Stress testing of ANZ NZ, ASB, BNZ and Westpac NZ shows the fours' combined pre-tax profit would tumble by $32 billion over five years to $4 billion, but they would not breach their minimum capital requirements.

These are among the conclusions of Reserve Bank and Australian Prudential Regulation Authority (APRA) stress testing of the big four NZ banks, as detailed by the Reserve Bank. The test was based on data and regulatory requirements as at March 2017, and ran for five years to March 2022.

The testing done last year included the assessment of two scenarios. In the first, a downturn in the Chinese economy spreads through trade channels to other emerging markets, with flow-on effects to other parts of the global economy, including Europe and Japan. A collapse in demand for commodity exports and negative investor sentiment towards the Australian and New Zealand economies triggers domestic recessions and a six month closure of offshore funding markets for banks. New Zealand’s unemployment rate quickly rises to peak at 11%, house prices fall 35%, and the Fonterra dairy payout remains below $5/kgMS for three years. The scenario assumes that macroeconomic conditions begin to improve by the fourth year, though property prices do not recover. Banks receive a two notch credit rating downgrade, and face elevated funding costs in both wholesale and retail deposit markets.

In the second scenario, the macroeconomic conditions described above were overlaid with an operational risk scenario, exploring the implications of an industry-wide misconduct event related to residential mortgages. The Reserve Bank says the monetary response to the downturn sees the Official Cash Rate cut to just 0.25%, but banks' higher funding spreads mean the decline isn't fully passed through to customers' interest rates.

"Consistent with previous tests, results suggest that strong underlying profitability from repricing actions to maintain their net interest margins would allow these banks as a group to absorb significant losses through the stress scenario without breaching their minimum capital requirements. While the test demonstrates these banks’ resilience, there remains uncertainty as to how such scenarios would unfold in reality," the Reserve Bank says.

"Cumulative pre-tax profit over the five years declined from $36 billion in a baseline projection, which assumes no stresses occur, to $4 billion in the stress scenario. The aggregate return on assets turned negative in years two and three, before recovering as credit losses abated," the Reserve Bank says.

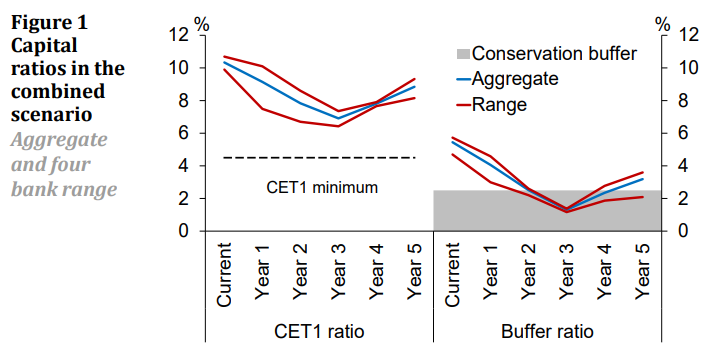

The banks began with an aggregate Common Equity Tier 1 (CET1) capital ratio of 10.3%, and an aggregate buffer ratio of 5.4%. The aggregate CET1 ratio dropped to a low of 6.9% in the third year, with individual banks' CET1 ratios falling to between 6.4% and 7.4%. Buffer ratios fell to between 1.2% and 1.4% at their low points, placing the banks in the middle of the capital conservation buffer. Most of the banks moved out of the buffer by the fifth year thanks to accumulated earnings. All four banks met their core funding ratio and mismatch ratio requirements during the test.

14% of loans default

The banks reported about 14% of their total credit exposures would default over the five years of the test. Total loan impairment expenses of $21 billion gives a cumulative loss rate of 4.3% of their total credit exposure. Credit losses were naturally spread across banks’ lending portfolios. Residential mortgage lending losses were $5.1 billion or 24% of total losses, farm lending was $4.4 billion or 21%, and general corporate lending was $4.4 billion or 20% of losses. Commercial property lending, and credit cards and other consumer lending, both accounted for 11% of losses.

The banks were asked to model scenarios involving industry-wide conduct risk and/or mis-selling in residential mortgage origination, with this having a material impact on their solvency and leading to a further credit rating downgrade.

"Submissions explored the consequences of systematic errors in automated property valuations, government-imposed moratoria on mortgage foreclosures, and flaws in origination practices, such as systematic miscalculations of loan affordability and inappropriate sales practices. The scenarios led to CET1 ratios falling a further 0.4 to 2.4 percentage points in year three of the test, compared to the macroeconomic scenario."

Outcomes sensitive to modelling assumptions

The Reserve Bank separately developed a standardised event involving a class action lawsuit for breaches of standards for loan origination, and prescribed a redress calculation methodology. The total cost to the four banks of this was $2.2 billion, there was a further notch credit rating downgrade, and five basis points reduction to net interest margins for all five years. However, the regulator notes it's challenging to calibrate the impact of an industry-wide misconduct event for NZ banks, given the limited number of relevant precedents.

It also notes there are uncertainties around the magnitude of losses banks could face in a real downturn, and the extent to which banks could restore net interest margins. Thus outcomes are sensitive to modelling assumptions used in the testing.

"Recent stress tests have shown that strong underlying earnings are an important buffer for the large New Zealand banks. The combination of low cost-to-income ratios, generally short repricing profiles, and resulting stable net interest margins, suggests that these banks would be able to internally generate capital in the form of retained earnings to offset significant credit losses in a stress scenario," the Reserve Bank says.

"Overall, these outcomes suggest that, as a group, the large New Zealand banks could absorb material losses in a downturn event while remaining solvent. The test shows that the strong underlying profitability that the banks are presumed to maintain through the scenario acts as a significant buffer, offsetting their credit losses and allowing them to generate sufficient capital to stay above their minimum requirements in each year of the test."

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

18 Comments

I'd suggest that considering the loose credit conditions up till now, a 35% drop in house values is conservative estimate if our banks found credit markets were closed. A 50-60% house price declines (Ireland style) would be more likely, with an OBR event or two to boot. I guess the RBNZ considers the likelihood of this occurring is as much as Irish Central Bank thought likely in 2005, or do they........

https://www.interest.co.nz/news/93891/rbnz-says-possibility-needing-unc…

Agreed. They should also have an 100% unemployment rate along with a zombie apocalypse scenario. It's BS that the banks can hide that they're failing with these weak as stress tests. Conspiracy between RBNZ, Trump, Kim Jong-Un and the big 4 IMHO!

Hi RP

I think catostrophic declines would be be mostly isolated to Auckland where the bubble has become the most over inflated. The rest of the country other than isolated spots like Queenstown are likely to be well within the 35% drop that they have modeled upon, especially as the migration out of the cities by the baby boomers will continue irrespective of the economic climate.

However I dont trust that the banks wont find a way to plead for tax payer bailouts....

But what % of the housing/debt does the Auckland market represent? 35% of population, but with higher median prices, so does Auckland represent 40% 45% 50% of the housing stock?

If we had a 50% drop in values we certainly would be in for a CYPRUS type scenario where all bank accounts over $100k take a haircut, I understand our banking system is set up in the same way in that banks have the power to rob bank accounts to save themselves for the greater good. Perhaps David could clarify this better ? Money in bank accounts is as vulnerable as anything else in a worse case scenario.

R-P,

The current housing situation here is by no means identical with the pre GFC Irish position. To see just how different,you should read Ship of Fools,How Stupidity and Corruption sank the Celtic Tiger,by Fintan O'Toole.

The level of outright corruption in the Irish banks,including the Central Bank was staggering and unlike Auckland,there was a surfeit of unoccupied houses.

linklater, the way I understood things was that prior to GFC, there was also a shortage of homes in Ireland, that's why they rose in value - right? Once the GFC struck, the young workers fled the country in droves leaving many vacant homes. Central Dublin fell the most. It could easily happen here too.

Presently, there is no obvious surplus of recently developed and unoccupied houses in Auckland - agreed.

The issue also deepens when deleveraging commences, this creates a surplus of homes available. There is also the existence ghost houses, this is a real wildcard. With the existence of bulk debt by a relative minority, this can easily damage the prospects for the rest. Once the availability of easy finance is taken away, the end result is the same. As far as the banks are concerned, there is no evidence yet of corruption however, with the hard sales target driven culture exhibited in the last decade by bank employees leads me to believe there could end the same way - in tears. For the participants involved, greed turns to fear.

Why are they doing this?

Because the world has a debt crisis which is starting to unwind.

Read this series

https://www.interest.co.nz/opinion/94571/john-mauldin-continues-his-tra…

I have read this series. I don't think that is the catalyst for the RBNZ's stress test.

I'll ask again, this time more specifically, what information does the RBNZ have to prompt them to undertake this study, with these kinds of numbers and forecasts?

It is a regular function by the RBNZ as part of its financial stability mandate. It makes regular stress tests, varying the criteria as it sees risks shift.

The RBNZ is not special in doing this. Every central bank member of the BIS conducts stress testing on the banking system they are responsible for.

There is no 'catalyst' per se. It is part of their normal assessment program.

Thanks for the clarifications David :)

If/when the asset bubble bursts there is likely to be a liquidity crisis as Banks are already less inclined to lend to each other, so whatever the fall in values requires sufficient liquidity in the system to allow a purchaser other than one with all cash, to buy. And even then would the liquid cash of the purchaser be available?

I can see a sort of swap arrangement working for some assets ownership changes but not for the level of Bank & Customer distress, I hope for the best but fear for the worst which could be brutal.

If that scenario occurs, a credit crunch could be expected.

https://www.investopedia.com/ask/answers/credit-crunch.asp

https://en.wikipedia.org/wiki/Credit_crunch

As unemployment rises, there are fewer potential buyers of property as they are no longer credit worthy, (or buyers lose confidence to buy property due to job security uncertainty, or buyers wait to buy at lower prices) meanwhile there is an increase of supply of property for sale as those unemployed are unable to continue servicing the mortgage on single incomes, and other owners look for liquidity. Hence there is an imbalance between supply of property for sale and demand by property buyers ...

Yes. The stress test essentially assumes that the financial system is stable. ie There would be forces at work arresting the downturn. Lets hope there are. I'm not so sure.

OCR rate decreases are a legitimate arresting force one but that all commentators now say that with most govts OCRs being very much lower than last time, only a small crisis could be dealt with.

Negative interest rates may mean physical cash may become decoupled from bank balance electronic funds face value ie Higher!

I believe that these stress tests began after the GFC, which they never saw coming. They won’t see the next one coming either. It’s all about confidence and they need to convey this sense of stability to hold things up. It all rests on how long the markets are prepared to accept low interest rates for. Once that comes to an end it’s game over.

So the banks make so much profit that they can afford to bail out the whole country for a few years and still make a profit?

Didn't Ireland top out at a 52% house price decline with a 16% unemployment rate?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.