Billions of dollars invested by hundreds of thousands of KiwiSaver members will be shifted to new funds on December 1.

The Government has completed its seven-yearly review of default KiwiSaver providers. It has effectively chosen to push out the large, mostly Australian-owned incumbents to make way for New Zealand fund managers.

Four existing default providers have been reappointed: BNZ, Booster, BT Funds Management (Westpac) and Kiwi Wealth.

Two additional New Zealand-owned providers have been selected to become default providers: Simplicity and Smartshares (NZX).

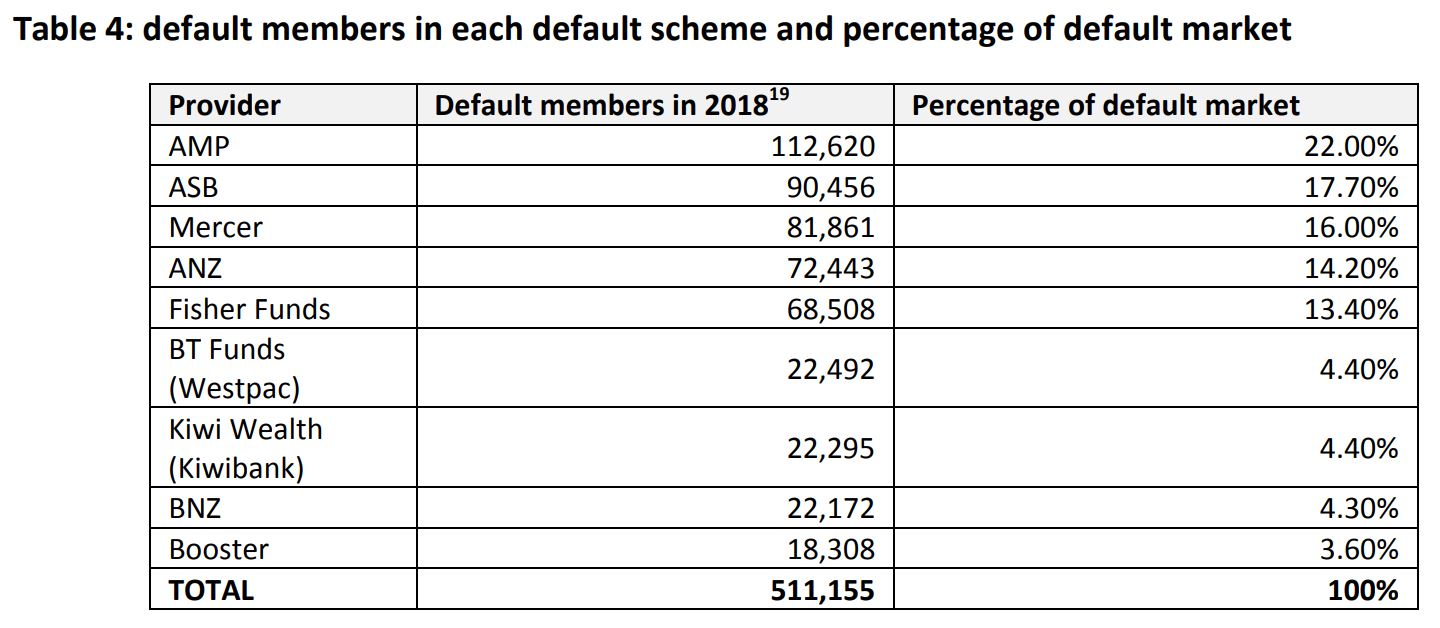

And five existing default providers have been ditched: AMP, ANZ, ASB, Fisher Funds and Mercer.

The change will be seismic. Around 83% of people invested in default KiwiSaver funds in 2018 were invested in AMP, ANZ, ASB, Fisher Funds or Mercer funds, according to the Ministry of Business, Innovation and Employment.

Some of these KiwiSaver members chose to invest in the default fund, while others were put there because they didn’t make a choice.

The people who didn’t make a choice will be shifted to one of the six new default funds on December 1.

Interest.co.nz doesn’t know how many people will be moved, but it does know that about 381,000 people had $4 billion invested in default funds, because they hadn’t selected a fund, as at March 2020.

If around 83% of them are invested in funds with one of the big five providers that will lose their ‘default provider’ status, 316,000 people and $3.32 billion will be moved.

But wait, there's more

The Government last year decided that as of December 1, all default KiwiSaver funds need to be ‘balanced’ rather than ‘conservative’. In other words, a default fund needs to be slightly higher risk, higher return.

So, all the default KiwiSaver members who will be shifted to new providers, will have their funds invested in balanced funds.

Meanwhile, members invested in default funds with managers that have been reappointed ‘default providers’ will have their investments shifted from conservative to balanced funds.

So fund managers will be trading a whole lot of cash and bonds for equities.

MinterEllisonRuddWatts law firm partner, Lloyd Kavanagh said the scale of the shift could cause “significant” price volatility if poorly managed.

“As yet, we have not seen the detail of how Government envisages that this transition will take place and over what time period,” he said.

Fees the focus

While a great opportunity for the new default providers, the change is a slap in the face for AMP, ANZ, ASB, Fisher Funds and Mercer, which confirmed they applied to have their default provider status renewed.

However, it’s important to note these fund managers will still continue to service KiwiSaver members who have actively chosen a fund to invest in.

The Government said proposals were assessed against a set of criteria, which included a 60% weighting on fees.

The remaining criteria included their ability to deliver the investment product (including a new requirement to exclude investment in fossil fuels production), manage transitional arrangements, provide a good customer experience, and the provider’s organisational structure and financial standing.

Finance Minister Grant Robertson said New Zealand ownership wasn’t part of the criteria.

Both he and Commerce and Consumer Affairs Minister David Clark hoped the low fees the new default providers have committed to will put competitive pressure on other KiwiSaver providers to lower their fees.

The Financial Markets Authority is requiring managers of KiwiSaver and other investment funds to meet quite prescriptive requirements to show they’re providing value for money.

Below is a table showing fee changes. Fees are calculated as a percentage of a member’s balance over a year. So, someone with a $10,000 balance, who is charged a 0.3% fee, will pay $30 over a year.

| Provider | New fees | Old fees |

| BNZ | 0.35% | 0.50% |

| Booster | 0.35% | 0.38% |

| BT Funds Management (Westpac) | 0.40% | 0.47% + $1.83 monthly fee |

| Kiwi Wealth | 0.37% | 0.52% |

| Simplicity | 0.30% | |

| Smartshares (NZX) | 0.20% | |

| ASB | 0.40% + $2.50 monthly fee | |

| ANZ | 0.44% + $1.50 monthly fee | |

| AMP | 0.39% + $1.95 monthly fee | |

| Fisher Funds | 0.52% + $1.95 monthly fee | |

| Mercer | 0.47% + $2.25 monthly fee |

36 Comments

I guess the takeaway is the government wants to make it mandatory for all Kiwisaver members to take on even more risks and prop up the share market in NZX with the fund providers sharing the costs.

This comes at a time when the equity market is probably at the peak- how thoughtful and caring.

The real takeaway is that the previous default of sticking people in a low risk, low return fund for their retirement savings was crazy. Dooming those with little financial literacy to sub-standard returns and a poorer retirement. The chance of a conservative fund outperforming an aggressive fund, or even a balanced fund as proposed, over a period of decades is essentially zero.

The only caveat is that since previous governments have set up kiwisaver to help prop up the property market by allowing members to draw on their retirement savings to fund a house deposit, some people do have shorter time horizons and should invest conservatively.

I strongly believe our Kiwisaver should be "No Exceptions" - except - for the house deposit exception.

Because, house ownership is vital at retirement. It's the best thing you can have.

It's a tricky one. I agree owning makes life simpler once retired, so long as the mortgage is dealt with or at least small. On the other hand, the ability for everyone to draw on their retirement funds and various government grants to buy their first house adds fuel to the fire and has helped push up house prices.

Maybe we're moving towards a happy middle ground where the government actually takes effective steps to make housing affordable and increase supply, in which case the kiwisaver fuel may not ignite in quite the same way.

Forcing this change when markets are so highly priced ??

It's difficult - imagine if they had made the change in 2008 in the depths of a crash. Best possible time to do it, but the media would have give crazy about the government forcing people to invest in such a beaten up asset class. When markets are cheap noone wants to invest in them because they are scared worse will come.

Yeah, I think they may have read the tea leaves wrong.

MinterEllisonRuddWatts law firm partner, Lloyd Kavanagh said the scale of the shift could cause “significant” price volatility if poorly managed.

Given the blunt way Labour handled the reselection process, it doesn't bode well for the handover. Perhaps this will be a mini black swan event that shows how close to the edge our markets are in this economy. $4b in the global scheme of things is tiny, but if our markets grind to a halt as a result it will undoubtedly unnerve the larger ones regardless of the reason. FUD is contagious after all. It would be ironic in the face of trillions being printed in the name of QE if $4b of real savers money was the catalyst that led to a global black swan. Time to get out the popcorn and wait and watch.

Fortunately I'm with none of the new ones as the directive " (including a new requirement to exclude investment in fossil fuels production) " is a Labour party sop to CC

The Government last year decided that as of December 1, all default KiwiSaver funds need to be ‘balanced’ rather than ‘conservative’. In other words, a default fund needs to be slightly higher risk, higher reward.

NZ bank depositors face more risk for virtually nil rewards while banks reap obscene profits with virtually no capital risk exposure.

According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

Overvalued stock markets are much the same in terms of risk profile.

The idea that “low interest rates justify high stock valuations” is really a statement that “low interest rates justify low expected stock returns as well.” Those high stock valuations are still associated with low prospective future stock market returns.

Worse, the notion that “low interest rates justify high stock valuations” assumes that the growth rate of future cash flows is held constant, at historically normal levels. If, as we presently observe, interest rates are low because growth rates are low, no valuation premium is “justified” by low interest rates at all.

Presently, the combination of record low interest rates and record high stock market valuations does nothing but add insult to injury.

...the iron law of investing is that a security is nothing but a claim on a future stream of cash flows. Valuation is a crucial determinant of long-term returns. The higher the price an investor pays for those cash flows today, the lower the long-term rate of return earned on the investment..

The corollary is also true. The lower the long-term rate of return demanded by investors, the higher the price moves today. So clearly, changes in investors' attitudes toward risk will strongly affect short-term returns. If investors become more willing to take market risk, it is equivalent to saying that they are demanding a smaller risk premium on stocks (that is, a lower long-term rate of return). Prices rise as a result. Now, the fact that current stock prices are higher also implies that future long-term returns will be lower, but that's part of the deal. Courtesy of Hussman Funds

Good to see that you seem to consistently know what I'm saying. :)

This is a new big fat tail conjured to pile onto the established fat tail.

The new operation will probably need something close to a 4x returns compared to the conservative funds to justify the change.

I'm not sure what you mean by new operation, but assuming you mean balanced Vs conservative fund types 4x is clearly not achievable. Over the past few years of strong equity returns, aggressive funds have returned something like double that of conservative, with balanced somewhere in between.

Over the long run, you can expect an extra percent of two per annum by making an aggressive decision, assuming you don't panic and sell in a crash. If you've ever played with compound interest calculations over 30 or 40 years you'll be well aware a percent of two a year is an enormous advantage and will make a real difference to the quality of your retirement.

May trash the share prices unless funds start selling their shares gradually now and artificially boost them as new providers buy those and more come December.

Providers do need to make a profit. How long before Kiwisaver funds become unprofitable through lack of attention to their management and few want to even bother.

Should of had NZ ownership somewhere in the weighting

I’m not sure if I’m going to get moved or not. Pretty sure I went default all those years ago and that just happened to be my bank which is handy. Since then I have changed to growth from conservative. So does that make me not in a default fund? If so all the losing default providers will be ringing round encouraging people to change fund type and the number being switched may be a lot less than expected.

JJ

That is my understanding also.

You bank still has a scheme, and you can decide to be there. Even if you are transferred, you can come back.

But it's a good time to decide.

I would avoid a big bank. Too many interfering interests to be sure they are seeking the best for your money. .

JJ, the change won't affect you, as you moved out of the default fund into a growth fund.

The Government is going to make $$$ out of this as well. Higher returns on the Balanced funds = more tax from the interest.

One thing is for certain, staff of the five ditched fund managers will be burning the midnight oil and working weekends up to December 1 writing to their default fund holders convincing them to transfer to one of their own other funds. AMP for instance is not going to let 112,620 current customers simply walk out the door.

so why wouldn't they have done that previously?

Kiwisaver is still a dog. Never liked it from the start and opted to pay off an extra $50 a week on the mortgage instead. Looking back I made the right choice in paying off the mortgage earlier, zero risk and guaranteed returns.

The pure mathematical returns would have been significantly higher from kiwisaver, with possible employer matching, government contributions, and returns for the last decade or so much higher than mortgage reduction could have got you. There may have been psychological benefits to being debt free, each to their own. I do both, overpay the mortgage a little each week while contributing enough to kiwisaver to get all the benefits.

Pity National removed the mortgage deferral option from KiwiSaver.

You forgot to add the word theoretical. The pure theoretical mathematical returns.....

No I didn't, I was talking about past returns. The markets have done extremely well since kiwisaver was started in 2007 and you've left money on the table by avoiding it. I'm sure you have your reasons and maybe the psychological benefits outweigh the financial costs, but the numbers are pretty clear.

Interest rate at the time for me was 8.6% so that's a pretty decent guaranteed return in the form of money I did not need to repay. Yes psychologically I was never going to give my money to someone else to manage, for me KiwiSaver was like a tax. Maybe if I was much younger it would have been a go, but for me there was no point in it.

With employer subsidy, every dollar I put in gets an immediate 60% return.

If you avoided that to instead pay down debt at 9%, and don't see how this cost you, you've got some learning to do.

Sure thats why I was able to retire at age 48 mortgage free. Must have really stuffed up somewhere, maybe it should have been age 45.

duplicate due to site cloudfront error (next time I will copy error code, today no)

It is incorrect to assume an employer subsidy exists at all as many companies simply took the "employer subsidy" out of the employees pay changing it from money the employee could have more choice in where and how they invest to less money in hand with less choice. For instance for many investing that money in security for hardship and redundancy would have been better because kiwisaver will not offer hardship support in most circumstances until after you have become homeless and destitute (not preventing it or you from losing your home). Better to be able to choose where you invest your money than the employer skimming it to make up for the required "contribution". You seriously cannot count a pay deduction as part of the return as anyone would still have that value to invest without kiwisaver.

David Clark pulling yet another swifty on the unsuspecting public

I think it's a good move. Noone is forced to change anything, fees are being reduced, and defaults are becoming more appropriate.

As before, you have complete control over which fund you invest in.

This would be sensible if it also accounted for age of investor. Hopefully anyone close to retirement will realise the risk and make decisions that are right for them. If they're in a default scheme now they're probably better off staying there whether ir not it was an active choice so may need to change.

For Kiwisaver to be a real incentivised investment vehicle tax concessions would need to be part (with eventual super means testing at the back end). Flat taxing it would also eliminate the ridiculous situation where an investor gets penalised if they underestimate their PIR but cannot recover an overestimation.

"Billions of dollars invested by hundreds of thousands of KiwiSaver members"

This is the same misunderstanding I've just been listening to on Morning Report - in their case, rabbiting on about 'investors'.

Lets be very clear: dollars are merely markers, debt-issued. If there ain't anything on the shelves, a dollar is worth nothing. And it's merely digital tokens we're talking about, not some guaranteed ear-mark of some future resource or energy-supply.

Secondly, investment isn't putting something in; it's an expectation of taking something out - that something being 'more'. So the combined bets have been of an ever-bigger tomorrow, indefinitely. That cannot be had (you can never have unfettered growth within a bounded system). So as the opportunities diminish, the bets become more risky. Had to happen.

I've never joined - preferring to purchase what I expect to need in the future, now. Before those shelves empty. There are going to be some very grumpy people, when they realise their bets were on the wrong horse(s).

The last thing KiwiSaver members need is for politicians to micromanage our funds. KiwiSaver providers are meant to make independent investment decisions in order to maximise returns. Politicising these decisions will ultimately result in lower rates of return.

Once the Government starts sticking its nose in, where does it stop? Will KiwiSaver providers be barred from investing in, say, meat production? Alcohol? GMOs?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.