Here are the key things you need to know before you leave work today (or if you already work from home, before you shutdown your laptop).

MORTGAGE RATE CHANGES

ANZ launched a "Good Energy home loan" at 1% fixed for 3 years to a maximum of $80,000. They say there is no limit to what they will lend under this offer program, and no end date for the offer has been announced. BNZ now offers a 1% cash-back to a maximum of $20,000 (at the max. that would be a $2 mln loan!). See and compare all non-rate incentives here. The Cooperative Bank, Kookmin Bank, and TSB all raised some fixed home loan rates.

TERM DEPOSIT RATE CHANGES

Kookmin Bank raised term deposit rates today.

VERY SLIM PICKINGS

Dominant Auckland real estate agency Barfoot & Thompson's June sales were at a 12 year low for a June, with the average price down by -$120,000 from the December peak. Barfoots sold just 684 properties in the month. They have 80 offices and "over 1,600 residential, lifestyle, rural, and commercial salespeople".

FMA 2, DU VAL 0

In October 2021 the FMA directed Du Val to remove advertising materials likely to mislead or deceive investors, considering they contravened ‘fair dealing’¹ provisions in the Financial Markets Conduct (FMC) Act. The FMA said the statements created the impression investing in financial products connected to property development was low risk when, in fact, property development, including associated finance, is inherently risky. The statements also claimed there were “no fees”, despite Du Val retaining any profit on projects above the return to investors. Du Val’s offers used the wholesale investor exclusion in the FMC Act. Du Val's court appeal of the FMA position has now failed on all counts.

SLIDING

Update: June vehicle registrations slid somewhat. There were 12,049 registrations of new vehicles for the month of June showing the market is weakening in the face of raising costs of living, high fuel prices, continued vehicle supply constraints and a weakening overall economy. Of those, 9563 were cars. more than -7% fewer than in June 2021.

SEVEN PERCENT FUNDING?

ANZ perpetual preference share offer of $250 mln (and unlimited oversubscriptions) is now open. They say it will be priced at the 6 year swap rate on July 7, plus an indicative margin of 3.25% to 3.45% pa. The six year swap rate was 3.92% the last time we looked, but it is retreating. In any event it will probably be funds that will cost them more than 7% pa for the next six years at least (and is quite the contrast to their 1% "Good Energy home loan offer". Borrow at 7%, lend at 1% ?!! Just a 'fun' contrast - obviously ANZ's treasurer knows what they are doing for the overall mix of cost of funds.)

NZX50 UPDATES

We have updated a number of NZX50 company profiles to incorporate their recent March 2022 annual report changes. Updated are Infratil, Ryman Healthcare, Goodman Property Trust, Kiwi Property, Pushpay Holdings, Argosy Property, Stride Property and Oceania Healthcare. Last week the overall capitalisation of the NZX50 dipped by -$665 mln (-0.6%) to %109.9 bln. F&P Healthcare (FPH, #1) fell -0.9%, Pushpay (PPH, #25) fell -7.6%, but Air NZ (AIR, #38) was up +8.3% to bookend the changes.

CASINOS CONDUCT & CULTURE CRISIS

SkyCity’s Adelaide casino will be scrutinised via an independent review as part of a widening Australian crackdown on the gambling industry.

INSURANCE INFLATION FROM CLIMATE CHANGE

One of Australia's largest insurers, Suncorp, says costs are rising from 'the material hardening of the global reinsurance market following elevated natural hazard activity in recent years.’. Their focus might be Australia, but Kiwi premium payers probably won't be forgotten in insurance repricing for rising natural hazard claims.

NO RECESSION FEAR IN AUSTRALIA

And staying in Australia, there was a big and unexpected jump in the number of residential building consents issued in May, up almost +10% from April when a -2% fall was expected. It is unclear how analysts could get that so wrong. Also rising is bank mortgage lending, up more than +2% in May from April, when a -2% fall was expected.

SWAP RATES DROP HARD

We don't have today's closing swap rates yet but they are falling sharply again today on top of last weeks retreat. Expect -10 bps falls just today alone. The 90 day bank bill rate slipped -2 bps to 2.83% today. The Australian 10 year bond yield is now at 3.49% and up +2 bps from this morning. The China 10 year bond rate is now at 2.87% and +3 bps higher today. And the NZ Government 10 year bond rate is now at 3.63%, down -8 bps from this morning and still lower than the earlier RBNZ fix for this bond which was down -12 bps to 3.67%. The UST 10 year is now at 2.89% and down -9 bps from this time Saturday, but little-changed today.

EQUITY PRICES RISE

The NZX50 is up +0.8% in last trade today. The ASX200 is up +1.0% in afternoon trade. Tokyo has opened up +0.6% today. Hong Kong has opened down -0.7%. Shanghai has opened flat.

GOLD DOWN

In early Asian trade, gold is down -US$3 from this morning at US$1810/oz.

NZD HOLDS

The Kiwi dollar is little-changed if slightly softer from this time this morning at 62 USc. Against the AUD we have firmed marginally to 91.2 AUc. Against the euro we are little-changed at 59.5 euro cents. That means our TWI-5 is now just over 70.3.

BITCOIN STABLE

Bitcoin is now at US$19,164 and virtually unchanged from where we opened this morning. Volatility over the past 24 hours has been moderate at +/-2.2%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep ahead of upcoming events by following our Economic Calendar here ».

30 Comments

Another 10 bps off the swaps will have almost completely erased the huge jump 3 weeks ago. What a strange market right now. I wonder if retail rates will ease back as well -- it didn't take the banks long to push them up on the back of that big jump in swaps.

Another 50bps call from the RBNZ soon might put the brakes on....I guess we will see.

The next 50 is baked it. Question is what happens after that.

All eyes on the 5 and 10 year swap rates.

7%+ rates are guaranteed... oh wait hold up...

1-2 year swap appears to be at an inflection point....in 2010 and 2014 they peaked around where we are...but have never gone higher in a post-GFC world.

Be interesting to see if rates manage to break out above this point, perhaps signaling the start of a new era...or whether we are in for more of the same.

I've been waiting for something to break but we seem be just bouncing along tickety boo!

I think the market is pricing in a lower OCR - nothing else makes sense with the 1 year swap rate down 50 basis from peak and 2 year down 0.75% from peak.

Housing Market fall......is about to begun and here vested biased are trying to say that worst is over.

https://fortune.com/2022/07/03/redfin-housing-market-predictions-2022/

This might out-DGM your link on the U.S. housing "bubble." From the venerable Wolf Richter:

For the last two years, the story was that there’s no inventory for sale, that there was a housing shortage, and that’s why prices were skyrocketing. Then there were other folks like me that pointed out over and over again that people weren’t putting their old homes on the market after they’d bought a new home, and that these people now owned two or three homes and that they were going to ride up the hottest real estate market ever where prices soared 20% or 30% or more per year, and then they’d sell those vacant homes which no one had ever counted as vacant.

https://wolfstreet.com/2022/07/01/housing-bubble-getting-ready-to-pop-p…

Good link it’s worth reading

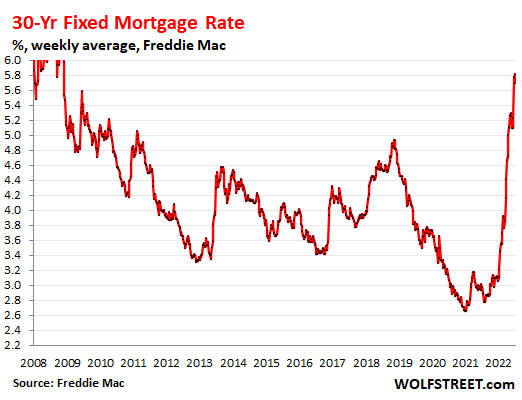

The 30 year fixed mortgage rate chart in the article is impressive. Back to GFC levels in very quick time.

https://wolfstreet.com/wp-content/uploads/2022/07/US-mortgage-rate-2022…

{kind=link}

All Wolfstreet stuff is well worth reading, unlike that dreadful Redfin link. That economist just spouted off the opinions his bosses have told him to have.

I get the Wolf on email regular, interesting stuff.

Markets are pricing less fed rate increases due to their rising expectations of a US Recession ….. Not necessarily a great result either …..

Yes, recessions, here, there and almost everywhere

Re- Aussie Residential construction. It rose 10% in ‘seasonally adjusted’(?) terms, but fell in real terms.

it seemed there was a burst of apartment approvals which lifted the numbers. These numbers can be a bit volatile. And as per NZ, the numbers lag - developers who might have been in the system for months seeking approval will typically continue through to approval, even if the economic picture is bad, because they have sunk so much cost, the least they can do is get their piece of paper granting approval for little additional cost. Which even if they don’t build they might use to try and sell a property.

"SkyCity’s Adelaide casino will be scrutinised via an independent review as part of a widening Australian crackdown on the gambling industry"

Perhaps this review of the gambling industry should also include the crypto, share and property markets? (50% sarc)

Add in the Pokies, Greyhound and Horse Racing..

Possibly they will be reviewing the Sky City Casino's policy of accepting $10000 in cash for chips, having the participant lose $1000, then cash in his/her chips for a casino bank transfer, or cash with a casino receipt, which freshly laundered with a 10% casino commission, shows as casino winnings of $9000. Time honoured income producing method for casinos all round the world.

And maybe the largest speculative market of them all.. FOREX?

FX so easy long one side of the pair, short the other via another house.....

I like the odd flutter at the TAB but man I hate Casinos. just cesspools of human immorality

Are you sure you just didn’t go into a Propellor Property seminar by mistake?

take a staircase or txt ladder to .......

Haha

casinos, whore houses, Propeller Property seminars, lowest of the low

Just to add:

Talk it up Suncorp.

"When aggregated by season, there is no trend in normalised losses from weather-related perils; in other words, after we normalise for changes we know to have taken place, no residual signal remains to be explained by changes in the occurrence of extreme weather events, regardless of cause. In sum, the rising cost of natural disasters is being driven by where and how we chose to live and with more people living in vulnerable locations with more to lose, natural disasters remain an important problem irrespective of a warming climate."

Normalised insurance losses from Australian natural disasters

https://www.tandfonline.com/doi/full/10.1080/17477891.2019.1609406

"Prominent Southern Baptists and other evangelical Protestants, on the other hand, have issued statements that are strikingly similar to the talking points of secular climate skeptics, and have attempted to stamp out “green” efforts within their own ranks. An analysis of resolutions and campaigns by evangelicals over the past 40 years shows that anti-environmentalism within conservative Christianity stems from fears that “stewardship” of God’s creation is drifting toward neo-pagan nature worship, and from apocalyptic beliefs about “end times” that make it pointless to worry about global warming."

https://www.tandfonline.com/doi/full/10.1177/0096340215599789

It's all good then. Lower swaps off their peak. I would say it's your change to lock in a still affordable longer rate. Inflation will go stupid soon. Remember fuel started increasing only 3 months ago. Next quarter is probably having surprise jump. We looking at stagflation ahead, it's not not not going to be a soft landing. But I am not an economist. ANZ would like that house with solar system or that Tesla car.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.