not to throw the country into recession as we try and stop everybody buying the things they need - as if this will somehow restrain Putin's aggression, or stop Saudi and US oil producers holding back supply to cash in. The answer is addressing shortages of productive capacity where we can, having a hard word with the onshore companies that are achieving record levels of profits ($200m per day at the last count), and buffering the public from offshore-driven supply shocks where we can (e.g. half price public transport, temporary duty cuts, etc).

Makes you laugh when Luxon says he wants the country to be 'aspirational' and raise peoples incomes...except if they are on the minimum wage and wants to open immigration to allow industry to hire cheap foreign labour.

Makes me laugh even harder at people who float this given that's literally what the Labour government did today. Got any more bangers?

Look at the minimum wage increase,lol...

And he wants to revert to making working Kiwis pay all the taxes while letting property investors freeload again.

Not exactly aspirational.

Do you think it is possible to live in a world without recessions and if so how?

Recessions are not inevitable. Firstly, when I say recession, I am not talking about how ever many quarters of GDP going down. I mean a slowdown in the real economy that is actually hurting the population. Two things that would help off the top:

Reduce the over-financialisation of the economy. The current approach creates an incredibly volatile and boom and bust economy - e.g. we have algorithms bidding up the price of wheat because their search engines are finding negative sentiment stories about Russia and Ukraine (wheat production is actually pretty stable!) We have suppliers hedging against future price increases, which is pushing up future prices and the cost of hedging, meanwhile those taking the other side of the hedging bet are pushing up the odds, and then parceling up their bets into tradable bundles - and so it goes on and on. We have got to the point where there are so many finance sector parasites and instruments weighing on the trade of real commodities, that the slightest stumble in the real world turns into a catastrophic spin as positions unwind. We need to put back in the controls that existed pre-1990 and limit the use of derivatives and bets on bets on bets etc. We also need to consider (as Keynes said) the use of strategic reserves for key global commodities to smooth prices during times of turbulence.

The use of a bufferstock of unemployed people to control inflation is cruel and ineffective. We need automatic stablisers that are tailored to the things that actually trigger recessions - e.g. job creation and fiscalstimulus schemes that can swing in as demand in the economy drops and unemployment rises, and fade out as things pick back up again and people return to private sector employment; mortgage interest rate premiums and LTV ratios that ramp up as risks in the housing market starts to bubble; and, discounted credit to support increases in productive capacity as the economy heats or we try and maintain the trade balance we need to protect us from currency swings.

I could go on!

I generally agree with almost everything you say Jfoe!

My only comment would be about considering how the status quo is hurting large parts of the population already - by the steps taken to avoid recession (which you point out..)

But to keep the status quo going, it is going to have even more unintended consequences....and create even more misery for large parts of society, and create even more financial and social instability. And ultimately any economy that has started QE is in the final throws of its expansion and glory days. There have been no exceptions, right back to the Roman Empire until now.

I'm more an eat your frogs in the morning type of guy when thinking of recessions. But we instead have can kicking leadership across the western world. They've been making the frog fatter and less desirable for consumption by the day..... instead of eating the frog, we've been feeding it. And perhaps so much so, that it might now try to eat us, instead of us eating it. (Or are we at that point already?)

https://th.bing.com/th/id/R.5706e183c2fbab11e97218f3c7f6f8ec?rik=WxtaOU…

Jfoe, are you actually Bill Mitchell? You are a scholar, sir.

"The answer is addressing shortages of productive capacity where we can, having a hard word with the onshore companies that are achieving record levels of profits"

In the same fashion that we addressed debt speculators and their excess profits as they loaded up with credit using ever lower mortgages rates, implemented as the result of imported deflation from cheap foreign goods (and some services)?

You realise I agree with you right? Of course, we should have taken action to tackle speculators, company share buybacks etc. But, just because we failed to take action to tackle the consequences of cheap credit, doesn't mean that we should let the rising cost of credit wreak havoc on working people who are already struggling.

I think we do agree with one another (see post above). My only deviation would be noting that rising the cost of credit might be the only thing that saves working people who are already struggling (whom haven't taken on reckless levels of debt). Either inflation chews up your income in consumption costs (unless we get out of the severely negative interest rate environment we are in), or interest rates chew up your income mortgage costs while the cost of consumer items drops as we return to a normal real interest rate environment.

Which frog do you chose to eat? (and you have to chose one....)

I have been of the view for more than 18 months that there can be no soft landing. But the hardness within the available options has been increasing.

KeithW

https://ourfiniteworld.com/2022/01/18/2022-energy-limits-are-likely-to-…

"Politicians would like us to believe that we live in a world of everlasting economic growth and that the only thing we should fear is climate change. They base their analyses on models by economists who seem to think that an “invisible hand” will fix all problems. The economy can always grow; enough fossil fuels and other resources will always be available. Governments seem to be able to print money; somehow, this money will be transformed into physical goods and services. With these assumptions, the only problems are distant ones that central banks and carbon taxes can handle."

Pigeons...home...roost...

Amazing really that mainstream economists still dismiss the work of the likes of Vaclav Smil, and any discussion of degrowth. It seems it may be just too difficult for them to process.

possibly not exactly the right place for the report this week- but no major "housing article" on interest today so this place will do.

Hutt Valley Market Update Week beginning 9th May

The number of houses for sale is continuing to trend downwards a large number of new builds came off the market this week.

Unfortunately, I can’t tell just yet if this is because they sold, their trade me ad expired or the development has been pulled – 8 are from the same development and were all withdrawn on the same day so I am tempted to think that the development in this case has been pulled. The development in question discounted each townhouse by 20K prior to withdrawing them from the market

Current Market Listings

628 houses on the market- down 18 on last week.

There were a large amount of houses withdrawn from the market last week unsold. There are a lower number of listings this week (Consistent for this time of the year) combined with withdrawals and what looks like a consistent number of sales appears to be the key reasons for the decline in the number of houses.

Based on the REINZ data which showed that 96 sold in Feb and 104 sold in March giving an average sale of 25 houses per week– 628 houses means there is 25 weeks stock on the market.

House Price Reductions

306 houses have a listed price

50% of the houses listed with a price have reduced their price since listing

The average markdown has risen this week from 83.5K to 84K.

Of those that have listed prices (pool 306) -30 have reduced their prices by 100K (last week this was 32 properties – a number of properties where the discount has been >100K have either been removed from the market or sold)

8 have reduced their prices by over 200K and 2 have reduced their prices by 300K with the biggest reduction been 350K (a total 20% reduction)

The data continues to show the majority of houses listed are under 900K. The Median house price for all 648 listings is now 830K. (Down 19K on last week and the lowest Median YTD – previous low was $839K)

The latest QV valuations (valuations by QV which are updated every month and give an approximation of a houses value)have dropped $130K since Jan for the Hutt.

In April the QV valuation had dropped 80K – approximately 20K a month since the start of the year but this escalated in April – dropping 50K in one month.

Houses sold vs houses removed

My records show 142 houses listed with a Price have sold YTD (up 6 from last week).

I have records of a further 122 houses (up 15 from last week) that have been removed from the market unsold YTD.

16 of those houses removed from the market have been listed on the rental market

The total number of houses removed from the market in the last 3 weeks is 46 (this compares to about 5 houses delisting a week over the previous 14 weeks).

The increase in the number of houses delisting is to be expected in Wellington where owners with cold damp houses try to avoid selling over Winter when this problem becomes quite noticeable. I am expecting more houses that listed in the peak of summer will be considering coming off the market for winter and relisting in Spring (for those sellers who can afford to).

Length of time on the Market

Given how slow the market now is – I’m adding a new Length of time – which is houses that have been on the market for over 90 days- effectively these houses listed in 2021 and Jan 2022 which remain unsold.

- 472 of the houses have been on the market for over 30 days - 75% (last week it was 463)

- 286 of the houses have been on the market for over 60 days - 46% (last week it was 292)

- 166 of the houses have been on the market for over 90 days – 27% (last week was 181)

Whilst I haven’t seen the latest time to sell numbers for the hutt valley – ¾ of the market has been on for over 30 days and with half the market on for over 60 days – you would estimate average sell time is at least 50-60 days at the moment.

For those thinking of getting a bridging loan when buying you would need to be calculating the costs of maintaining the loan for at least 3 months – 60 days to get the sale and then a further 30 days to settlement.

I am aware that a number of houses with price by negotiation are actually under offer but subject to sale of another property – in some cases there has been a chain effect occurring where there are now several houses all in the chain subject to sale.

Rental Market

Meanwhile the rental market has 194 properties for rent (down 8 on last week), and up 72 on this time last year – when just 122 houses were for rent.

Average rental price reduction is $53 a week (up $3 on last week) and 42% have dropped their prices since listing.

As noted last week I have also been noting how many properties are listed for rent over $650 a week.

At the moment the percentage of properties listed at $650 fell this week to 40% - last week it was 43%. This is the lowest percentage of houses over $650 since the week of the 27th Sept 2021 when 38% houses listed were over $650.

Very informative. Worthy of being articles rather than just added to the comments.

Maybe discuss with David?

KeithW

Agreed. It's a microcosm of market action. Very focused on analysis.

Lots of great info there. If you used tables and charts it would make it more powerful particularly if you also show the history (if you keep it). But realise difficult to do in the comments section?

Yes, I'm with others above. I feel the Hutt is a good bellwether. Highly diverse property market and easy distance/good PT to a main center.

Your data is so rich it deserves an article on its own.

Glad to hear rental prices are heading downwards - that relief is certainly needed across many in this community..

the part of the headline that reads "house price falls to get worse.." is of course dependant on your situation.

Another option would be "House price falls to continue.." which would take out the emotive language making it sound as if it is a bad thing, given that lower house prices long term would be better for many if not nearly everybody in the long term.

There is not anywhere as many lines in the press about peoples Kiwisaver investments going down.

I feel for folk who bought recently to put a roof over there heads...the other "investor/speculators"...well you pays ya money,ya takes ya chances,some investments go up,some down,welcome to reality.

An OCR peak at 3.5% is very optimistic. The peak will be at around 4%, and it will stay there for a significant amount of time. Swaps are already indicating an OCR peak closer to 4% than 3.5%. Mortgage rates will go over the 7% threshold. As I fully expected (and I was not the only one for sure) the RBNZ has now to pick up the pieces of their stupidly shortsighted ultraloose monetary policy of recent times. The Government's wasteful spending does not help either. Unfortunately will will have to get through a recession induced by the necessary and unavoidable big correction to the housing Ponzi - the hope is that such correction does not turn into a potentially catastrophic rout.

Fortunr,

Do you think a recession will force the OCR to a lower ceiling than this. The reversal of economic fortunes since the RBNZ started raising the OCR has been breath-takingly fast and I can't see the wider economy being resilient enough to manage to stagger into 2023 intact.

To much debt, access to debt being restricted, interest rates repricing long debt positions, NZD falling fast causing imported goods to rise, labor shortage, inflation roaring, Russia running amok, big cracks in China, China property defaults, ..... and the big one, the sacred housing market in NZ has turned its toes up and looks to be entering free fall just like the US stock market. A big difference between those options is the US stock market has the advantage of liquidity, and visibility. I can reprice itself in the click of some sell transactions, and is visible for all to see instantly.

Debt based speculation is great while debt costs almost nothing. Once the tide turns, can you survive the weight of that burden without drowning.

If a average wage couple have no chance of buying a home who will only top 5% earners could buy in Auckland , this needs to be fix quickly or young couples will just leave country and all you will have is a lot of retired people selling houses to each other.

Average wage couple? We're a way tf above average earners and have the benefit of some rental income due to recent family movements and have a healthy deposit, and we STILL can't 'afford' anything reasonable without hooking both of ourselves up to another lifetime of servitude. We really have zero idea how others are coping, or where tf those that were willing to pay double to triple what we could ever reasonably offer got their money. It has become so unhinged that I'd suggest it's only the financially deranged and desperate or newly minted lotto winners / 1%-ers that can actually 'afford' commensurate houses at the levels they are now.

Planting my victory vegetable garden this weekend

Its got to be a rout. The whole asset play is well overextended. While the fabulous Jacinda & co saved the economy from Covid collapse the rest of the west did the same. The run up was great, the decline will be hellish.

Topliss says house prices going down will be "worse". I say thats "better"

The Labour market is tight. Best news I have heard in a while.

Agreed,I repeat my post from above...

the part of the headline that reads "house price falls to get worse.." is of course dependant on your situation.

Another option would be "House price falls to continue.." which would take out the emotive language making it sound as if it is a bad thing, given that lower house prices long term would be better for many if not nearly everybody in the long term.

There is not anywhere as many lines in the press about peoples Kiwisaver investments going down.

I feel for folk who bought recently to put a roof over there heads...the other "investor/speculators"...well you pays ya money,ya takes ya chances,some investments go up,some down,welcome to reality.

My reasonably priced yacht looks to be on the not to distant horizon.

Not a single word on the limits to growth within a finite system. Do economists even understand the concept?

We just have to be more productive 🙄

There is plenty of room to become "more productive", however requires working smarter not harder. One of our primary exports is in the dairy industry which is a considerably unproductive use of land (~1 cow per acre rule of thumb) and resources (thinking on the environmental offset side). To become more productive we need to find ways of matching those exports within other industries while trying to shake off the notion that we're the worlds clean green pasture, because we really aren't anymore.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.