Hopeful first home buyers faced a mix of good and bad news in April, with house prices at the bottom end of the market declining in every region of the country, while a steep rise in interest rates made mortgage payments the most unaffordable they have been in the 18-year history of interest.co.nz's Home Loan Affordability Report.

The Real Estate Institute of New Zealand's national lower quartile selling price dropped to $640,000 in April from $661,000 in March, and has now declined by $30,000 since it peaked at $670,000 in November last year.

April's lower quartile price was lower compared to March in every region of New Zealand, with the decline now spreading to regions such as Canterbury, Waikato and Nelson/Marlborough, which up until last month were continuing to post rising lower quartile prices.

The biggest decline has been in Otago where the lower quartile price was $505,000 in April, down $75,000 compared to its peak of $580,000 in October last year.

That was followed by Auckland, where the lower quartile price was $900,000 in April, down $66,000 compared to its peak in November last year.

Other regions where April's lower quartile prices were down significantly from their recent peaks were Northland -$60,000, Bay of Plenty -$47,000, Hawke's Bay -$40,000, Taranaki -$45,000, Manawatu/Whanganui -$60,870 and Nelson/Marlborough -$30,000.

On their own these price falls would be good news for hopeful first home buyers because it would mean they would need to save less for a deposit and borrow less for a mortgage.

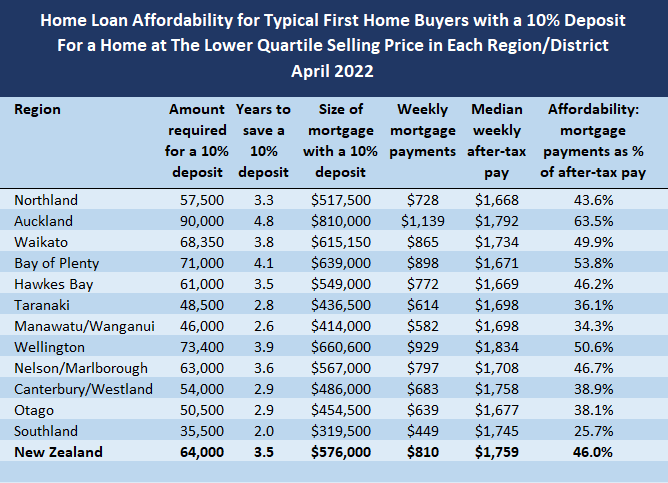

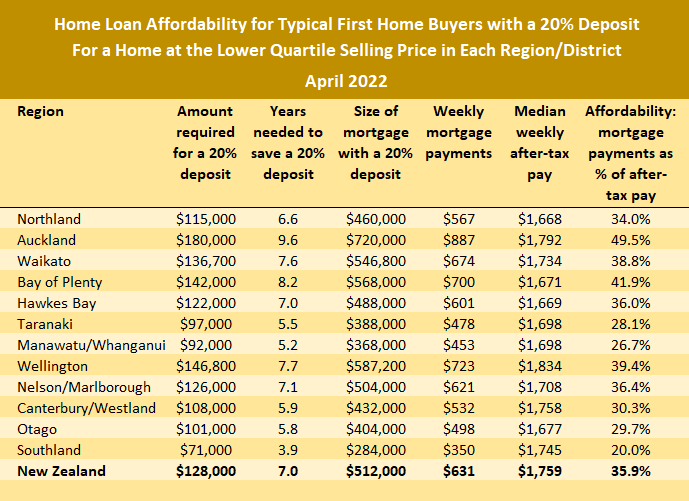

The amount needed for a 20% deposit on a home purchased at the national lower quartile price peaked at $134,000 in November last year and had declined to $128,000 in April, a saving of $6000.

The amount of debt buyers would need to take on for an 80% mortgage declined from $536,000 to $512,000 over the same period.

Unfortunately those savings have been eclipsed by very sharp rises in mortgage interest rates, which have pushed up mortgage payments to levels that would likely be unaffordable for people on average wages.

The average of the two year fixed mortgage rates charged by the major banks increased to 4.96% in April from 4.41% in March, and has almost doubled since it hit a record low of 2.52% in May last year.

That means the mortgage payments on a home purchased at the national lower quartile price with an 80% mortgage would have increased from around $611 a week in March to $631 in April, even though the amount borrowed would have been $24,000 lower in April.

In the 12 months from April last year to April this year, the mortgage payments on a home purchased at the national lower quartile price with an 80% mortgage would have increased from $432 a week to $631 a week, up by $199 a week or 46%.

The Home Loan Affordability Report also tracks median pay rates for couples aged 25 to 29. This suggests the after-tax pay for such a couple both working full time would have increased $35 a week over the 12 months to April this year. Meanwhile, mortgage payments on a home purchased at the national lower quartile price with an 80% mortgage would have increased by $199 a week over the same period.

So what the housing market has given to first home buyers in the form of lower prices, which result in smaller deposits and smaller mortgages, it is taking away in higher mortgage payments.

First home buyers appear unlikely to get any relief from that trend any time soon. That's because it is the rate at which interest rates are increasing rather than the amount they are increasing to that is unusual.

The last time two year fixed mortgage interest rates were at their current level was September 2015, and they were above current levels for the entire period from January 2002 when interest.co.nz began compiling the figures, to September 2015, reaching as high as 9.64% in 2008.

So by historic standards, current interest rates are still relatively moderate.

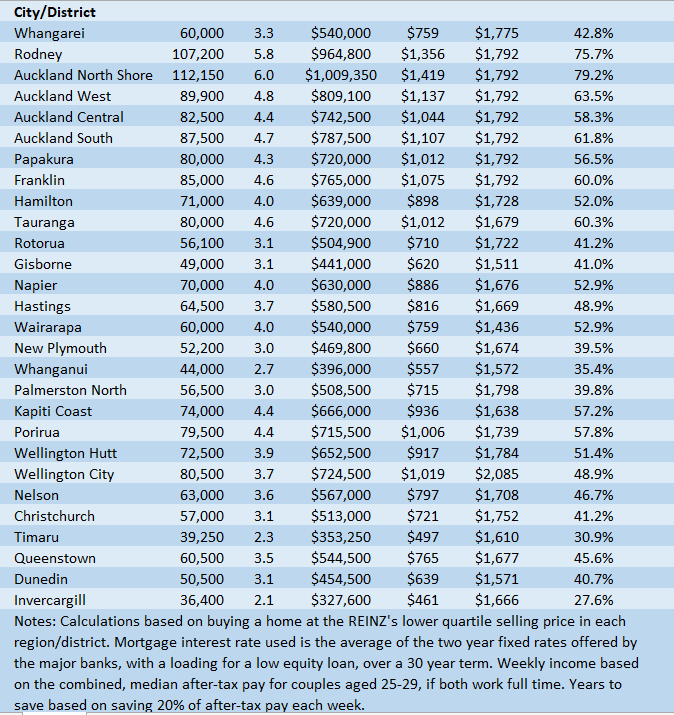

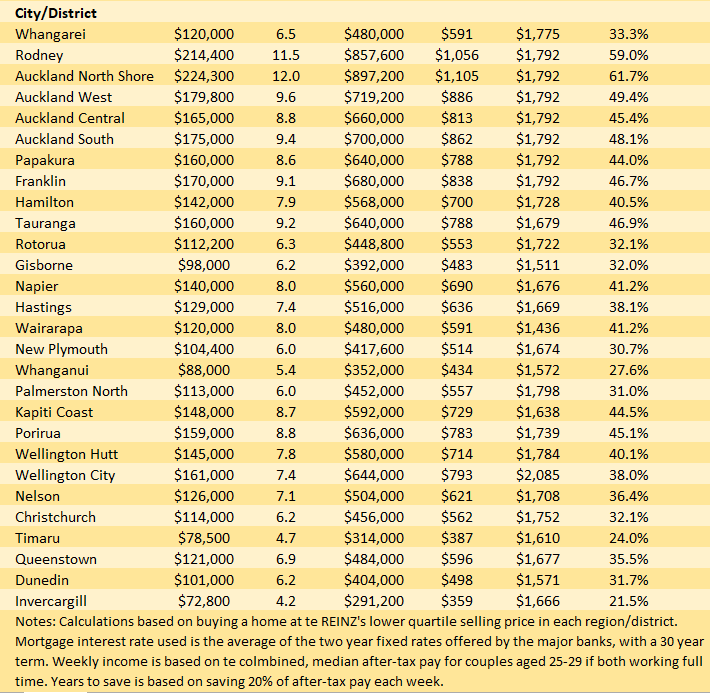

The tables below show the main affordability measures with 10% and 20% deposits, in all main urban areas in the country.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

131 Comments

This may be true for now, but not necessarily so for much longer, especially after the Ponzi implodes and house prices decrease by 30% to 40%.

Mortgage rates up, house prices down. Weekly payments, the same. Buying a reasonable house in a reasonable suburb is competitive.

Woopsy do.

lol

A price drop to that extent will trigger widespread joblessness in the construction, real estate and financial services sectors and quickly ripple out to retail and hospitality.

Most non-homeowners would struggle to earn a stable income, let alone be in the financial condition to borrow hundreds of thousands for a house.

You’re right, not sure about “most” but if the trend continues the unemployment rate will rise and this puts pressure on there being a recession.

If we ignore the spin (and supply/demand pressures) on the article and instead consider it as “house prices yet to meet availability of credit” then there are only two primitive factors at play. One of those factors will need to give to provide a sustainable housing market and it seems as though RBNZ hands are tied.

A price drop to that extent will trigger widespread joblessness in the construction, real estate and financial services sectors and quickly ripple out to retail and hospitality.

Unfortunately when you have house prices rising ~30% in some areas over a twelve month period during Covid then this is what happens, hence the reason many many commentators were up in arms yelling from the roof tops "This is unsustainable!!!".

The time to avoid what you are speaking of was some time ago now, but people were making crazy money and simply didn't care. The cards have begun to fall so the price will just have to be paid, whatever that ends up being. Pointing out the potential dire consequences now does not make up for the fact that we had been repeatedly warned it would come to this.

Yep! "Unsustainsble" indeed. I like this word as much as the World Economic Forum does - pity they never use it in relation to debt.

I bet property colomnists in the press who have been promoting property right through the pandemic, and right up to the cliff-edge, will be super popular with those who bought the cool aid.

Even a 20-25% decline will whack those sectors, but obviously the impact increases the greater the house price declines are.

Unfortunately a rise to that extent has led to widespread disillusionment and despair amongst non-homeowners, leading to a population decline and lack of essential workers. It has fuelled inflation and is destroying the economy.

Since the rise was so rapid, I doubt a fall to that extent would make so much difference..it only takes prices back 12 months. In 'normal' circumstances where prices were rising around the 5% mark I would have agreed with you.

Exactly. All youth are non home owners and it is leading the hard working smart ones (without a silver spoon free house) yo export themselves. Just when they are about start a 40+ career paying tax in NZ. That they now pay tax elsewhere. Aussie is doing it's best to send some back though,via 501.

When you look around and wonder where all the NZ born and raised medical, teachers, police etc etc are, this is why.

What a result.

One must be very cautious when discussing the issue of human capital flight. ✈️ ✅

Kjeldorian gets his knickers in a well proper twist about it.

You forgot to write "I think" at the beginning of your post

There is no need to be a first home buyer at the moment.

The smartest kids are hopping on a plane for overseas experiences ✈️✅ and the second smartest kids are standing back while the market reverts to mean. 🫧⤵️💥

Only the very dumbest kids are buying the slums of tomorrow at today's prices. 🤯

Be Quick

7% guaranteed

Flee NZ

Two out of three correct. Not bad that's still a pass.

Impulsive decision making often leads to strife, I don't recommend "Be Quick". CWBW is learning that the hard way.

Depends what you are marking them for.

3/3 are obnoxious spam.

There's always going to be certain class of stuck-in-the-muds that get triggered at the thought of people leaving for better and more interesting life prospects.

They are inevitably driven by the fear of seeing their friends and colleagues 'get ahead' while they stagnate in a country rapidly going backwards.

There are always those who are weak willed and flee at the first sign of trouble.

First sign of trouble? LOL

The signs of trouble have been obvious for a very long time. There are some around who believe that people are obligated to stick around and be victims.

But those who have aspirations in life know that the only prize for being "strong willed" is going to be co-governance and a pat on the back for being a good tenant and tax donkey.

When you face any hardship your first instinct should be to run.

Those who are less simple will assess the hardship and use their judgement to weigh up if its short term hardship worth enduring for a worthwhile goal, or long term hardship for that is not worth enduring for a lousy goal.

Looking around at the state of the place, the answers are fairly obvious. Increasing numbers of astute people are now making this decision and voting with their feet. The caterwauling will grow louder as more of the tax donkeys move on to greener pastures, while perpetrators will rant and rave like Jake the Muss about how they'll be back. But many of them won't. It's human capital flight.

Brrr, it's a bit cold today, better move to Aussie

A trip to the northern hemisphere sounds like a better idea, don't you think?

Too many problems up there, where should they be fleeing to?

My car won't start, better flee to Aussie

Getting quite salty aren't we? Is that because you "invested" in extra houses "for your kids" at peak bubble? How is that working out?

Someone insulted me on the internet, uprooting my family and buying my plane tickets now

As I've stated countless times it's a hedge. It's working out great.

Not salty, just sick of your bullshit

Throwing a juvenile tantrum becuase people on the internet are observing and commenting on the brain drain is peculiar behaviour.

Are you afraid that your own rent donkeys are going to leave next?

I quite enjoy people insulting me on the internet. It lets me know that the facts are hitting home.

Spamming the same “advice” is peculiar behaviour.

i don’t have a “rent donkey” and don’t know what that is.

A “fact” spammed must be true

7% guarantee

be quick

flee Nz

What is peculiar about being consistent? You are a very strange person.

Yes, this is correct. 7% mortgage rates are coming and heading abroad is a solid strategy.

What’s peculiar about spamming the same message on every post?

You're worse than Raid Shadow Legends

I think that getting off the screens and going outside for a walk will do you a world of good.

Speak for yourself Brock.

Please do go on and elaborate...

Just a right of passage in NZ for our youth to spend time overseas, work and travel do an OE.

Ah yes, keep normalising this to be many's only shot at ever owning a home. The only 'right of passage' in NZ is to have your pockets turned inside and held upside down by your elders for any spare coin you have managed to save by living like a celibate monk.

Yeah houses will remain unaffordable as people will still borrow the max…. Just lower amounts.

Houses will only be affordable when the OCR is higher than inflation to slam the brakes on.

A fair way to go

While I have noticed a lot of prices dropping in Auckland, I think we are in a strange time where the prospective first home buyer (like myself) no longer has the benefit of low interest rates, but doesnt really have the benefit yet of softened prices. Vendors are still expecting prices from a time of low interest rates. This is also not helped by the various property valuation sites which haven't really adjusted their estimates at all. We have recently made the call to pop to London for a couple of years, make double what we make now and return (hopefully) to a humbled market.

You'll have an amazing time 👍

You and many others I would suggest - I'd also suggest that 2 years becomes 5 years+

Good call Adam, my partner and I are hopping over to London for a few months (remote working holiday). Basically the plan is to just watch this train wreck till the end of the year at least.

May consider buying (at an extremely sloth like pace) next year. My recent home-owning friends don't like this "bad attitude".....

I'll pour out a little liquor for all those recent FHB's while we're in Camden.

Partner and I (late twenties) off to the UK for a month to see family but we will definitely be having a scope of the lifestyle... most likely move over mid 2023.

Question will be do we buy mid a rental here before we leave... Haha

Sounds like a like a very similar situation to us. We lived in London for 3 years and loved it. (Partner still works for UK company)

Unfortunately we came back due to COVID semi tossing up wether to buy end of 2020, but I looked at what was happening here and overseas with that rest home patient printing trillions, China getting wrecked etc and we decided to sit out. (Still are)

Never felt so vindicated, admittedly there were a few moments I questioned this decision along the way.

Unfortunately friends around me just had ants in their pants to buy end of 2020 and throughout 2021 (some of whom are now in negative equity), they still sit in the cathedral of "houses only go up" my opinion was not a welcome one to say the least.

It seems they don't want to discuss it these days...

I would really hope the correction is faster than 5 years, we definitely want to come back and start a family, but we we won't be sacrificial lambs on the altar of human stupidity.

US/UK/AU is not off the table.

Good call mate. I had the best 4 years of my life in London and only came back for family reasons. Anyone in their 20's or early 30's with a shred of ambition would do the same particularly with the way things are right now in NZ.

Incredible adventures, new friendships, amazing cultural experiences, it's not just about the money but growing as a person - personally and professionally. I don't think I would be where i am today without that experience.

There's a lot of chat about jumping overseas at the moment but I don't necessarily think London is the smart move. Inflation is markedly worse, expected to hit 10% and the abysmal whether 10 months of the year won't help your depression. A number of friends over there are looking at either moving back or AUS. If we hadn't tied ourselves to a house in Auckland my partner and I would seriously be considering Sydney as a place to move to with it's lower inflation, higher wages and great climate.

Well Aussie might not be all it's cracked up to be either:

Michael is joined by Russ Stephens, Co-founder of the Association of Professional Builders, to discuss reports that half of Australia’s building companies are on the brink of collapse

‘From the data we collected, we could see that more than 50% of building companies were starting to experience cash flow challenges and were unable to pay their bills as and when they became due and payable

https://www.2gb.com/podcast/half-of-australias-building-companies-are-o…

Who said I was depressed?! haha. London makes the most sense as my partner is a corporate lawyer and the salaries in London for this are obscene! Also, London's abysmal weather doesn't matter so much with Europe on your doorstep!

London's weather is not much different to the south island or even lower half of the north island. I am from Manawatu and spent 20 years in London and the number of days you can be in the garden in a tee shirt (ie not too cold, wet or windy) is greater in London than Manawatu. Not to mention that UK houses are built with the winter in mind, unlike the traditional NZ house.

Patience grasshopper your time will come.

That title is misleading and ignores the bigger picture.

With a 19% mortgage it is was very worthwhile paying every spare cent off a loan (assuming you purchased the home in high mortge times at lower prices).

With low interest rates mortgages are massive and the spare cash thrown at the massive mortgage has almost zero impact.

Higher mortgage rates = lower prices, and increased ability to pay off more capital. This is exactly what new home buyers need.

💯

It's suprising how few people grasp the mathematics of this.

(sorry did an edit after you comment)

yes, 100% correct.

I appreciate that interest.co.nz has to 'bait' the headline sometimes to get us to read and comment. And there are a lot of insightful comments.

But it shouldn't be at the expense of them writing a balanced article, rather than the reader having to go to the comments to get both sides and the balance.

Although there are some good articles, the comments section is by far the biggest reason I am here.

Agree. The vitriol can be a little tedious at times however, the humour and commentary from obviously well informed commentators is priceless!

This is true but you aren't factoring in inflation. If you are locked into a mortgage with a low interest rate (circa 2.5%) your best bet is to kill your mortgage as aggressively possible while on that rate. Inflation is eroding the value of your cash so there is little value in saving + the sharemarket isn't looking appealing either.

Hutt Valley Market Update 16th May

To start with this week – the real estate agents in the Hutt have started to come to the realisation that the “property party “ is well over

I received an email from a “large Hutt Valley real estate firm” on Friday with the heading “Huge Price Reductions on these Properties”

Normally these type of email headings are reserved for Kathmandu and Briscoes and every kiwi knows you don’t pay full price at these retailers unless your desperate.

So It makes sense with these real estate headlines that buyers have quite a bit of time up their sleeves and FOMO has rapidly disappeared. Makes sense to ensure (as you would at Briscoes and Kathmandu) you don’t pay too much- further discounts are likely in the near future.

Current Market Listings

611 houses on the market- down 17 on last week.

Quite a few houses sold last week (mainly in the 700K-850K range) and also there was a large number withdrawn unsold– at least 11. May is looking to be a stronger month for sales than April and March were – recent house price falls may be encouraging people back into the market – specifically in the bottom quartile of the market

There continues to be a low number of listings this week (Consistent for this time of the year) combined with withdrawals and what looks like a consistent number of sales appears to be the key reasons for the decline in the number of houses.

Based on the REINZ data which showed that 96 sold in Feb and 104 sold in March and 98 in April giving an average sale of 25 houses per week– 611 houses means there is 24.5 weeks stock on the market.

I am expecting given the withdrawals and low number of new listings for the number of listings to fall to around the mid 500’s

House Price Reductions

308 houses have a listed price

55% of the houses listed with a price have reduced their price since listing

The average markdown has fallen this week from 84K to 82K.

Of those that have listed prices (pool 308) -34 have reduced their prices by 100K (last week this was 30 properties

6 have reduced their prices by over 200K and 2 have reduced their prices by 300K with the biggest reduction been 350K (a total 20% reduction)

The data continues to show the majority of houses listed are under 900K. The Median house price for all 611 listings is now 830K. (Steady on last week and the lowest Median YTD – previous low was $839K)

REINZ data showed the April Median was 847K – my data for April showed 849K.

The latest QV valuations (valuations by QV which are updated every month and give an approximation of a houses value) have dropped $130K since Jan for the Hutt.

In April the QV valuation had dropped 80K – approximately 20K a month since the start of the year but this escalated in April – dropping 50K in one month.

Meanwhile Homes is indicating there has been an approximate $110K drop on house prices in the Hutt valley– since the peak which they are indicating was early Nov 21. According to homes prices are back to June 21 prices – so flat with this time last year.

Houses sold vs houses removed

My records show 157 houses listed with a Price have sold YTD (up 15 from last week).

I have records of a further 133 houses (up 11 from last week) that have been removed from the market unsold YTD.

18 of those houses removed from the market have been listed on the rental market

The total number of houses removed from the market in the last 4 weeks is 57 (this compares to about 5 houses delisting a week over the previous 14 weeks).

Length of time on the Market

- 441 of the houses have been on the market for over 30 days - 72% (last week it was 472)

- 303 of the houses have been on the market for over 60 days - 50% (last week it was 286)

- 169 of the houses have been on the market for over 90 days – 28% (last week was 166)

The number of houses on the market over 60 days is for the first time over 50% (one in two). This has risen from 32% of houses in mid March (one in three) and just over 1 in 4 houses have now been on the market more than 3 months.

The time to sell is getting longer and longer. Anybody looking for a quick sale of their property would need to be well under the QV valuation or have a very attractive property at a very attractive price.

A real estate agent did advise most houses are going conditional with subject to sale as the most common condition in some cases there is chain effect occurring where there are now several houses all in the chain subject to sale. So anybody with cash is going to be an attractive buyer at the moment and could probably get a premium discount on the asking price.

Rental Market

Meanwhile the rental market has 198 properties for rent (up 4 on last week), and up 93 on this time last year – when just 105 houses were for rent.

Average rental price reduction is $58 a week (up $5 on last week) and 42% have dropped their prices since listing.

As noted last week I have also been noting how many properties are listed for rent over $650 a week.

At the moment the percentage of properties listed at $650 is 41% - last week it was 40%. This is the lowest percentage of houses over $650 since the week of the 27th Sept 2021 when 38% houses listed were over $650.

And it tanks the vapour equity of debt stacker investors, while increasing debt servicing cost. The squeeze of negative leverage. Loans are coming due for rollover and conversations about real equity will happen.

More popcorn pls.

Especially those 40%'ers on Interest Only. Having paid of zilch/nada of the principal.

You mean those "hard working mum and dads" who are "just trying to get ahead" and "save for their retirement" while bleeding the peasant class dry?

Lets have a moment of silence please for those greedy suckers... they are about to go dooooooown.

It's comments like this that I really hate. Gleefully wishing misfortune on others.

A lot of these "greedy suckers" are every day working class people who put their money where they were incentivised to. A lot of them won't be able to weather it, there will be loses of life savings, there will be divorces and there will be suicides.

But f'em they aren't FHB so they deserve pain and misery.

Nonsense.

- We have had YEARS of gleeful newspaper articles celebrating rising prices.

- We have had YEARS of saturation-level propaganda about "hardworking" landlords.

- We have had YEARS of avocado on toast bulls//t and people looking down their noses at renters.

- We have had YEARS of people like you - and yes I'm looking right at you Kjeldorian - telling renters that their situation was hopeless that they would never get out of the rental trap.

People like you - yes you Kjeldorian - have been gleefully observing and contributing to the "pain and misery" of renters for years now. So suck it.

- Did I say celebration of house price rises were any better? No

- Did I say all landlords were faultless and hardworking? No

- Did I say the avocado on toast nonsense was true? No

- Did I say that renters situations were hopeless and they would never get out of the rental trap? No and I've been saying the opposite for years.

I haven't been gleefully observing and contributing to the pain and misery of renters, I've been trying to empower people to improve their situations (to great derision here)

You could not be more wrong with your post.

A quick Google search comes up with this one of several examples of you Kjeldorian gleefully pontificating to the peasant class (December 2021):

"The truth that nobody wants to hear is that yes, in the last few years it has become harder to buy a house. But it is not impossible, if you follow the "rules" of budgeting and investing you can do it.

Or you can follow the advice often given on here, give up, it's hopeless. Leave NZ and if you can't leave then put all your savings into booze. "

A perfect example of the revolting attitude that you and so many other Kiwis have had towards renters. Don't lecture me about wishing misfortune on others.

" - Did I say that renters situations were hopeless and they would never get out of the rental trap? No and I've been saying the opposite for years."

""The truth that nobody wants to hear is that yes, in the last few years it has become harder to buy a house. But it is not impossible, if you follow the "rules" of budgeting and investing you can do it. "

You just proved my point?

You are saying that I have a revolting attitude towards renters but you are calling them peasants. You are the one that hates renters.

He's merely speaking your language by calling them peasants.

My language? I love renters, I was one for ages.

I think the whole crash situation is hard for some people to accept all they have ever seen is more money printing they just have to understand the bubble of everything is now over and the main game in New Zealand is housing which over next few years will topple back to around 2011 price’s. This will give the young generations a chance to get in the market its the only way to have a better society.

.... and if they put their MONEY where they were incentivised to, they will be fine.

If they BORROWED somebody else's money in order to enslave their neighbor then they are more likely to go down.

They rolled the dice. They gleefully took the massive capital gains over the last few years. Nobody forced them to take the risks. They can live with the consequences of their actions.

There is no way that average Kiwi houses are worth a million bucks and only somebody blinded by greed would think they could "get ahead" by buying something so stupidly overpriced to rent out to their fellow citizens. They deserve everything coming to them.

Their money + borrowing. Incentives have been housing for decades.

Slavery is illegal.

They invested, they didn't go to skycity.

You give these people too much credit in terms of financial knowledge.

I don't wish ill on anyone, as tempted as I am to make an exception for you.

Keep doing what you're doing Kjeldorian. Seems there are a few twisted minds on this site who revel in the downfall of others, aka bully mentality.

What's the difference between slavery/serfdom and debt servitude?

It's ok now because we willingly choose servitude and aren't forced into it?

Turning homes into speculative investment vehicles is great for the FIRE economy, but as anyone can see, not so great for society or the economy as a whole. It rates up there as the best propaganda/marketing scheme since De Beers and the diamond market and everyone fell for it. Social engineering at its finest.

The more "money" that goes into future "wealth", the less there is circulating in the economy now, and more debt creation and money printing is needed. So, the numbers are bigger, we're wealthier than we've ever been, yet we can't afford any of it from both an environmental and societal perspective and nor can we afford a reset to real values.

Solution? Let's keep doing the same thing over and over again and hope for a different result!

Every previous civilisation learned the hard way too.

Housing is a scarce resource that unless they've been living under a rock the last few years they must have known many people are struggling to afford.

Despite this, they've bought up more than they consume themselves for their own benefit.

I see nothing wrong with wishing misfortune on them, just as I see nothing wrong with people laughing at people buying up all the hand sanitiser or toilet paper then not being able to sell it.

*Shrug* Investments are never without risk. Many aspiring FHB too are every day working class people locked out of home ownership because older working class people want to turn shelter into their own personal retirement vehicle off the backs of the young.

I have ZERO sympathy.

Investments are not usually without risk.

Although in recent years, obviously, New Zealand's property market seems to have been supported more like a welfare scheme than an investment where prices are free to fall. If the market is permitted to crash by allowing some free market risk and pricing, that might be a bit of restoring it to an investment rather than a welfare scheme.

Any FHB hoping to tap their KS to form part of a deposit are also watching that balance get ravaged at the moment.

(ask me how I know... )

You didn’t move your KS to a cash fund?

Hi HouseMouse. I moved everything to Cash/Conservative as Covid hit NZ the early 2020, and staved off some of the losses. I then watched as the CBs cranked up the QE and my Conservative fund went backwards in real terms.

I fully expect CBs/Govt to pull out all the stops to juice assets again and again, but I am also a very conservative person by nature, so settled on 65/35 Cash/Growth split last year. Have seen approx 4.5% loss (nominal) this year, not including govt/employer and my own contributions. I'm with ANZ.

"Im with ANZ" ... there in lies your problem. Also if its for retirement and you are young stop jumping in and out of funds, stick to a growth fund and leave it alone for 30 years

Not young. 50, with two teenagers, trying to secure a home for us after a protracted divorce 4 years ago. Would rather not touch the KS but am competing in a market with couples with 2x KS+ bomad or with speculators using equity. Divorce settlement unfortunately coincided with the market going bonkers 🙄

Good thing is I have some equity from the divorce+ KS, an 'okay' salary and am debt free. 👍

Wish me luck!

Not young. 50

Beg to differ on that point, I'm also 50 but still young?

Debt free is a VERY good thing.

Agreed, 50 tis fine. I feel young, and am in much better situation than 4 years ago, but I'm very wary of taking on large debt on a 25 - 30yr term. Would quite like to stop working one day :)

Good luck, debt free is a good position to be in. In UK the oldest they will give you a mortgage to is to finish by 75 and then only certainly lenders. Not sure about NZ.

Was 52 when I got the $560000 25 year mortgage on a $700000 property. So I guess they expect me to keep working long past retirement age. At least I'll save on transport costs by getting free buses on my SuperGold card. Would just need a job where I turn up after 9am and leave before 3pm.

Unfortunately with the interest rate increase I cannot do 10% KS any more and have dropped that to 3%. Still growth fund but I doubt it'll be enough to clear the mortgage at 65.

Last year, BNZ was happy to give us a 30-year mortgage, which meant we'd be paying till we were almost 80! We thought that was nuts and did not even consider borrowing the amount BNZ was happy to throw at us. (How many others in a similar situation last year happily borrowed such big bucks?!)

Then in December, after bank directors became accountable for irresponsible lending courtesy of the CCCFA, the bank called to say we can now only get a mortgage for 20 years, which is a lot more sensible. So I figure, the CCCFA is probably a much-needed piece of legislation that hopes to save banks and people from themselves. Too bad it probably came in too late for many..

Good luck Slapheid from one slapheid to another.

Wishing you luck, Slapheid! All the best with getting it all sorted.

So it is the price of lower quartile houses that are on the decline, not the other 3/4.

"That was followed by Auckland, where the lower quartile price was $900,000 in April, down $66,000 compared to its peak in November last year.

Other regions where April's lower quartile prices were down significantly from their recent peaks were Northland -$60,000, Bay of Plenty -$47,000, Hawke's Bay -$40,000, Taranaki -$45,000, Manawatu/Whanganui -$60,870 and Nelson/Marlborough -$30,000."

Auckland, Nov 21 to Apr 22, say decline of 6.8 %, average per month 1.4%. Roughly works out to be 16% in Nov 22.

Has it ever been a good time to buy except in hindsight? Go find me a news article from any period about how easy it is to get into a home

Whenever the going is good the market quickly adjusts. Always.

There simply aren't any FHB who can jump in or will jump in. Why would you catch a falling knife for exorbitant prices to live in some shitbox in a bad area?

These property owners seem to think they can get 685 or 700k for whatever garbage property they have for sale when it is $1500 per fortnight in interest after a 20% deposit.

The vast majority of young people aren't earning enough to pay for these mortgages or to save for a deposit when landlords charge $750 per week for rent. I completely support rent strikes by tenants until rent prices go down. Rent is effectively a tax on income which robs the producers and workers for their income, renders our wages uncompetitive through higher wages needed to pay higher rent with no benefit for consumption.

The parasitism of the Property market's dominance over the economy makes it bankrupting to raise a family or to invest in the future. All the young people who stay and try to raise families are robbed blind and worked to death just so their children are thrown into daycare so they never see them. This system does not work for anyone except the vampires who make the loans.

Rent is not a tax on income it is a cost for an essential part of living. You either provide this for yourself(purchase it) or rent it from somebody else. It's fact of life and is not free. Rent prices charged by landlords are based on costs that they pay of owning and running the property. Very many do not make any money from a cash flow perspective i.e. day to day running of the rental property.

Rent prices charged by landlords are based on costs that they pay of owning and running the property

Let me stop you right there.

No thanks just stating facts.

Some days I wish this site required users to pass a simple test before they could post on this site.

Bu then there would be no comments.

There would be a couple, but no-one reading would understand them :)

Across the broad sweep of time you are correct. Rent reflects the cost of someone providing the accommodation. Zoomed in it doesn't work that way. When I rented out my house, I didn't add up my costs and put on a 10% margin, I just looked at the market rent. The house that is leveraged to the eyeballs rents for roughly the same as the one next door that has no mortgage outgoings - maybe less as the owner can't afford vacancy.

As you say, there is no rule that says my rental income will cover my costs, or even that capital gains will show up and compensate for a poor investment.

Rent prices charged by landlords are based on costs that they pay of owning and running the property

Yeah nah, couple of questions................

Rent is an essentially part of life, but when it is excessive, it is negative on economic productivity. The classical economists (Smith, Ricardo, Marx, George etc) all opposed excessive rents due to their plunder of income generated by productive work. Even the Physiocrats recognized that it was negative for the economy. When they spoke of the Free Market, they meant free of rentier capitalism where someone clips the ticket without improving value in any way.

Landlords might not make money off the rental, but they were off capital gains, which now doesn't work for them. So rents have gone up to keep overleveraged landlords solvent.

The issue is that the extremely high housing prices mean landlords need to make yield to cover mortgages, which depends on wringing out their tenants of all their possible spare income. My rent is 50% of my income and I earn well into the six figures range taking care of a SAHM and kid, both of us took the advised path of University (Engineer and Lawyer respectively) and despite saving for two years straight, were priced out until houses started free falling. We are infinitely better off than our peers working shit jobs for 1/3 or 1/2 who picked the wrong degrees living crammed into derelict houses in the city.

Guess I'll be born earlier next time so I can catch the market.

We are born when we are born, we just have to do the best that we can to get ahead and provide for our families. I have bought at the bottom of the market and top of the market, but if you are in it for the long term you can ride it out, but its not easy. When I was renting it was 50% of my take home pay. When I bought it was 70% + rates and maintenance. So really doesnt stack up. I guess NZ market is based on IO loans and making the money on capital gain when the property is sold. But the rental still needs cash flow to run day to day and capital gain is not guaranteed.

I get you are boomer posting at me, but here's some perspective. 50% of your income on rent when you are in the top 5% of income earners (and I live in a shit neighbourhood) tells you it isn't sustainable. How about the huge portion of the population subsisting on 50-60k?

Precisely. When people say things like "we just have to do the best that we can to get ahead and provide for our families," the big assumption they are making is that the status quo can't or won't change, and that the only thing to do is for individuals to alter their behaviour to accommodate the status quo. But 'doing the best we can to get ahead and provide for our families' is often best served not by individual action, but by collective action. And the first step to collective action is acknowledging - and raising awareness of - the fact that particular groups are being treated unfairly. The best thing to do as a member of that group is not to try to play 'model minority' and do what you can to work within a system that seems hell bent on shafting you and others like you, but to work to change the system.

Well I am not a 'boomer' I am not old enough. We are individuals and cannot act as a collective, so I stand by my comments, we do the best that we can, at the end of the day I have to earn the money and pay my bills each month no other people are going to chip in and help. So my lifestyle choices dictate the outcome for me and my family, so budgeting to what I can afford, no new car, no overseas holidays etc.

So my lifestyle choices dictate the outcome for me and my family

The problem is that it is fairly obvious that most people they don't. People who have made very similar lifestyle choices in terms of getting qualifications, working hard at their jobs, delaying having children, living carefully and saving etc, now have very very different outcomes depending on when they were in a position to make these choices. This is the problem: there seems no apparent reason why a hardworking nurse, teacher, policeman etc should have a vastly different standard of living and set of opportunities because they qualified in (say) 2020 as opposed to 2010, but they do - and not for reasons outside anyone's control like a natural disaster or something like that, but because successive governments have pursued a set of policies explicitly designed to transfer wealth from younger workers to older asset owners. People can see that despite working just as hard and doing all the right things, their life choices and financial outcomes are significantly worse than people just a few years older than them, and that's what injustice looks like.

Also, refusing to believe that collection action is possible seems strange. How do you explain situations where groups of people achieved significant change, like the French Revolution for example, if you don't believe in collective action? At some point, the solution is not to continue being a well-behaved peasant in order to maximize the scraps you get from the table, but to band together and demand a seat at that table. Your views don't seem to leave any room for that or even acknowledge that it's possible.

I did not say I did not believe in collective action but that I could not act in a collective way. I just concentrate on my own finances. When purchasing my first house in the UK, I had given up 2 years prior as it was not possible for me as I was priced out of the market. . 2 years later market crash and 8 out of every 10 houses I viewed was a repossession and a lot cheaper so then it was possible for me to purchase. Its not when you are born that dictates what happens. Its right place right time and personal choices.

In the space if two sentences you say 'it's not when you are born that dictates what happens' and 'it's right place right time and personal choices'. Can you not see that when you are born has quite a lot to do with being in the right place at the right time? And that the set of personal choices we have available to us depend on the circumstances we find ourselves in?

Not really, we just have to do the best we can with the circumstances that we are in at the time, it is no use blaming the previous generations.

A person or set of people in power make a set of decisions that result in you getting unfair treatment. Maybe your boss, for example. It's perfectly reasonable to instead of just shrugging your shoulders and saying 'oh well, I just have to to the best I can under the circumstances', point out the unfairness and do what you can to get it addressed. If someone was being unfairly treated by their boss, to tell them 'well, not point blaming them, just put up with it' would be ridiculous advice. I don't understand why some people are so set on preserving what is clearly an unjust status quo to the extent that simply pointing out the injustice is taken to be 'blaming' and 'not doing your best.' If everyone had this attitde we'de never have got beyond feudalism.

So are you going to tell the previous generations they did it all wrong and they should compensate the current generation?

I'm going to keep pointing out that one generation has benefited at the expense of another as a result of a long running set of policies that have pretty clearly resulted in injustice. And that that should be taken into account when developing policies going forward. If you want to call that 'telling the previous generations they did it all wrong and they should compensate the current generation' then it's up to you

Nice post Al, liking the positivity

Fixed it for ya...

Rent prices charged by landlords are based on the cost of debt they incur by overpaying for housing in an effort to offset income tax, and being forced to update features like basic insulation and heating...

fhb will always be better of with less debt

All this means is that prices haven’t yet fallen back into the range buyers can afford to pay, and still have considerable way to fall yet.

For FHB the other big factor is how much less of an advantage investors will have. Interest rates rising means the yield will be becoming less attractive at the same time their equity position is worsening.

Good time to sit back and wait

All the day in,day out breathless comments. Will bottom out in 3 or more years. Daily hand wringing and grumblings and groaning ,is unnecessary,really. For me,just building the deposits ,enjoying life.

Worth noting that total mortgage repayments have been increasing on average by around 3.5% per year over the last six or seven years - despite the housing boom. This is about the same as rent increases.

Sadly, people always spend as much as they can afford on housing - whether they are buying or renting. There is always a slightly better house in a slightly better suburb within reach.

We are only at start of downturn interest rates still just up from emergency level, inflation climbing and NZD tanking which will put inflation higher. If anyone is think of purchasing a house now it would be prudent to wait could be two or three years till prices finally hit bottom at which point they will be 50% too 60% from top last year.

It would be prudent to grow your emergency fund as much as possible because if we are down 50-60% we will be deep in a recession.

Even in the deepest of recessions, the unemployment rate only reaches around 10%.

Which means that 90% of people who want to work can have a job. Recessions are tough on some people, sure. But the vast majority of people make it through recessions just fine.

Agreed. The problem is that many have lived their entire lives being protected from any negative financial effects and encouraged to live beyond their means. The very thought of this coming to an end does not bare thinking about.

Yes indeedy Smudge02 price discovery and no bailout are sadly lacking in the life education of recent history. The only advice I could offer first home buyers is , be patient but not too patient.

Depends on where you live.

USA/Britain, sure

Spain, Greece, Ireland to name a few, not so much.

Also youth unemployment usually tracks at 3-4x the unemployment rate so even if, IF, unemployment stayed at 10% you're looking at youth unemployment of 30-40%

For context in the USA great depression house prices dropped 35% and unemployment was 25%.

Hi Greg, It is not fully truth that rising interest rates are disadvantage to FHB.

Firstly FHB are already at disadvantage with or without interest rate hike BUT falling house prices are big plus for FHB despite rising rate as now if they do manage to buy house their mortage will be 20% or 30% less as all indication are that fall of 20% to 30% is imminent ( have already fallen by 10% to 15% though with resistance as those who are able to hold are holding for now with hope that like in past 2008 and 2018 this downfall too will be short and shallow, not realizing that this time is different as RBNZ is not able to rush to support by reducing rates or LVR, instead is forced to do opposite so worst is yet tome).

1: Having mortage of $600000 Is better than $800000

2: Saved from buying into ponzi under FOMO and seeing their equity turning into minus.

Advantage or disadvantage, the madness had to stop as also not good for economy in the long run, so earlier the reset, better it is as cannot avoid facing, What we are facing now.

Anyone arguing that economy reset is not good is influenced by vested biased interest as economy cycle has to play out.

What I found of interest is that the median weekly income in Palmerston North of $1798 is better than the $1792 of Auckland North Shore, but the median house price of $508500 is so much lower than $1009350.

Why would anyone want to work in Auckland for the same salary but have to pay double for housing? Is it really that more attractive in our biggest city? Or are there other factors at play?

A LOT of asset rich lower income OLDER folks live on the North Shore.

The fact is people are so much better off to buy now than a year ago. It's too simplistic to say the market is "taking away" the benefit of lower prices with higher repayments. If you had bought last year you are stuck with the level of debt you bought your place with- yes you might have paid off 10-20k more by locking in a low rate for a year or two, but if you had waited until now you could have saved more money in the form of a deposit AND have the benefit of the lower prices of today (which in most cases is going to be lot lower than 10-20k). We're seeing entry level prices in parts of Auckland (e.g. Mt Wellington, Avondale) $100k-200k+ down on what they would have been mid-last year. I suspect we'll see a large group of people with a massive amount of debt on a house that's worth significantly less than they bought, and who also will inevitably have to fix at these higher rates at some point. When their rates come up for renewal, they may also no longer have the 20% equity required to lock in the banks lower rate card, making the climb to equity that much tougher. It is sad that this will mainly impact first home buyers, but I guess that's the way the cookie crumbles. Long run though, building costs are going up alongside these drops, meaning new construction will quickly fall off, ultimately meaning a new bigger bubble at some point in the distant future.

Unfortunately the priority for many home buyers is securing the loan to buy in the first place. Not nearly so easy this year as in the past.

Feeling like I dodged a bullet here by securing for 3years. Gives me time to either generate more income or hold out for the rates to stabilise. if that fails then sell at a loss perhaps. But I’ll hold on for dear life

Talk about stating the bleedin' obvious!

Sometimes I feel like I was the only one watching effects of politically driven monetary interference on the real estate market in the 1990s...

If only Labour had regarded all as a housing crisis rather than a first home ownership crisis*....by now a massive state housing build would be well under way creating constructive (literally 😬) solutions.

(I believe that the Labour policies are quite cynically aimed at voting potential first home buyers and their families.)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.