By Jenée Tibshraeny

National is proposing to tinker with the tax system to cheer up baby boomers upset by the low interest rate environment.

Ok, so the party didn’t pitch its idea quite so crudely in its economic discussion document released on Monday. It said:

“Savings (including retirement savings) are currently taxed relatively heavily while borrowing to invest is taxed relatively lightly. This is exacerbated in the current environment of low interest rates and steady but positive inflation.

“Savings are taxed at the full marginal rate on their entire nominal returns, including the inflation component. Meanwhile, borrowers are able to deduct their full interest payments, including the inflation component, from their investment income to lower after-tax returns.

“Not accounting for inflation in the tax system creates distortions in economy-wide investment and savings decisions and the allocation of capital…

“Is there merit in allowing savers to deduct the inflation component from their interest income to help address New Zealand’s low level of private savings and reduce the high effective tax rates on savings?”

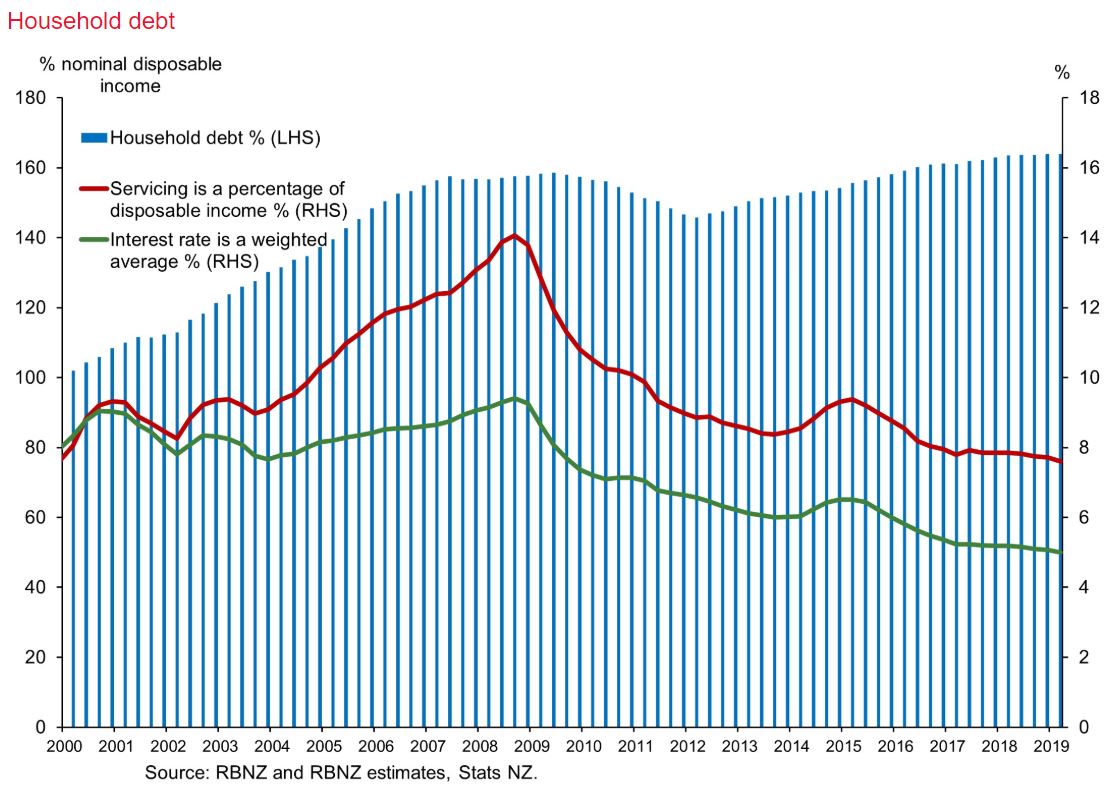

Yes, household debt in New Zealand is high.

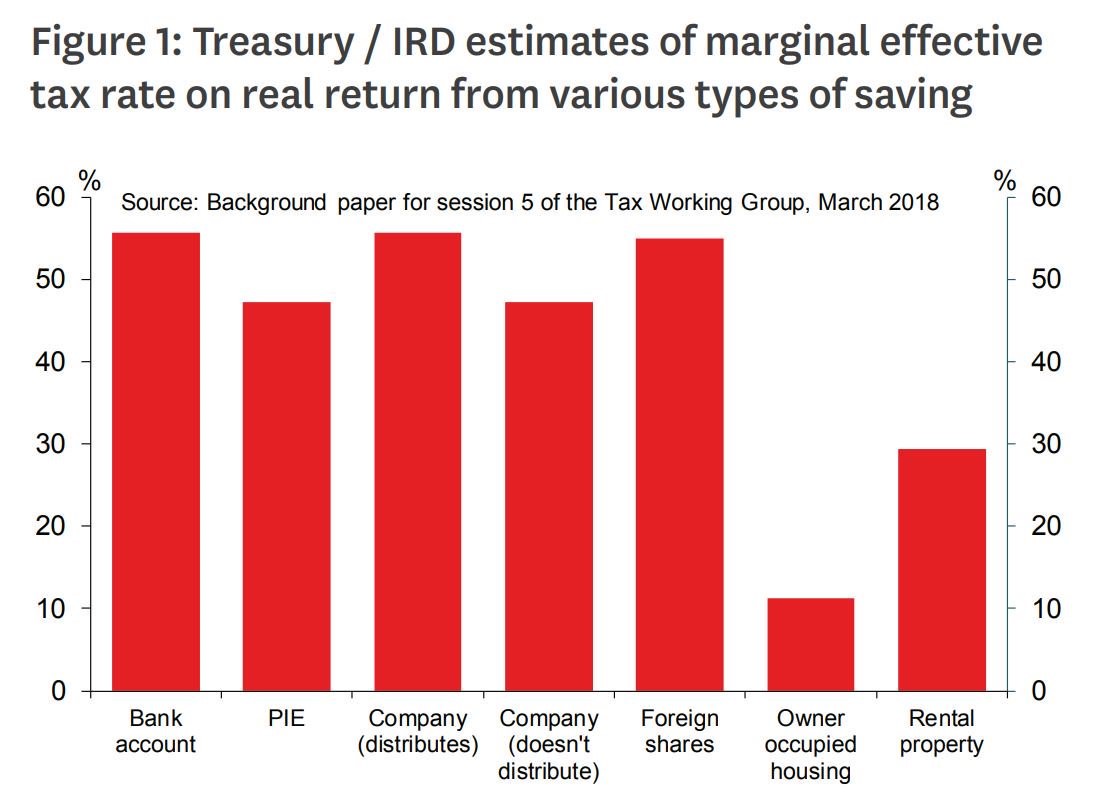

And yes, the marginal effective tax rate on bank savings is relatively high:

But no, deducting inflation from interest earned off savings isn’t the way to address these issues.

Un-evening an already uneven playing field is a bad idea

Firstly, National can't say what it means by “savings”. Is it referring to interest earned from the $181 billion households have in bank deposits?

It mentions “retirement savings”. Does that mean KiwiSaver investments? If you get inflation deducted from your KiwiSaver returns, shouldn’t you be able to deduct inflation from the returns of your “savings” invested in other PIE funds?

And what if your “savings” plan involves investing directly in the bond market? The low interest rate environment is also detrimental to you. Do you deserve tax relief?

As for investors who “save” by investing directly in equity markets - the economic uncertainty causing interest rates to fall might be damaging their portfolios. Why can't they get tax relief?

My guess is that in order to keep this policy simple, its application would need to be limited - perhaps to bank deposits and maybe KiwiSaver - at which point a distortion is created in the tax system New Zealand has worked hard to keep simple.

Distortions prevent money from finding its way to where it’s most productive.

In this case, already well-off baby boomers, who happen to make up a large portion of the voting population, wouldn't have to change their behaviour in response to normal market forces, like everyone else would.

You can't respond to a cyclic issue with a structural change

The tax system needs to endure different phases of the economic cycle. It can’t be used to provide a favoured class with relief during a particular phase of this cycle.

The Reserve Bank has talked about low interest rates being the new norm, but what happens when they pick up? Would National be keen to provide savers with tax relief then?

And what if the inflation rate surpasses interest rates? IE, what if the discount became greater than the expense?

National didn’t like Labour and the Greens’ attempt to use a capital gains tax to make housing more affordable for first home buyers.

Now it wants to use the tax system to make bank deposits more lucrative for savers - ironically many of whom would’ve benefited from untaxed capital gains earned selling property that sky-rocketed in value.

If it was sincerely interested in bringing more fairness to the tax system, it would address the glaringly obvious issue shown in the above graph - that the marginal effective tax rate on property is way below that of other asset classes.

More saving = less spending = lower interest rates = problem exacerbated

Putting the fundamental issues of distorting and misusing the tax system to win votes aside, allowing savers to deduct inflation from interest earned simply doesn't make economic sense.

It doesn't encourage people to put their money where we really need to them to put it - in businesses to grow the economy, in our capital markets, in our debt markets to support infrastructure investment.

Sure, if we’re all going to make the most of the low interest rate environment and borrow and spend to stimulate the economy, banks need their coffers replenished.

But this policy is counter-intuitive. It discourages the stimulus needed to prevent interest rates from falling further… and hurting savers even more.

I briefly spoke to National's finance spokesperson Paul Goldsmith on his way to Caucus on Tuesday morning (after writing this piece). He explains his rationale behind the potential policy:

69 Comments

Yes, good points and fair questions. But there are some social issues in the mix, as well. For instance, does reduced investment income and increasing fixed costs, insurance, rates etc, mean enforced tightening of the belt to the extent that some retirees go short on good diet, home heating and health insurance, amongst other things. Hunkered down and depressed even. So at an age and stage of life when health problems escalate for obvious reasons, might this not impact significantly, on an already stretched public health system?

You are correct about the uneven playing field. 5% of the population pays one third of all income tax, while 50% of the population pays only 8%. https://ibb.co/YTGJNJP

I recall DC quoted recently from stats, that are no longer being published, that 14% paid 60% of all personal tax? May not have that quite right?

5% of the population must be on such obscene numbers if they're shouldering 33% of the income tax burden. Maybe if the wealth was spread around, that 50% of the population might be in a position to contribute a little more from their pay.

What you’ve said goes without saying. The top 5% pay disproportionately more tax because they earn more and if the 50% earned more they would be required to pay more. But how do you propose the the wealth be “spread around”?

A land tax (like we used to have) and a citizen's dividend would do it.

Could go for a land tax as long as there is a poll tax vs rates.

Proportionately more INCOME TAX.

A lot less GST as a % of income.

NZ has a regressive tax system.

No personal allowance either.

What the government really needs to do, but won't is make retirement income insured - ie contributory, like National Insurance in UK and combine it with an insurance product for care home fees.

Stop taxing people for working.

Perhaps, for a start, as simple as a tax rebate on health insurance. That might well encourage people to invest into and take responsibility for their own healthcare, reduce the burden accordingly on public health system? But then, on the other side of that, there was Mr Cullen at his cynical best. “ If you can afford health insurance, you don’t need a tax break.”

We have been down that road before and thru it out. Howse about the politicians start thinking about benefits for all New Zealanders instead of pandering to specific groups just to get elected.

First start would be an over hall of our MMP electoral system. Sick of the dog wagging the tail of the dog. NO to list MP's MP must be voted in by the PUBLIC

Your original post about the income tax system is a good start.

Do you have the source for that image? (I'm not doubting it, just wondering where it came from).

ACT Party tweet

OK, I also found substantially the same information from the IRD website. If anyone wants to be able to use the information without adding page views to the ACT Party Twitter account, it's here: https://www.classic.ird.govt.nz/aboutir/external-stats/revenue-refunds/…

The only thing uneven about that is how there are 50% of people earning less than $30k.

I'm in that top 3% and more than happy to pay that tax. I can only hope others in the same fortunate situation are thankful for their wealth, not moaning because the poor aren't paying enough.

Nice humblebgrag / virtue signal. Everybody, please note that this guy is in the top 3%. For every 100 people he passes in the street, he earns more than at least 97 of them. Very modest though, not the type to go plastering his income level all over the internet.

Yeah, bragging about your income is really tacky.

Unlike bragging about your various investment properties, the height of class.

Who?

I'm sure one of them will come in to this post by the end of day tomorrow. Some random quote from a motivational speaker or some spattering of exclamation marks about how Christchurch is very stable, you know who I'm talking about.

Never seen a spruiker brag about how many properties they have on this site (not saying it’s never happened). In fact I’ve noticed that they are all quite secretive about it.

I don't think you need to specify a specific amount to constitute a brag. northman46 doesn't meet that criteria either.

Noted. Now perhaps think about the point actually being made - those of us who do well through luck of birth, education, opportunities and whatever else the world has thrown our way should be decent enough to acknowledge the role of luck and not resentful about supporting those who drew worse cards.

Or stop voting for a party that constantly puts your group (Boomers) ahead of everyone else? Next the Gold Card will be decommissioned in 2037..or when last Boomer expires.

Sure, fine, good point. Bragging wasn't my intention. But you've completely ignored the point.

You can do well without being bitter and selfish.

The numbers change quite a lot when you include GST. Looks like you have only included income tax, you should specify this.

The big problem with that being we only count some sources of income and not others. Thus we have massive moneymaking that's getting off tax free while people working in productive enterprise have to bear the load.

And yes, as Blobbles notes, by limiting the discussion down so much to specifically only one type of income tax, you also miss GST.

Wow those 95% are such lazy bas$#5ds and need to get of their collective ar#$ add work harder. Bludgers.

“Distortions prevent money from finding its way to where it’s most productive.” - Yup, just look at what inflation targeting has done for starters.

Sorry Jenee.. Is it a bad idea or an unclear idea? The article is titled to suggest its ill-conceived then you cite a lack of clarity around how the policy would be implemented and applied and what is meant by savings.

You seem to fill in the blanks then conclude its all a bad idea. Please tell me how you have come to this conclusion given the unknowns you cite.

You ask the question about Kiwisaver? Equities? Bonds?... all good questions then completely undo your article with "It doesn't encourage people to put their money where we really need to them to put it - in businesses to grow the economy, in our capital markets, in our debt markets to support infrastructure investment".

Surely it would benefit capital markets if Kiwisaver, Equities and Bonds were included..... but as you say, its not clear what National mean by savings or retirement savings. So say that.... not fill in the blanks for us.

All I can take from this is Jenee doesn't have any real savings and will have to retire at 67...so, "nothing in it for me so ill make up some economic rationale as to why its a bad idea".

Jenee - why not try compounding the benefit of not paying tax on the inflation component of your kiwisaver returns until you are 67 and then let me know if you still think its a bad idea.

Deducting inflation from interest earned on savings is a bad idea regardless of how "savings" is defined in my view.

Your personal attacks are unconstructive and distasteful too just FYI.

I take it you’d prefer to tax the interest (including inflation) as well as the value of the savings themselves? I.e. tax the savings even if no interest is being earned. Like bff Geoff wants to.

Yet you fail to address my point. You ask many good questions about the lacking detail but then seem to answer them yourself and conclude its a bad idea.

What if bonds, equities, kiwisaver were included and promoted investment in capital markets?

Where are the personal attacks? All I can see is he's using your first name in his response.

Thank you... personally I took exception to the tone in the article directed at baby boomers... and I'm not even one.

From my perspective this is an opinion piece and the author has taken exception to someone disagreeing with her opinion.

It is definitely an opinion piece. Sadly, the opinion aspect is selective in nature. The soundclip at the end is an interesting bit to listen to. Always have to laugh when the interviewer tries to couch questions such that there is no possible way to provide a rational answer.

Yes, I recognize that it is labeled as an opinion piece, so it does not have to abide by normal journalistic standards. I just wish that opinion pieces would stick better to factual foundations instead of starting with a conclusion and using only selective data to support that conclusion.

nothing in it for me so ill make up some economic rationale as to why its a bad idea

Anyone who understands inflation will realize that the real inflation has not been in consumption of goods and services, it's been in assets (property, equities, etc). Bridges is just practising populism, not offering any kind of real solution to appease savers.

So boomers happy with falling interest rates the last 30 years meaning paying off the mortgage got easier by the decade while asset prices sky rocketed - what a dream run! But what about young people who have been struggling to put together a deposit for a house - where has the care been for them the last 10 years of National power?

8.5% and more prior to 2008 GFC. But yes certainly that is half of the mid eighties rate(s) prior to the 1987 equivalent. So in that context, yes you could say they have fallen overall, for thirty years one supposes.

I think inflation should be taken into account when quoting high interest rates.

Problem from Central Bank viewpoint is that interest rates are lower than inflation.

Negative rate means just that - and so much of world already has them.

Inflation needed to erode debt but if interest rates negative or too low, bond holders will not buy government debt.

That is a big problem and banks seem to have no answer except current playbook.

If you want to increase consumer demand I am afraid, best way is to redistribute to lower half of population who have higher propensity to spend.

Of course Tax Group has refused to do that, as have government

Not to mention a good portion of them would have taken out a mortgage during a period of high inflation (hence the incessant moaning about 20-something percent mortgage rates) which is perfect on a table loan, particularly a loan that's only a very small multiple of their annual income.

Young people are struggling to put together a deposit that's essentially the same multiple of income as a Boomer's first mortgage would have been. Why were people taking out mortgages in the 70's? Didn't have the discipline to save when the banks were throwing money at them.....what a frivolous bunch.

Summed up many years ago in Punch when it was around, a cartoon of two elderly banker types, one exclaiming to the other, “in my day it was our ambition to pay off the mortgage, nowadays the ambition is to get one.”

Indeed, would be pretty self-obsessed of folk to hark and celebrate dropping interest rates because it benefits their portfolios, then want a National party to exempt them from the downside of low interest rates - lower interest on their savings - instead of them standing on their own two feet and paying their own way.

At some point surely there's a case for living up to the claims of having done it all on one's own two feet.

Great analysis and a great quote:

“Putting the fundamental issues of distorting and misusing the tax system to win votes aside, allowing savers to deduct inflation from interest earned simply doesn't make economic sense.”

I might have the math wrong on this but wouldn’t high inflation/high interest rates been worse for this problem than low interest rates/low inflation.

If interest rates are 2% and inflation is 2% and tax is for ease of calculation 33% then you’ve lost what? .65% or something.

But if interest rates are 20% and inflation is 18% then you’ve lost like 4.5% or something. So actually much worse in late 80s by my reckoning.

Anyway, best they can do is knock a couple of points of the PIE. But unfortunately we can’t cut rates because boomer retirement and health costs. Fast forward five to ten years and we’ll probably be raising taxes.

"It doesn't encourage people to put their money where we really need to them to put it - in businesses to grow the economy, in our capital markets, in our debt markets to support infrastructure investment."

This is exponential growth you're advocating? There seem to be minds which don't get the problems with exponential growth, nor where it is vis-a-vis our little planet. Trump annexing Greenland, doesn't give the US a doubling-time, nor does South Basin oil - if its there - give NZ a doubling-time. The planet is up against the limits-to-growth now, and ínvestments' are really bets that it will get bigger in the future. So were the interest-rates that deposits used to earn. These signals are there for the thinking.

Th problem now is that 'savings' cannot 'earn' what was a temporary rate of return (but which short-term thinkers think of as 'normal'). So the Nats are trying to dig a hole under the car as it sinks into the quicksand - to keep a margin (at least in people's minds).

Bit like bailing the Titanic with a bucket - bigger problems are afoot. We are entering a low, then no, growth paradigm. Sorry to all those whose training or belief or psychological need is for this to not be so. Only those who address this overarching issue, will remain relevant.

Wow, how innovative of the tories, what next....announce the health budget will be sponsered by Phillip Morris? And the tories argue the pgf is a pork barrell affair? I can't think of a more self serving shortsighted policy for loaded boomers who can't be bothered educating themselves in how to invest across mixed asset classes. In many ways that succinctly sums up why the NZ economy is so stagnant, we lack financial sophistication. Savings account...what is that anyway?

Hi Jenée

You are not often incorrect, but you have the wrong end of the stick on this issue. Ever since 1923, when Jacob Viner pointed out that the inflation component of interest income is not income but merely compensation for inflation, economists have been nearly unanimous that (i) there is no good economic reason to tax the inflation component of interest income and (ii) there is no good economic reason to allow people who borrow to invest to deduct the inflation component of interest income from their taxable income. Nobel-prizing winning economist Franco Modigliani is merely one of the highest profile economists to make this case. The United Nations manual on the System of National Accounts (1993) recommends that GDP measurements should be adjusted so that the inflation component of interest income is not recorded as part of GDP (although most countries do not do this.) The tax falls mainly on elderly and unsophisticated lenders (those who do not hedge against inflation by buying shares or property) and for this reason it is sometimes called the Widow’s tax as many elderly lenders are in fact elderly women. The great beneficiaries of this rule in New Zealand have been property investors and farmers; and there are good reasons to believe that the excessive taxation of interest income is part of the reason why house prices have gone up so much in New Zealand since 2000. There is a well established literature on most of these points.

The situation is worse in New Zealand than inmost other countries because in most countries savers can hold interest earning assets in special retirement income saving accounts that are taxed on an “Exempt-Exempt-Taxed” (EET) basis that means that the inflation component of interest income is effectively exempt from tax. New Zealand changed its tax system in 1989 and got rid of its EET system – a measure that other OECD countries decided so was so daft that none followed. As National observes, this means New Zealanders who save by lending money are amongst the most highly taxed people in New Zealand. If NZ does not reform the taxation of retirement income savings in line with standard economic theory and normal international practice, changing the tax on the inflation component of interest income is a sensible step.

One of the more disappointing aspects of the Tax Working Group is that they got this issue completely wrong. I suspect it is because the group included very few properly trained tax economists - or because they lacked people with guts to stand up to Cullen, who has been wrong on this issue (but not all issues) for decades. (In fairness to Cullen, he has been advised by IRD officials for decades, and they have been adamantly opposed to the exemption of the inflation component of interest income from income tax for decades, despite finding no support from economic theory for their position. Their justification is that it is administratively complex, as if they had never heard of the computerised tax records.) Actually, that statement is not really true – most of the Tax Working Group report was disappointing, partly because large parts of it ignored standard economic theory as well as normal international tax practice. It is hard to believe the Tax Working Group started from the argument that income from different sources should be taxed at the same rate when that position was rejected as a theoretical proposition nearly fifty years ago by the Nobel prize winning economists James Mirrlees and Peter Diamond – and it has been rejected in practice by almost all OECD countries (except New Zealand) . This is one of the reasons why taxes on businesses and capital income are so high in New Zealand relative to other countries, as National has noted.

National should be given some kudos for their position. It might even help young people, as it will reduce the incentive for landlords to bid high prices to purchase investment properties as an alternative to investing in over-taxed interest earning taxes.

Andrew

Hi Andrew, really insightful comment. Thank you. I might need to give you a call to discuss further. Particularly keen to unpick this statement a bit further:

If NZ does not reform the taxation of retirement income savings in line with standard economic theory and normal international practice, changing the tax on the inflation component of interest income is a sensible step.

Saving = less spending you say.

This is a problem for "growth".

There are so many issues with growth it is difficult to know what to say.

Income growth should be key to spending - NOT doing our damnedest to get people to get into MORE debt.

Income growth rests on productivity which NZ has abysmal record on in last 15 years.

Proportion of savings contribution to spending by over 65s is very hard to estimate.

Seems a good joke to make pensioners work another 2 years and then give them a few more crumbs re savings tax relief. Pensioners already have most of the wealth in NZ

Try asking what income and productivity are?

The proxy you are advocating the accumulation of, is an expectation that there will be more stuff to buy in the future. The raw material for that stuff is not only finite in nature, it's being drawn-down best-first, so not only does it get scarce, it takes ever-more energy to extract per ton.

Given that labour is less than 1% of 'work done', productivity gains are 99% energy-efficiencies. They inevitably follow a law of diminishing returns - the laws of thermodynamics being immutable. That's why they have plateaued - although you could fudge it to fool yourself if you lowered wages in the direction of none. Which is what we did by offshoring processing.

Let's just toss the family home into the mix as well - the other great distortion. No tax on that return and in another oddity, also exempt as income or an asset for our benefit testing rules. The saver with no home misses out in all areas.

A government funded retirement for everyone, with no need to contribute at all and no means testing is crazy. It is even more crazy (and plainly criminal) as not to properly fund the plan every year out of general tax income. Such a plan is simply a bribe to the generations who get it and is financially unsustainable. The same as all other "subsidised" things. The subsidising party will need to either ration them (as they cannot afford the actual needed quantity) or the consumers will waste it (the example is NZ houses build in 60s and 70s, cheap energy meant no need for insulation, You save your own money building the house and spent other money to warm it up).

The only thing that makes a subsidised system work is constant population growth, and a constant increase in the number of people working and a constant increase in taxes from these workers. Change any of that, and the system will collapse.

Well said - I'd have added that betting on the availability of future stuff (essentially resources and energy) has to be guaranteed. Meaning that x litres of proven oil and y tonnes of chip and bitumen, need to be earmarked before you build a greenfields road. And that the food and energy required to support the old, will be there when they're old.

Planetarily, we are orders of magnitude past being able to do that.

Given the current lot made wild promises, yet delivered next to nothing except higher taxes, hugs and world class virtue signalling, yet still evidently have support, who can blame National for throwing chelsea buns to the hoi polloi?

you don't fix one distortion by creating a new one.

you take away the first distortion, I have always thought is silly an investor can deduct interest from their mortgage but a property owner can not, and there are plenty of structures created to take advantage of that

Did National get their caucus to put 3 policy ideas each into a bucket, they did a draw and then vomited the results out in their recent policy announcements?

We shouldn't be paying tax on our savings end of story. Lets remember 20 odd years ago we paid no tax on our savings and then tax was introduced and the overall situation got worse so how was taxing your savings making things better ? what do you suggest, increase the tax on your savings ? You have already paid tax on your earnings, stupid idea to then pay more tax on your savings. The people who have conscientiously saved their money and not just blown it all deserve better. One minute your being told to save for your retirement, the next your being taxed to death and told to blow the rest to "Stimulate the economy" I think not.

B-b-b-b-but Carlos, if we didn't tax savings the Government would miss out on sooooo much tax revenue. Where else would they recover this shortfall from? Taxes on non-productive enterprises such as property investment is out of the equation i'm afraid.....

UPDATE: I briefly spoke to National's finance spokesperson Paul Goldsmith on his way to Caucus on Tuesday morning (after writing this piece). You can listen to him explaining his rationale behind the potential policy by clicking on the audio inserted at the bottom of the story.

I'm more concerned with Jenee's sensationalist headline suggesting that only boomers have enough money to have any savings.

Firstly there are many boomers who are struggling to make ends meet and won't have any savings. and is she saying that no other generation can afford to save? Perhaps a headline that focused on the real issue of that National are looking at the tax treatment of savings.

Agree.... the article correctly highlights some questions that National will need to define how this would work.

I would think baby boomers would be somewhat dismayed they have for years paid tax on their nominal returns when subsequent generations would only pay tax on their real returns. The compounding benefit of that is enormous and for a young saver would be significant.

.....is NZ any different? I suspect not.

"Average mortgage debt among older Australians has blown out by 600 per cent since the late 1980s after accounting for inflation"

https://www.abc.net.au/news/2019-08-27/mortgage-debt-causing-older-aust…

ABSOLUTE NONSENSE !

If I was allowed to have an inflation and tax adjusted return on my savings , I would save more in the Bank ................. and lets not forget the savings in the bank are the pool of available capital for growth and investment in the economy .

My Savings are someone else's Capital , quite simply savings are part of the capital formation continuum , and without capital we would not have economic growth

Nope. While the planet could underwrite it, you could have economic growth.

How you tabulated the trading of processed parts of the planet, is irrelevant. If folk thought the digits (it's a long, long time since it was gold in real equality) they'd tabulated were going to get them processed parts of the planet in the future, well, that only worked until it couldn't.

And trying to work out how much planet is left, via counting the tokens, is doomed to look increasingly stupid. Without planetary parts, capital is worthless digits. Time we moved on.

I shall vote for the package if Simon can find his way to include some helicoptering of cash to Kiwis, say $2k per each, and stipulate no tax on the first $15k of interest earned from Banks, etc. All to stimulate the economy and to direct more revenue/income to his Business friends, but hey I don't mind that.

Boomers shouldn't be afraid to do the sums and monetise some of their capital to provide money for living expenses.

Indeed. A bit odd to receive hundreds of thousands to millions in benefit from these central bank policies then bemoan not receiving enough from them elsewhere. Spend some of that money received through the policies. Simple.

Do we forget that the retirement age was lifted from 60 to 65 by steps in the early 90's' no 20 year preparation, happened rather quickly for those near retirement, impacted those born before the war marginally and was in full effect for current boomers and the rest of us after the boomers. I have to work an extra 5 years, before I get the pension. however its not all about me. I had more than enough time to plan and was under the opinion that I wouldn't receive the pension if I had a super scheme. If I live longer than 65 and get a pension its a bonus.

This effort to get us Boomers to SPEND SPEND SPEND , is just a load of cods .

Apart from the fact that the schools taught us about thrift and that's what we knew and did ( I still have my post office savings book form the 1970's ) , we also understand the need to live within out means and to avoid being a burden on the State .

Post WW2 thrift was a part of our daily narrative

Economists have routinely pointed out ( it was economic orthodoxy when I studied economics) that Savings were a every important part of the country'e health and wellbeing , and success .

Nothing has changed , the savings of one are the capital resource of the business , farming and other productive sectors , and pooling out savings in savings banks , co-ops and building societies enabled home ownership

We need to save , live within our means , provide for our old age , take care of our health and not expect Nanny State to wipe our backsides , if possible .

And saving should be rewarded with a decent return

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.