Cast your mind back to October 19, when New Zealanders waited with bated breath for New Zealand First Leader Winston Peters to get through his six-and-a-half-minute long speech, before finally announcing he’d decided to form a government with Labour.

Peters said too many people had come to view today’s capitalism “not as their friend, but as their foe”, and an “economic correction or slowdown” was looming.

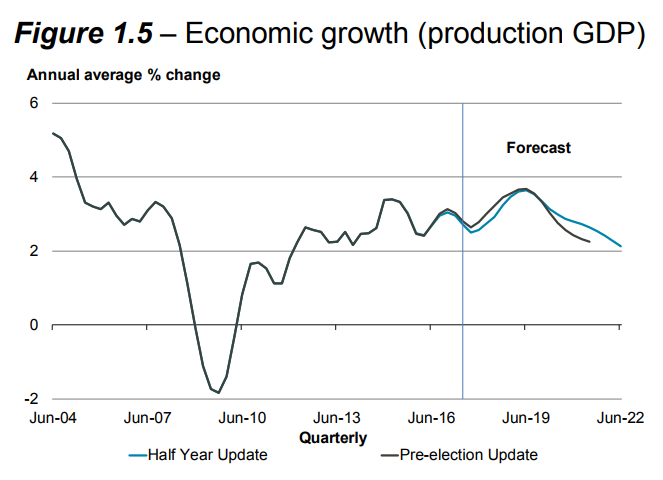

Fast forward almost two months, Treasury’s projections for where the economy’s going will make you think Peters was talking about a different New Zealand back in October.

Its Half Year Economic and Fiscal Update is upbeat and doesn’t differ as much as expected from its Pre-Election Fiscal Update released in August.

Treasury sees annual GDP growth averaging at 2.9% over the next five years – a slight improvement from its pre-election forecast.

Yes, the Labour-led Government is going to spend more – channelling all of the money the previous government set aside for tax cuts into its families and tertiary education packages.

And yes, its capital spending on KiwiBuild and resuming contributions to the New Zealand Superannuation Fund will see its net capital spend come close to hitting the $5 billion mark over five years.

But Treasury’s rosy outlook for economic growth, buoyed by population growth, low interest rates, increased government spending, a positive international outlook and higher terms of trade, gives it confidence Labour will be able to follow through on its promise to reduce debt from 21.8% of GDP to 20% of GDP by 2022.

Extra tax revenue only $6.6b over four years

Nonetheless, the Leader of the Opposition, Bill English, hasn’t missed the opportunity to have a go at the Government for the incongruency between Treasury’s projections and the comments made by Peters in October.

English, during question time in Parliament on Thursday, asked: “Has the Prime Minister asked the Deputy Prime Minister whether he believes these [Treasury’s] forecasts given his public statements that the economy is headed for a downturn, if not a crash?”

Answering the question on behalf of the Prime Minster, Deputy Prime Minister Winston Peters said: “Yes the Prime Minister can confirm that – that it was a cause to be careful about into the future, not to spray money around on consumerism and on giving tax breaks to your mates. And in short, not to take from the needy to give to the greedy.”

Finance Minister Grant Robertson too gave assurances during question time that he was confident he would meet his 51 coalition commitments in the budget operating and capital allowances.

Yet Treasury only expects tax revenue to be $6.6 billion higher in the four years to 2020/21, than was forecast in August when it included the National-led Government’s proposed income tax cuts.

Only $0.7 billion of this tax revenue is expected to be “macroeconomic” driven.

Treasury’s projections ‘somewhat of a best-case scenario’

Politicking aside, bank economists believe Treasury has worn rose-tinted glasses, overplaying the amount of wiggle room the Government has to follow through on its spending commitments, while sticking to hitting its debt reduction target.

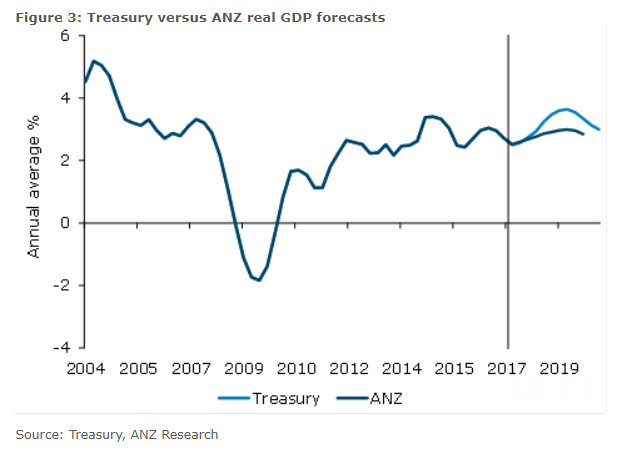

Westpac economists call Treasury’s forecasts “too optimistic”. ANZ economists say they “represent something of a best-case scenario”, while ASB economists coin them “bullish”.

At the heart of the matter, there’s consensus that the economy can’t growth as much as Treasury thinks it will.

Westpac economists say: “Treasury is forecasting 3.6% GDP growth in the year to June 2019, compared to our own forecast of 2.8%.

“If GDP growth doesn’t accelerate to the extent that the Treasury is projecting, the risk is that the Government revenue will fall short, requiring Government to either rein in some of its spending plans, find additional sources of revenue, or abandon its commitment to reducing net debt so rapidly.”

ANZ economists go on to say Treasury’s growth projections hinge on two assumptions: “First, that despite clear capacity pressures right now, residential investment continues to grow strongly. Second, labour productivity growth picks up to average 1.1% per year over the next five years.

“We are a little sceptical on both fronts. In our view, while we are constructive about prospects going forward, this economy has already picked the low-hanging fruit.”

ASB economists also believe Treasury’s growth forecasts are more upbeat than theirs, as Treasury sees stronger inflation growth.

ANZ economists recognise the new government’s “more expansionary” fiscal stance, but ultimately only see a fiscal boost replacing other growth drivers, such as the housing market and construction, rather than driving the economy to above-trend growth.

23 Comments

The good news is that they aren't using anymore the utterly nonsensical GDP growth rate that they claimed during the election campaign. They have backed down to just "rosy".... :)

Oops... Labour needs to update their fiscal forecast page...

Still showing greater than 4% GDP growth per year.

There are two key features that standout from the latest employment report.

One, is the sheer number of jobs created and two, despite all these jobs we're still no closer to getting a pay rise. There's just no pressure on wages....It's great for business, it helps keep costs down, but it's not so great for consumers and households as they keep doing the hard yards, indeed working more hours, but struggling to get ahead. Consumers, whose spending accounts for the equivalent of 60 percent of the economy, are doing it tough, weighed down by soft wages growth, higher energy costs and the debt levels. It ties in with why retailers are struggling

http://www.afr.com/markets/plenty-of-jobs-but-no-pay-rises-or-rba-inter…

Hot on the heels of 'Australian' billionaire families The Murdochs and the Lowys selling up, another Old Money member of that club, The Packers, appears to be doing likewise. Sure, there's an element of asset shuffling going on, but when it all ends, and the money is back in Family Hands, one has to take notice....These families didn't get to where they are without knowing what comes next....

"James Packer's Crown Resorts to sell $700m assets" (AFR)

The smart money is getting out .....

That's just the visible smart money

So the purchasers of the assets are dummies heading for a fall?

I would think that if someone is spending the sort of money that they do to buy those assets, they will have access to the same crystal ball to gaze into, as the sellers.

Unless the new investors are from lazy institutions like KiwiSaver fund managers, where it does not matter where the customers money goes (or is lost) as long as "fees" can be charged.

I found it quite absurd that the first thing new ministers are going to do is to LEARN his/her portfolio.

We all know what can happen if you put an inexperienced egocentric person into a leadership role.

That's really an unavoidable design weakness in democracy. I look at it this way, in three ears at least they will have a handle on how can be done and will have some good learning/mistakes under their belt.

The road to success is paved with failure.

Horse... committee. .. camel... :)

What was absurd was National Party ministers had not learnt their portfolios.

JT, having actually Read the HYEFU, the Alternative Scenario One case (P55) seems much more likely to me. I suspect that's much more in line with the bank economists, who, after all, don't need to answer to a Motley Electorate, but to shareholders and investors - a much more pragmatic bunch.

Treasury's own summary of Scenario #1:

Scenario One illustrates the impact of recent weakness in a number of economic variables persisting through the forecast period. Specifically, labour productivity fails to pick-up as forecast and business and consumer confidence remain soft, dampening investment and private consumption growth. Weaker demand leads to lower inflationary pressure and softer nominal GDP growth, resulting in less tax revenue and higher net debt.

And together with my own assessment of the Budget Holes (which, charitably, could result from a terribly rushed process, or, uncharitably, from a Litany of Lies), I rather suspect that the 20-odd Holes, if back-of-ciggy-packet guess, were estimated at 30-50 million each, constitute a $NZD 1 billion Hole already.

I will be particularly Interested in the Vote:Education outcome, say after March, when the full extent of liability for the following aspects of the Tert Ed Free-for-All will become dimly apparent:

- Institutional funding to make up the lost Fee income

- Plus the $50/week increment to allowances

- Plus the increment to actual enrolments over predictions/TEC funding allowances

- Plus the increment to institutional funding for staffing, teaching and other resources to handle #3

.

Still, we certainly live in Interesting Times, no? And we can certainly do with many more Qualified Aromatherapists.

does the 600m/year allowance for new spending allowance have to cover the inflationary growth on the $100billion year govt expenditure (particularly given inflationary impact of falling NZD and rapid increase in minimum wage)? If so then it is a joke.

To the extent that those cost inflation factors have not already been included in Departmental budgets for FY18 (and, for the more switched-on Gubmint CFO's, oxymoron alert...FY19), then why, yes. That's the essence of Joyce's riff on 'The Hole'.

And as Treasury, in full CYA mode, have inserted a long list of Fiscal Risks in the HYEFU, it's quite clear that there's deep skepticism at 1 the Terrrace about core assumptions, and they most likely view this 'Budget' as a hastily thrown-together effort, lacking deep analysis of many significant costs.

But, hey, the reaction to the whole schemozzle is gonna get overtaken by Xmas Hysteria - 'Kaikohe teen drowns puppy intended for present', 'Campers attacked at Paturau, 100 feared Clubbed', 'Non-indigene driver involved in head-on with Logging truck - export timber preserved'.....and in the meantime, there will be Xmas leave cancelled for TEC and WINZ as they try to sort through the implementations and deliver to a horde of expectant clients, every one of 'em with their Hand Out for the Munny......

I find it interesting that usual supporters for the coalition seem to stay away in droves from threads attached to detailed criticisms of their team.

What I found amusing was Mr Peters. The way I see it we earn it and taxation is the governments way to taking what you earned away from you. Mr Peters would have us believe that keeping what we earn is (a) consumerism and (b) greedy.

Using this logic I better build a fence around my vege garden in case Mr Peters decides I am greedy to eat my own produce.

I've noticed the same, Foyle. Those of us who have worked in or consulted to Gubmint, have a much more nuanced view of the inner workings, and especially of the limitations, of the beast.

Budgets, particularly whole-organisation ones, have a lot of interdependencies. Along with Treasury, I doubt that the current effort has captured more than a fraction of these - note the constant use of 'behaviour' and 'uncertainty' in the HYEFU text. A classic example (P9):

A range of other policies are likely to impact the labour market and wider economy, including Fair Pay agreements and further pay-equity settlements. These are expected to increase labour costs and may therefore reduce labour demand further. In addition, improving pay and/or conditions is likely to increase labour supply (through higher participation rates, for example). It is difficult to quantify the extent to which these will impact the economy at this time, given uncertainty over how many industries and/or professions may be eligible and therefore these are treated as risks to the economic forecasts until further policy detail is available. There is also a specific fiscal risk related to pay equity claims within State-employed and State-funded sectors.

This is clearly bureaucrat-speak for 'We do not have clue one about what the new Directors of the Good Intentions Paving Company are gonna do next'.

I detect a marked lowering of the general tone of discourse on the site from about mid-year, which is frankly quite off-putting. I've pulled back on both reading and common tating as a direct result.

After all, if we wanna see primates competing in the Poo-Put comps, we can tune in to Discovery.

Or Parliament channel.....

I for one, greatly appreciate your commentary.

What I find funny is the assumption that somewhere a switch exists, flicking which will turn off unskilled migration and bring more skilled and talented resources to NZ. An increase in minimum wage will not help reverse this problem. We do not have high paying jobs that talented expats migrating to our Western counterparts seek. If we had those jobs, our own skilled people would not be leaving the country in droves in search of greener pastures.

But Treasury’s rosy outlook for economic growth, buoyed by population growth, low interest rates, increased government spending, a positive international outlook and higher terms of trade, gives it confidence Labour will be able to follow through on its promise to reduce debt from 21.8% of GDP to 20% of GDP by 2022.

The least of NZ's worries!

so the hyefu is a lolly scramble. nothing put aside for health, education, infrastructure. etc.

with contributions recommencing to the super fund at the top of the economic cycle.

and debt will go from $56b to $70b to fund this

no increase to operating expenditure. nothing on infrastructure. very little in the way of targeted funding.

wow!

Our rock star economy was funded by $50 billion of govt borrowing.

Population growth is to remain our growth industry.

Servicing the population growth with police and schools and infrastructure is still in deficit.

How can Winston be wrong?

We are financially cooked. Recession can be the only outcome.

Erosion of the NZ lifestyle continues.

New housing subdivisions, dozers ripping up farmland as if there is no tomorrow, new kebab shops, bakeries and convenience stores, medical centres etc, all run by immigrants, have yet to run into one of these new businesses being run by born NZers. All to service new immigrants. If this is not a giant ponzi scheme I don't know what is. Here in Hamilton, it is exploding and yet it is still being said Hamilton needs even more houses. It is madness of the highest degree. In order now to stay in much the same place we have to go at break neck speed hauling in more people and chopping up more and more land.

And I did not even touch on the rapidly increasing congestion on the roads, you can just about see it increasing by the day. Again, it's nuts.

Hamilton, and every other Regional Centre, choked by the idiocy of the two-tier LVR changes and the general migration objectives. Traffic? 5 years ago it took me 3 minutes to 'trek' into town to pick up the worker after her shift finished at 5 pm. Now? I have to leave 40 minutes early just to join the throng of others who've been forced to re-schedule their lives to get into town at 5, all to accommodate the influx of new residents. And what for? Growfff...... I repeat, idiocy....

(NB: When I set up a new dealing room, I got the desks; installed the phones; put in the computer network and enough seats etc for the new staff, THEN I brought the staff in. I didn't herd them into an empty room and say "Good luck! The equipment will be along when we've made enough money to pay for it". That's how infrastructure should work in the country - put it in FIRST; catered for 10 years ahead, then ship the people in, not the other way around)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.