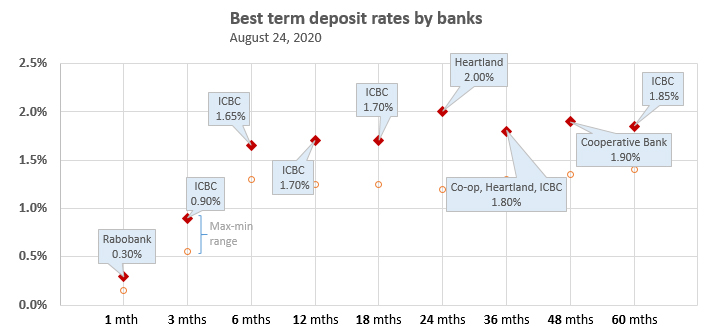

A couple of weeks ago we looked at who is offering the 'best' term deposit rates in this environment of low and falling rates.

Here is an update of that review.

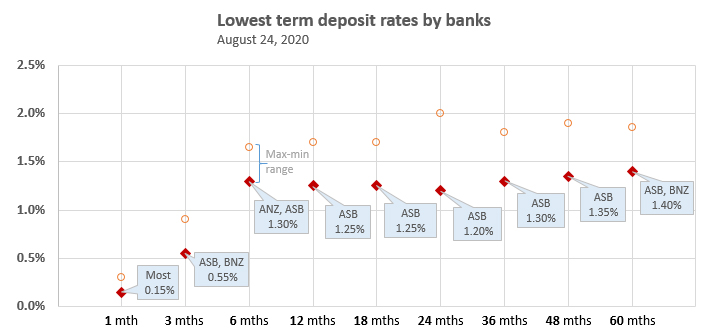

Now we want to look at the bottom end of this market because that is where the most activity is occurring.

The main banks are awash in liquidity and just don't need more customer deposit funding.

ASB, one of the four large Australian-owned banks operating here, made more notable cuts to their term deposit offers, taking them down to record low levels.

Others will follow.

This is part of a 'journey' towards rates that will become effectively zero.

ASB is just the first in a race to lower what they pay savers for term deposits.

We will be getting the RBNZ Dashboard data release next week so we will then be able to inspect a whole range of new data by bank, but it is already clear that bank liquidity is high and rising. And this is at a time lending activity is struggling to grow. More cash than can't be lent out at a margin is a trap for banks. How they respond to this pressure will be important to watch.

And the central pressure they are under comes from the RBNZ. The regulator has clearly signaled that a negative OCR is a likely 2021 outcome. That in turn means severe margin pressure on banks is ahead, and they are now facing up to what they will have to do to adjust to a new, and unprecedented reality.

And that is unlikely to benefit savers in any shape.

Here are the bank net interest margin tracks that are now under threat from the combined pressure of low interest rates, low loan demand and RBNZ signals that the OCR will go negative.

| Net interest margin | March 2018 | March 2019 | March 2020 |

| per RBNZ Dashboard data | % | % | % |

| ANZ | 2.2 | 2.2 | 2.1 |

| ASB | 2.3 | 2.3 | 2.2 |

| BNZ | 2.2 | 2.2 | 2.1 |

| Kiwibank | 2.1 | 2.0 | 2.0 |

| Westpac | 2.1 | 2.2 | 2.0 |

| Cooperative Bank | 2.3 | 2.3 | 2.2 |

| Heartland Bank | 4.5 | 4.7 | 4.5 |

| SBS Bank | 2.6 | 2.5 | 2.5 |

| TSB | 1.8 | 1.8 | 1.8 |

The odd thing is, low rates don't discourage consumer saving. If anything, they encourage it. Maybe it is just the times, but household deposits are rising at the rate of +7.9% per year. Bank lending is up only +6.0% in a year.

But fewer people are bothering with term deposits themselves (-2.1% shrinkage in a year), just leaving their funds in transaction accounts (up +32% and that is not a typo) or very low-returning savings accounts (up +15%). That customer reaction of course enhances bank margins if they don't have to pay anything for customer money.

There is a good chance household deposit levels will grow faster in the immediate term while bank lending struggles to find any growth. It is an environment where there is no chance of "a decent return" for savers.

And for banks, the same future is before them. The chopping of term deposit rates is just an intermediate step for banks as markets price in negative official rates. It is a new future where banks are probably going to have to radically change their business models just to survive. And that will almost certainly not be friendly to savers.

75 Comments

"...just leaving their funds in transaction accounts (up +32% and that is not a typo)"

No surprise really?

As deposit returns lower, transaction portability becomes crucial. ( call it Liquidity if you like)

Who wants to lock in 5-year deposit money at negligible return in case it's needed? (Let's be honest. Just figuring out what's going to happen on Monday is hard enough given the abnormality of society/the economy at the moment, never mind about 5 years time!). Borrow it at those rates? Sure! But not tie it up.

So the lower rates go, the more people will save, the shorter-term they will tie their money up for.

I remember when we bought our house about 15 years ago, the cheapest mortgage rate was the 5 year. Probably the opposite situation- rates were a lot higher so savers were happy to lock those in for 5 years and the bank wanted the security of lending it out for the same term.

Yes, the tail end of people’s 1 year fixed mortgage at 3.x seems a long time to wait for a renewed 2.45% rate. People moving to shorter terms on deposits as well - a 6 month rate at 1% or 3 years at 1.3% - no point.

Hi BW, how do you reconcile Greg's statement:

"it is already clear that bank liquidity is high and rising"

with your claims of a liquidity crisis which will lead to deflation? (again not trying to argue, just trying tounderstand your view)

Yes, also, if you distrust the borrower you tend to lend for shorter periods. It is a highly adaptive response to favour liquidity over return during times of upheaval.

Shift some maturing TDs to a transaction account in order to use some of it up. That's my approach nowdays.

Exactly, it’s happened in Europe but somehow the RBNZ thinks we will get a different outcome? The RBNZ are just late to a pretty shitty party.

Also if you have a look at the interest rate difference between a bonus interest rate savings product and a term deposit its very small. So why lock away money in a TD when you get almost as much return from the saving product and still have the money on tap if you need it? And if you do you'll only lose one or two months worth of bonus interest rather than the entire amount from a TD.

And for banks, the same future is before them. The chopping of term deposit rates is just an intermediate step for banks as markets price in negative official rates. It is a new future where banks are probably going to have to radically change their business models just to survive. And that will almost certainly not be friendly to savers.

Good timing. This week, BlockFi received new Series C funding for their already successful lending venture. USD stablecoins are already paying interest rates of around 8%. For those who understand what it's about, it's a no-brainer compared to retail bank term deposits.

https://www.alleywatch.com/2020/08/blockfi-crypto-finance-products-zac-…

The odd thing is, low rates don't discourage consumer saving.

The government has raised ~$34.645 billion in freshly minted deposits since the end of March 20. Around $14.0 billion has been retained in the Crown settlement account at the RBNZ to fight future covid outbreaks. How much of the balance in the form of government transfer payments has found it's way into bank customers' deposit accounts?

Exactly. The sheeple have no idea as to the extent that they're just pawns in a very big game while others make out like bandits with the spoils of this malarky.

The author has misappropriated the low rates as the cause of savers' encouragement.

This is incorrect. (If I had a beer everytime...)

Savings increase as rates reduce because they are both reactions to an economic environment with great uncertainty and Japanese overtures.

**Unsustainability accelerates**

The odd thing is, low rates don't discourage consumer saving. If anything, they encourage it.

I disagree with this. Low rates are the by-product of the economic reckoning caused by the faltering of the debt-driven economic model (Covid has just hurried things along). Rates have been on a downward path for quite some time and this has not been accompanied by greater rates of savings. More likely the opposite. In the short term, perhaps people have spent less for sure. But NZ is not a savings culture regardless of interest rates. And if attitudes and behavior changed to say that of Japanese h'holds, the NZ economy would probably collapse overnight (speaking literally here) as too much would be removed from the consumption components of the economy.

"But fewer people are bothering with term deposits themselves (-2.1% shrinkage in a year), just leaving their funds in transaction accounts (up +32% and that is not a typo) or very low-returning savings accounts (up +15%)."

That's because they are looking to shift their savings else where, like another country that is willing to at least protect their customers money from banking collapse!

LOL.This is exactly right, in my personal case I have quite a but of money floating in my savings account (matured term deposits that I did not renew), that is temporarily parked there while I am progressively diverting it towards other investment vehicles, in NZ and overseas.

yep to transferwise then commerzbank then degiro. Or to the gold refiner then gold.

No wonder people are flocking to Sharesies, Hatch, Stake etc and Smartshares.

Whose loss in the long term ?

RBNZ made a mistake in reducing the percentage of resources the Banks had to raise from local sources.

I think there is a serious possibility that banks are going be funded in the future by the RBNZ to such a level as to be virtually nationalized.

We used to ridicule the USSR for its failed collectivist, central command economic policies; it is funny to see how we now appear to be going exactly towards that direction.

All to support certain folks asset portfolios, because they should be exempt from risk and personal responsibility.

Am I missing something? Why would anyone risk having money in a bank when when you get no interest as such, and it is at risk if a bank fails. Whats the point, why wouldnt you just get a safety deposit box and keep it out of the banks altogether. I mean there is no upside and its clearly a risk leaving it in a bank when you see how exposed banks are with their investing in the overpriced property market.

Banks' balance sheets are in the range of $620 billion, currency in circulation ~$8.0 billion, banks' vaults have $0.833 billion available for further distribution.

Correct, I think the safety deposit box is starting to look appealing. But I think the issue may be with the pricing of insurance on such deposit boxes - if the amount of money is significant, this may be an issue. For example, the "nzvault" option is asking you to contact them directly for insurance quotes, and the "commonwealth vault" option does not provide such insurance directly.

I have not seriously investigated this option yet - but I am definitely going to do it.

If you are keen on investing in term deposits overseas, this is a very interesting option (provided you accept the implicit exchange rate risk) - you can get rates that are already close to current NZ deposit rates - and you have the added benefit of a government guarantee, which in NZ, with its OBR environment, you do not have. If you estimate a 1% chance of a NZ OBR event within the investment period, then it does not make sense to keep any deposits in NZ banks.

One things is for sure - I am leaving very little as term deposits with NZ banks - it is just not worth it and I am not going to take unrewarded risks in order to subsidize others.

but there is no insurance with leaving it in the bank either? and at least in a safety deposit box you can go and take what you want without having to order it 10 days in advance or explain what you want it for.

You are totally correct RealAgent, but I was thinking about some catastrophic event that may destroy the vault itself. A very remote possibility, I know.

Everything has become a gamble now, no certainty. I would suggest that there is a reason there is no Govt guarantee on bank deposits and the feeble guarantee the GOVT has on the table is a sign that is being ignored by many. I suggest they are very worried about the housing bubble and the security of all these loans the banks hold. The only way you make money on a property is to find some sucker that will pay more than you did, and we are running out of suckers. Also, it looks like it will be some time before we can import more suckers from overseas as we have been doing. On the basis of all this, I think a natural catastrophe is less risky now.

yep, I agree, RA. Once the interest rates have achieved rock bottom and the QE has reached its terminal extent, the housing Ponzi will run out of fuel. And this is when things will get interesting.

I would have agreed with you, not long ago... but it appears the queue of ‘suckers’ is endless. And why not invest in property, with terrible returns, when returns are terrible everywhere? Every option leads us in the same direction: ever-accelerating inequality...

Being involved in selling these overpriced assets, I can tell you we are running out of suckers nationally. First homeowners have been easy targets but we will reach the end of this pool shortly, by the end of the year I expect. The only people prepared to buy an overpriced property even now, is someone that has just sold an overpriced property, but that is running out too. Very few imported buyers now, so who is left to buy? You need a good supply of fresh suckers to keep this market turning, and that's the problem and why it will end.

This should just be the only comment on every property article

RA, so you'd feel safer having a few $100'000's in cash in your safe at home than in the bank?

absolutely without question

Because the cashless system is very close, so your notes in the box will be worthless once cashless is implemented. You may have some buffer time to deposit and convert, as happened in India for high end currency notes.

This is a possibility.

I think keeping cash in a basket of currencies might be an interesting option. For example, the possibility of the ECB going cashless, or the USD becoming an electronic currency only, are pretty remote and in any case something that may only happen as a long term prospect.

Definitely, I would have more confidence in such currencies than in the NZ$, especially when the financial system is under the governance of an out-of-control RBNZ, which currently gives me very, very little confidence

Yes any concept of the NZ govt and the RBNZ being "holier than thou" has now completely gone in an instant.

To join the money printing brigade is in my view very short term thinking indeed. Sure most other countries are doing this and given this, the exchange rate and bond yield implications of doing it look attractive. However, if I was involved I would not have gone down this slippery slope route.

But who cares what I think! My wife and dog don't even care. Haha.

Invest in USD denominated ETFs, may be that is a better alternative then putting money in oveseas banks ?

Whatever the risk is having your money in the bank it is much lower than that of taking a mortgage on an overpriced asset and ending up over-leveraged in an uncertain context like we have now.

The West continues it's decline as they destroy the pension system further. When is the turning of the tide? Has it begun? What form will it take?

Changes in trend are usually associated with increased volatility in all areas of life. Is this why the US is in such deep, deep turmoil politically and socially and financially? In short, is this the darkest hour before the dawn?

Technology stocks and commodities and gold may the better store of value. We certainly live in "interesting times". Being a food producing nation is a blessing.

I'm glad you're asking one of the most pertinent question which is so often ignored: WHEN? We probably all agree the world is in an unsustainable path and many have said it will end in disaster soon, for years. So "WHEN"?

In my opinion the collapse is much further away than most believe.

I invite everyone to share their views on "WHEN" the collapse will happen

My guess is now. Changes of trend take a while to play out, looking back they seem like an event, but actually can take place over a period of years. It has taken a long time for the West to decay (50 years). I find it startling that we built more houses in 1974 than we can possibly do today, with a much smaller population.

https://www.interest.co.nz/sites/default/files/styles/full_width/public…

{kind=link}

Thanks for your reply RW. May I ask is your assessment from an academic perspective? Because I'm in property and there is no downturn whatsoever now (see today's Interest auction results nationwide)

OCR & QE should reach their limits next year, so I had originally thought the end was nigh within the next few years. Then I googled what happened in Japan - 100 year mortgages to 'promote home ownership'! Now I think this bubble could have a lot longer to run - sadly things are so badly distorted that there is no way out. The can will keep getting kicked from one generation to the next...

Stuckathome what it really means is get stuck in, don't give up. Carry on and do the best you can.Thats all most of every generation have ever done. Some things never change and aspiring to better you'r own situation is as old as time.

RW, I struggle to see the correlation between number of houses built in 1974 and fiscal and monetary policies today, can you please explain?

Yvil - 1st of April 2056 !

Just Kidding, if you believe in MMT there doesn't have to be a crash ever, and QE in NZ$ can be written off at the stroke of a pen ! I used to believe that currencies should be pegged to gold now I don't. If it is pegged to gold then the Economy has a fixed amount of money in it like the game Monopoly. In Monopoly there can only be one winner but under MMT everyone in theory can be winner's ! I'm not concerned about a collapse more focused on having a great life. As a great man once said monies only a problem when you don't have enough. I wonder how RP's TD are going Haha and his predictions of a total property collapse and a L shaped recovery !

Yes, QE/MMT may be part of the solution, if it is used to cancell the excess debt load. It is a big if, though, as it is far more likely to make the misallocation of resources far worse. As in turning us into New Argentina.

I don't think there will ever be a "when" Yvil tbh. Nor do I believe there will be a "collapse" which sort of infers a sudden event. I do think there will be changes but I think they'll be slow and incremental, much as they always have been, barring warfare of course. Most won't notice the changes until they look back over many decades and say "those were the days when ...."

Thanks for your reply Hook, an interesting view and you may well be right… I thought we would reach a tipping point where share markets worldwide will reduce over 50% in value, this will have a flow on effect of people not spending, then many companies going broke, massive job losses and finally big losses of other assets as well but I might be wrong

Well the current PE values are a little out of whack to be sure. But if folks have nowhere else to put their money (other than under the mattress) I think they'll keep on rumbling along. I personally think there are a lot of retail investors looking at capital gain rather than fundamentals and divy yield, which admittedly is boosting prices for some companies and could easily result in pain and headaches. Right about now there is only uncertainty and elevated risk going forward, with all asset classes. Maybe the "free ride" has reached the bus stop? Time to get off - time to get on? Who knows

Unfortunately farmers are being hammered by this govt.

Hopefully the era of fanatical farmer bashing is finishing. Food is the basis on which all else depends. Time for some home truths for the entitled generations.

Farmer bashing has been undertaken for years by the unwashed,overeducated but ill informed, underemployed sector who would moan at the water damage created and the carbon emissions caused when the fire brigade puts the house fire out.. until it's their house. They generally fail to see the overall picture, i.e. food security and supply. In my experience they are very myopic

Wish I could share your optimism Rodger! Farmer bashing is alive and well and If our current elected (and unelected) muppets get back into power it will be ramped up to a level never before seen!

let them beat their drum DD. I just shrug and mutter "muppets" and carry on. You can never convince some people so it's a waste of energy and emotion trying. I take perverse and never ending pleasure I'm profiting off their appetites, whilst dining on fresh fruit and veges, free range eggs and unadulterated home reared beef and sheep, all the while breathing fresh clean air and admiring the view and enjoying the peace and quiet.. It's a tough life!! lol.. Until it p#sses down with rain and you're in the middle of calving, then it's not such fun. I still wouldn't swap it for a desk though

Hook, I couldn't agree with your sentiments more. Been behind a desk and wouldn't go back! The frustrating thing as that the muppets can't see the golden goose standing right in front of them!

Yeah I'm with you, spent most of my life in the bush trapping possums,shearing sheep etc all good. But we do have a problem with our fragile landscape we are farming. I have been involved with hill country development for many years and as I get older I am realising a lot of land we are farming in NZ is totaly unsustainable. We have very little tractor country. Grazing hills only works so long as the fert goes on and before the soil slips away, unfortunately. Long term we will produce less protein of our hills as they degrade. Don't know what the answers are but get in to it and enjoy life today.

Yes the Boomer generation needs to wake up and smell the roses..

It's nothing to do with boomers or any generation. It is simply a human thing.

You need to accept who planted the roses in the first place frazz.. certainly not your generation

The hard work of the Boomer's parents who returned from war. Worked their arses off to build a better society for future generations, but bred a spoilt entitled and greedy generation who couldn't carry on that tradition.

$60 billion in debt thanks to Key incentivising watering loans. And now farms prices mean they cannot cash out.

What a lot of drivel. Farms looking to "cash out" aren't the ones who are carrying the debt, they are smaller family type farms whose owners are just sick of the BS. The MS payouts are looking good for the coming season and often the farms being sold ( the smaller ones) are being flipped to carbon farmers for very good returns. Hort returns are good and getting better. Hill country sheep farms and some beef farms are under a bit of pressure but this is cyclic and the owners know how to farm through it.

R W,

In the context you used it, its should not have an apostrophe-just saying.

My concern David will be the effect on listed floating bonds/notes if the OCR is negative. Most were issued when there was no talk of negative interest rates. The investment statements talk about paying interest but can a floating rate bond require bondholders to pay the bond issuer? Infratil perpetual bonds are an example.

On one hand the banks are paying next to nothing to depositors, on the other they are rorting borrowers who are on floating mortgages. ANZ and all the other big banks are charging at least 1.1% more than Kiwibank for floating/revolving facilities....!

Borrowers on floating terms now probably deserve to be "rorted" unless they are planning to sell soon. These borrowers are trying to hold out for lower interest rates thinking they are smart but will lose any gains in lower rates (if they come) due to higher payments now on floating. Kiwibank isn't very competitive on fixed rates, they never have been. Their deposit rates aren't that flash either. For a "Kiwi owned bank, for kiwis by kiwis" they're actually pretty hohum.

Hook, why does any borrower deserve to be rorted by banks?? Next you'll be saying girls who wear short skirts deserve what they get!

The disparity between fixed and floating rates is huge (especially compared to oversea) and there are plenty of reasons why some borrowers prefer the latter, that do not involve selling soon or holding out for a better rate because they think it is "smart".

Sounds like it is you who thinks you are smarter than the rest of us....

I'm certainly more realistic than a lot here and I don't resort to overseas examples to make their argument appear more robust. As for girls and short skirts.. if you want to wear a g string to the pub don't moan when your @rse gets grabbed.

What people fail to understand about taking money out of the bank and into a safety deposit box?

Banks are creators of the money supply. If assets collapse and banks go into liquidation or Obr bail in or bail out. It means the physical cash has zero value because when banks created the currency when they purchased a security ie the mortgage and house that backed it. When the assets collapse the money created backed by the asset now has no value. Or heavily debased.

There is more to a banking system than liquidity: there is velocity.

That is what will be falling.

Can lead horse to water but cannot make it borrow, or lend for that matter

Which is why government is helping business because banks were not doing their bit, as Finance minister said months ago.

Velocity is just GDP / money supply. Numerator's down and denominator's up so not surprising, but if people lose faith in the purchasing power of currency that situation could invert very quickly. It would be uncontrollable. Dangerous game.

And what happens when the savers revolt? Oh that's not a problem - the RBNZ will magic up some money and lend it directly to the banks (via the term lending facility). Whole system is FUBAHR.

Exactly right. Maybe Orr and company should be reading about the failed central command economies of real communism and how such economies ultimately imploded under their own structural faults. The term lending facility is the first step towards virtual nationalization of the entire banking system - Brezhnev would have been proud.

The complete mis-pricing of risk, and the killing of the bond market, both caused by such reckless behaviour of the RBNZ, will zombifie the entire economy.

Make no mistake - there is no free lunch and the NZ economy and financial system will ultimately pay a dear price for the dubious advantage of kicking the can down the road a little bit longer, and of being able to pretend that the economic cycle can be magically made to disappear with the magical thinking of QE and negative interest rates.

Let's continue selling houses to each other, who cares about the real economy!

There's an unlimited amount of money at the NZ Reserve.

As interest rates go negative, and risk of bail ins rise, buying gold becomes more attractive. One of the old arguments against gold was that it has no yield - well no yield is better than paying the bank to hold your cash.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.