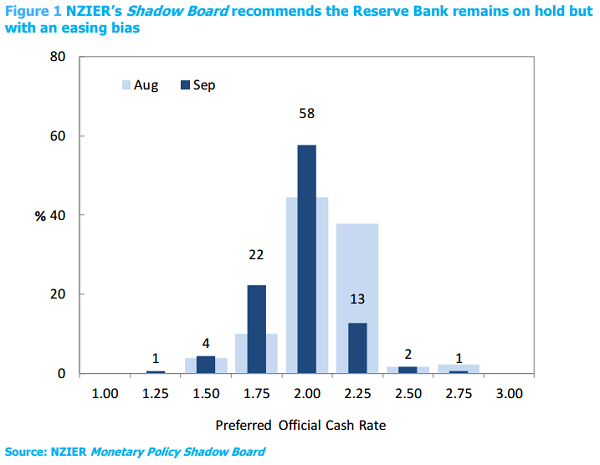

The New Zealand Institute of Economic Research’s (NZIER) Monetary Policy Shadow Board is increasingly open to an interest rate cut.

The nine business leaders, economists and academics on the Board are calling for the Reserve Bank (RBNZ) to keep the Official Cash Rate (OCR) on hold at 2% when it’s reviewed on Thursday. Yet their average recommended rate has fallen to 1.95%, from 2.08% last month.

“We are seeing solid momentum in the New Zealand economy, driven by strong domestic demand. But continued weak inflation and a strengthening New Zealand dollar are unhelpful for the RBNZ in achieving its 2% mid-point inflation target,” says NZIER Principal Economist Peter Wilson.

“The tension between weak inflation and rapid house price acceleration remains very taut, with the higher New Zealand dollar also adding to the RBNZ’s dilemma. Nonetheless, the RBNZ’s primary focus on inflation means further easing is likely.”

Five of the Board members have revised their preferred rate levels down from August, while three have increased theirs and two have kept theirs the same.

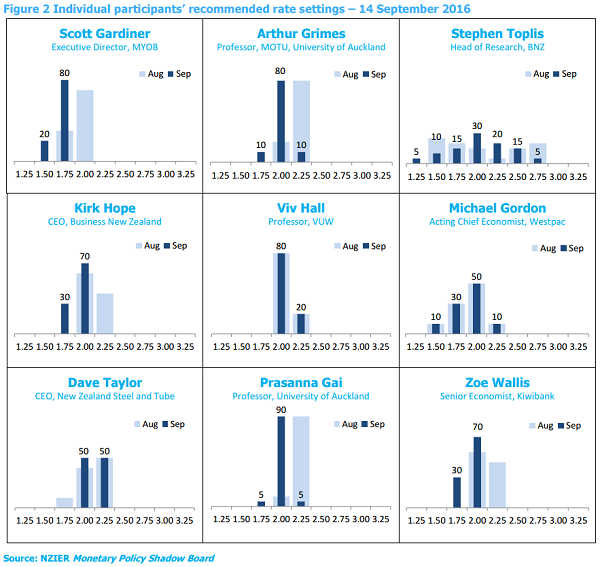

Kiwibank senior economist Zoe Wallis says: “Inflation remains conspicuous by its absence but growth is solid and expected to improve further. A higher NZD is creating further downward pressure on tradables inflation and risks sending inflation expectations lower still. A clear easing remains appropriate to combat weak inflation pressure, although there isn’t a rush to ease in September.”

MYOB executive director Scott Gardiner is on a similar page: “Whilst GDP figures will be expected to show good growth according to the latest MYOB Business Monitor many of regional businesses are still challenged by the effects of low commodity prices. So with cash low still the number one issue facing business, a reduction in rates would be welcome relief.”

On the contrary, BNZ head of research Stephen Toplis says: “We think there is a 70% chance that rates should be at or above current levels. That said we stress that these assumptions are based on the core premise that New Zealand can cope with sub-target inflation for an extended period. This is probably not the view that the RBNZ holds.”

MOTU professor Arthur Grimes would rather sit tight: “Inflation is low, house prices are rising fast, growth is robust, while international conditions vary from quite strong (US) to quite weak (Europe). Given these contrasting forces that are affecting current and future inflation, a wait-and-see approach to interest rate setting (with no bias for future changes) is warranted.”

Victoria University of Wellington professor Viv Hall agrees: “CPI inflation remains low and stable within a 0-3% range. Further OCR cuts are unlikely to assist rapid achievement of the 2% PTA mid-point target, are likely at best to have only a temporary downwards effect on the exchange rate, and could provide a further boost to house price inflation which would outweigh modest dampening effects from enhanced macroprudential measures. So, no recommendation for an OCR change.”

Westpac acting chief economist Michael Gordon has likewise maintained the same stance over the last month: “The latest developments - higher dairy prices and a higher NZ dollar - seem roughly balanced in their impact on the appropriate policy setting.”

The Board’s other members include Business New Zealand CEO Kirk Hope, New Zealand Steel and Tube CEO Dave Taylor, and University of Auckland professor Prasanna Gai.

51 Comments

Sorry I should have explained that a lot better. Using CPI (a highly flawed tool) tradables have been mostly deflationary and are countering non-tradable inflation. Combining the two we're ending up with 0.4% official inflation. I've oversimplified and written my comment poorly.

The CPI visulisation provides a clearer idea (and indicates there may be inflation approaching 1%).

http://www.stats.govt.nz/datavisualisation/cpi_ttnt.html

True. It's your assumption of the impact of this, though.

The real weighting of tradable inflation is coming from items that don't significantly increase with an increase in consumption potential.

Plus you also assume that the trend of the last 5 years is going to continue. Look at the trends prior to that - like in all economic growth phases, the tradables inflation was positive..

I am watching to see what happens with the trend. If tradable inflation goes up to zero the CPI would be close to the PTA target.

I think there's potential for the tradable inflation to become positive. It's just a matter of how long it's going to take, and what other hidden economic problems are going to cause chaos over the next two years.

Firstly.

Please write a massive article about it.

"The proof is in the pudding" is not adequate when you are making a blanket statement of the scope you did.

Secondly.

"At no point has a change in interest rate had a direct bearing on Inflation"

That statement is just blatantly incorrect.

Well if I write a big article, then why don't you also enlighten me with all the proof that my statement is blatantly incorrect. Inflation based economic models are clearly not working. If they were then with each decrease we would have seen a corresponding increase in inflation. We haven't.

As for the links - how about I just bullet point it in simple terms.

CPI, Inflation, and Growth.

1. CPI does not measure inflation, it measure an increase in prices.

2. Inflation is a measure of the purchasing power you have to buy something.

3. Value of the currency can impact purchasing power - but only on imported goods.

3. CPI does not count income, (or value of the NZD) so cannot determine purchasing power.

4. Inflation does not equal growth.

5. Growth is an increase in income allowing for people to buy more, the increased demand allows new businesses to start and meet the shortfall of supply.

6. CPI does not count housing costs (mortgages), the biggest single expenditure most households have.

Interest and Inflation.

1. Income is not linked to Interest rates.

2. Cost of goods is not linked to interest rates.

3. Currency can be linked to interest rate, but it is relative to all other currencies (and therefore other nations rates)

4. Interest rates do have an impact on the spending habits of mortgage owners, but not as much as the housing market itself. A $100k loan at 10% is much more manageable than the a $1mil loan at 2%

For the RBNZ to control inflation, they need to measure it correctly, then look at how they can change the variables linked in to that measurement. Interest rates themselves will not do anything.

"Inflation based economic models are clearly not working. If they were then with each decrease we would have seen a corresponding increase in inflation. We haven't."

Have you ever looked at graphs? Because it might be a revelation for you to look at NZ inflation trends since 1990.

CPI, Inflation, and Growth

1. Inflation's definition is the increase (decrease) in the price level of goods.

2. Inflation is a measure of purchasing power. It makes no sense to state this when it contradicts your first point that CPI is not inflation.

3. Correct.

4. Inflation equals nominal growth. But not real growth, if that was what you were alluding to.

5. Correct

6. Correct. CPI does not count capital costs.

Good work, you have a pretty good fundamental understanding. Baring a couple of errors.

However..

Interest and Inflation

1. Income is directly linked to interest rates under an inflation targeting regime and expectation based monetarism.

2. Cost of goods is directly linked to interest rates under inflation targeting. I don't know of any goods that increase in price when funding costs decrease..

3. Currency is always intrinsically linked to real interest rates - see the Fisher condition.

4. I don't know what you mean by this - since the mortgage values and propensity to service said mortgages are relative.

"For the RBNZ to control inflation, they need to measure it correctly, then look at how they can change the variables linked in to that measurement. Interest rates themselves will not do anything."

So your whole argument is on the basis that for the last 26 years the RBNZ key policy tools have had no impact on the economy?

Because, ahh, even without an advanced understanding of monetary economics or statistics/econometrics it is pretty plain to see that inflation rates have been relatively well aligned with RBNZ policy decisions over that time.

The rates are a reactive measure, Inflation rates trigger the rate changes. Not the other way around.

The stability of inflation over the past 26 years, therefore has nothing to do with OCR. When they have changed the OCR there has not been a corresponding change in inflation.

If a link did exist, we wouldn't require a whole RBNZ to decide when to change, it would be a straight mathematical formula. Inflation increases, rates decrease, and vice verse. The fact that we don't do that suggests very strongly that they are not linked.

I should have added to my last paragraph.

If a link did exist, we would not wait to see what CPI (inflation is doing) before changing a rate. We would know what the Inflation would be as a result of the rate change, and could therefore make proactive changes to inflation.

"The stability of inflation over the past 26 years, therefore has nothing to do with OCR. When they have changed the OCR there has not been a corresponding change in inflation."

So, you are saying that by coincidence inflation volatility has miraculously disappeared?

The long term inflation stability was completely due to what?

"If a link did exist, we wouldn't require a whole RBNZ to decide when to change, it would be a straight mathematical formula."

See the Taylor rule and related literature.

"So, you are saying that by coincidence inflation volatility has miraculously disappeared?"

When was all this so called volatility? In the 80s? Inflation ran rampant due to human behaviour. A massive crash happened - the crash scared everyone and changed behaviour. Inflation targeting was then introduced after the behavioural changes and has been falsely credited for fixing the original mess - ignorant of the change in behaviour.

The GFC changed peoples behaviour again. We are now in the first period (in NZ) where inflation has become volatile under inflation targeting, and it is clear interest rates are not able to control it. Therefore the theory is flawed.

"The long term inflation stability was completely due to what?"

Thinking Interest rates are a solve-all is just ridiculous. There are quite literally millions of things that impact inflation. As mentioned above, human behaviour is the single biggest factor, and this can be shaped by pretty much anything.

- The costs of raw resources, energy, and workers.

- The relative profit a business wishes to make.

- Global factors such as trade agreements, migration, and currency fluctuations.

- Individual choices

- Govt regulations

- Natural disasters

"See the Taylor rule and related literature."

The Taylor rule is designed to set interest rates, not inflation rates - it is a reactive formula that has inflation as an input (one of several). It therefore only proves that interest rates are correlated to Inflation. Not vice versa.

Reworking his formula to calculate inflation, leaves you still needing the other factors he describes. None of which are controlled by the interest rate.

"When was all this so called volatility? In the 80s? Inflation ran rampant due to human behaviour. A massive crash happened - the crash scared everyone and changed behaviour. Inflation targeting was then introduced after the behavioural changes and has been falsely credited for fixing the original mess - ignorant of the change in behaviour."

So, another coincidence. Perfectly timed with the introduction of expectation based monetary policy.

You believe in coincidence, a lot.

"The Taylor rule is designed to set interest rates, not inflation rates - it is a reactive formula that has inflation as an input (one of several). It therefore only proves that interest rates are correlated to Inflation. Not vice versa."

Do you want to re-read that statement?

"It therefore only proves that interest rates are correlated to Inflation. Not vice versa." You do understand what co-variation is, right?

Yes technically the rates are correlated, I used the wrong word. But I think with your technical knowledge you also understood the point I was making.

Now, rather than just trying to find fault with my points on technicalities, can you actually show any evidence as to how Interest Rates directly control inflation?

As I have said numerous times, I can not find any myself. Neither you, nor Taylor, nor any other Inflation targeting economist has proven that Inflation can be controlled by Interest rates. At best you have shown a correlation, which exists purely because that is the theory so both factors are used in the formula.

I could just as easily say Inflation is linked to my cat going to the vets. Using the formula My Cat going to vet= Rate of inflation *100. So if inflation is 3% I take my cat to the vet 3 times a year.

There is now a definitive link between them. Yet only one can determine the other.

Inflation determines interest rate. Not the other way around.

Almost all of it..!!!! (a little over dramatic to make my point )

Something is badly broken when Money supply grows at 8% compound and the CPI flatlines at 1%.

After all... Inflation targeting is a tool of "Monetary Policy".

In a Global world... CPI Inflation targeting , is myopic... in my view.

In the mid 2000s' we had 15% Money supply growth....

Money supply growth that is continually in excess of income growth ( GDP )... can be problematic over time.... and it takes us down the road of financial instability.

I'm assuming you think the inflation targeting policy framework is hunky-dory...and is still relevant in what is, and always has been, an evolving economic landscape..

this is just my view...

True, I will not disagree with your points.

Excessive credit growth without corresponding growth is worrying. This is only a problem in the case that we have central government policy, however.

Inflation targeting, not burdened by the incentives of central government to mismanage credit growth, is a sound regime. At least it is the best mooted and tested thus far.

To say it is myopic is not correct. One look at the DSGE and forecasting models that Central Banks these days implement would reverse this view.

I'll be the first to admit it isn't perfect, but the solution isn't to bag it based on little fundamental understanding of the dynamics of the theory. This is what bothers me the most. If the majority of commentators (I'm not saying you) simply read the Central Bank policy disclosures, discussion papers, etc, they would do themselves a significant favour.

Ok.. I hear what u are saying.... AND...

Central Banks, in their wisdom, have allowed money supply to be endogenous. ie.. money supply expands and contracts as a response to the demand for credit.

One of the, underlying , fundamental premises for having an edogenous Money supply is the idea that People are "rational", and make rational decisions.

This premise is WRONG... 40 yrs of watching mkts has shown me this.

It is a Central Banks job to manage credit growth...NOT ...Govts. ( both a function of prudential policy and price stability )...???

The excessive credit growth of the last 40 yrs has had a profound impact on the incredible growth the western world has had over the last 40yrs.... very good... but...

AND... The GFC has shown that there really are some shocking cracks in the paradigms that Central Banks

have, and which we see manifest in such things as the Inflation targeting policy framework.

Nothing wrong with bagging something.... if it is in the spirit of enquiry and asking questions..??? dont u think..??

We live in a very, very different economic world since that days when inflation targeting was first introduced.... would,nt u agree..??

I still say it is myopic... :)

I would agree with an endogeneity issue. However, only slight and not as simple as you outline.

The proposition that credit demand significantly drives overnight rate decisions has substantially more consequences than we see.

Sorry, I didn't mean the govt. controls credit growth. I meant that it doesn't adequately punish those who exploit it at unsustainable rates. i.e. those that are large enough don't realise their risks due to transfers/subsidies from central govt.

The proposition that credit demand significantly drives overnight rate decisions has substantially more consequences than we see.

Are u saying it does..?? ie.. overnight rate decisions driven by credit demand.

OR ..R u saying that it would be problematic to base OCR decisions on changes in credit demand...

( which , after all, is what the Central bank does, in a roundabout way, by using the CPI as a "proxy" and the OCR to influence the demand for credit )

"Central Banks, in their wisdom, have allowed money supply to be endogenous. ie.. money supply expands and contracts as a response to the demand for credit."

You said causation flows from demand for credit, not I..

Of course it would be problematic. Who is ever going to demand high financing costs if causation flowed that way?

Demand would perpetually be for low interest rates and inflation (or lack of, in current cases). Good way to cook an economy, I guess..

MOTU professor Arthur Grimes would rather sit tight: “Inflation is low, house prices are rising fast, growth is robust, while international conditions vary from quite strong (US) to quite weak (Europe). Given these contrasting forces that are affecting current and future inflation, a wait-and-see approach to interest rate setting (with no bias for future changes) is warranted.”

Hmmmm...

Goldman Sachs Group ’s gauge of U.S. financial conditions—a closely watched barometer that both reflects economic growth and offers a view of investor expectations of market trends—is at its tightest level since June. The financial-conditions index was at 100.27 Friday, up from 99.86 on Aug. 18. Tighter conditions reflect more difficulty borrowing.

“The market is calling the shots now, not so much the Fed,” said Don Ellenberger, head of multisector strategies at Federated Investors. “That is going to be the case until the Fed surprises the market and hikes [interest rates] even if stocks have sold off a little bit.”

The rising cost of borrowing dollars for brief periods is hitting financial institutions and other companies around the globe, a tightening of conditions that further limits already slim prospects that the Fed will raise interest rates at its meeting ending Wednesday. Read more

In August 2015, George Saravelos thought he had put his finger on one acute source of the financial stress that followed China's depreciation of the yuan.

China's sales of reserve assets to prop up its currency, he said, amounted to "quantitative tightening" — the exact opposite of the money-supply policies central bankers use to try to reflate asset prices in the wake of the financial crisis. Chinese sales of primarily U.S. dollar assets were draining global liquidity and dampening global risk appetite, according to the Deutsche Bank AG strategist, thereby contributing to the selloff in stocks and bonds.

Fast-forward to September 2016: at the start of a week of major central bank announcements that may force Beijing to take further action to defend its currency, the specter of Chinese quantitative tightening looms once again. Read more

It seems as if everything is once again coming to a head; markets seem to be on edge no matter how much is purported to be going right, waiting to find out if the distant but serious “overseas” commotion will remain an object for foreign consideration alone, or, as last year, confirm this summer’s apparently unshakable suspicions (that really aren’t so far away after all; see below) that nothing has truly changed. Read more

The market is calling the shots now, not so much the Fed,”

agree with this, case and point last week markets sold off as it looked like a rise might happen, suddenly Fed members come out with statements that now is not the time before lock down for meeting

they will hold and when minutes come out there will be wording to the effect of we don't feel right time to raise as events could force us to reverse track

Please post supporting evidence to refute the inferred claims residing within the contents of a recent comment?

Just look at the correlations of inflation rates to overnight rates, yourself. Sure, correlation <> causation, but consider the Taylor Rule, use a Fisher condition.

To say that money supply has had no impact on inflation in the past 8 years is completely wrong.

Don't simply call me out on the evidence, without also calling out the OP.

Everyone know the prices of almost everything is under downward pressure , with the exception of building materials and Auckland houses.

Just wait until the immigrants realise there is no point in paying over- the -odds for our smelly damp leaky hovels , and then we will all be in trouble .

when peoples biggest cost, housing, has wildly inflated out of reach I just yawn when I see CPI figures. Yes cut OCR because of 'deflation' then see what happens to house prices, and peoples' ability to afford to live here. Of course other prices fall because people can't afford other goods and services. This system is not working.

Its quite simple. True inflation is in house prices. But the rbnz and govt dont get that. Abandon inflation targets. The world has changed. Inflation is dead. Economic stability should be the number one rbnz target. Not outdated inflation policies that only worked when the world central banks weren't mass printing. How about a gold backed nzd? Or won't our American masters allow such a move?

The Reserve Bank's primary function, as defined by the Reserve Bank of New Zealand Act 1989 is to provide "stability in the general level of prices."

The majority of debt is created for mortgages for residential housing

Date - Agriculture - Business - Housing - Consumer

Jul 2016 60,502M 91,743M 223,052M 15,381M

http://www.rbnz.govt.nz/statistics/

Housing 57% of debt

Yet, housing has such a small weighting in CPI

http://www.stats.govt.nz/browse_for_stats/economic_indicators/CPI_infla…

Housing and household utilities group / Home ownership

(% weighting CPI)

Year of adjustment - Purchase of new housing - Actual rentals for housing

1993 7.02% 4.30%

1999 9.87% 6.16%

2002 8.48% 5.54%

2006 4.66% 6.87%

2008 5.51% 7.85%

2011 4.01% 8.78%

2014 4.20% 9.22%

Apparently the Reserve bank had concerns about House price inflation in Auckland in 1996:-

http://www.rmastudies.org.nz/documents/ResBankF.pdf

The Impact of the Resource Management Act on the "Housing and Construction" Components

of the Consumer Price Index Owen McShane August 1996

1.3 House Prices, the CPI, and Control of Inflation.

Changes in new house prices are a significant component of the Consumer Price Index (the CPI). New house prices directly effect the CPI but, as with all second hand goods the sale price of existing houses has no direct impact

2.5 Costs and Inflexibility

…

On the other hand, if a government decided to ban all new motor cars, the price of all cars would immediately begin to rise and would continue to rise even as the stock of motor cars grew older and less "valuable". Similarly, systematic restrictions on the supply of new housing can effect the price of all housing in the market. Hence, although new housing costs represent only some 2 percent of housing in the Auckland Region, a restriction in the supply of this 2 percent impacts on the price of the remaining 98 percent.

2.2 The NZIER Report A report by the New Zealand Institute of Economic Research points out that: …the housing market is complex: housing is both a consumption item and an investment good

Housing inflation makes up only 4.20% of the CPI basket, and as you can see it has had a falling effect on CPI over the last 20 years even though it has quadrupled in price over that period. Probably as it has become more expensive, less people can buy, less houses have been sold and it has fallen out of the basket. Even though housing will dominate people’s financial life. It is a problem with CPI that as housing has become more unaffordable due to it’s inflation, less of it has been bought, the less it’s effect on CPI

And with increased credit government revenues increase. But are we looking around the world and seeing what i see? Tightening credit, reducing real demand, and an underlying depressionary environment marked by central vank QE? Where does it end. QE to infinity? Bond market is the biggest bubble on the planet. And when risk is repriced, up go the interest rates. Not to mention the fact that most derivatives are derived from interest rates. So it collapses and we have nothing. Or the central banks print to infinity and buy every hard asset on the planet with their phoney money. 2 case studies.... china for tightening credit and Japan for QE to infinity. I saw an article today indicating china loan growth is falling rapidly. But thats ok, nz will be unaffected right? Nothing to see here folks, move along. Interest.co.nz could do better in covering some of these points because i know for a fact the mainstream media certainly won't.

Could someone explain to me-in very simple language please- just why we need another interest rate cut?

As I understand it, our economy is doing ok,with growth predicted to be over 3%, though I know that on a per capita basis, it will be significantly lower. That would not seem to be a signal for rate cuts. Does the housing market need the stimulus of a rate cut? I would not have thought so.

The RB seems to still believe that it must get inflation back to around 2%,but why and would(yet) another 0.25% cut help it to achieve that objective anyway?

To my simple mind, the world is in a deflationary era and one which is likely to last for many years. QE will not change that,nor will negative interest rates. At some point, I believe that there will be a hard landing for both the equity and property markets; a version of Schumpeter's 'creative destruction', but when and how hard the landing will be,I simply don't know.

As a long-term stockmarket investor(over 40 years) with an absolute focus on dividends,all I can do is gradually increase my cash weighting,reduce my average portfolio P/E and wait for the crash.

You are correct that QE & NIRP will not change the deflationary era. The RBNZ won't say this but the reason to reduce rates is because NZ is subsidising those with lower rates in these currency wars.

NZ's economic growth is almost entirely immigration; as you point out - NZ productivity is going backwards.

I wish nothing more for the free markets invisible hand & capitalism's creative destruction to return but unfortunately the world is firmly in the hands of the top 62 people who own > 50% of the world's wealth.

If I were you, I would increase your weighting in gold - the world's premier currency. There comes a point when holding cash is far more risky and we are at that stage. Take a look at Deutsche bank - derivative exposure higher than the entire world's GDP, HSBC not far behind - if one counterparty fails (remember the motivation of these bankers), the whole shooting match is over.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.