The Reserve Bank is giving banks seven days notice that it plans to remove loan-to-value ratio (LVR) restrictions on their residential mortgage lending for at least a year.

The move is in response to the economic downturn caused by the COVID-19 pandemic. LVR restrictions are limits on banks to reduce the amount of low-deposit mortgage lending they can do. (The details on where the limits are set are at the foot of this article).

The Reserve Bank says LVR restrictions are aimed at reducing the risks to financial stability from a severe correction in house prices. The restrictions were introduced in October 2013 in response to high levels of high-LVR mortgage lending, with policy settings adjusted since as risks have evolved.

"The current economic conditions resulting from the COVID-19 crisis have caused the Reserve Bank to consider the removal of LVR restrictions, given the counter-cyclical nature of the LVR policy. This action will also avoid any uncertainty around the implications of LVR limits from the mortgage deferral scheme. It is important that banks continue to provide support to borrowers during these extraordinary times," the Reserve Bank says in a letter to banks.

"The Reserve Bank intends to remove the LVR restrictions for a period of one year, until 1 May 2021. We have not yet determined what, if any, LVR limits will be needed in the future. This will be further considered ahead of the end of the 12 months, and will be consulted on as necessary."

Reserve Bank Deputy Governor and General Manager of Financial Stability Geoff Bascand says as is normal for changes to macro-prudential measures, the regulator is consulting with banks on its proposal, for seven days.

"Feedback will be collated from industry stakeholders over this period and a decision will be made promptly after that," says Bascand.

"The change, if effected, will be made via a change in bank Conditions of Registration. If the decision is made to remove the restrictions, the Reserve Bank will monitor lending activity and feedback from retail banks over the next 12 months as the economic impact of the COVID-19 pandemic becomes clearer. After that period, we will review whether to reinstate LVR restrictions. This provides banks and customers certainty that no further changes to LVR requirements will be made for at least one year."

LVR restrictions apply to new high-LVR loans, and not retrospectively to existing loans. Existing borrowers are only affected if they want to take out a top up loan.

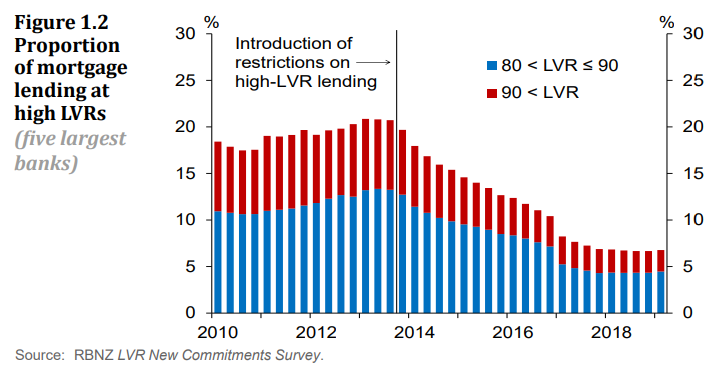

The chart below comes from the Reserve Bank's May 2019 Financial Stability Report. At that time the Reserve Bank said LVR restrictions had been in place since 2013 to address the risks associated with high household indebtedness and stretched house prices, and had made households and banks more resilient to financial shocks.

The details of the current LVR restrictions, as set out by the Reserve Bank, are below.

Investor loans – 30% deposit / 5% of investor lending

LVR lending restrictions are tighter for investor loans due to the higher risks associated with this type of loan. The current policy classifies investor loans as high-LVR if they are more than 70% of the property’s value, and restricts high-LVR lending to no more than 5% of a bank’s total new investor lending.

Owner occupier loans – 20% deposit / 20% of owner occupier lending

This class of loan is for borrowing secured against owner occupied property. The current policy classifies owner occupier loans as high-LVR if they are more than 80% of the property’s value, and restricts high-LVR lending to no more than 20% of a bank’s total new owner-occupier lending.

Special cases

There are some exemptions relating to borrowing to build a new home, for non-routine repair work (e.g. fixing leaky homes) on existing properties, bridging finance, refinancing of existing loans, shifting loans from one property to another (provided the total value of the loan does not increase) and loans made under the Housing New Zealand Mortgage insurance scheme (including Welcome Home Loans). The construction exemption covers any loan for a residential property purchase under the government’s Kiwibuild programme. In addition, borrowers with owner occupied and investment property collateral can use the combined collateral exemption to obtain finance up to 70% of the value of the investment properties and 80% on their owner occupied property.

235 Comments

Wow that is crazy.

As I said many times in the past 30 days, insanity is the new normality.

Agreed. I guess it allows banks to not trigger low and dropping equity thresholds. Will be interesting to see if this leads to the usual suspects leveraging up further.

I think you have nailed it there averageman.

You've pinned that tail right on the donkey (ass) averageman.

This is literally saying to FHBs, 'we have a very big, powerful and fast train inbound, please go an stand on the tracks and see if you can slow it down a little so the rich can clear the tracks' (i.e. property investors can get a good exit price from the market).

They are actually willing to use FHB as cannon fodder. Completely and utterly unbelievable. If the 'have nots' didn't know their place in society before this, they do now.

It's just a clear signal the RB has no understanding the new BAU, is different to the old BAU?

This part is even more crazy, once they drop LV Restrictions they can't suddenly put them back after a year otherwise that will cause lots of mortgagees : "The Reserve Bank intends to remove the LVR restrictions for a period of one year, until 1 May 2021. We have not yet determined what, if any, LVR limits will be needed in the future. This will be further considered ahead of the end of the 12 months, and will be consulted on as necessary."

So within the space of a month or so the capital ratio requirements have gone out the window with LVR's as well.

It's basically like the captain of the titanic saying we're taking on water, man the life rafts but limit seats to investors. Normal safety procedures no longer apply. Give the lower classes a chance to enjoy the upper decks, but only from the bottom of the Atlantic once its confirmed there's no hope of staying afloat.

Incorrect, LVR limits only apply at loan origination. Once you're in the club, you get to stay there, so long as you keep paying your martgage.

Not if you need to switch lenders to get better mortgage rates in the future.

except you won't, because you'd be in their high risk bracket, and they'd want to charge a premium for that.

This stimulus.. largely fear based on his RE driven believe/force to believe, maintain. Can it save Airlines? jobs? Tourism industry etc? .. now, that's how that becoming crystal clear for NZ public - in this worldwide eventuality? NZ as being ushered into F.I.RE economy by neoliberalist the past 30 yrs, into economy which rely heavily on RE, RE is the petrol/oil for the engine.. need to be kept, re-ignite to keep on moving. Sadly, when the bugs carried havoc.. those in the car will jump out leave, or stay dead. RE by any NZ authorities will be the the key answer to 'stability' proper R & D, Healthcare systems are all below RE, so?.. all of you young professionals? .. get out of NZ while you can.

.

Hey Yvil this must be a silver lining for those FHB without a large deposit and still in work. They can now buy a first home on extremely low interest rates and give the landlord the flick. Imagine buying a 500k home and it costing approx 3 to 400 pw in interest.

https://www.rbnz.govt.nz/news/2019/05/lvr-restrictions-promote-financia…

“By improving the resilience of both households and banks, LVR policy has played a useful role in promoting financial stability during a period of heightened housing market risks,” Deputy Governor and Head of Financial Stability Geoff Bascand said.

Why are you removing it now, at a time of heightened risk? Makes no sense whatsoever.

“Macroprudential policy is not about eliminating risks for banks and households, reducing house prices, or managing the business cycle. Affordability pressures on the housing market and the rental market require a much broader policy response,” Mr Bascand said.

If it's not about managing the business cycle, why are you now removing it to manage the business cycle? RBNZ are crooks and liars.

LVRs were supposed to protect banks i.e. if there was a big drop in prices then they wouldn't have bad debt (customers owing more than the house is worth). I don't understand why LVRs should be removed now? It seems to keep house prices up.

I'm not sure it will make much of a difference. Banks would be mad to be lending at >80% LVR at the moment. I suspect the change is to address home-owners who's LVR is about to increase by virtue of a fall in 'V'.

Banks may not offer 95% or 100% but the V in LVR doesn't affect the matter as it is around new loans only.

Does it apply when you go to re-fix your mortgage?

No, never has. Valuations are only for credit events, like top ups.

Banks may not offer 95% or 100% but the V in LVR doesn't affect the matter as it is around new loans only.

Can you clarify, where does the article state that banks may not offer 100% mortgages?

The article didn't say that I was just saying that banks may not or they may - that's true.

The only purpose of this is to keep house prices up. Why? Vested interest. There is no other logical explanation. The RE 'industry' seems to have more power than anything else in NZ now.

At first it seems crazy to remove LVR's at a time of crisis as they have been setup to protect banks in the first place. The reason why the RB is going to remove the LVR's now is to keep banks lending and avoid mortgagee sales. The effect of house prices dropping too much would not only be catastrophic for FHB who bought recently but it would also exacerbate the downturn and affect absolutely everyone

Fully agree. It flies in the face of the alleged reason for having them to begin with! RBNZ conveniently forgets to mention the RWA rating of low depo loans remains high, so still consumes a lot of capital

..RWA rating of low depo loans remains high, so still consumes a lot of capital

{kind=link}

Does it apply to the four Australian banks using the internal calculations model subject to RBNZ pre-approval, which ANZ previously chose to ignore?

Internal models will still attach higher risk and higher losses given default on higher LVR loans, relative to low LVR loans. This is part of the RBNZ approval process.

The ANZ and others received their own letter version from the Mr Bascand

"21 April 2020

[Version for all registered banks subject to LVR restrictions, ie all except ANZ branch, Bank

of China branch, CCB branch "

Quite right.

But there's something morally reprehensible in allowing citizens; encouraging them even, to take on debt that would otherwise be unplayable.

What matters is that current and future loans can be serviced and repaid.

Any drop in value is just figure work for anyone that can still make their payments; the current 'value' is unimportant in that regard, and repayment capacity should be the ONLY basis of extending debt .

Banks have the flexibility to vary current lending terms to accommodate any stressed borrowers. If that can't be done, then they should be 'let go'. Replacing them with a borrower on 'worse' LVR terms makes no sense other than to make the risk situation - worse.

If our 'stability' relies on a limitless access to debt, is it really stability? Maybe it's time to find the new equilibrium, an actual stability. Propping up the current virtual 'stability' is getting very very costly.

Com'on Courtjester, look at the whole world since the GFC, yes the economic stability fully relies on ever more debt. Your moral compass seems to blind you from this blatantly obvious fact. Now please note I'm not condoning it, I'm not saying it's right or good but it most certainly is the case and continuously expecting it to change is being foolish. Do you think this is the last "contribution" towards debt from the RB or government, I certainly don't. There could be plenty more including Helicopter money etc...

You used to point out quite often that I'm a pessimist (DGM even). But I must clearly be an optimist to be surprised by such developments. I have faith in humanity (just look at how far we've come with regards to renewable energy in a decade). I believe that at some point someone powerful and wise will make a bold decision and take a step sideways instead of pushing the ever growing rock of debt uphill.

The sun is coming out and the self licking ice cream cone is feeling the heat....won't take long for it to melt now.

Hahaha

House prices are going to head South, it is a surety. This is desperation from the RBNZ.

Well I guess there is also the 'financial stability' aspect of the RBNZ's role.

A 20% house price crash would not be good in that respect...

What is happening Fritz, from not seeing eye to eye at all one year ago, we seem to agree on a multitude of aspects now. lol

Ha ha. Brothers in arms. Maybe it's my Swiss ancestry coming through.

Do you have Swiss ancestry? If so where from?

Lausanne. On my mother's side. Her grandmother.

So quite far back.

Bizarre new world where even you too agree.

Thanks for the entertainment guys!

"Well I guess there is also the 'financial stability' aspect of the RBNZ's role.

A 20% house price crash would not be good in that respect.."

From memory, the RBNZ stress tests in November 2017 indicated that the banks had sufficient capital where unemployment reached 11% and a 35% fall in house prices.

Can't see a more recent published update than stress tests undertaken as at November 2017.

See page 5 for assumptions:

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Bulleti…

FYI, a 35% fall in house prices in Auckland from the November 2017 median household price of $880,000, would be $572,000 (approx 40% from the recent median household price of $950,000)

The unemployment rate might surpass the RBNZ stress test limits. Unclear if all the fiscal stimulus will keep unemployment below stress test levels of 11%.

Banks. The RE industry and specuvestors are just transactinal activity around the outside of debt.

" After that period, we will review whether to reinstate LVR restrictions. This provides banks and customers certainty"

Cool! But which customers is it giving certainty to?

Hop into the market today at 100% LVR and then try to sell to The Next Buyer down the track at 80% LVR!

What could possibly go wrong.....(Another idea to add to the long list of "They have no idea what they are doing!")

Madness. The pumping must continue, no matter the cost.

The house is on fire. RBNZ proposes dumping a truckload of oil on it.

Someone needs to take all that oil they can't even give away

Right? Crazy how the world can turn upside down in just a few weeks.

Off topic I know, but West Texas for May delivery costing oil companies $30+ to get rid of. I'm expecting a healthy cheque, next visit to the pump! ;-)

While we’re at it, I saw it at USD -38.31 this morn. Tried to buy a million barrels in my IB acct. No joy, sadly.

Virgin Airlines Aust just imploded.

And now our banks are going to make it easier to buy sinking assets, therefore for FHB to lose their equity. Cool!

RB said some time ago they would do whatever it takes to support realestate values this is further proof if any was required to do just that . No realestate price drops in nz does this apply to residential only what about commercial and industrial they may as well go the whole hog and support farms as well no lvr on farm purchases either .

And at the price of a zero bound Barrel of Oil..., they can afford too....well they could afford to if it was not Taxed quite so much in New Zealand......rip-off the customer to our Benefit....systems.

Now even RBNZ is planing to remove loan to mortage restriction and this is in situationwhen many are losing their jobs and business.

Attitute should be like RBNZ as who cares as long the bubble created is sustained (though not possible this time by throwing any amount of easy and cheap money) and banks should be more carefull but they too may go overboard as are playing with deposit and money of average kiwi in case of going burst.

Question to be asked is this the time to be more realxed or vigilant to give easy loan and create more risk.

Here we go.

Everything will be done to stop the crash of the housing ponzi.

That's why I think it will 'only' fall by about 10%, overall (some places more, some places less).

1) Unemployment gets over 10%

2) Unemployed people can't pay their mortgages.

3) Distressed owners ask for a mortgage holiday.

4) Mortgage holiday ends and they are still unemployed.

5) They (or their bank) try and sell their house. Many more sellers than buyers. Result: big house price drop.

6) The process self-feeds

7) Result: house prices decrease by at least 20%, maybe more in some tourist spot

Note that there is no LVR easement, nor QE, nor zero interest rate that can change any of this. At the end of the day, the housing Ponzi scheme ultimately sucks on the real economy. Real economy in trouble -> housing Ponzi scheme collapses. No financial trick can avoid it, just maybe spread it a little bit through a longer period.

Agree - 'at the end of the day', if GDP starts dropping, our mortgage servicing ability across the board falls, and with mortgages at rock bottom, it only means one thing....and government/reserve bank can only do so much to support prices...

And the insane thing about all this is around the RBNZ mandate around stability - yet their policies create the instability. Madness.

Only politically acceptable (acceptable to some) solution to your example is banks don't force sales and instead write off loans or govt buys loans. Banks don't want forced sales and govt don't want more homeless people.

Could be an opportunity for govt to step in take over loans and facilitate transactions between desperate sellers and renters. Ninja loans though.

Shit just got real alright.

"The LVR policy is aimed at reducing the risks to financial stability from a severe correction in

house prices. " RBNZ 21/04/2020

Clearly a severe correction is the RBNZ base case.

Exactly. Banks going forward will tend toward lending only to those employed in what they perceive to be stable employment. Government jobs being the most likely candidates.

But given that the top echelon just took a 20% paycut, surely that will make its way throughout the whole public sector in time (if not more?). So isn't that a 20% drop in mortgage servicing ability for the sector - essentially removing any change to LVR?

My impression is banks more concerned about equity than servicing now. Total turnaround.

That's exactly the case now - sixty percent of bank lending is extended to the creditworthy one third of households for the purpose of speculative residential property investment.

Yes, and by severe correction we are not talking about 5 or 10%, we are talking about 20% (or more in some areas).

Careful we don't just feed yet another investor feeding frenzy again and push the lower quartile property prices higher increasing un-affordability and even higher debt levels on balance sheets

Interesting to see where this goes... I think a simpler solution would be to offer targeted LVR exemptions for those who need it if house prices decline below owner equity levels

Yes I agree, but I cant see an investor feeding frenzy: some investors might survive and few ones might even thrive, after some pain, but many will go belly up.

Agree with you... there are many investors were already thinking of selling due to new rules. This is for recent borrowers, many of Jacinda's voters who believe in her almighty superhero powers.

It's a bit like the lockdown though... easy to get into, how the hell to get out. Do we revalue all the properties later... how? Who pays for that? Can see a frenzy for registered valuers later.

No other option if shit goes pear shaped but full govt bank bailout guarantee now. Can't see any alternative if that's where it's going.

Then presumably we'll sort through the wreckage later, assign appropriate values in relation to lending and altered income so no one loses money and is hard done by, everyone's happy, Jacinda gets her votes and life goes on!

Simple.

The other option is a massive unprecedented Jacinda vote winner full scale debt jubilee for all. I may even change my stripes and vote for that.

That would be prudent and you'd think banks have a buffer to be able to offer that if needed.

RBNZ can remove the LVRs if it wishes - however will banks be prepared to lend on 5% or even 10% equity with high levels of uncertainty in both the housing market and employment.

Of course taxpayer will bail them if anything goes wrong

Note the consultation. "Stakeholders". Well I'm a stakeholder as I'm a tax payer. I want my voice known.

THIS PROPOSAL ALLOWS BANKS TO SELF GOVERN LENDING. THE PROPOSAL IS CRIMINALLY NEGLIGENT.

NO OTHER DEVELOPED NATION ON EARTH HAS THIS REGIME AND FOR GOOD REASON, BANKS BLOW UP WHEN CREDIT EVENTS OCCUR.

DONT PUT THE TAX PAYER AT RISK TO PROP UP THE HOUSING MARKET.

You need to use a larger font.

My largest font would read.

"and you propose this with ZERO DEPOSIT INSURANCE ???!!! "

I obviously have not made myself clear .

What I meant was - " you need to use a larger font - that would teach them. "

apologies for shouting, this made me quite upset.

You're right to be upset. A big part of our problem as a nation, is that we don't get upset enough, and we rarely let it spur us into any real action.

Just suck in the first home buyers, this is corrupt. Do they give a us a guaranteed low interest rate too?

well .. actually they kind of do .

And why would a bank give anyone a risky loan when prices are falling and dole queues are climbing?

As the late great John Clarke said - you don't need to repay debt, just service it, otherwise you haven't got a loan at all.

Brilliant ........and so true !!

Priceless clip.

Is this like relaxing the Building Code during an Earthquake?

And letting everyone back in.

Yes. It most certainly is.

Hahaha......and they see this as a possible way to restore confidence. Talk about grasping at straws.... clearly the banks solvency is even worse than we realise.

I think it would be worth the entertainment just to see if Banks lend >80% in this market.

WTF!! You could not make this shite up

Wow this makes me so angry, there is no price discovery any longer its all a big joke

This will enable property investors to easily offload their properties. Maybe they should sell their properties to their tenants.

So that the tenants, who have been paying the landlords mortgage during the boom, can then live for years in negative equity. Who would be that stupid.....FHB say 'hold my beer'.

IO

Glad to see you finally recognise "tenants, who have been paying the landlords mortgage" - something I have been posting for some time. :)

Missed your point (if you had one)?

Have another look, it's just before the smiley face

The point is to buy a house, you're better off paying your own mortgage than somebody else's.

The point is to buy several, then somebody else can pay off your mortgage.

Needs to be replaced with DTI restrictions. LVR was only ever going to keep feeding the ponzi.

Good call. DTI of 4x would be the go for speculators.

Amazing to daydream about that, but it's never gonna happen.

Mind-Boggling Stupidity on behalf of the RBNZ

Years ago I read there were over 500 staff at the RBNZ. So now there'll naturally be over 750. And so anyway, you wonder what they all do right? And I wonder, how, with 750 staff, this is the best policy they can come up with. After all the copious meetings, reports, analysis, this is the best they can do.

You may not have much capital to speak of, and your jobs may now be tenuous, but by all means, borrow away. It’s probably fine though as banks on their own will finally be more reluctant to lend to people with low deposits now.

If there was ever a sign that the party is over, this is it.

Are they basically saying, FHB please come and rescue us, but be willing to get completely wiped out in the process?

Is RBNZ a friend or foe ?

Or

Foe in disguise of a friend - more dangerous

WHO WILL BE RESPONSIBLE FOR DEPOSIT HOLDERS /AVERAGE KIWI P, IF BANK DEFAULTS.

Can Governor assure that no such thing will happen as banks will be forced to take higher risk due to competition.

He may resign in such a scenarion but that will not help many who lose their deposit in bank or may be everyone should withdraw cash from their bank in hundreds of thousand dollar and invest in safe deposit locker.

Any advise from experts on interest.co.nz or is this fear unjust.

Government should answere as to who will be responsible for Reserve Bank Governors adventure.

Media should raise this question with government as firing or resigning will not help average Kiwi who will be on road for ni fault of their own.

Does one has right to sue Governor or government as looks that probablity of banks going burst is high now by this action of Governor supported by Labour led Government.

Mainstream media is owned by the banks and RE 'industry'. They will never raise concerns about what happens to buyers in a falling market. That would imply that house prices can go down and money could be lost on property - which, as we all know, is impossible.

I have no answer, just want to add that I find it extremely concerning that the ATM limit went down from $2000/day to $800/day to $300/day in the past few weeks. There's a bank run happening right now.

Can you link to any bank release saying they've dropped it to $300? I haven't heard that and i'd like a source for that claim.

Purely anecdotal, the limit at the ATM I usually go to had $800 last week, yesterday it was $300.

I heard the ASB banking APP broke last night. Some people could sign in however all they could see was their Kiwisaver account balance, no other accounts were showing up.

Could this plausibly be about limiting exposure for workers that have to restock the ATMs?

Yes - interesting that this isn't in the news. Think its more a limitation of physical cash distribution to ATM's rather than bank's concern/s about outflows?

You are probably right there with a small bank run due to lockdown. But there is also the logistics issue of re-stocking machines that also would have prompted a reduction, I am guessing. Everything is going much slower right now, even for essential business.

It is clear that the RBNZ is now assuming what many housing speculators still refuse to admit, in their delusional thinking: the simple, unavoidable fact that house prices will decrease significantly in the future (I guess at least 20% if not more), moving a few owners and speculators near or at a negative equity position. This temporary removal of LVR will allow banks to better support home owners in such a position. It is clear though that housing speculators will be monumentally shafted - I can't see banks supporting them any longer, LVR or not.

The RBNZ should have made this clear, and removed the LVR restrictions only on first homes, though. Supporting housing speculators is the last thing the NZ economy needs right now.

In any case, the removal of LVR should only be a very temporary measure: having strong LVR restrictions in the past few years, and strong capital levels, is what will allow banks to survive this impending real estate carnage. We do not want banks to come out of this in a shaky financial position, just because we were forced to support the fools preaching the self-serving, Ponzian, moronic myth of ever-increasing house prices. They have made their bed, and now they should be left to sleep in it.

(My jaw hitting the floor) I can't tell who is more drunk; the Reserve Bank, retail banks, the real estate industry or me for believing this conduct has been well intentioned all these years! Has the RBNZ shared their modelling on house price values? Surely that needs to accompany these types of announcements. In the absence of that this decision is absolute madness.

Just yesterday a couple of people asked me where I thought house prices were heading…

I answered there was too much uncertainly for me to make a prediction but that basically it was a tug-o-war between the economy tanking, businesses closing down and people losing their jobs vs more and more cheap money being thrown at the problem.

Note, I'm not casting a judgement wether this is right or wrong, good or bad, I'm simply stating what is

Will be interesting to hear of Mr Reddell's take on this.

Wow! "Since there was never a good case for LVR restrictions - something not even Muldoon used - it is good to see the Bank proposing, somewhat belatedly, to remove them for now." https://twitter.com/MHReddell/status/1252359302238490627?s=20

They should be getting sacked and charged for this.

First up against the wall when the revolution comes!

I don't know about anyone else, but I'm rapidly losing faith in our financial system and that worries me very much because of what it means.

Smoke and mirrors! The RBNZ's own data showed the limits were never even being close to maxed. The servicing of the loans is key... which, with COVID19 and responsible lending codes, is still going to be the main inhibitor.

I think I was reading the quarterly notes from US bank Morgan Stanley who indicated that while previously they required 5% collateral they now required 20% as their own guideline. What this indicates to me is that banks themselves will not take the risk.

I feel like this isn’t really going to affect how retail banks lend.

Could you elaborate?

The official LVR might have been reduced but retail banks weren't pushing up against their allowance to lend to borrows of more than 80% LVR to begin with. Previously banks were allowed to do 20% of their lending to borrows with less than 20% deposit, but despite this, only 10-15% of their loans with being made to low deposit borrowers.

Retail banks still will determine their own exposure to high risk mortgages and even in the 'good times', far below 20% of their lending was going to these parties. Just because retail banks can lend to high risk borrowers, doesn't mean they will; and in the current environment I suspect they'll be even less inclined to do so.

I see this move more as a signal that the RBNZ expect property prices to fall and this is a desperate attempt to cushion the fall.

I wish the Reserve Bank weren't independent, so we could vote this current governorship out.

And replace him with who? Would the next in line do anything different? I doubt it.

Max and Stacy

WHAT ON EARTH????

As an aspiring first home buyer I am NOT ok with this. I don't want my friends to be DEEP in the hole because of this.

Aspiring FHBs could have targeted with far more specific relief if needed - even recent FHBs who are still in their first home could have been too. I'm stunned that this is even being considered.

Your comment is the only appropriate reaction to this madness.

It seems a reckless decision at first but I'm not sure it is.

I doubt that the banks will start lending at over 80% LVR in the current environment because it's simply too risky.

So why get rid of LVR's?

Possibly to avoid weak borrowers (many recent FHB's) to be pushed over the 80% threshold if house values fall by more than 10% and avoid them an uncomfortable phone call from the bank? Surely, that's a good outcome

thats my thoughts as well, this is more about keeping people in their houses rather than new lending

which does makes me wonder about the bank stress tests, were they not supposed to measure a downturn of 30%.

But probably not 30% unemployment and or reduced earnings/mortgage servicing ability across the board.

How will it keep people in houses? Restrictions only ever applied to new lending.

if house prices fall by too much it upsets the banks balance sheet so they call in the high leverage loans to balance the books, ask any farmer how hard a bank can become in a downturn they go from friend to foe

House prices falling does not impact a bank balance sheet; loan impairments do, and there may be correlation between impairments, unemployment and eventually house prices - but remember house prices certainly moved up regardless of incomes.

But specifically, how does lifting a speed limit - which was never even pressed against - help house prices not to fall? It's a straw man argument.

If a bank has no credit appetite to lend 90% (especially if today's 90% = next years 110%) then they wont, regardless of a speed limit.

Notwithstanding that higher impairments could = greater risk could = greater risk premiums could = higher interest rates could = higher impairments... hmmm.

Nope, Not relevant, LVR restrictions only apply at loan origination.

This will be about trying to prevent a property market crash. Suddenly the inflated market matters a lot.

WOW finally Labour realises that crashing house prices would cause untold damage -- to those FHB's who bought in the last few years and the huge number of home owners with limited equity - but to keep them propped up they are going to create a whole new group of over leveraged borrowers in a crazy and almost certainly falling market - do they not get that larger property portfolios are much better leveraged and will simply ride out this storm and start picking up even more properties as the chaos unfolds

Ludicrousness of the highest degree

I'm sure you're aware that Labour has nothing to do with the RBNZ's decisions.

when a Ponzi looks like collapsing, the only solution is MORE players

This is bad, while OCR is 0.25% and now there is no LVR restrictions, it's like as long as we can live for now, we can absolutely throw tomorrow away. Feel sorry for the people who've just bought houses.

Can you please tell me which bank offers 0.2% interest, I'd love to take up that offer. Thanks

The RBNZ, But they won't deal with you.

Sorry, I meant OCR got to 0.25%. Got the wrong number. Just made a correction now.

Every bank offers lower than that. To their savers. Thanks RBNZ

Great news, nothing will change as always.

The party is on, all the free drinks are on the table. Some will have a great time, some won’t get much to drink and some will end up with bad hangover.

I smell the desperation, while I sense the opportunity

I give up!

WTF let’s throw some petrol on the fire!

Great news, but banks are going to be quite stingy with new lending anyway.

Banks not taking on any new to bank customers however lending for existing customers may be more likely to approve if things look kinda ok...

Kinda.

Well its a real kick in the guts for a wannabe fhb that suddenly has job security issues if the housing market gets further away from them because of this.

Anyone else get a 6 page letter from John McFarlane (Westpac) recently - basically saying to shareholders that we're in trouble but will do our best even though were all being overpaid so we need more overpaid committees/directors to make change?

As I have always said now for years ..... the PPP - "Property Ponzi Party" ...gotta keep it going at ALL COSTS ! Please note ....ALL costs ....

It can be quite tricky under COVID-19. PPP needs fresh meat to continue, and that fresh meat is immigrants. COVID-19 stops immigration, literally. It will be interesting to see how immigration policies play out next.

The next logical (aka absolutely insane) step would be to abolish the FBB.

Yes they will have sort the supply chain of "fresh meat" as soon as they can, or housing prices may drop.

There will be thousands of New Zealand citizens wanting to return to New Zealand.

And tens of thousands leaving New Zealand. I'm not sure why people think immigration reversal goes only one way.

And going to which jobs?

RBNZ will next allow approval of NINGA loans and will buy them off the banks. Got to keep the property ponzi going.

what the heck is a NINGA loan?

Ninja

No income no job

Ninja.

Manna from Heaven for Many.

"The Reserve Bank is giving banks seven days notice that it plans to remove loan-to-value ratio (LVR) restrictions on their residential mortgage lending for at least a year."

unclear if this is the

1) change in LVR

2) change in speed limit of LVR's

Excerpts from RBNZ - https://www.rbnz.govt.nz/faqs/loan-to-value-ratio-restrictions-faqs

A) What are LVR restrictions?

A loan-to-value ratio (LVR) is a measure of how much a bank lends against mortgaged property, compared to the value of that property. Borrowers with LVRs of more than 80 percent (less than 20 percent deposit) are often stretching their financial resources. They are more vulnerable to an economic or financial shock, such as a recession or an increase in interest rates. When we talk about high-LVR (low-deposit) lending, we are generally referring to someone with less than a 20 percent deposit – or an LVR ratio of greater than 80 percent. For investors purchasing property secured with a mortgage, deposits of less than 30 percent (LVR of greater than 70 percent) are considered high-LVR.

These restrictions provide a buffer in the face of a sharp housing downturn, which would particularly affect highly-indebted home owners and investors.

B) What are the current LVR restrictions?

There are two nationwide speed limits for owner occupier and investor lending. Banks are permitted to make no more than 20 percent of their residential mortgage lending to high-LVR (less than 20 percent deposit) borrowers who are owner occupiers, and no more than 5 percent of residential mortgage lending to high-LVR (less than 30 percent deposit) borrowers who are investors.

C) Why has the Reserve Bank imposed LVR restrictions?

The Reserve Bank introduced LVRs in October 2013 in response to rapid house price growth, especially in Auckland, accompanied by a sharp increase in the use of low-deposit loans. The policy helped to strengthen bank balance sheets and had an immediate dampening effect on housing market activity and house price inflation. From late 2014, upward pressure on housing prices re-emerged, predominantly in Auckland, posing renewed risks to financial stability. Investor lending had been increasing rapidly and was a significant contributing factor to the renewed housing market strength.

A sharp correction in house prices is a key risk to the financial system. A severe fall in house prices could have major implications for the functioning of the banking system and cause long-lasting damage to households and the broader economy. Housing lending makes up about half of bank lending in New Zealand, and a home is usually the single largest asset that a family owns. There has also been a rising incidence of small investors (that are heavily reliant on credit) in the housing market. These factors mean that any instability in the housing market could undermine the stability of the wider banking system and economy.

haw haw ......

Who could have believed oil negative $37usd p/barrel? Now 20% deposit to 0%? Look at council rates, all that money local councils borrowed, and for what? Look at insurance costs. Who would/could buy. I imagine the renters can now hold the balance of power, just to keep average annual costs covered, owners will be desperate to have a tenant. Rates and insurance have been quietly creeping up, and with the euphoria of ever increasing capital gains, no one noticed. The costs of owning a house are not in the owners control, so who would want to buy? Negative rent? Doesn't seem possible,being paid to live in a house? Let's see.

That will only happen if there is an empty house tax. And even if houses value drop to 40% of what they are worth now, there will be rents and buyers and etc. Please note that even for oil, the story is for the American oil not globally. Russia has delivered a massive blow to US fracking industry. It will take years for them to recover from it.

Rates and insurance and maintenance still have to be paid on empty houses.

And how paying someone on top of all those costs will help the owner? But if there is extra expenses to avoid (as will be the case of empty home taxes) then yes: you will pay $100 in taxes (plus all other expenses) but if you pay someone $80 to live there then you will be $20 better off (if you want to keep the house that is).

I remember a time in late 80's, early 90's, when landlords were offering free turkey hamper, 2-4 weeks free rent, electric and gas included. I think that qualifies as paying someone to rent a place. The point being that landlords were competing to get tenants, which equates to sharing the costs of the property, but certainly not making a profit. Don't many landlords today top up the rental mortgage from their own income? (So I've read on here) with capital gains having vanished, unless they can sell, haven't they just become prisoners of their own debt? This is what I mean by paying tenants to rent.

Reserve bank are expecting house prices to tank. This decision is proof that their modelling has scared them. Looks like panic, smells like panic, then it is ....

I think this shows that everyone is scared witless of what is going to come. I agree with people who say this is not intended to encourage new lending (as who on earth will want to borrow and who on earth will lend, regardless of "restrictions" those are needed when there is crazy demand for credit), but to avoid creating a huge swathe of risky mortgages (where the value of collateral is not enough to cover the debt) thus giving the marginal debtors a little bit more space. Not sure if it is going to be effective, but i can see why the RBNZ is doing it.

That's my thought too. Psychology plays an important role in the current property market. RBNZ could have chosen to "ease" the restriction, instead, the chose to remove it completely. It sounds much better.

Could be far less sinister: giving FHBs chance to get one of the upcoming bargains. 20% of a property that’s fallen by 20% to $700k is still $140k. Interest on a $650k mortgage at 3.5% only @$440 a week, cheaper than rent even after rates etc, much cheaper when you take into account the inevitable capital gain.

I was uptick-pondering until I came to "the inevitable capital gain"...

haha and what about adding in principal to payments? Or do FHB's just buy and never worry about paying back that part of the loan?

Well Principal payments are considered compulsory savings I guess? At the end of it you should walk away with a fully paid for home, but you've forgone opportunity cost where Principal Payments could have been put towards investing in shares to generate a far better return.

(Interest+Rates+Insurance+Maintenance?) @ $600 a week + $300 principal payments vs (Rent) @ $450 a week with $450 per week to invest elsewhere.

Good luck inflating your rent payments away though.

In reality it will usually be a well capitalised investor who swoops in - borrowing the full amount.

More leverage to solve a debt problem...extend and pretend. Utterly reckless and misguided from the RB.

FHBs are now being sacrificed at the altar of the property gods - being encouraged to go in at 100% leverage into a declining market. We can only hope that banks themselves provide the handbrake and refuse to lend at such levels.

These were my initial thoughts also Pietro. I thought the LVRs only made it harder for FHB. I think this is to make it possible for those in a secure position to buy a home during the bust to jump the deposit hurdle. It might also soften the blow of the bust to the market a tad. More hands up at auctions...

This move is purely to allow banks to broaden their high income low deposit loans. Banks will not increase risks at this time, only lower them. But it expands the potential base of clients in a diminished environment and will allow some high income earners the opportunity to buy in at a price point they are comfortable with.

I did lay out on this site, the past couple of months as what they need to do to prop up/keep on their home asset valuation, every little bit.. they'll follow it. All? just to maintain their Neoliberal grip manifested in F.I.RE economy.

Next? FHB lowering threshold, OCR down, they're frantically try to maintain this one economic single bar of GDP productivity, removed or lowered further the banks CAR.. RBNZ is try to jolt the zombie economy. In small NZ? this is largely Psychological.. what none of them have control off? - worldwide affairs. NZ duffrunt.

How many on this site get it almost 100% like moi? - OCR down by 75 basis, defer deposit guarantee, defer CAR & capitalisation percentage, suspend LVR, soon lowering FHB (they kind of a bit embarrass here).. as all those parameters directly to hold the F.I.RE economy. Only couple weeks back Orr's stated spend, spend..until this S**t..happens

https://www.scoop.co.nz/stories/HL1507/S00101/the-fire-economy-new-zeal…

https://www.youtube.com/watch?v=MGrBCtOt4Qs

Orr's vested interest on his RE valuations & the rest of ruling elites, economist - all there 'subconsciously' at play

This is probably more about making equity available to households with more recent mortgages (i.e. most likely larger balances, i.e.the most at risk of default), so that they will be able to draw on a LOC to help cushion interrupted household income if one partner is made redundant for example. They probably already bought close to the previous LVR limit. If you give people a bit of room to work themselves out of it rather than force a sale for short term delinquency issues, you're probably doing everyone a favour.

Let's face it, if you have borrowed 7x income and one of you loses your job in an environment where Ue is growing,wages are falling and asset prices are deflating, additional headroom is only going to delay the inevitable.

Well its not a place Id want to be but Im optimistic that given a bit of time most people will adjust, and create better opportunities for themselves. You are right that it might make them think twice next time before backing up the ute to the bank. I think 7x is optimistic too. Banks should only be allowed to use the main breadwinners income in servicing calculations. It used to be like that in the mists of time before markets turned permanently bubblicious.

Very true. I can recall my first mortgage being restricted to 3.5x earnings. Seems a very long time ago.

When I bought 2.5 years ago, my wife (a qualified teacher) was unemployed for maternity purposes. I earn an alright wicket, however due to the responsible lending code the bank wasn't willing to lend any higher than 3 x my salary. Blessing in disguise, as my wife went back to work 3 months later and fast forward today our mortgage payments are <10% our gross household income.

Next comes OBR and a grab for savers deposits to bail out those who borrowed like drunken sailors. Aspiring fhb's should be very afraid. All done under the cover of the old persons virus.

Why does getting rid of LVRs worry so many?

It is what it is, and if you think it will help people, then rip into it yourself!

Why you would be worried when it doesn’t affect you is a bit puzzling?

The fact is that Banks won’t be lending to anyone that they are not happy with.

By the way, I believe prices in many places in NZ will not be dropping, as you can own for less than renting in many places.

This being the case then you would be plain silly if you were continuing to rent with interest rates being so low and for a long time!

Personally will be buying more but not actively looking, as the deals will come to us.

"The fact is that Banks won’t be lending to anyone that they are not happy with."

err, no mate. Banks lending practices are restricted because at times they behave like f*cktards lending money to anyone who fills in a form. That's what caused the GFC. Try watching The Big Short.

"you can own for less than renting in many places."

It's supposed to be more expensive to rent! By a BIG margin ( you, of all people, should know of the inherent risks of being a landlord, and surely, need to be compensated for that in the rent you charge?)

"The Norm' used to be 7% to rent over the equivalent cost of owning. But now, once it's "line ball!" you should rip out and buy! Madness.

Paying 'rent' to a bank as interest or rent to a landlord is no different.

The speculative cost/benefit of 'owning' may or may not be attractive, but given we haven't seen a 'may not' for some 40 years, the odds of that happening ( now?) are getting bigger by the day.

It's still much cheaper to rent than own in higher value, central locations.

The man you are a property BULL so will never believe property is dropping. That is your psychy.

How anyone can believe property will hold when we have just paid out 10 Billion in wages on the basis revenue has dropped 30% is beyond me - never mind the economic carnage unfoldling across the globe, virus or no virus.

The only person who should buy now is the one who has no home and can pay cash.

"Why would you be worried Dif it does not affect you"

Perfect summation of the world view that got us in this mess (debt that is)

Ie: I am all right, sod you

"Why you would be worried when it doesn’t affect you is a bit puzzling?" Because I have a moral compass.

Yikes, economic armageddon is on the horizon but hey FHB, why don’t you mortgage yourself up to the neck. This is insanity!

Shut up and take my money!

This is the simplest for NZ public to understand: South Island being struck again by major quakes, water, food, drinking waters, milk, sanitary products, shelters, medication are all becoming essentials for peoples to survive.

But alas, all of their respective local councils, banded together... open up shop of buying & selling gold bar.

Folks, even Prof. Jane Kelsey stating some of those Neoliberal actors are easily identified to prop this F.I.RE economy. To undo their 'intertwined' legally binded scheme by either red or blue team? is difficult. BUT do ask me on how to undo them 'legally' - you need to pay me for my answer.. ha ha ha.

FFS..... and that middle F is not a word in my everyday vocabulary!

With such a continual gap between haves and have nots, the country has never been more divided. It's not going to be possible to roll out same solution, as back in 2008. Too much of NZ is impoverished. When it comes to the virus, we are all in it together, when it comes to national finances, those that hold high levels of debt are on their own. From 2008 onwards, a large number lost the lot, and in 2020, they're the ones with nothing to lose. It's like a game of othello, the pieces just change colour, just like that. Those in lofty positions are going to find it's a long, and painful, way down.

The central banks are fighting deflation. This is because money (debt) is being destroyed. They need people to take out new loans in order for this ponzi scheme to carry on. It's a game of musical chairs. Now that the music has stopped; some are left standing up.

Money is being destroyed … EXACTLY

There will come a point soon where money holds no value … value will be in what youre holding in your hands

NZ. Make the rich richer and the poor slaves.

Which category do you classify you in?

AO has just stumbled into GR on cuba street and they now both at the strippers dishing out the dollars...im off to buy a G string

I suppose they need to give leeway to banks to continue to prop up the residential construction side of the property market. With consents at all time highs and large developments coming to market, how else would the still employed (over the next 12 months) gain access if they have only had a small deposit? They will be the target of RE and Banks being 'encouraged' (many words could replace encouraged) to get on to the property ladder and take out a 90% - 100% loan.

Developers will be thrilled and relieved. So will councils!

Negative equity .......

https://www.google.co.nz/amp/s/amp.scmp.com/business/article/3080115/mo…

Lol. You didn't really think old man Orr was going to let the value of his multi-milllion property portfolio slide did you?

This is the guy who was busily stoking another property boom with his reckless OCR cuts just a few months ago. Blind stupidity and as crooked as they come.

Financial stability is not letting the debt peddlers pump prices to nose bleed levels in the first place. Not this ambulance at the bottom of the cliff desperation when the property ponzi implodes.

Internet rates are effectively zero. Printing money on unimaginable scale. No deposit insurance. LVR restrictions removed. No DTI. My savings in the bank are being taken for granted.

Thanks Adrian. You've finally motivated me to take whatever cash I have sitting in NZ banks and put it into PMGOLD. The writing is on the wall. Anybody with savings in a New Zealand bank is a sitting duck and is supporting the last gasps of the property ponzi.

RBNZ - Reckless Boomers of New Zealand

Anne Gibson, Tony Alexander, Ashley Church, Bindi Norwell and the rest of the property cockroaches are going to have a field day trying to lure the young and the gullible over the cliff edge with them.

Utter madness. There is no other explanation other than it is self interest. Those making the decisions are looking out for themselves and the value of their property, not applying the mandate they swore to uphold, which is the long term stability of the financial system. Or more importantly, the long term stability of the people they are supposed to represent.

Yes - we need to manage the next 12-24 months carefully or those who feel they have been hard done by may no longer buy into the system they're being forced to live within = riots/revolution.

The petro dollar. USD, global reserve currency. These have now become history. Global financial stability? What we are in now in is GFC 2. The gfc was never "solved", simply postponed, and made all the worse for it. There is a new world order underway, and nations are either going to be a part of it, or be enslaved by it. Like the "rich" masters, that are simply in debt. They are the new slaves. The real wealthy are less than 1% of the population, and they only ever look after themselves. Homelessness, mental health, suicide, poverty, who really cared about these things over the last decade? They wouldn't have continued to get worse if the powers that be didn't want them too. Same now, it's just more of the former "middle class " getting thrown under the wheel, and still, the powers that be will not care. Largely because they are worried, as they always are, that they may lose their own positions.

What's not happening? People buying houses. Who's not creating credit? The banks. Who's suffering? The banks. What are they doing about it? Jawboning the polies & their ilk to their advantage. This is rich & privileged looking after the rich & privileged. The same game as last time. Where's the new thinking? Bullied out of the room by the rich & privileged. Why? Because when you're the rich & privileged you don't ever want that game to change. Perhaps we (the little people) should create a 21st Century guillotine, then they might listen to us?

You are a brilliant communicator. People love you right now. But you also know if Auckland property prices are 20% or more down in the next few months. In September you are toast.

We should elect Chinavirus for PM.

It delivered on the promises to cut immigration and slash house prices that Jacinda reclassified as "aspirational".

brilliant idea: encourage more negative equity at the v time when house prices are most likely to fall.

Why is all this defensive chicanery required for people to try to buy a house?

Because wages are too low and house valuations are too high.

We buy fewer houses than in 2003-4 (in 2019-20, over 12 months)

With around a million extra people and about 15% more stock, at lower interest rates.

Does this look like a healthy market to anyone in policy making?

Really, there is no policy, just more of same of what is not wanted and doesn't work

As somebody already said. It's not a market if prices are never allowed to fall.

Where is tothepoint and THEMAN2 in all of this?? :D

Stroking eachothers egos.

Brock, I personally don’t need to be stroking anything!

At the end of the day, it is up to the Banks as to who they lend to, and they will be pretty careful with it!

They will be taking into account where they are getting the money to service the loan plus age more than ever!

The only reason people will be selling at under what their property is worth is if they are being squeezed like a lemon.

There will be winners and there will be losers just like there always is!

Government needs to stop this insane idea of RBNZ's. People need less debt into the future, not more. Not only will our young adults will now be burdened with servicing a huge public debt but if LVRs are lifted, they'll be burdened with even more private debt. But perhaps government is happy not to intervene as it only seems to care about protecting the politically powerful baby-boomers' property investment values... but that's democracy and the it's the demographic that has the clout to get what they want e.g. Jacinda's "no CGT while I'm the leader..." promise.

My wife and I have secure jobs (permanent contracts for teacher/nurse) and currently have about 12% deposit. We have some credit card debt we are paying off currently (original plan was to look at getting a home next year).

This seems like good news to me. Wait 6 months or so and then jump into a property when they drop? With LVR removed the banks should be pretty happy with our deposit + stable income. I'm aware they will keep dropping but they will surely bounce back and this would be a long term live for us anyway.

Am I being naive? What am I missing here

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.