This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

1) The 'hubris' of trying consign the oil industry to the dustbin of history too quickly.

It's a catch-22 situation. We're trying to wean ourselves off fossil fuels in order to save the planet. But it's a long, slow transition away from the likes of oil. And on the journey the moves we make to try and reduce oil use can push the price of it higher. This, of course, hits us in the pocket, typically hitting those who can afford it the least the most.

In an episode of Bloomberg's Odd Lots Podcast this week Peter Tertzakian, Managing Director of energy-focused private equity firm ARC Financial, talks about these issues. Tertzakian is based in Canada, a major oil and gas producer. He notes staffing shortages in the sector, among other things, are making it harder to ramp up production.

Driven by an end of oil narrative and climate change concerns, Tertzakian describes how fewer people are being attracted to work in the oil industry. He cites the petroleum engineering department at the University of Calgary. Typically there'd be 30 or more students in a graduating class, but currently there's just one.

He describes a messy transition away from oil that is contributing to a perfect storm.

As I watched the boom and the bust cycles, there was always a repetitive theme on the oil and gas side. When the price of oil and gas went up, that was the signal, the siren goes off for the companies to go back and drill more and bring more supply on. Now, as we all know over the course of the last half dozen years, that signal's been broken because of the vilification of the industry, climate change concerns, the divestment movement, end of oil narrative, all that kind of stuff.

And then of course the turnover of investors in many of the publicly traded western oil and gas companies basically who want their money back in terms of dividends. So that means there's not a lot of money going back into the ground, certainly not as much as there used to be, to give us supply side response to meet the demand which is still there and as we can see growing. Everybody's back flying and going on vacations and driving. And then you lose your upstream talent pool, and combined with a war in Europe with Ukraine, and boy, it's just like the perfect storm to create an energy crisis the likes of which we have not seen since the 1970s.

Tertzakian goes on to discuss financing challenges the industry faces with ESG, or environmental, social and governance, issues at the fore of western investors' minds today.

There are two major sources of financing like in any company, equity and debt. So historically, especially when the price of the commodity goes up, equity players from Wall Street come in and say 'here go drill, go produce more.' And you produce more, the cashflows are strong so you are able to borrow more. But the combination of seven years of low prices and not making any money, already investors were saying 'give me a call when you make money.' And then on top of that the divestment movement and end of oil narrative, ESG and many financial institutions, pension plans for example, saying 'no, we're not allowed to invest in these companies anymore,' and banks coming out and joining things like the net zero banking alliance, which basically says no more fossil fuel debt investing.

And so now we're in a situation where the oil and gas companies are making a lot of cashflow, they can finance themselves and they can even drill themselves, but the investors who stuck with those companies are basically saying 'well, I stuck it out with you, give me my money back, a dividend and buy back shares and so on.' Again we're in a situation where the ability to make decisions to put money back into the ground, to grow production is very encumbered.

What's happening is there's what I call the ALT finance universe that's starting to emerge. So the ALT finance universe are equity providers, debt providers that are not overly concerned about ESG. And they say 'fine, sure we'll give you the money, may be at a higher price.' So they come in and they start financing these companies, - at the moment at $120 a barrel, or even $100 a barrel, oil companies are vigorously paying debt down. They don't need any money, and they are issuing special dividends, and so on.

But the issue's going to come when the price of oil falls back to say $80, and we think it's all ok but really it's not. It's a very precarious situation because the route issue of still the need for fossil fuels, oil and gas for several decades in my opinion, is not going away.

Having financed a range of different types of energy and watched previous transitions, Tertzakian argues it's not a good idea to prematurely abandon the oil industry.

Because the price goes up to $120 [a barrel], gasoline goes to $5 [per gallon]. It's like a massive carbon tax, say the equivalent from going from $50 a barrel to $120 a barrel. That's like imposing a $250 a tonne carbon tax on the people, which is huge and it disenfranchises the lower income strata of society and creates all sorts of social issues and polarisation. So it's one way to think about forcing people to switch off of oil and gas and to alternatives. Except the alternatives are not available easily, it costs people money which they don't have now to say, buy a electric vehicle or replace their furnace or their heat pump or air conditioning or whatever. And so we just create this really distorted economy that speaks to a very disorderly transition that has potentially a lot of civil unrest and problems.

The transition does not occur overnight. If you look at historic transitions they take decades. It's a lot of hubris to think we could get off this stuff in a matter of a few years and make a switch, [which] is being disproven right now.

It's a fascinating listen with Tertzakian concluding we should be focusing on the core objective of reducing carbon emissions. Putting an industry out of business is a lot harder than reducing emissions, he suggests.

2) How the US could lose the new cold war.

Joseph Stiglitz, Nobel laureate in economics and Professor at Columbia University, casts an eye over what he sees as a new cold war pitting the United States against both Russia and China. To win support from other countries Stiglitz suggests, in a Project Syndicate article, the troubled US ought to get its own house in order, with China the more serious long-term combatant than Russia.

This front in the new cold war opened well before Russia invaded Ukraine. And senior US officials have since warned that the war must not divert attention from the real long-term threat: China. Given that Russia’s economy is around the same size as Spain’s, its “no limits” partnership with China hardly seems to matter economically (though its willingness to engage in disruptive activities around the world could prove useful to its larger southern neighbor).

But a country at “war” needs a strategy, and the US cannot win a new great-power contest by itself; it needs friends. Its natural allies are Europe and the other developed democracies around the world. But Trump did everything he could to alienate those countries, and the Republicans – still wholly beholden to him – have provided ample reason to question whether the US is a reliable partner. Moreover, the US also must win the hearts and minds of billions of people in the world’s developing countries and emerging markets – not just to have numbers on its side, but also to secure access to critical resources.

In seeking the world’s favor, the US will have to make up a lot of lost ground. Its long history of exploiting other countries does not help, and nor does its deeply embedded racism – a force that Trump expertly and cynically channels. Most recently, US policymakers contributed to global “vaccine apartheid,” whereby rich countries got all the shots they needed while people in poorer countries were left to their fates. Meanwhile, America’s new cold war opponents have made their vaccines readily available to others at or below cost, while also helping countries develop their own vaccine-production facilities.

3) Can the Fed fix what's driving inflation?

Upping the ante in its battle against CPI inflation running at 8.6%, the US Federal Reserve last week increased the Federal Funds Rate by 75 basis points. This was its biggest increase since 1994. Inflation of 8.6% is even higher than the 6.9% the Reserve Bank of New Zealand is grappling with.

Casting an eye over Fed Chairman Jerome Powell’s press conference, J.W. Mason, Associate Professor of Economics at John Jay College, City University of New York, heard the sound of a man with a job he knows is impossible, but who feels duty-bound to go on regardless.

He points to comments by Powell that it might be possible to bring inflation down without causing a recession, but the pathway is challenging due to issues not under the Fed's control such as the impact on energy, food, fertilizer, and industrial chemical prices from Russia's invasion of Ukraine, plus supply chain issues more broadly.

This was the key moment. The Fed chair acknowledged that current inflation is mainly due to factors that have nothing to do with U.S. credit conditions.

In effect, we’re looking at a job that calls for a sewing machine, or maybe a fire extinguisher, when all Powell has is a hammer. But as the rest of the press conference made clear, he plans to go on swinging it.

Let’s take a step back. Today’s macroeconomic orthodoxy puts economic management in the hands of the central bank, which relies mainly on a single instrument, the overnight interest rate between banks. This arrangement is based on a certain model of the economy. In this model, the supply side—the productive capacity of a country’s labor and businesses—grows at a stable pace. Spending, meanwhile, may run ahead or fall behind, depending mainly on developments in the financial system. Asset bubbles may raise desired spending beyond what the economy is able to produce, as businesses take advantage of cheap financing and households of their paper wealth. Bank failures may cut off credit, pushing spending below potential.

If these assumptions hold, then it makes sense that the institution that sits at the apex of the financial system is also the one that manages macroeconomic imbalances like inflation or unemployment.

But the assumptions may not hold. Macroeconomic disturbances may come from the supply side rather than the demand side. Demand may fluctuate for reasons unrelated to finance. Supply and demand may not be independent of each other. Depressed demand can discourage capacity-boosting investment, while strong demand can encourage it.

In these cases, the Fed’s power over the financial system may not be enough to stabilize the economy. Efforts to offset supply disruptions by adjusting the flow of credit somewhere else may fail to address the underlying problems, or even make them worse.

4) Vladimir Putin's rich friends.

The Organized Crime and Corruption Reporting Project (OCCRP) has written about LLCInvest.ru, an email domain not publicly visible, a bunch of interconnected companies holding palaces, resorts, yachts, jets, and bank accounts full of cash, and some apparently wealthy friends of Russian President Vladimir Putin feature too. The implication, of course, is that it's Putin, who as the OCCRP puts it "cultivates a public image of abstemious patriotism," who's the wealthy one with the friends stooges for him.

The Black Sea palace has been claimed by an old friend and former judo sparring partner of Putin’s, Arkady Rotenberg. The surrounding vineyards are split between two other Putin associates: the son of one of his childhood friends and a well-known oligarch, Gennady Timchenko. The villa north of St. Petersburg belongs to Sergei Rudnov, the son of another old friend who died in 2015.

But all these assets, seemingly held by many different people, have something in common: They are owned through companies and nonprofits that are connected to each other by an underlying technical infrastructure visible through an email domain: LLCInvest.ru.

Every major asset that has been publicly attributed to Putin shares this connection.

The “LLCInvest” companies also hold dozens of other valuable properties and businesses. Some are associated with Bank Rossiya , a lender widely known as “Putin’s bank,” while others ultimately belong to members of his inner circle.

LLCInvest is described as looking like a cooperative, or an association, in which members can exchange benefits and property.

In total, journalists were able to identify 86 companies and nonprofits that appear to be part of this loose network. Together, they hold assets worth at least $4.5 billion, including mansions, business jets, yachts, and bank accounts filled with cash. All of them are interconnected, sharing the same corporate directors, registration addresses, and service providers such as auditors and registrars.

5) A new take on local politics.

Satoko Kishimoto, who lives in Belgium, has been elected mayor of the Tokyo district of Suginami. Yes, someone who doesn't even live in Japan, let alone the region she now represents, has been elected mayor. This is a very Covid-era story.

According to The Brussels Times, Kishimoto has been living in Leuven for more than a decade. Although she is originally from Japan, she seems pretty settled in Belgium with a husband and two kids.

And although she has been in Japan campaigning, her husband Olivier Hoedeman says they may not actually move to Japan.

Whether Kishimoto and her husband will move to Japan, or how they will go about it is not yet certain, he said. “Our youngest son is still in secondary school and still has a few years to go. So moving to Japan is not going to be so easy. We still have to think about it.”

So how did Kishimoto even end up running for mayor of Suginami, which has a population of about half a million?

“During the Covid-19 crisis, when everything happened online, Satoko participated a lot in online public debates in Japan from Leuven,” her husband Olivier Hoedeman said on Flemish local radio on Monday.

“Satoko is very interested in politics and through her work for the Transnational Institute in Amsterdam, she knows a lot about it too,” he said. “She became very popular with the progressive movement in Japan and was asked to run for mayor in Suginami.”

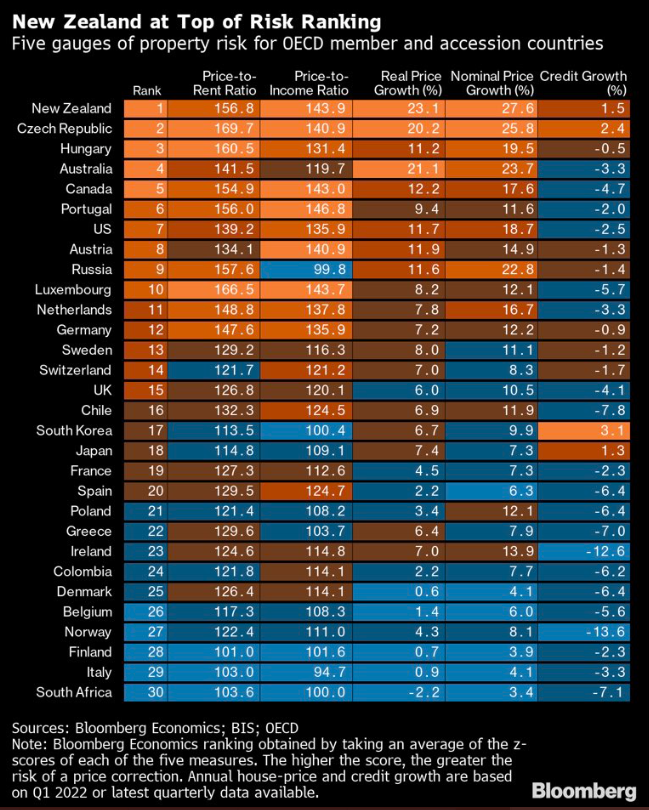

5+1) NZ No. 1 for property risk.

New Zealand comes in at the top of a property risk ranking chart of OECD countries compiled by Bloomberg.

If 2021 was the year New Zealand’s house-price growth reached dizzying heights, with an annual increase of close to 30%, 2022 is shaping up to be the year the music stops — and the abrupt change has left people scrambling.

58 Comments

NZ has the most inflated housing bubble in the developed world. It is no surprise that it has been ranked as the number 1 highest risk of a significant price correction. Housing prices in NZ would have to halve in order to reach sustainable, sensible levels in synch with economic fundamentals.

This is a Gold Medal podium finish for New Zealand. Keep up the good job guys.

Throughout the pandemic lockdowns and on, have to admit I got heartily sick and tired of our PM & her ministers & bureaucrats, incessantly crowing that New Zealand was “world leading.” Perhaps we were but for sure, the above property risk chart has us at exactly that without any doubt at all. The PM & her ministers though are oddly silent. Why is that?

... Chris Hipkins crowed that we were " front of the queue " ...

And we still are : #1 most likely country to endure a house price collapse ... Gold Medal to Labour ...

... honorary Silver to Adrian Orr ... onya , buddy ...

And a Bronze to the nations local councils ... incompetent , as ever ...

And a large Platinum to all the voters who made it clear they would not tolerate any Capital Gains Tax in any form whatsoever.

Can’t recall the vote on that.

I can. It was before the 2017 election. The electorate got wind of the potential tax grab(s) that Labour were plotting and at the eleventh hour Jacinda & Co threw their cart into reverse and that included hurriedly vouching that there will be no CGT, so long as Iam Prime Minister. So in that way there was a vote only it happened before rather than during the election. A very clear case of electioneering on the basis of whatever it takes.

I'm surprised that National did not approach Hanna-Barbera to come up with another Dancing Cossacks commercial. The first one in 1975 was very successful at not only giving National the vote, but appeasing the self centered voting generation which to this day still shouts the loudest when it comes to paying their fair share.

Well now. That Labour government of Kirk had implemented ACC, a property speculation tax, sent a frigate & cabinet minister to protest the French nuke testing, cancelled a Springbok tour, commenced rail link satellite towns such as Rolleston and introduced compulsory superannuation. Regrettably that government is unfairly maligned. But none of those initiatives were either unsound or unjustified. But an oil crisis and the passing of Kirk largely undid them. Muldoon introduced electioneering based on personality attacks that were particularly vicious, and without doubt he excelled in that. Once Kirk was no longer present, no one else in Labour could withstand him.

So there was no vote.

Having lived and visited a number of countries around the world, the cost of our homes are crazy, but more importantly what you get for the cost is out of line. I visited open homes last year and saw homes priced over $1m with no central heating, wood rot, requiring new roofs, little insulation and kitchens/bathrooms requiring upgrades.

The price of new houses can't reduce by much due cost of materials & labour & paperwork.

Land prices can reduce, but resource consents, and service infrastructure can't.

But land can only take, say $100k off the price of a new house, maybe $200k. So NEW house prices can't reduce by much.

So the building industry will (and some say it has already) grind to a halt.

On the bright side - just as the new gib plant comes on stream, demand will have evaporated.

All this, unless we can bring more people in - and why would they unless they are escaping from N Hemisphere.

4) Vladimir Putin's rich friends.

The Black Sea palace has been claimed by an old friend and former judo sparring partner of Putin’s, Arkady Rotenberg. The surrounding vineyards are split between two other Putin associates: the son of one of his childhood friends and a well-known oligarch, Gennady Timchenko.

Hmmmm,,,

Yeah - always hard to tell who is lying the most!!!!

esp in gangster land….

Why is this a bad thing?

If you are going to be a the authoritarian ruler of a Nation, you should have a cool palace. It is plainly baller, and it would be far cooler if we had that sort of style of patron politics here. Honestly sick of the catladies and kindness.

Were no1!!!!. Shows the endemic culture of greed presented as debt inflated housing.

Nothing to be proud of.

Yes number 1 and with the aggressive interest rate rises definitely the 'canary in the mine' scary stuff ahead!

Yes, no. 1, as long as that means we beat the Aussies, then that is all that matters.

It doesn't matter how bad that being no 1. means.

The NZ exceptionalism attitude is disturbing. There was a time when NZers were more humble about achievements. Proud but humble.

That all changed and I think the property bubble is partly to blame. NZ (and Aussie) sailed through the GFC. Yes it was tough but we didn't really take the pain like other countries as Chinese stimulus enabled our banks to keep partying while immigration and the scammy education sector kept trucking along.

We believe our own BS and have been lead to believe that we are economically bullet proof. Granny Herald likes to run copy from some obscure publication about how NZ is #1 for something. Anything. After a rugby test match, they run stuff "what the world said" (when most of the world doesn't care about rugby or the All Blacks). They know people lap this stuff up. The govt doesn't actually do anything because they believe they can get away with it by stroking the egos of the sheeple and telling them how great they are.

We need to go back to being humble, pragmatic, and understated. I think it's better and healthier for society in the long run.

Not long before he took over as head coach Brian Lochore said to me something like “there is nothing worse than an over confident All Black team.” Over the years NZ has had great success from being the underdog, a dark horse, of low profile. Too often now the image, both that of player & team, is set as of higher importance than the work on hand. It strikes me that if NZ is so damn good at something or other, why does that have to be broadcast stridently to the world rather than just letting the achievement speak for itself. It is too painfully like the little bloke in the far corner shrilling look at me, look at me.

Well put.

perhaps a housing crash and nasty recession will bring back a bit of the old kiwi humbleness.

there’s a weird mix in this country of insular cockiness on the one hand, and inferiority complex on the other. Hence the prevalence of reporting on things that stroke the kiwi ego.

unfortunately most liveable city in the world - a sham - won’t fit the bill this year. Auckland has gone from 1st to 34th…

there’s a weird mix in this country of insular cockiness on the one hand, and inferiority complex on the other.

Agree. Paul Theroux wrote about the inferiority complex of Pakeha NZers in his book about the South Pacific. The insular cockiness has been there but has grown. And I also think that's partly because of the bubble.

Yes that insular cockiness inferiority combine aptly sums it up. Quite some time ago a German business colleague, who knew NZ well, socially & commercially, quipped New Zealanders look from afar at the world with a pair of binoculars, but held the wrong way round. He added, for good measure, that the nation just needed to jump out of its own shadow.

If only it were true.

How long ago? Did you offer any advice in return perhaps on how the magnificent people of Deutschland could have viewed or conducted themselves differently too?

Conducted themselves differently? Seeing as how he was fortunate to escape the Nazis, but his parents weren’t, don’t imagine he needed any advice with regard to that.

Great selection Gareth - thanks.

#1 is a fairly intelligent discussion, on an upper Titanic deck, without much reference to the Plimsoll line. We have not the spare energy - or the time - to build replacement infrastructure; we took 200 years to accumulate this dedicated-to-fossil-energy collection. And we are already in debt, unrepayable. And therefore flying blind, via accounting in 'money'.

The crux of the problem is that we are an energy construct, not an artificial token one. In energy terms, we can no longer afford ourselves. That shows up as unwillingness to 'fund' capex, as remaining options get sequentially worse.

https://consciousnessofsheep.co.uk/2022/06/22/the-new-new-new-world-ord…

Interesting quote from Putin in there too.....

Couldn't lead in anything but inflated housing by nearly all more important metrics like poverty , pollution, inequality etc we trail the rest . The government should be ashamed.

More like we all should be ashamed....

Unfortunately I voted for her too. Not next time. Or the other mob.

Every nation gets the government it deserves.

Joseph de Maistre

Original text:

Toute nation a le gouvernement qu'elle mérite.

Letter 76, on the topic of Russia's new constitutional laws (27 August 1811); published in Lettres et Opuscules. The English translation has several variations, including "Every country has the government it deserves" and "In a democracy people get the leaders they deserve."

I don't want to continue to have the calibre of Prime Minister New Zealand deserves. It's just not good enough.

You can probably hear the hissing sound now. It comes from Auckland & Wellington & other places of highly priced housing. It's the sound of all the hot air being let out of the bubble, to my & many others relief.

Minus 15% from the 2021 peak is my pick for the end of 2022 with another 5% in early 2023. The only thing that may delay that is if our wonderful govt ramps up our immigration, which I wouldn't discount in an election year. What's it to be? Stable house prices with moderate increase in immigration [workers & skills] or falling house prices with a continuing labour shortage?

I think deep down, we all know the answer to that.

Remember in the gfc how construction completely stopped for an extended period, interest rates dropped eventually and building was too slow to pick up again as people started to move here?

That's my call for what will happen this time round.

You are very likely right. But you will be ripped to shreds here for saying anything other than property prices are going to tank 50% and a massive oversupply is only months away.

We can have both,

Prices tanking to a level that matches expected interest rates for a few years, and massive oversupply in the strange corners of NZ that do not have jobs or anything else drawing people to them (especially in a recession).

When immigration is touted as the recovery mechanism, and house building subsidies/support downplayed as 'suppressing prices', we can sail away nicely into the next bubble.

Construction stopped about a year before the GFC, with the collapse of the mezzanine finance sector.

I think you could be right, but not for another 2-3 years. We’ll have a significant over supply within the coming year.

but come 1-2 years later, interest rates will be lower again and we will have another round of house price inflation, although in my opinion it will be much milder.

The spiciness of future house price inflation will be subject to how big the fall is and whether we decide to put a barrier at the top of the cliff.

The closure of our one and only oil refinery - Marsden Point will do nothing towards making our lives easier, "greener", or less expensive.

This refinery has served us well through all seasons of geo-polictical turmoil, supplying us with 80% of our petroleum needs and 70% of aviation fuel requirements.

Note well, that not many people are aware that this process is underway. With Marsden removed, 100% of our refined oil needs will have to be imported by sea tanker, each one returning empty at normal charter fees.

Think how much you are destined to pay at the pump - that is, if it will be available at all should conflict erupt in the western Pacific.

I've given up caring Pathos, you can't discuss it in public. My advice is to spend more time in non-woke countries where the service is still amazing and affordable. Fly Qatar or Emirates, holiday in countries that haven't signed up to net-zero. If NZ wants to twist itself into knots about methane become a giant pine tree plantation I really couldn't care less anymore. I can afford the fuel and to travel and highly recommened it.

Are there still non-woke countries?! Pray tell.

There are, including Turkey which was amazing despite reports of it's demise and Istanbul is the most impressive aiport I've ever seen. Total chaos at the Western airports I visited in sharp contrast to the well oiled efficiency at non-Western.

Turkmenistan

TK - does that level of selfishness reflect a race?

Or just an individual?

And why the insecurity?

We import the oil to refine at the refinery anyway. So I expect the ships are already 'returning empty'. It was a privately owned refinery that was not making money so it closed. That must mean refined fuel can be imported cheaper than they could refine it from imported crude?

My understanding was that Marsden supplied around 70% of NZ’s fuel. That percentage may have reduced pro rata, as the nation has expanded? What though is difficult to understand is why NZ’s own crude was not considered for refining by the Muldoon government? Appreciate NZ’s crude is of a different grade, but was it not economical to refine that first and then import to top up? If we had had a refinery as such it would still be operating accordingly. Bit hazy and under knowledged on that. Anybody fill in the gaps?

My understanding is that Marsden Point consumed 3% of the country's energy as a refinery. I think we have exported a portion of our national emissions by closing the refinery - success! Hopefully the increased emissions in Sth East Asia stay up there.........

The hand-wringing over raising rates is getting extremely tiresome. When Reserve Banks where dropping rates no one, I mean no one, was arguing they shouldn't because lower rates wouldn't increase global commodity prices, like oil or food. Reducing rates was all about "boosting demand within our economy" and "the wealth effect" as commodity prices stayed low and we offshored entire industries to China.

Look, we get it, you like low interest rates because you have a vested interest in the status quo. Unfortunately some of us also enjoy price stability and using money to purchase goods which is made difficult if it necessitates a wheelbarrow in place of a wallet. The China offshoring boom is finishing and that means either another China comes along we must curtail demand.

What do we all think a neutral interest rate is ( I mean the one you and I pay at our Australian owned bank )

I would say 5%, but is that just a round number?

I hear the current mortgage rate in the USA is 5% fixed for 30 years.

In historic context that's still low because the average FED funds rate over the last 50 years is about 4.9%.

Is 'neutral interest rate' a useful concept? We have long term trends within our economy be they demographic, investment cycles, political and geopolitical cycles etc. that fundamentally mean our economy isn't stable. Similarly NAIRU, the more you think about it the more you realise it isn't a fixed number.

Maccy B gives its perspective on the horror show unfolding in NZ. Love the headline:

Ardern watches in horror as Reserve Bank steers New Zealand into recession

https://www.macrobusiness.com.au/2022/06/ardern-horror-as-reserve-bank-…

Horror? Prime Minister Ardern will claim the government have achieved their house price objective and do a victory lap. A rent collapse would do a lot for child welfare in New Zealand.

Also, FYI, RBNZ likely prefer "transitory recession" with the emphasis on the first part.

In all fairness though, Governments of both colour claim "victories" in situations totally out of their control. If people are happy to blame Labour for 30% annual house price inflation, then they deserve just as much credit for the falls.

Horror? Prime Minister Ardern will claim the government have achieved their house price objective and do a victory lap. A rent collapse would do a lot for child welfare in New Zealand

That's possible. Maybe a photo shoot with Zalensky will seal the deal with the NZ public and bring them back from the dead.

Bank of England bullish on the survivors of the crypto crash.

After a period of uncertainty that followed a major rout of the cryptocurrency market, digital assets seem to be on the road to recovery, with the United Kingdom’s central bank comparing the crash with the burst of the dot-com bubble.

Specifically, Bank of England Deputy Governor Jon Cunliffe said the survivors of the crypto market crash could rise to become the technology companies of the future, like Amazon (NASDAQ: AMZN) and eBay (NASDAQ: EBAY) after the dot-com collapse in the early 2000s, Bloomberg reported on June 22.

https://finbold.com/boe-crypto-crash-survivors-could-grow-to-rival-amaz…

Oil prices... That was a particularly good OddLots episode (and the competition is tough). The thing that is being missed though is how OPEC are using their increased market dominance.

Basically, OPEC love oil prices at $100+ - big money for them and easy for OPEC to hold the price high when Russia are out of the picture. BUT if the US oil companies step up production and / or Russia gets back online, then prices will start to drop. When they do, OPEC will *drop* the price to sub-$70 and all of the US companies will start to lose a tonne of cash and production will fall and investors will bail.

We have had one cycle of the above - and that's why investors are staying away from expansion. The fix is in. They can see it.

I am no fan of the oil companies, but those who are determined to destroy the fossil fuel industry asap without regard to the consequences, have a lot to answer for.

It should be obvious to even the most committed Greenie that the transition to a carbon free world cannot be achieved without fossil fuels. We will need much more mining of essential metals and minerals and guess what? the mining of them will require fossil fuel energy.

Once voters begin to understand this, much of their enthusiasm for green energy will disappear-and quickly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.