By Andrew Cornell*

One of the key things banks do is borrow money for short periods of time and lend it out for long periods - maybe take deposits for three months and make home loans for 20 years. It is what is called ‘maturity transformation’ and when all goes well, it’s a profitable business.

That’s because short-term interest rates are normally much lower than long-term ones and banks profit on the spread. Hence the old bankers’ joke about the 3-6-3 rule: borrow money at 3 per cent, lend it at 6. Be on the golf course by 3pm.

Of course, plenty can go wrong. Loans can go bad. There can be a run on deposits, draining cash reserves. And today there is another issue: because inflation is so low and central banks are printing so much money, there is very little spread between short and long term rates.

It’s the negative 1-1-0 rule: borrow at less than nothing, lend for almost nothing. And no golf.

This Wonderland of negative interest rates is hitting bank profitability. Meanwhile, even though central banks are the ones driving rates negative in a bid to lift economic growth, those same banks are wary of unintended consequences, collateral damage and policy binds.

(Increasingly too, central bankers such as the US Federal Reserve’s Janet Yellen or the Reserve Bank of Australia’s Glenn Stevens are debating whether such low rates are even working as a basic stimulus.)

Restore health

During the savings and loans crisis in the US in the 80s in the United States, which saw massive insolvencies in the banking sector, regulators were able to use the interest rate spread to help restore health. They lent otherwise sound banks money at low rates, those banks were then able to place the money in other highly secure assets and rebuild their balance sheets on the spread profits.

Negative rates then are becoming a systemic challenge. As the global banking lobby, the Institute of International Finance (IIF) outlined in a recent paper, they hit bank and other financial institution earnings and valuations in a number of ways.

According to the IIF:

• Bank net interest margins are compressed pressuring income, leading to lower market valuations, which raises the cost of equity.

• Insurers face rising re-investment risk. For insurers with duration mismatches, low rates could impact their ability to generate the income needed to meet long-term liabilities.

• Pension funds face growing funding deficits as interest rates fall to very low levels. Ultimately, negative rates could render the whole concept of saving for retirement unworkable, potentially requiring some form of public policy assistance to retirees.

European Central Bank executive Benoît Cœuré addressed the dilemma in a recent speech.

“It has been suggested that at some point the level of rates can become low to the extent that the detrimental effects on the banking sector outweigh the benefits of lower rates,” he said.

That point is known as the “reversal rate” and at that point bank profitability will fall, reducing capital generation via retained earnings, which is “an important source of capital accumulation, and thereby eventually restricting lending”.

That is, at that point, low rates which are intended to boost investment would have the opposite effect.

There have been volumes written on whether money printing and zero or negative interest rates will actually work and Keynes’ famous description of “push on a string” comes to mind.

Last week, two public companies, Henkel and Sanofi, issued bonds at negative yields. In theory, they should now spend the money raised investing but there’s no indication they will. Meanwhile those who bought the bonds – guaranteeing they would cost themselves money – presumably assumed there’s no growth on the horizon and other options would cost even more.

Even in Australia, where the latest economic growth figures were promising and the official interest rate remains well (ish) above zero, the market is analysing the impact on bank profits.

Damage

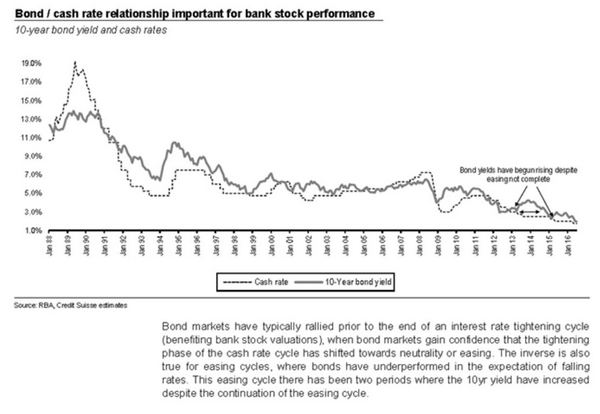

Credit Suisse’s Jarrod Martin produced a research note last week outlining the damage zero interest rates in Australia would do to bank profits. CS’s conclusion is zero rates would cut major bank earnings by 9 per cent.

“We see this easing cycle (in the official overnight cash rate) as being different from the past four - it has been sustained for a far greater period and looks to continue further; we believe that negative earnings impacts for banks become more pronounced with each incremental step towards the zero bound.”

So are negative interest rates doing more harm than good? Harm in the sense the aim – easier financing to generate investment – is being more than offset by the cost to banks rising to such an extent it crimps their ability to make that finance available.

The ECB’s Cœuré offers no answer: “While theoretically appealing, a precise estimate of the point where accommodative monetary policy becomes contractionary and/or an issue for financial stability is extremely challenging.”

As he says: “Low (and negative rates) have both a one-off short-term impact and more persistent effects on a bank’s profitability and capital. And bank capital matters for credit provision and for financial stability, as low bank capital means high leverage.”

Critical hit

Critically, Cœuré emphasises how interconnected modern financial systems, both nationally and globally, across markets and regulatory structures, are. It’s not a matter of whether something is good or bad for banks or the economy but rather how each measure of policy interacts with others.

“The exact magnitude of the effect of negative interest rates on aggregate bank profitability is uncertain, since it has to be put in the context of what would happen in the absence of monetary policy action,” he says.

Moreover, there are a range of second order impacts which could potentially create instability in the financial systems. Take the case of companies issuing negative rate bonds.

What that means is investors are prepared to accept lower and lower returns but risk has by no means declined by the same amount.

In chasing better returns, financiers too go further out on the risk curve. If rates do rise or economies continue to stumble, that could contribute to a bad credit cycle.

“Financial stability risks could also materialise outside of banks, through excessively inflated financial asset prices and if zero or negative rates encourage asset price volatility,” Cœuré says.

There is a body of research which suggests ‘bad’ risk taking, when the price (interest rate charged) does not reflect the risk is more prevalent when rates are low.

Australia’s new central bank governor, Philip Lowe, alluded to these challenges in his first speech as governor.

“Maturity transformation has become more expensive,” he said. “So too has providing market making services in some financial instruments, generating concerns about a lack of liquidity in bond markets.”

“More broadly, the cost of many forms of financial intermediation across banks' balance sheets has become more expensive. The promised benefit of this additional expense is that the system is now more stable. But we need to keep an eye on this trade-off, because a well-functioning system needs to be able to take risk at a reasonable price.”

While the populist argument is often ‘banks are too profitable’, the reality is banks are an essential component of economic recovery and even central bankers struggle with the right balance between shareholders, customers and taxpayers.

------------------------------

*Andrew Cornell is managing editor of ANZ's BlueNotes. This article first appeared on the BlueNotes website here, and is used with permission.

16 Comments

Are negative rates doing more harm than good ?

Is the Pope a Catholic ?

If you destroy/ devalue / discourage / disable / debilitate any one of the FOUR FACTORS OF PRODUCTION you are headed for big trouble .( the four being :- Land , Labour , Capital , Enterprise)

Just ask British trade Unions about what they did to labour rates that saw the demise of British industry

Or ask the Russian communists about what they did to the business / entreprenuer capitalist class

Or ask the Chinese communists about what they did to land ownership rights

Or ask Robert Mugabe about what he did to the value of his currency.

The unintended consequences of the Fed and ECB actions have not been felt yet

Things are starting to spin out of control. Kunstler:

The elites operate in their own twilight zone of ignorance, only at a loftier level, flying on wings of sheepskin. Submitted for your approval: Harvard wizard Kenneth Rogoff’s new book, The Curse of Cash. This is the latest salvo in the international campaign to herd all money into the control of central banks and central governments, supposedly to make central planning of the economy more effective — but really for the purpose of extending the fallacy that the mis-pricing of credit and collateral (that is, of everything) can save the current incarnation of crony capitalism, and more to the point, save the fortunes of the racketeers running it, along with the reputations of their intellectual errand boys. Henceforth, all “money” transactions would be traceable, allowing unprecedented power for authorities to regulate the lives of citizens.

Herding all the “money” onto central bank computers only allows for more three-card-monte maneuvers to conceal the bezzle. It would be much harder to hide the destruction of value in circulating paper currency. Eliminating currency as a medium of exchange can only lead to the repudiation of “money” — which will beat a quick path to the repudiation of all authority. And there is your recipe for really suicidal political disorder.

http://kunstler.com/clusterfuck-nation/signs-of-desperation/

Short answer: YES!!

Interest rates do harm, period.

Less harm than would be done without them, though.

About negative interest rates:

This month, once you have traversed the paragraph about golf balls, there is the observation that “US$11 trillion of negative yielding bonds are not assets – they are liabilities”.

Not only is this a memorable one-liner, it provides ample food for thought.

On the basis that “an asset is a resource with economic value that an individual, corporation or country owns or controls with the expectation that it will provide future benefit”, then Gross is correct.

Holding a bond bought on a negative nominal yield to redemption will crystalize a financial loss, not a profit: the value of the coupon payments will be outweighed by the capital loss on redemption.

Supposing that the purchasers of underwater bonds have their marbles intact, what are their possible motivations? I can think of four.

First, the investor is acting under regulatory coercion: he or she is obliged to hold a fixed income ‘asset’ that matches the length and type of their liability, or that fulfils the provisions of Solvency 2 or has a zero risk-weighting for Basel 3.

Second, there is corporate treasurer or family office custodian that cares not for the yield but places paramount value on the option value of high quality liquidity.

In other words, the utility of a short-dated government bond exceeds the carrying cost. Better to lose a small, but known, sum of money than to risk losing an unknown, and potentially larger amount.

Third, there is the speculator who hopes that the yield will fall further into negative territory and thus the bond price will rise in defiance of its destined plunge to par value.

A variant of the speculator is the foreign investor who is willing to hold negative yielding bonds if she thinks that the base currency is materially undervalued: the prospective exchange gain will exceed the nominal capital loss in the currency of issue.

Finally, there is the deflationist. Deflationists live in an upside-down world in which it makes sense to give up current capital in favour of a lesser amount of future capital because money in the future will be worth more than today’s money. So much more valuable will tomorrow’s money be in relation to today’s money that even a negative nominal yield serves as no deterrent.

So, there you have it.

Central bankers and academics may pontificate about the attractions of increasing the inflation target, but the prevalence of negative nominal yields is designed to appeal to deflationists who reckon that there is no chance of inflation returning even to the muted annual rate of 2%.

They invest in government bonds to express their belief in the failure of policy, not its success.

How long can the markets, or capitalism in general, continue to function with the distortions that negative interest rates bring?

low interest rates for long are deflationary.

So.. yes.

It creates bubbles and redirects investment towards speculative economy to run away from low returns of the productive economy.

Kenneth S. Rogoff asserts:

In principle, cutting interest rates below zero ought to stimulate consumption and investment in the same way as normal monetary policy, by encouraging borrowing. Unfortunately, the existence of cash gums up the works. If you are a saver, you will simply withdraw your funds, turning them into cash, rather than watch them shrink too rapidly. Enormous sums might be withdrawn to avoid these loses, which could make it difficult for banks to make loans—thus defeating the whole purpose of the policy.

Take cash away, however, or make the cost of hoarding high enough, and central banks would be free to drive rates as deep into negative territory as they needed in a severe recession. People could still hoard small bills, but the costs would likely be prohibitive for any realistic negative interest rate. If necessary, central banks could also slap temporary fees on any large withdrawals and deposits of paper currency.

Economists generally like the idea of adding negative interest rates to the tool kit of central banks. John Maynard Keynes weighed it quite seriously in his great work “The General Theory of Employment, Interest and Money” (1936). He was writing, however, in an era before electronic banking, so he saw it as a thoroughly impractical idea.

Not everyone likes negative rates. There is particularly strong resistance from the financial sector, which worries about the difficulty of passing negative rates on to small depositors. But these concerns can be significantly alleviated. Banks could be compensated for allowing zero-interest rate deposits of up to, say, $2,000 per citizen. Read more

James Grant's rebuttal:

The author does not forget to salt his text with words of caution. They are unconvincing. Mr. Rogoff is a true believer in the discretionary command of monetary matters by former tenured economics faculty—the Ph.D. standard, let’s call it. Never mind that, in post-crisis America, near 0% interest rates have failed to deliver the promised macroeconomic goods. Come the next crackup, Mr. Rogoff would double down—and down.

Curiosity is notable by its absence in these pages. How have we come to this radical pass? What is it about today’s monetary and banking arrangements that seems to impel us to more and more desperate policy gambits? The nature of modern central banking and the pseudoscience of modern monetary economics are themselves surely part of the problem.

Interest rates are prices. They impart information. They tell a business person whether or not to undertake a certain capital investment. They measure financial risk. They translate the value of future cash flows into present-day dollars. Manipulate those prices—as central banks the world over compulsively do—and you distort information, therefore perception and judgment.

The ultra-low rates of recent years have distorted judgment in a bullish fashion. True, they have not, at least in America, ignited a wave of capital investment—who needs it in a comatose economy? They have rather facilitated financial investment. They have inflated projected cash flows and anesthesized perceptions of risk (witness the rock-bottom yields attached to corporate junk bonds). In so doing, they have raised the present value of financial assets. Wall Street has enjoyed a wonderful bull market. Read more

Interest rates are prices. They impart information. They tell a business person whether or not to undertake a certain capital investment. They measure financial risk. They translate the value of future cash flows into present-day dollars. Manipulate those prices—as central banks the world over compulsively do—and you distort information, therefore perception and judgment.

Oh..so very true... also the dance of consumption vs savings ( deferred consumption) vs investment ....

Central Banks have created a contrived economic world...

Parts of the private sector have been deleveraging in USA

http://suddendebt.blogspot.co.nz/2016/09/total-usa-debt.html

I love it how there is this assumption that there is some control over interest rates, then a graph shows the firm downward trend over which there is clearly no control.

Perhaps if you aligned CPI/core inflation with it, it would give you more perspective?

"Ultimately, negative rates could render the whole concept of saving for retirement unworkable,.."

It is. Retirement is the ultimate reflection of an economy "wealthy" enough to generate enough surplus each year to pay a whole lot of people to sit round and do nothing and consume. It belongs to an era of cheap to produce Oil. It is easy to overlook that all that can be consumed each year is pretty much what the world economy has made and produced each year - concepts of debt and savings obscure this.

Negative rates on the other hand are a reflection that the system is on its last legs.

Last week, two public companies, Henkel and Sanofi, issued bonds at negative yields. In theory, they should now spend the money raised investing but there’s no indication they will. Meanwhile those who bought the bonds – guaranteeing they would cost themselves money – presumably assumed there’s no growth on the horizon and other options would cost even more.

Sorry that analysis is bunkum. It makes perfect sense to buy a security that is almost guaranteed to increase in value. They are expecting to be able to sell them to the ECB at a nice profit. The author presumably knows that but this is a press release for the poor banking sector.

negative interest rates is a lie, this is simply the destruction of capital...

As a British employer i found the greater expense to my business was the inflated cost of the property i operated it in. I sometimes wonder if capitalism couldn't operate without cheap labour , or is that a reflection on those who own it .

I see negative interest rates as unnecessary, they end up doing more harm than good , end up leading to the next crash .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.