By Gareth Vaughan

Those who saw my Top 10 last week may recall the first item was entitled; The milk powder paradox?

This highlighted a book by ex-pat New Zealander Michael Parker called The Pine Tree Paradox; why creating the New Zealand we all dream of requires a great university. I suggested his thesis that exporting wasn't going to make New Zealand rich, which he argued through several examples led by pine trees, could now be extended to milk powder given over supply in the market and tumbling prices.

Having met and interviewed Parker back in 2011 I thought I'd flick him an email highlighting my Top 10 and ask him what he thought.

Turns out Parker, who is a Hong Kong-based equity strategist at Bernstein, has been thinking the same thing and sent me a copy of a report he issued on July 24.

Commodities, Parker notes in the report entitled; Strategy Blast: The Pine Tree Paradox... An Abundance of Everything, used to be a pejorative, or contemptuous, term.

"Producing stuff that lots of other companies and lots of other economies can also produce was viewed as a risky way of making a living. Sure when demand outstripped supply, prices and margins would rise. But with the low barriers to entry endemic to commodities, those high margins would simply encourage new capacity. Oversupply was viewed as a constant threat. Then along came China. Demand - as a constraint - was taken off the table for a decade, and commodity prices roofed it. That, as we continue to learn, is not a permanent condition."

Almost regardless of what the commodity is, the narrative is identical, Parker continues.

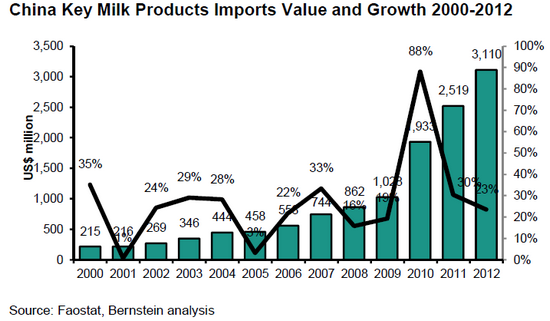

"Driven by urbanisation and the burgeoning middle class, Chinese demand for [milk] has spiked over the last five years, raising prices for [whole milk powder] to record levels. Even so, by volume, the [6] million tons of [milk product] that China imported in [2013] was far from sufficient to bridge the gap between developed market and Chinese consumption on a per capita basis. Accordingly, industry expectation was that the global [dairy] market would remain tight for at least the rest of the decade."

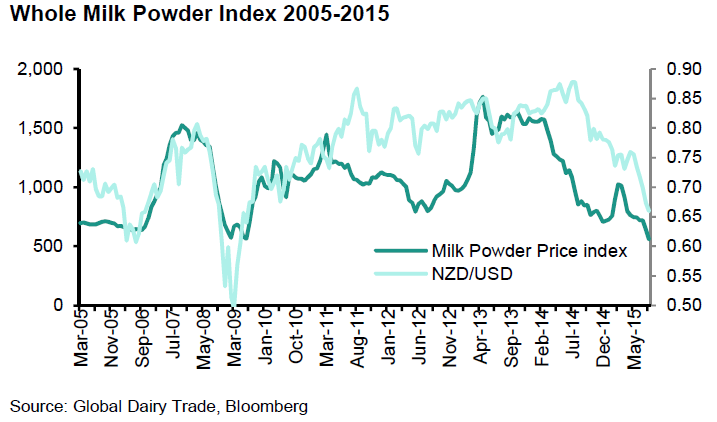

"That didn't happen. Despite rising demand in China, capacity increases globally (it only takes three years to [raise a herd of dairy cattle]) and the relatively simple process of producing [milk powder] resulted in increased supply from a multitude of sources. Prices have collapsed since the beginning of [2014] to the lowest levels since the global financial crisis."

For economies such as New Zealand's, where economic growth and exports are joined at the hip to the fortunes of commodities, the drop in the price of the key export heralds a fall in the value of the currency and a sharp economic slowdown, Parker adds. And as the economy slows interest rates are cut with the Reserve Bank having cut the Official Cash Rate last month with more cuts expected to follow.

"It is a painful lesson for companies and economies. The ability to produce something better and cheaper than anyone else in the world feels like a sustainable, competitive advantage and, strictly speaking, it is. However, when that something is a commodity, being the low cost producer is no guarantee of riches. When demand for that commodity ceases to rise faster than the new sources of supply, and/or when substitutes become available, prices collapse. That's bad news for both high-cost and low-cost producers. And, by definition with commodities, there are too many suppliers to mount a coordinated response."

Thus being the Saudi Arabia of something isn't necessary good news. This, Parker says, is the Pine Tree Paradox. You may be able to grow pine trees faster in New Zealand than anywhere else. But to compensate other countries such as Canada just plant more pine trees so what feels like a competitive advantage isn't one.

"Admittedly, Kiwis are slow learners. Broadly this same dynamic played out in the 1950s with wool (who knew the Korean cease fire would last?), in the 1970s with butter and lamb (who knew the UK would join the EU?) And, to a greater or lesser extent, with pine trees, kiwifruit, wine, peaches and a dozen other agricultural products over the last few decades. The relatively recent collapse in the price of milk powder is simply the continuation of a 70-year old pattern of being structurally long a cyclical trend."

"There is plenty of commentary around to suggest that what happened with milk over the last two years is very different from what happened with other commodities, where prices also tumbled. Like snowflakes, commodities are all unique... except they're all exactly the same."

Parker's report goes on to make the case again substituting Australia for New Zealand and coal for cows, noting tongue in cheek that coal and cows couldn't be more different.

"Chinese demand for [power] spiked over the last five years, raising prices for [coal] to record levels. Yet by volume the [300] million tons of [coal] that China imported in [2012] was far from sufficient to bridge the gap between developed market and Chinese [power] consumption on a per capita basis. Accordingly, industry expectation was that the [coal] market would remain tight for at least the rest of the decade."

"That didn't happen. Despite rising [power] demand in China, supply improvements globally (it only takes three years to [build a coal mine or a dam]) and the relatively simple process of producing [electricity] meant increased supply from a multitude of sources. [Coal] prices have collapsed since the beginning of [2012] to the lowest levels since the global financial crisis."

He also makes the point that importing commodities is always the least favoured option given they are bulky and expensive to transport. Ultimately, Parker says with rare exception, commodity prices are likely to stay low for a long time.

"The lesson for most commodity producers is: stop investing. The best option for low cost producers (all those "Saudi Arabia of XXX") in an environment of weak or no demand growth is to cut growth CapEx to zero. There is an immediate improvement in free cash flow along with the ability to pay dividends, reduce debt or buy back stock. Australia doesn't need any more coal mines and New Zealand doesn't need more cows."

"It is always tempting to blame "perfect storms" when things go this badly for any sector. The truth is that the problem, when it comes to commodities, isn't the black swans. It's the camels."

The last point is a reference to Parker being asked by an Indian colleague when they began analysing global milk supply whether they should include camels.

Separately Parker has undertaken major research on data from the Chinese government and Chinese companies looking at how reliable it is. There's more on this in an interview he did with Barron's here.

*This story was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

43 Comments

There is a lot of sense in this article. Alas I fear New Zealand will continue to do the opposite of the recommendations.

It's fine with 20/20 hindsight to be critical, but NZ was fully positioned to take advantage of the dairy boom with the formation of Fonterra at just the same time that China entered the WTO.

It is possible to become rich from commodities as long as you don't run off chasing rainbows. There are rich kiwifruit orchardists out there, and there will be a few rich dairy farmers around still. The trouble is that at the first sign of good prices most people automatically and immediately thoink it is different this time, and the boom will last forever. Investing in a dairy farm paying $40-60k/ha is investing in a rainbow, the same goes for every boom that has its bust. People just seem addicted to throwing money down the drain. That is the real problem we have, as far as this issue is concerned at least. The gamblers mentality, all or nothing, it'll be nothing soon enough for some people.

the normal pattern for boom busts is the weak ones go under and the market corrects with the strong surviving and supply adjusting down to match demand.

how will that work with dairy farms will we see some convert back to sheep or beef.

at the end of the kiwifruit boom a lot ended up ripping up their vines

its not the weak ones and the strong ones.

It's those with excess wealth already (that survive) eg cross-subsidising,

and those entering the market eg the young that fail. sure some foolish people go under from bad management or overleveraging but they go under regardless, they just increase the overall economy until they do break.

Red meat better be deleveraging asp. Has there been a fundamental change in the raw-to-plate process? If not then the price is still cyclic based on yesterdays prices. As cattle heads come off prices will drop. from low milk or from high grain prices, we're just tailing the end of the northern hemisphere season now. (and tailing the winter season in NZ so few heads roll this time of year).

So don't be too cockie about the local meat prices just yet.

Also keep in mind vertical vegetation farming IS growing (against the price trend). (was hoping to use a variant for lucerne by the dairy shed, using dairy waste as a nutrient source).

That and parcelled food delivery, and improved vegetarian recipes for the public (vegetarian != lettuce salad).

On the commodities thing... why has petrol and diesil not followed the commodity drive downwards??

The UK in the past 12 months increased milk production by, 1.6 billion liters or 80,000 tankers or 40 pints for every person in the country.

Your math is a bit astray AJ. That actually works out to "14 extra pints per person per year" and up to 130 pints per person per year, or now up to one pint every three days. Not really that much.

Or 136 million milk solids, or 800-ish NZ dairy farms, hardly much at all, the Chinese could buy all of those before breakfast..

1.6 billion litre = 2.81 billion Imperial pints / 63 million UKers = 44 pints per person per year? Or perhaps I should have divided 160 billion by 1.76 = 14 pints?!

Sorry David, I pasted it out of The Cornwall newspaper. Must be the Cornish school system.

It's OK, we'll just export our housing stock instead.

And our dairy farms...

Yup why not. National's economic policy is akin to a garage sale.

But given how hopeless the outlook for NZ dairying is, wouldn't foreigners buying dairy farms be doing us all a favour? They'd take on themselves the burden of this activity that is never again likely to do anything but drag farm owners into debt and despair. That would be a bit stupid of them, but that's their problem.

Then the ex-dairy farm owners could take the money, use it to help put some of New Zealand's eggs into different baskets and save us from our appalling dependence on this single commodity that the Government has forced us into. Win all round, isn't it?

That's a bit negative. Our Dear Leader says prices will rebound - do you not believe him?

Certainly they doing us a favour...just like if you're struggling to pay to mortgage, selling your house to a foreigner for extra money would be great for your home and kids. Sure you'll be homeless. Sure you'll have to bid against those foreigners for a new place to live. Sure in the future if you want to live in a house, or for your kids in a house, in a future you have to bid against those people just to get back to where you were.

OTOH.... if we find a way to make the dairy farm work - maybe not as a [pure] dairy farm - that is better for us, our family, our future, and others in our culture.

Yup, selling the farm is a bad move.

It will be interesting to see how many dairy farms sold to overseas investors will keep them as dairy farms.

Food production world wide is getting more and more precious and important.

And MAF has just approved Monsanto corn to be planted in NZ.....welcome GE crops, anyone? More roundup? Less bees?

We don't learn....

It's depressing, so it is.

crooked MAF/Nats

Do you have a link re MAF GE Corn planting being allowed?

Is not "selling the farm" an old truism for a dumb self destructive move.

Only in Once-Upon-A-Time-They-All-Lived-Happily-Ever-After land

A good few herds have already been physically exported by the clever chaps at Fonterra.

https://www.tvnz.co.nz/one-news/business/live-cattle-shipment-boosts-fo…

Real "win / win" indeed. Next they will be letting Chinese convicts in to milk the cows on Chinese farms here.

All I'm saying is that we can't have it both ways. If we're saying that dairy farming has now become a hopelessly dodgy business and New Zealand is far too dependent on it, then we ought to be glad if Kiwis are getting out of it and leaving the foreigners to waste their money on such unprofitable enterprises. On that premise it's a good thing if some dairy farms are sold, bringing new money into the country which can then be put to other uses (ie, diversifying the economy).

If we do think it's a bad thing that foreigners are buying dairy farms, then that must mean that we do think dairying is a good and valuable industry to be in longer term, so where is the problem with its ongoing share of New Zealand's economy?

Foreigners _aren't_ wasting there money on it.

They can achieve vertical integration, they can move all their dirt and risk offshore to NZ, they have asset protection against their own government forces. But none of that is good for NZ.

Even worse it takes more of our _CAPITAL_ASSETS_ and puts them in foreign hands. That is B.A.D.

hmmm you might not be understanding what is so bad....

So you don't want that asset right now. (a bit like not wanting dinner right after eating lunch)

But once that capital asset is sold, especially if its land or IP, then it is _gone_.

If ever you want it for something else, or you see a need later, tough it's gone...and because you didn't want it there's extremely high probability that you didn't even get a significant perpetuity from it.

just because dairy looks bad _now_, isn't a guarantee that the land/IP isn't worth a lot in the future.

In fact bidding really high, then flooding the market to crash the prices...is CLASSIC takeover practice. Sell that dairy land in any significant way - you can _guarantee_ the persons who now have contorl of the market will jack the prices on you... and too late for you now, you'd have to buy at the top of the market...if they'd even let you have your land back at all!! (aka "beads'n'blankets" or "Asian tide" techniques - which is why historically Korea is wary about Chinese traders)

Attachment to export of commodities will indeed, for a period, make us rich. And it will also, just as certainly, for a period impoverish us. The heights and depths of these periods, and their extension in time, are largely if not completely out of our influence. The factors are external to the commodity producers.

Because the factors are external, out of our hands, all that Fonterra, government ministers, economists and other commentators are able to offer is the plaintive platitude that ‘prices will rise’. No-one knows when they might rise or by how much. The influences are ‘out there’, external, out of our influence.

Saying that prices will rise is, in terms of business or economic planning, no more than the logic of day-dream. Yet, New Zealand appears determinedly, again and again, to prefer this sort of day-dreaming to getting on with developing non-price oriented competitive advantages. These are not mysteries – at the risk of sounding preachy, these factors are well researched, well understood, and exploited by successful businesses in every corner of the globe.

They're things like invention, innovation, discovery; specialist or complex product offerings; distinctive expertise or skill bases; distinctive organisational competencies; intangibles such as recognised leadership, reputation, authenticity; intellectual and creative assets; intellectual property, patents, copyrights, registrations; cultivated customer relationships; barriers to competitor entry, barriers to customer exit; organisational and cultural assets; brand influence and loyalty; etc; etc.

These directions require more focused work than commodities, and this may be why they’re not commonly favoured in New Zealand. We seem, from government down, and through our major industries, generally to go for the apparently easy, less demanding outcome. We centre the country and our economy on relatively unimproved or relatively easily replicated product. If there's value to add, we tend to leave this to others.

But the truth is also that our national attachment to commodities will not securely support an added-value society – meaning education, healthcare, ACC, welfare, and the rest of it. And the result is an economy continually blown one way or another by external forces, and perpetually in need of borrowing to fill the gap between a commodity economy and an added-value society.

" Companies selling commodity like products should come with a consumer wealth warning - Danger - competition can be injurous to human wealth " Buffett said it all some years ago.

commodity prices over time tend to fall.

this is supply and demand. as demand lifts, alternatives become more viable (increasing supply).

in the mean time pressure from buyers needing to absorb their own costs push down what the can bear.

The cost of getting commodities to market is $X, which has debt attached; when the debt is paid back, the normal practice is to soften selling offer to increase market share, also using the "nest-egg" business to subsidise future leverage. resulting price competition pulls down price in a commodity market - where in a consumer market, the old product line would be "dogged off" (stopped) and a new one made or rebranded - this is not possible in a bare commodity product/service (so in markettng terms the market gets very "mature" and as such is identified by dropping prices (and profitability) ).

Universities are a glut on the world market.

There never was a pinetree paradox. Radiata grows at the same rate in Chile and they have cheaper labour. Then there's Brazilian hardwoods planted at scale - growing at twice the rate as radiata.

At least with the slumping commodity prices the peak earth stuff can be given a rest till the next upswing in the business cycle.

About 40 years NZ had a bunch of mature pine trees. They were having real issues selling off the lumber, and NZ-inc didn't have the money to invest to build sawmills or anything else to value add to that volume.

Rather than do something sensible the government of the day sold the _forest_ including the land, in order to get some cash. Pine tree paradox - plant a popular commodity...20-25yrs later, no market for it. How do you even recover your initial outlay let alone your target investment yield.

Because it's a commodity, it costs _more_ money to find something useful to do with it.

But if you sell off the land, and pretend the trees were valuable, then you get rid of the whole problem....so what if you end up tenant paying rent in your own country. It's not like the government actually paid for the land in the first place.

Do some reading before you comment Cowboy. "...pretend the trees are valuable". No need to pretend there is about $5 billion in annual value there and 20k odd jobs. Compare running sheep on steep country to radiata and pines win hands down. As for the land being sold learn about cutting rights.

"Forestry Corporation owns the forest crop, not the land on which it is planted. The land is still owned by the Crown and will not be sold."

"The partners in Kaingaroa own the harvesting rights to the plantation with most of the underlying land owned by local Iwi."

It is curious that, a decade ago, as the exchange rate (NZD/USD) increased, to much wailing and gnashing of teeth by the dairy industry, so did the value of milk products on the world market. No one seemed to be able to explain it, other than the possible supply/demand argument. Equally curiously, the exchange rate is now tracking down as milk product value falls. It could be argued that this is because of the (lack of) demand/supply situation weakening our economy. Or it might be, as others have commented, that the US economy is stronger and the USD is rating higher against other currencies as a consequence. I'd hesitate to attribute any causal relationship.

The dairy industry has experienced these sorts of swings over the last century or so but "race memory", particularly amongst journalists and media commentators, has dimmed and we tend to see the latest as the worst, if not the only, disaster in recent times.

I am concerned that many commentators, particularly, economists (unfortunately), seem to see value-added dairy products as the only salvation for the dairy industry. That cannot happen. The highly valuable products tend to be short-run (i.e. small quantities) and often using minor components in milk. Lactoferrin, manufactured by Tatua and Westland, is an example. But to produce a few kilograms, hundreds of thousands of litres of milk have to be processed. So what do they do with the rest? Process it into so-called commodity products. This is even more true of the esoteric protein products produced by Tatua over the years. Runs were often less than 10 to 20 tonnes, and one-offs, but were worth maybe $200,000 per tonne or more. It is, perhaps, worth noting that as the production of (i.e. the market for) value-added products increases so does its value start to fall. Eventually, as with infant formulæ, they, too, become "commodities".

I perceive two problems, one of which can be addressed, the other being in the "lap of the gods".

The first is that the Dairy Restructuring Act requires Fonterra to take all milk offered to it. Removing this requirement would lessen the pressure on Fonterra to keep increasing its production, and would reduce the desirability of dairy conversions. It might also take pressure off farmers who are pondering whether or not they can reduce production (although, in reality, they should not because their overheads are high whether their herds are producing milk or not).

The second problem is a corollary of Parker's Pine Tree Paradox. Until recently the only effective net milk exporters were NZ and Australia, which is why Fonterra is said to control 35% of the global milk product trade. However (as a result of the Pine Tree Paradox?) Europe and the USA have become net exporters too. This will undoubtedly have an effect on world prices. And it will continue for as long as they see profit in it.

Will the cost efficiency of pasture based milk production triumph? I have no idea but I consider that clamouring for "value-added" production will be of little avail. What might work is to return to the days of carefully sought, individual, contracts backed by high-quality products, albeit commodities, much as the New Zealand Dairy Board used to arrange. Even with its faults, the Boards methods didn't seem to be "broke". The "fix" doesn't seem to be better, although, to be fair, dairy farmers have received good returns over the last decade or so.

Until international geo-politics get in the way

China establishing 100,000 cow dairy farm to supply Russia

http://www.nzherald.co.nz/northern-advocate/news/article.cfm?c_id=15034…

Gary K, what I'm forced to wonder about the dairy industry is whether it has truly or fully exploited the added-value advantages that are (fast becoming were?) available in the New Zealand environment. For instance, I can't understand the enthusiastic introduction of these vast indoor factory farms. Volume, sure. But added value?

I look at other rurally-derived products, such as New Zealand super-premium pet foods, where qualities that we might take for granted - such as 'grass fed', 'pastured', 'pasture-raised', 'non-feed lot', 'free-roaming' - etc command significant international value. (I'm not in this or the dairy industry.)

In a world where consumers - high value consumers - are ever more concerned with qualities of origin of this sort, I cannot understand the willing degradation of our natural environmental advantages. What products need to do is hold a mirror up to the attitudes of chosen consumer groups (which should be the moneyed ones) or, in other words, do their thinking for them. These qualities of origin, husbandry, etc, are particularly important among urbanised, middle- and upper-earning consumers - which we're told is Fonterra's market.

We can discount the consumer preferences - for example, laugh sometimes at the organic thing - but these are their truths, and they're willing to spend for them.

It seems to me that if the industry wants to chase its tail into low-value commodity positioning, our continuing environmental degradation is a pretty good way to accomplish it.

Funny the meat industry dinosaurs are still going , and meat is doing ok

Great comments Gary K......

I too agree that chasing the value added component of milk with large volumes will eventually see a fall in that value, and then you are no better off. What Tatua does is very niche, and small volumes made specifically to the client requirements.

Fonterra undoing is (as you say) is that it HAD to take new supply under DIRA, and so had to allocate capital to extra capacity (tankers, stainless). If the DIRA is re-formulated to remove this requirement then Fonterra then has more certainty for capital expenditure, and growth. Rather than constantly chasing its tail to deal with extra milk. They will only take new supplies if they can make extra $ (payout for the shareholders).

What Fonterra hasnt done well is to market our product as 100% safe, Natural and 100% quality. People will pay a premium for this. Thats the value added for a commodity based company.

Plus, Fonterra hasnt built quality brands. Brands that you dont even know are owned by Fonterra. ......think Nestle......they own Nespresso. A top brand, not directly related to dairy........but consumes milk.

Yeah it's gonna interesting where meat production will go in the long run. A chinese investor has just bought a couple of sheep and beef farms in our area. I would say he's just land banking. Not sure what this will do to the industry as this kind of thing gets going. The super rich holding the best properties won't be too worried about production or what's happening to the local market prices for beef and lamb.. Can't see production increasing by this form of investment.

Of course it won't be, there is no checking to see if some of these pie in the sky plans for land selling into the hands of foreigners are actually benefiting the country at all

Not so fast

If he is a Chinese National and the land areas are greater than 5 hectares each he would have had to put up a development and operational case to the OIO. If you know when they were purchased you can go to the OIO site and see the decision and approval. Not sure a simple "investment" is an acceptable case. If just land banking and the land is not worked and starts to revert you can pot him

Of course if he is a naturalised New Zealander with a New Zealand passport no problem

I believe the guy has residency, but it will be interesting how it is run, he doesn't live in the area. Cashed up land bankers don't add anything to the industry.

Well land values are going to need to drop substantially if beef are going to be viable on an ex dairy farm ,no one seems to have an answer but the invisible hand maybe more of a fist

That graph shows how easy National have had it in their terms, there was quite a bit or harking on about how Labour had the luxury of high commodity prices during their last terms, but National have had it even easier, but still have yet to manage to make a surplus once, while Labour did it 9 times in a row.

Case closed National are the worst economic managers of the country, Labour always do a better job of it.

that has always amazed me when you check the history and how many times national have run up debt and sold everything they could find.

and how many times labour have paid down debt

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.