ASB's launch of market leading rates for home loan terms of 3 years and longer has pushed into focus the spread of offers in the home loan market.

The differences between the lowest and highest carded rates have now widened considerably.

In fact, for terms from two to five years, they are their widest in 2016.

And the only reason they are also not their widest in 2016 for the 18 month term is that the 3.95% HSBC Premier rate has now ended. It has been replaced with a 4.19% rate.

And HSBC had a 3.99% rate for one year that ended in January and during that time the variations were wider for the one year term. However since then, the current one year spread is the widest.

Usually, carded rates are generally closer than they are now. That brings into play other non-rate factors and incentives.

But when they diverge by as much as 0.60% to 0.80% there are clear advantages to those offers at the low end of the range.

Bankers, their treasurers and their economists like to talk up their 'cost of funds' and 'rising risk spreads' but based on what we can observe this is more about padding margins that real funding pressures.

Each bank's NIM (net interest margin) can be read in their disclosure statements and they can be compared with the weighted sector results in the RBNZ monitoring. (See S20.) And the latest data available shows that this margin is still above (just) their ten year average. Profitability is handsome, so there is no margin compression occurring. The talk of 'margins under pressure' is just banks talking their book, and they have a loud voice.

The variation in carded mortgage rates is not a variation between challenger banks and mainline banks. Some of the most competitive rates are being offered by main banks. So the 'margins under pressure' reason sounds hollow.

Wholesale swap rates have been low for some time.

Credit spreads, as revealed generally by the Australasian investment grade CDS index suggest that these have been declining in 2016. Specific offshore bond term sheets for bank borrowing also suggest very low credit spreads.

The main aspect holding costs up is what banks pay for retail term deposits. This is an important funding element necessary to maintain their RBNZ required core funding ratio. Unfortunately for savers, household bank accounts are very flush so the competitive instincts around attracting retail savers is currently rather low (to the distress of many in retirement). But the brutal fact is banks don't need to compete hard for this money. Savers are generally lazy and don't shop around like borrowers. And many savers still are very averse to risk so won't transfer funds to instruments that might put their capital on the line (such as managed funds - for example, even default KiwiSaver funds have been delivering far better results than any term deposit).

Despite this, and to their credit, banks have kept their term deposit offers reasonable in the circumstances. (It is those who hold their funds in savings accounts who have taken the biggest reductions.)

The point about mentioning bank funding offers is that banks still have options to reduce what they offer savers and savers probably are facing some downside.

Banks who actively manage their 'replicating funding portfolio' (that is fancy banker talk for managing the lazy money savers are holding in the bank and who show no sign of moving it) will be in a position to be more competitive on the home lending front.

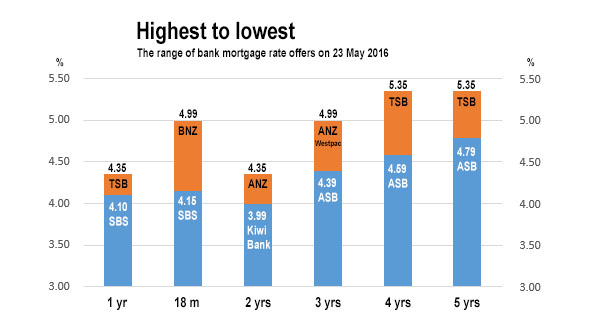

Here is a graphic that shows which bank has the lowest, and which bank has the highest carded mortgage offer starting today (Monday, May 23, 2016):

It may be a fleeting perspective. With variations this wide, it seems unlikely banks at the top of the range can stay there without leaking market share. Shareholders punish managers who leak market share.

The full comprehensive list of all home loan carded rates are here.

Here is where fixed rates stand after today's changes:

| below 80% LVR | 1 yr | 18mth | 2 yrs | 3 yrs | 4 yrs | 5 yrs |

| % | % | % | % | % | % | |

| 4.25 | 4.89 | 4.35 | 4.99 | 5.20 | 5.30 | |

| 4.25 | 4.25 | 4.19 | 4.39 | 4.59 | 4.79 | |

| 4.25 | 4.99 | 4.19 | 4.49 | 4.99 | 5.15 | |

| 4.29 | 3.99 | 4.75 | 4.90 | 4.99 | ||

| 4.25 | 4.95 | 4.19 | 4.99 | 5.09 | 5.19 | |

| 4.25 | 4.35 | 4.35 | 4.65 | 4.89 | 4.99 | |

| 4.19 | 4.19 | 4.19 | 4.49 | 4.79 | 4.99 | |

|

4.10 | 4.15 | 4.15 | 4.65 | 4.99 | |

| 4.35 | 4.35 | 4.19 | 4.79 | 5.35 | 5.35 |

In addition, BNZ has a fixed seven year rate of 5.55%, while TSB Bank offers a fixed ten year rate at 5.75%.

2 Comments

yes. New Zealanders are very risk adverse. Given the behaviour of the financial services industry what would you expect. I think the only reason the Financial Services obtain any investment at all is that you always need to have some there and some cash. And there is shortage of alternatives.

Being about to whip down to your local council and buy bonds there over the counter would be a good alternative.

Integrity is a very important quality in a bank. If they go around saying they are under pressure with funding costs and it is impacting them in there ability to pass on OCR cuts they need to be telling the truth.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.