Treasury is foreshadowing government spending (fiscal policy) playing a greater role in supporting the economy beyond the COVID-19 crisis.

Secretary to The Treasury Caralee McLiesh told Wellington’s economics community, gathered at a Treasury and Reserve Bank-run event on Tuesday, that the agency is “examining opportunities to modernise the public finance system”.

McLiesh, who rarely speaks publicly, said Treasury was considering how its approach towards managing the economy needs to evolve with structural changes in the economy.

A key change since the 2008 Global Financial Crisis (GFC) is that globalisation and technological advancements have made goods and services cheaper. This has kept inflation and thus interest rates low.

Accordingly, central banks have less room to lower interest rates to boost economic activity… which is where fiscal policy is useful.

McLiesh explained: “Beyond the pandemic, over the last decade there has been a growing view in economics on the need for a more active role for fiscal policy in macroeconomic stabilisation.

“Evidence from the period after the GFC has improved our understanding of the benefits arising from fiscal policy, showing that both spending increases and tax cuts can boost output in the short-term.”

McLiesh also noted that fiscal policy can provide more targeted support during shocks that have uneven impacts on particular sectors or regions. On the flipside, monetary policy (or changing interest rates) is more broad-based.

McLiesh recognised the downsides of fiscal policy are that it can take a while for changes to be implemented or take effect. Politically, it’s also easier to provide stimulus (IE tax cuts) than take it away.

Removing support too soon could cause scarring

In the context of the COVID-19 crisis, McLiesh warned against the Government removing support too soon.

“Our view is also that there are high marginal benefits to wellbeing for spending to offset the worst aspects of the crisis and avoid long-term economic scarring,” she said.

“With limited space for conventional monetary easing and ongoing uncertainty, consolidating too early could also have significant risks to long-term living standards…

“If the economy ultimately responds better than expected, automatic stabilisers will be triggered and monetary policy could be adjusted.”

But what about debt?

McLiesh recognised more fiscal policy increases debt. But she said we shouldn’t fixate on this.

She noted that while Treasury in 2019 thought the government shouldn’t take out debt worth more than 50% or 60% of Gross Domestic Product (GDP), there is no golden number when it comes to government debt.

“Upper limits on debt depend on context,” she said.

McLiesh said the Government would be able to continue finding investors willing to buy its debt, even if debt to GDP was “far in excess” of 50% to 60%.

What’s more, the Government could continue to service debt at these levels, as interest rates are low.

“While fiscal discipline is always important, it is also important not to have an excessive focus on debt levels as an end objective in and of themselves,” McLiesh said.

“The general rule of thumb is that debt should fund spending where, across generations, the benefits in wellbeing exceed the costs of that spending.

“The ‘right' level of spending therefore depends critically on the value of spending initiatives. Where initiatives can deliver high value for money, the appropriate level of debt will be higher.

“And with debt servicing costs at historically low levels, there is greater headroom for high-quality investments that raise living standards across generations.”

McLiesh spent some time explaining how much of a game-changer low interest rates are when thinking about government debt.

“With interest rates expected to be below growth rates for a considerable period, it is technically possible for debt as a percentage of GDP to fall, even with a structural budget deficit,” she said.

She said this is a “fundamentally different dynamic” to back when the principles that guide the way a government manages the economy were created.

McLiesh also noted the fact the Reserve Bank has bought nearly the same amount of New Zealand government debt as has been issued since the onset of COVID-19, to put downward pressure on interest rates.

Interest rates could find their new norm at a higher level

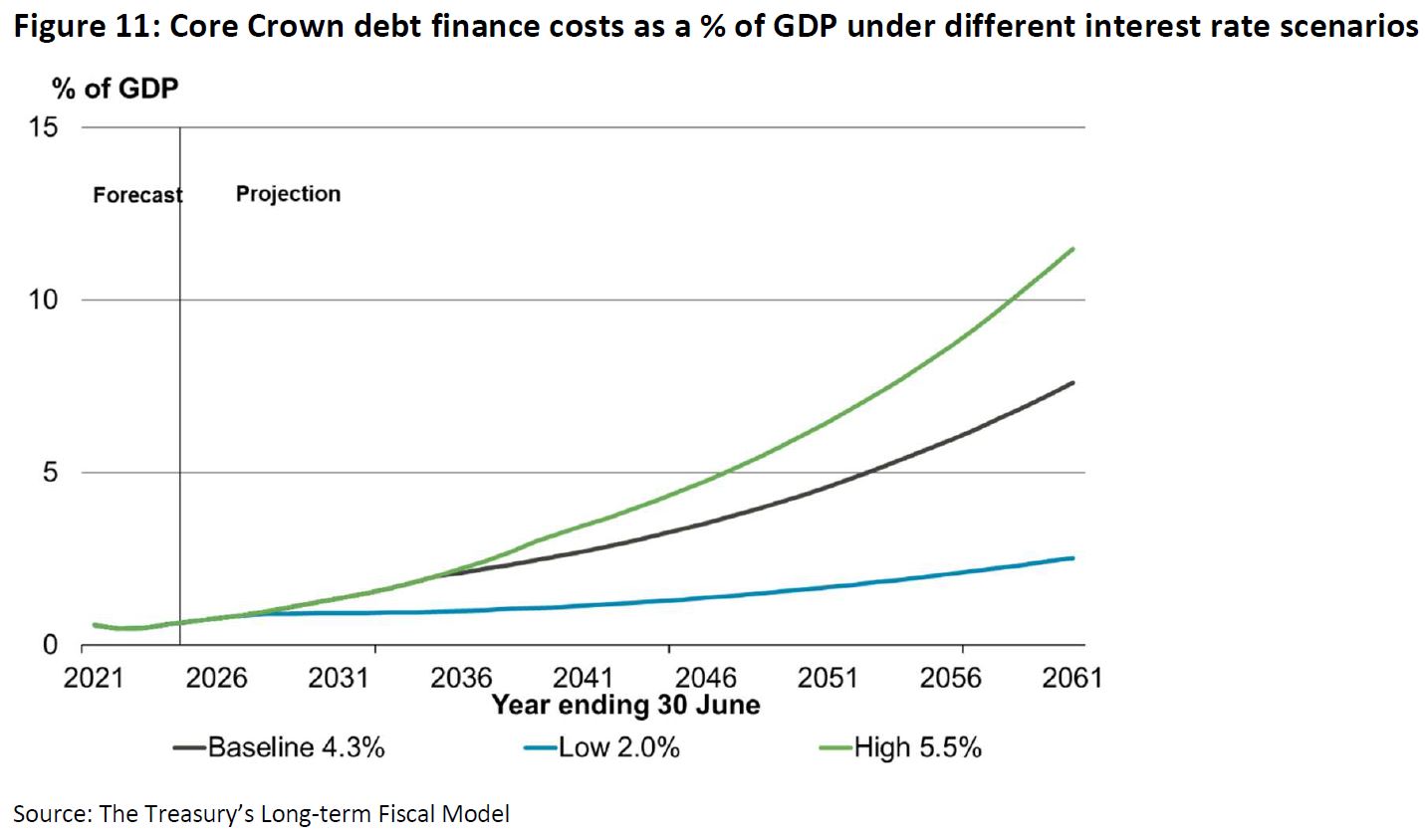

Nonetheless, McLiesh was aware; “While factors influencing the long-term decline in interest rates - such as changing demographics, globalisation, technology, inequality - are unlikely to quickly change, we cannot discount the possibility that favourable debt dynamics will reverse.”

She said that if interest rates rose from 2% to 5.5%, the government’s debt servicing costs would rise from 2.5% to 12% of GDP by 2041.

McLiesh also noted that because New Zealand is a small open economy susceptible to economic shocks and natural disasters, it should maintain some buffers to respond in a time of crisis.

How to modernise the system

Coming back to her core message of modernising the public finance system, McLiesh said: “This includes a greater focus on strategic planning and wellbeing outcomes, improved collaboration across agencies to achieve those outcomes, further emphasis on base not just incremental spending, and a stronger medium-term focus.

“These changes aren’t just about our budget systems, they are also about making fiscal policy more effective.”

Finance Minister Grant Robertson has also said he’s keen to reform the Public Finance Act.

See a transcript of McLiesh's speech here.

50 Comments

Call me old fashioned, but going further into debt 'because interest rates are cheap' seems a bad idea.

How about we stabilize our population, pay off all our debts, and then lend money to other nations. Let them work for us.

Like I said, it's an old fashioned way of thinking.

I'm sorry to say it, but you're old fashioned. (No offence intended)

No need to be sorry. I am proud of my old fashioned ideas on finance.

Unfortunately I have seen some very decent hardworking people wiped out by debt when the cycle turns, as it inevitably does.

Government finances are different to "decent hardworking people" finances. Something to do with the power to issue currency and to tax - means sovereign currency issuing countries like New Zealand would only default on debt if it chooses to.

We will follow whatever they do in the USA

Right now, the USA, for all the justification of low rates this & sovereign tax this, cannot pay back its debt. They could not politically choose to make the cuts necessary. Try proppossing military cuts and see how many votes you get..

The only way interest payments are affordable is via raising more debt.

And faith in this debt market is being propped up via the government buying its own debt.

They dug themselves into a hole they cannot escape without either default or massive system changes and people (like this article) are now trying to convince you that no no, everything is OK, it's actually the winning strategy all along.

This game of Continued growth of finances is just an artificial construct, a complex bartering system with winners, looser and people manipulating the rules to keep it moving.

But at the end of the day its masking the real challanges we face as a species. Humans demand growth, and this financial system we are working does not encourage us to ask "what is sustainable?", but rather "how can I always have more?".

I don't know the political solution that works next, but anyone with half an objective brain can see we are not on the right path.

yes,fiscal policy now favours the shifty rather than the thrifty.to live by a protestant work ethic has been replaced by a need to lie and hide your money.

Depends on what you do with the money. Used well can result in a much stronger financial position in the long run.

That's a pre Limits-to-Growth comment, indeed a linear one.

Sifting through the placatory jargon, I reckon this is the nub:

"a greater focus on strategic planning and wellbeing outcomes, improved collaboration across agencies to achieve those outcomes, further emphasis on base not just incremental spending, and a stronger medium-term focus."

It's like pulling teeth - but methinks we've run out of time to morph the narrative. And it's not really clear if she gets what that byte means. I'm guessing no journalist though to ask Limits questions? For those who haven't bothered reading it, here is the pertinent backgrounder:

https://surplusenergyeconomics.wordpress.com/

On the basis of which you'd be pretty skeptical about incurring debt, full stop. And you'd be saying 'stronger very-long term focus'.

I used to think like that, I mean we are in debt so it must be another country that's lending us the money right ? Wrong every country is in debt, that's how new money creation works, its lent into existence in the form of a debt to be repaid in the future. The whole system falls over if everyone paid back the debt and we were in credit so in fact more and more debt is seen as "Growth". Money now is just numbers pulled out of thin air but your ability to pay that back is real in terms of time, effort and resources. Weird system isn't it, borrowing from the future to pay for the now. Cheap interest rates just encourages more borrowing and house prices to go boom. This somehow gets perceived to be a good thing by the powers that be and the cycle continues.

I am sceptical of claims loans are just made out of thin air. In that case who gets the interest charged on the loan and why do they deserve it? And why pay interest on term deposits if you can magic up the money for free?

I always understood countries borrow from those that have cash to lend, be it another country such as Saudi Arabia or China, superannuation funds, insurance companies, large funds pooling private wealth etc. If we don't need to borrow from them what do they do with their cash for a return?

You may find this video informative on your questions:

https://youtu.be/TkCU_n0h4Qc

Double post

Fascinating era indeed. Cheap debt and low interest rates work well due to Globalisation. However due to current covid situation and continuous supply chain disruption, I highly doubt we can maintain them much longer.

“And with debt servicing costs at historically low levels, there is greater headroom for high-quality investments that raise living standards across generations.”

Convincing banks to monetise zero risk weighted capital government debt inevitably crowds out private bank commitment to grow the 150% risk weighted productive value added sector.

What good is being derived from banks' $29.882bn stake in the inert monetary base, while the government sits on $36.498bn Crown Settlement Account deposits waiting to be disbursed to in need recipient taxpayers from the RBNZ?

Governments have a history of squandering capital beyond that which is required to sustain national welfare. And yet the neoliberal desire to privatise the public estate persists.

Yep. Clown world.

In this recent interview with Mihi Forbes, Mike King summed up the government intention vs delivery perfectly. https://www.newshub.co.nz/home/new-zealand/2021/06/mike-king-lashes-out…

Government sit in their ivory towers with the choicest theories about everything from A to Z. But they have zero clue about delivery, because they have zero experience delivering within the constraints of real world parameters like small businesses do every day.

Governments economic orthodoxy from 1976 onwards was borrowed and swallowed from Friedman and Hayek.

Before that it was Keynes 1935-75.

Government spending money into existence (for infrastructure) is vastly more preferable than banks lending it into existence (for house price inflation).

We have zero chance of maintaining our current collection of infrastructure, given resource draw-down and energy-reduction (plus entropy - everyone should understand entropy and its interplay with complexity).

Why try and build even more, wasting more of what's left for future generations? Talking present wellbeing is all very self-justifyingly well, but shafting future options is longitudinal colonialism. Of which we're all guilty.

The amount of Govt money spent that hasn't been taxed back (aka 'debt') is just a number. The 'cost of debt servicing' scare stories are a last gasp attempt at trying to convince the public that this 'debt' number is somehow important - RBNZ has shown that it can set the interest rate on bonds at whatever level it wants. This view will be dominant within a year or so, even US senators get it now... https://twitter.com/i/status/1405657111514779649

Debt is a claim on future stuff, and it's delivery. (Thought I'd change from resources and energy - but that's what it is).

If the Government places that claim, it displaces other options. I'm no private-enterprise booster; PE is typically even shorter-term-looking; I mean others horizontally and more and more importantly, longitudinally.

No point in handing future generations flyovers-to-nowhere, made from fossil fuel feedstock with no PlanB. That's not a bequest, that's a mill-stone.

The rampant exploitation of natural resources to accelerate the death of all living things on the planet is absolutely a claim on the future - but some numbers on a Govt 'debt' spreadsheet are absolutely not a claim on the future. What is important is Govt spending the money it creates on the right things. For example, widening roads to support ever more urban sprawl = very stupid, whereas building new infrastructure now to dramatically reduce energy and resource consumption forever = smart.

Hardly surprising that inflation is low. New Zealands peak GDP per hour worked was 2012 and GDP per capita was 2014. We should be poorer than we where almost a decade ago because we are less productive.

To some extent that's been disguised to many by rising asset prices but I suspect, when the current market/credit cycle ends, we might well feel a pinch. I think it was Jimmy Carter who said "If we succumb to a dream world, we'll wake up to a nightmare."

Wow. Imagine what the Secretary for the Treasury will say when she realises that New Zealand is a sovereign currency issuing nation.

Still, big progress to recognise the benefits of fiscal policy.

Central banks. Making it up as they go from one crises to the next.

Why don't we just live within our means.

Lots of "woke" thinking in this article. People in NZ will eat it up, because we have never experienced a very serious financial crisis since the 1930s. The current NZ government does not have a clue about management of finance. The next significant financial crisis will see NZ unprepared and in serious trouble.

As long as they keep the housing ponzi alive as being the only economy in NZ. Not just for argument but is reality.

Debt is the new mantra. More debt more successful as government and RBNZ are more stressed for individual defaulting than the individual borrowing as it will expose RBNZ and Government policies.

So chill and borrow and if any problem, RBNZ and Government will find a solution for you as they are at risk.

Unfortunately governments lose elections quite regularly and if something big happens to cause stress, the other lot will get in and change lots of stuff.

1966, 1987, 2008, 2020

Debt is the new norm. Economy is no more based on fundamental but is based on access to cheap and easy debt - New Norm.

ICU is the new norm, so no need for normal ward in the hospital. Permanent emergency mode.

While I understand that this is not about the average person's banking, this bit still got my attention; "A key change since the 2008 Global Financial Crisis (GFC) is that globalisation and technological advancements have made goods and services cheaper. This has kept inflation ...... rates low." From my perspective this is not so. I see the costs of goods and services increasing at a faster rate than my salary. And while the author of this will argue that the evidence is [now] historical, current rates increases are mind blowing. Horizons (Manawatu / Whanganui ) imposing an 8%+ increase is just one example. It appears the Government at all levels is bound and determined to drive their captive populations into poverty!

Agreed. That jarred with me, too. I suspect she's pretending not to know.

If you keep a lid on ferment long enough, the lid blows off. I suspect that is what the massive debt-issuance coupled with increasing real scarcity (and worse per-head scarcity) is; a ferment.

Hilarious. 45 years of economic orthodoxy saying government spending is big evil and harmful to economy.

And as soon as cannot cut rates any more, lo and behold government is good to go again for the high priests.

More borrowing is answer. No raising gov spending y raising revenue, no, no. Cannot raise taxes as electorate do not want to be told things need paying for. 45 years under-investment due to economic bigotry and now told answer is to borrow more. AND inflation figures published are a multi-year adjusted joke anyway.

The economists in the 1940s were five times as knowledgeable as the brainwashed neoliberal set we have now: http://www.constitution.org/tax/us-ic/cmt/ruml_obsolete.pdf

I'm no crypto fan, but it's this sort of talk that boosts crypto's appeal. Why would you ever leave any wealth in fiat with this sort of carry-on being discussed?

Because as soon as the current monetary system is facing imminent collapse your Fiat will simply converted to Digital anyway. Digital is the Plan B. You simply need a mix of hard assets and cash with no debt to come out of the transition with only a flesh wound.

It will be too late by then - your fiat will have been devalued to the point where it is worthless. I'd much rather have assets and $ denominated debt than $ when it all hits the fan.

That's fine if you can keep up the payments when it hits the fan. It's not an instant process. The usual pattern is incomes drop for an extended period, assets need to be liquidated by the heavily indebted as as they fall into arrears, asset prices drop. The cashed up pounce when asset prices bottom out.

It would be such a privilege to see NZ having a negative symbol on its OCR publication in my lifetime.

Clint Ballinger has this to say on his website which is pertinent to this article.

Decouple Spending From Bond Sales

"Government bonds for funding are well understood to be an unnecessary, vestigial custom for currency-issuers.* There has been discussion of eliminating them as they serve no funding purpose.

An argument in favor of eliminating bonds is that they are the foundation for the widely held yet false belief that a “national debt” limits what public projects can be carried out. Eliminate bonds associated with “funding” and we achieve a more transparent, easy-to-understand system with no “national debt” for the media to discuss. This in turn enables the media and public to see the logic in optimizing spending up to the public’s own desired resource use for their own wellbeing (healthcare, education, a job guarantee) and in turn electing representatives who will do so".

https://clintballinger.wordpress.com/2018/11/13/decouple-spending-from-…

So politicians get no limits on spending. That looks like a recipe for runaway inflation to me.

So why do we allow the banks to create almost unlimited quantities of money just to drive up the price of housing by the use of monetary policy? The availability of resources should be the limiting factor on the governments spending and not some perceived debt limit. The governments debt is only the private sectors savings of our currency anyway as 'sectoral balances' illustrates.

The chickens will one day come home to roost on the excess lending into housing. Look to any number of overseas experiences on that one.

The voters understand the concept of a government debt, which kind of keeps politicians under some control. Remove that measure and they will surely overspend to pander to voters short term interests. Enough of that spending will find it's way overseas, and so the NZD drops which gets us into an inflationary spiral.

Edit reply t/l - it should be measured in energy :) represents 'work done'.

This is the fundamental flaw in MMT too - you get to spend the remaining effort on behalf of the public, and to heck with the debt.

The problem is that this crop of politicians haven't got what it takes to ascertain a de-growth future, and they'll therefore shoot their bolts in the wrong direction. A pity, when it's the last one we'll get to shoot.

Nah, build a space elevator - infrastructure guaranteed to reduce power consumption on the planet and enable infinite growth.

No you don't understand the issue. As a sovereign owner of the currency the Government can issue all the money it wants, but this is not without cost, although it is not 'debt' as it is commonly discussed. Taxation is still required, just that the vectors for taxation become different, as taxation is no longer for the purpose of funding government spending. But the Government can create all the money it needs to fund infrastructure for example.

Take local Government rates as an example. Horizons (Manawatu, Whanganui) have just announced an 8%+ rates increase which is mind boggling, and so far above inflation that it is not funny. They appear insensible to the fact that NONE of their rate payers will have seen an income increase that comes close to that level, and most if not all none at all. They will argue that legislation requires them to carry out the work funded by these rates, and therein lies the solution. If Government requires local Councils to meet certain standards then the Government should fund it. Instead Government at all levels seem bound and determined to drive their constituents into poverty. While i have used Horizons, I have noted multiple reported rates increases across the country, and none have have be at or less than the official CPI, rather most being significantly large, all the while ignoring that with COVID still ever present, most people are suffering some degree of income loss.

No Murray - excess demand for the remaining bits of the planet, is what is 'driving people into poverty'.

That is reflected in Rates, and I suggest, in house prices (if we think of that as 'finite land' prices, added to and obscured by debt-issuance). If wealth is access the resources and energy, poverty is the reverse. It gets obscured when we think in $$$$$ terms, the messy bit being the digital expectation. Yes, Govt can 'issue' 'money' - it could also just decree that something gets done, with something, by someone (usually done at the point of a gun). And it could illegitimise that 'money' by law in a heartbeat. But the real conflict over resources (for roading, pipework, diggers) is now outpacing the ability to make stuff, so yes, people are going to get 'poorer' per time. Falling EROEI couldn't have any other effect

While I agree in the end result, I don't agree with you in the pathway, or parts of it. The problem is constrained resources, but government expectations, and therefore legislation fails to recognise this. Councils only have limited ability to constrain economic activity, that is more the purview of the central Government. The issue we face is Governments placing expectations on Councils without considering the cost, or the ability of populations to fund them. Councils have little choice but to go to their constituents for that funding, and are indeed empowered to do so. But there is little to no right of the population to challenge those demands, even at elections. in addition, Councils are failing in an important part of their roles; "so yes, people are going to get 'poorer' per time" Councils should be able to have a voice at central Government to tell them that rates rises are unaffordable for their populations. They don't do this because they do know that if they did, it would incur increased Government scrutiny of their activities and operations, which may be of benefit to their constituents, but most certainly wouldn't for those in power at the local level.

So what we have as an example, is regional councils required to manage waterways and water quality, but their ability to constrain the activities that place these at risk either doesn't exist or is severely limited. The discussion seldom goes towards restraining farming, but is more about changing farming practice. There is plenty of scientific evidence to indicate that changing practice has only limited impact until the practice is restrained. Again as in so many other areas of this debate, the authorities actively avoid the hard discussions until something smashes them in the face, and then generally the discussion is about how to wriggle out of the consequences without restraining the activities that cause the problem.

Why not build 20,000 Govt houses? Like the 50s.

Kill 2 birds with one stone - fiscal stimulus and housing relief (no more motels as ‘housing’)

Because there is enough housing in NZ now,

Just not evenly distributed.

And 'like the 1950's' is so far out of whack, it's hard to know where to begin. We were in the inflection part of the growth curve, most of the resources and much good-quality energy remained untapped - and there were 3 billion inhabitants of the planet, consuming a lot less per head. And our inevitably-congested sprawl (complexity theory is worth reading up about) hadn't happened. Yet.

Yes, but asset inflation has been rampant, with massive doses of QE aimed at encouraging consumer spending through the "feel-good" effect of higher asset prices-property in particular.

Somehow, this should be reflected in the inflation stats.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.