The organisation that represents central banks from around the world has slammed the technology behind cryptocurrencies, saying that “however sophisticated”, it’s a “poor substitute for the solid institutional backing of money”.

The Bank for International Settlements (BIS) says that “looking beyond the hype,” it’s difficult to identify specific economic problems that cryptocurrencies solve.

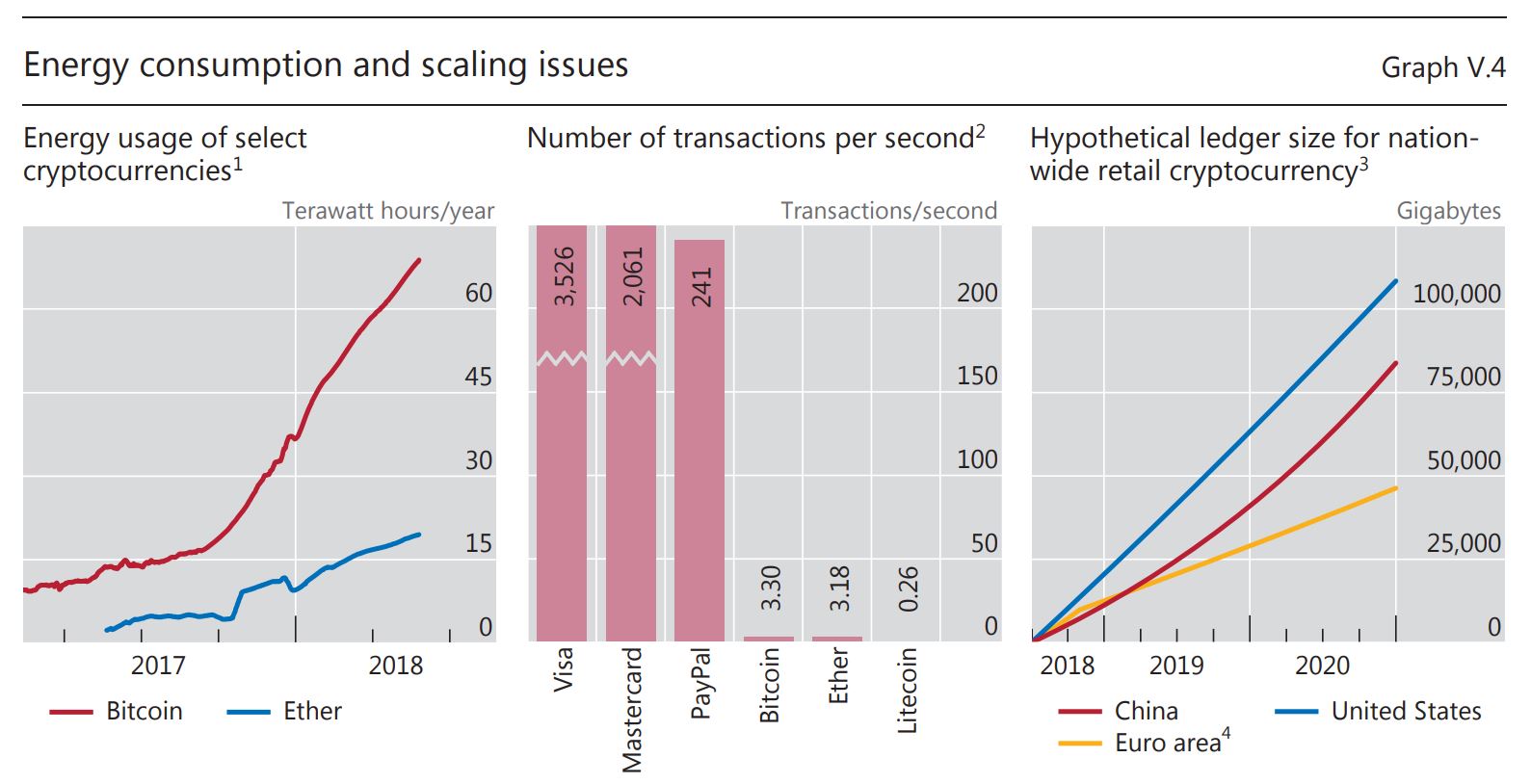

Transactions are slow and costly, prone to congestion, and cannot scale with demand, it argues in a new report, Cryptocurrencies: Looking Beyond the Hype.

The decentralised consensus behind the technology is also fragile and consumes vast amounts of energy.

Scalability

BIS explains that the way cryptocurrencies achieve trust - through their supply being predetermined by a protocol and users verifying transactions - is inherently inefficient.

For example, the amount of electricity used to mine bitcoin alone was at the time the report was written equivalent to that used by a country the size of Switzerland.

“Put in the simplest terms, the quest for decentralised trust has quickly become an environmental disaster,” BIS says.

With cryptocurrency transactions requiring users to download and verify the history of all transactions ever made, each transaction increases the size of the ledger.

And as the ledger gets bigger, it takes longer for transactions to be verified.

“To process the number of digital retail transactions currently handled by selected national retail payment systems… the size of the ledger would swell well beyond the storage capacity of a typical smartphone in a matter of days, beyond that of a typical personal computer in a matter of weeks and beyond that of servers in a matter of months,” BIS says.

It goes so far as to say that with large volumes of files being transferred, the internet could be brought to a “halt”.

Another scalability issue arises as, in order to limit the number of transactions added to the ledger at any given point in time, blockchain-based cryptocurrencies only allow new blocks to be added in intervals.

This can congest the system, which reduces the usefulness of cryptocurrencies in making day-to-day transactions, like buying coffee.

Volatility

BIS says that without a central issuer able to manipulate the value of a currency to keep it stable, cryptocurrencies’ values fluctuate entirely with demand.

“Further contributing to unstable valuations is the speed at which new cryptocurrencies - all tending to be very closely substitutable with one another - come into existence,” BIS says.

“Recalling the private banking experiences of the past, the outcome of such liberal issuance of new moneys is rarely stability.”

BIS also recognises the problem of “forking”. This occurs when a subset of cryptocurrency holders coordinate on using a new version of the ledger and protocol, while others stick to the original one.

This happened in 2013, when a flawed software updated led to one part of the bitcoin network mining on the legacy protocol and another part mining using an updated one.

“For several hours, two separate blockchains grew; once news of this fork spread, the price of bitcoin tumbled by almost a third.”

Other uses

BIS concedes that while cryptocurrencies don’t work as money, the underlying technology “can be efficient in niche settings where the benefits of decentralised access exceed the higher operating cost of maintaining multiple copies of the ledger”.

It identifies low-volume cross-border payment solution services as one of these “niche settings”, as all the intermediaries involved in the current system make it expensive.

BIS notes “cryptopayment systems” are one of a number of technologies that could improve the system, yet “it is not clear which will emerge as the most efficient one”.

SWIFT - the provider of the world’s main international payments network - is rolling out an upgrade to its system which speeds up cross-border payments and makes them more transparent.

Its head of Oceania earlier in the month told interest.co.nz this negates the need for an entirely new blockchain-based system.

Furthermore, the results of a trial it was involved with, using blockchain technology in the reconciliation part of cross-border payments, conclude the system upgrades banks would have to do to use the technology are too major.

BIS goes on to say: “Some decentralised cryptocurrency protocols such as Ethereum already allow for smart contracts that self-execute the payment flows for derivatives.

“At present, the efficacy of these products is limited by the low liquidity and intrinsic inefficiencies of permissionless cryptocurrencies.

“But the underlying technology can be adopted by registered exchanges in permissioned protocols that use sovereign money as backing, simplifying settlement execution…

“Crucially, however, none of the applications require the use or creation of a cryptocurrency.”

Regulatory challenges

Recognising the challenges of regulating cryptocurrencies, BIS says only a globally coordinated effort “has a chance to be effective”.

It says regulators could monitor whether and how banks deliver or receive cryptocurrencies as collateral.

It also suggests regulation could target institutions offering services specific to cryptocurrencies.

“For example, to ensure effective AML/CFT, regulation could focus on the point at which a cryptocurrency is exchanged into a sovereign currency.

“Other existing laws and regulations relating to payment services focus on safety, efficiency and legality of use. These principles could also be applied to cryptocurrency infrastructure providers, such as “crypto wallets”.”

Central bank issued currencies

BIS concludes there isn’t a strong case for central banks to issue digital currencies.

It warns issuing a “general purpose” central bank digital currency to consumers and firms would “profoundly affect three core central banking areas: payments, financial stability and monetary policy”.

Therefore, central banks in the likes of Canada, Europe, Japan and Singapore have experimented with issuing narrowly targeted CBDCs [central bank digital currencies], restricted to wholesale transactions.

“In most cases, the central banks have chosen a digital depository receipt (DDR) approach, whereby the central bank issues digital tokens on a distributed ledger backed by and redeemable for central bank reserves held in a segregated account. The tokens can then be used to make interbank transfers on a distributed ledger,” BIS explains.

While the same limitations outlined above apply, BIS says, “the design choices for the convertibility of central bank reserves in and out of the distributed ledger need to be implemented carefully, so as to sustain intraday liquidity while minimising settlement risks”.

BIS says that while the experiments conducted have largely replicated existing systems, the blockchain-based replicas aren’t “clearly superior” to the status quo.

This explains why central banks don’t feel any urgency to issue digital currencies.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

17 Comments

What ever happened to just taking a sack full of cash to the bank and then T/T ing it out as required?

This blockchain rubbish sounds like a solution looking for a problem.

Why are you using a bank for international transfers there are way cheaper and faster options?!

Also, what's a "cash"?

Do sacks still exist?

Do you ride your house down to the post office to pay you taxes with a sack of gold?

How did you managed to get on the internet?!?!

You are truly fascinating moa man, I have so many questions.

I got on the internet late 90's.

Used to own a payment processing company.

Have seen most of the crapolla that happens.

For our own business we would use hand delivered T/T instructions.

Bank staff knew us, we knew them. Worked out well.

” it’s difficult to identify specific economic problems that cryptocurrencies solve."

Talk about asleep at the wheel.

Central banks are the problem that cryptocurrencies solve. If we had sound money that was not manipulated and devalued by central banks then we wouldn't need crypto.

Fake news:

"Transactions are slow and costly, prone to congestion, and cannot scale with demand, it argues in a new report, "

Obviously they did not read about lightning network which is fast, cheaper and scalable.

"The decentralized consensus behind the technology is also fragile and consumes vast amounts of energy."

Miners can run on renewable energy. We have other technologies that use vast amounts of energy like shipping and cars but the value derived from them is worth the cost in energy. If Bitcoin provides a banking system for all this is a massive benefit to humanity.

"With cryptocurrency transactions requiring users to download and verify the history of all transactions ever made,"

False, you can make a transaction without downloading the whole blockchain.

"BIS says that without a central issuer able to manipulate the value of a currency to keep it stable, cryptocurrencies’ values fluctuate entirely with demand."

Haha they have to manipulate to keep it stable, so its inherently unstable?

SWIFT "head of Oceania earlier in the month told interest.co.nz this negates the need for an entirely new blockchain-based system."

Haha so we dont need blockchain. thanks for telling us what we need, Luckily we can decide for ourselves.

"BIS also recognizes the problem of “forking”

Forking is not a problem, its designed to protect the network and is resolved within the protocol"

"BIS concedes that while cryptocurrencies don’t work as money"

Really? https://www.thoughtco.com/what-is-money-1147763

The item serves as a medium of exchange - check

The item serves as a unit of account - check

The item serves as a store of value - both Fiat and Bitcoin are unproven on this ( gold is proven as a store of value)

"BIS concludes there isn’t a strong case for central banks to issue digital currencies."

This is the one correct fact, they have their system. Leave the future of sound cryptographic programmable money to the people, incorruptible by the vested interests of bankers and politicians.

Yes that word manipulate was surely a mistake that slipped out, as was perhaps "sovereign currency". These guys are keen to keep clipping the ticket.

But I went off bitcoin, or blockchain in general, when looking at it for my father. There is no way he could work in the digital realm to buy or use bitcoin. I also learnt it is no secure unless you have a separate computer that has never been connected to the internet.

If you want a long term store of wealth, it has to be physical and demand no yield (not be linked to artificial inflation by money printing). Wealth also lies in a means of production. Build something or grow something. It is frightening how many people think their long term wealth lies in a house.

I agree that Bitcoin is not for everybody, this is its strength. The current banking system is suitable for your father as they are the custodians of the funds and if he forgets his password or get hacked they might give him his money back. Bitcoin is not suppose to replace the current banking system which even with its faults, serves the needs of many. It is an alternative that enables innovation and services undreamt of before its inception.

"I also learnt it is no secure unless you have a separate computer that has never been connected to the internet. "

This is false. If you encrypt your private key then even a hacked computer will not provide access to your funds. see here for more info https://bitcoin.org/en/secure-your-wallet#online

I was initially interested in blockchain, but its strength is its weakness. It has to be massively distributed to be secure, but the bigger the distribution the more expensive it becomes. A small distribution means it can easily be corrupted by one big player.

Without bitcoin 'mining' nobody can transact bitcoins securely, and currently bitcoin mining is consuming more electricity than Switzerland.

How much electricity does the current banking system use? Is it a good use of electricity? Humans make decisions every day about how and where to expend energy. We could not have got to where we are now without consuming vast quantities of energy. There are many things in the world that use energy with questionable value. Think of all the TV's and waste that goes into making mindless programs. How much time and energy is wasted on PC and mobile gaming?

The point is, if you are using that much electricity to process 3.5 transactions per second, you are never going to make it to 3,5000 like visa. Yet on the other hand without the mining/blockchain/encryption you can't have a secure/safe currency.

My understanding of the Lightning network is that it only uses BitCoins that were present when the payment channel was initiated.

i.e. if you leave the blockchain with 10 coins. then you can trade that 10 coins as much as you want with someone else in the same payment channel. But if you need 11 coins, you reconcile the payment channel and are straight back into the blockchain.

To solve this, they network the payment channels together becoming a "Lightning network. Doing this removes vast swathes of "transactions" from the blockchain.

Therefore defeating the very aim of blockchain which is to be a definitive record of transactions (i.e. public, secure, and transparent.)

The aim of Lightning network is to scale transaction speed and capacity, you can choose to use this method to transact or you can choose to use the usual Bitcoin transaction on chain. The important thing here is the ability to decide how you make transactions. If you don't like either then you will always have the good old banking system to use.

Bitcoin. You give some money to a guy called Alfonso you found on the net, and he sends you back an email saying you have a zillion bitcoin. Heard this one somewhere before. Nothing new under the sun.

if this is you then you shouldnt be on the internet...

Is that a bust of Nero in the background?

Fake News

Halt the internet.

lol

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.