Today's Top 5 is a guest post from Jeremy Couchman, senior economist at Kiwibank.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

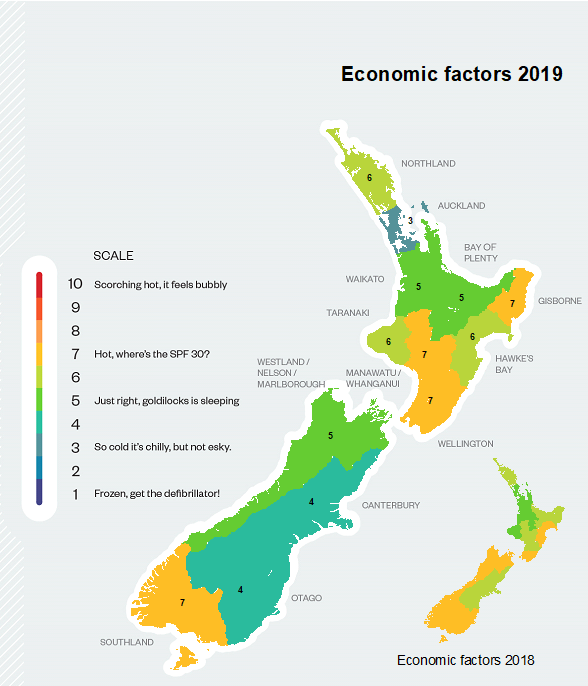

We’ve updated our regional analysis. Compared to a few years ago, most regions have cooled along with national GDP growth. Last year, we highlighted the growing divergence in “The performance of the provinces: improves beyond Auckland”. The divergence has worsened this year, with Auckland stalling, as aggregate GDP growth has surprised us on the downside.

The Kiwi economy recorded below trend growth of just 2.1% year-on-year in the June quarter, the lowest rate seen since 2013. Worryingly, businesses remain despondent, according to surveys, pointing to a further slowdown into 2020. The deterioration in business intentions demands a policy response, and we think the RBNZ will respond. We expect the RBNZ to cut the OCR to just 0.5%, and we may see another 50 basis points move in November. Fortunately, not all regions are in a tough spot, with Gisborne, Whanganui/Manawatū, Wellington, and Southland trucking along for now.

Here are the top 5 highlights from the regions.

1 The Super City is super slow:

Auckland typifies the slowdown in the regions, and the City of Sails is flailing in the wind. The Auckland housing market remains particularly soft, and many firms in the region highlight capacity constraints as impediments to growth. But there are signs that Auckland’s housing market is finally stirring, and where Auckland goes the rest of the country tends to follow.

To give Auckland a chance, the policy response should not just come from the central bank. We also need central government to step-up and trim the main sail as the Super City heads towards hosting the next America’s Cup. We need more infrastructure investment to lay the foundations for future growth across the country. The Government is in an envious fiscal position with plenty of room to borrow and invest, and at record-low interest rates too. Maybe the strong readings in Wellington have politicians thinking things are good. At least until they open a business confidence survey.

2 The economic temperature drops in the south:

Apart from Southland, regional scores took a tumble this year. The down draft has been seen in the NZIER’s business survey, with profitability and hiring sharply lower in the south over Q3. External forces are at play here, with guest nights falling in line with slower growth in tourist arrivals. But their remains opportunity for firms who look to invest. As our banker on the ground in Canterbury notes, “… business is there for those willing to go out and chase it.” – Grant McIntyre, Senior Commercial Manager.

And we expect the RBNZ to lower the hurdle rates for business investment further to nudge more firms to take the plunge.

3 Some of our smallest regions top the standings in 2019:

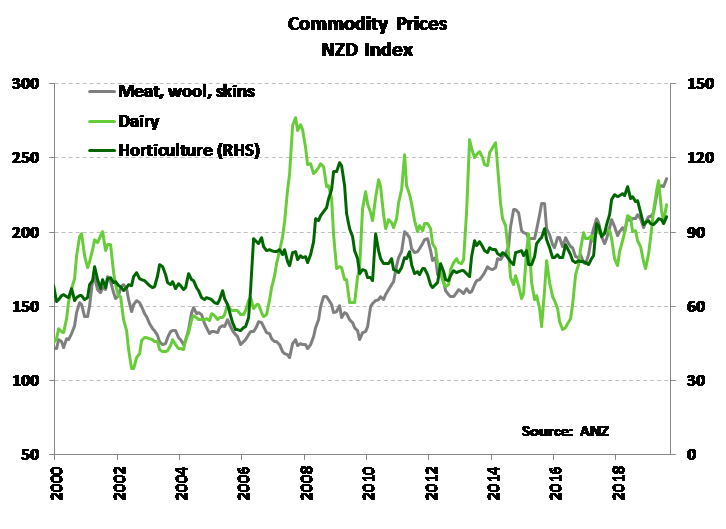

Fortunately, not all regions are experiencing tough times. Some of our smaller regions, such as Gisborne, Whanganui/Manawatū and Southland have maintained or even seen a rise in their regional score - which were already decent. Housing markets in these regions have surged as they catch up to the larger centres, and investors hunt for decent rental yield. Construction activity has responded and people in these regions seem generally happy to open their wallets and spend. Also many regional economies are being protected by the storm brewing offshore thanks to resilience in our key commodity prices.

4 Wellywood is looking good:

Wellington looks to have benefited from consistency across most underlying measures this year. For instance, growth in employment, retail sales, and guest nights are tracking comfortably above average for the region. Like Auckland, Wellington is becoming a victim of its own success. The almost 40,000 people added (a 7.6% gain) to the region’s population between the 2013 and 2018 censuses has increased pressure on local infrastructure and the cost of housing. And the upbeat assessment may not last. On the ground, Wellington’s notorious gales must be adding a windchill factor. While the housing market remains solid, “…business confidence is certainly down over the last year” in part due to a “…lack of progress in recent years on critical infrastructure projects within the city.” – Peter Charlesworth, Regional Manager.

5 Risks to the regions are coming from all sides:

An extended period of depressed business confidence is weighing on actual business decisions. It started with a change in government and a period of heightened policy uncertainty. Depressed confidence has led to firms reining in investment and headcount. And there is an inability among firms to pass on rising costs to customers – hammering profit margins. The longer we keep our heads down, the worse the outlook will be for growth, inflation and employment.

Financial conditions have eased substantially following the RBNZ’s recent rate cuts. But credit conditions may tighten. In December we are expecting to hear the RBNZ’s final decision on its proposed bank capital requirement rules. Banks will be told to hold more capital against their lending to help the financial sector weather the toughest of financial storms. Bank funding spreads are likely to widen, and it may be harder for some sectors of the economy, such as agriculture to access credit.

Gale-like headwinds are blowing in from offshore, the US and China are still deeply involved in a trade war. Although they are at least willing to talk. In the meantime, global trade and growth among our major trading partners is slowing. For now, we are being partially protected by resilient commodity prices and a falling currency. But this may not last.

17 Comments

Nice info graphic with the map. So looking at Auckland which is clearly lagging due to being far too dependent on the property market which has generated a false economy, that has also been killing off our real economies by sending the cost of living sky high and closing businesses here particularly in the tech sector.

So how to revers Auckland's false economy - Easy! Tax the by product! Almost 40,000 empty homes are now situated in the central and main commuter districts of Auckland. If we were to adopt the very successful Vancouver Empty Homes Tax model this could generate $460,000,000 in tax revenue each year and probably at lot more! This is based on the average unoccupied home value being $1,170,000 due to most of these homes being in the more expensive parts of Auckland according the the latest census figures, - 1% tax on home value = average yearly tax of $11,700 per vacant property x that by 39,393 unoccupied homes = $460,898,100 in tax revenue. Main advantages: -

1) Huge tax revenue generated that can be used to build homes and improve services for NZ.

2) You are mostly taxing Speculative Overseas Investors vacant property who can't vote in this country.

3) Reduces the overall cost of living in Auckland by freeing up more rental property.

4) Helps business to thrive since they can attract and retain staff more easily with reduce cost of living in AKL.

5) Deters money laundering.

More info on the Vancouver's empty homes tax : Opinion: What Vancouver’s impressive Empty Homes Tax revenue tells us https://www.vancouverisawesome.com/2018/11/30/empty-homes-tax-vancouver…

And build a lot more affordable houses!

That will boost the construction sector, but will also mean people have more disposable income to spend in the economy or invest.

Yes, I also forgot to mention that the Empty Homes Tax can help to reduce road congestion too in inner city areas, since it frees up more rental property that is in the more expensive central suburbs. And the Vancouver model has been proven to far exceed any operation costs, so much so that is is currently being adopted by other countries/cities too such as the USA (New York and San Diego), France (Paris) and Singapore.

Makes more sense than the prescription in the article itself:

To give Auckland a chance, the policy response should not just come from the central bank. We also need central government to step-up and trim the main sail as the Super City heads towards hosting the next America’s Cup. We need more infrastructure investment to lay the foundations for future growth across the country. The Government is in an envious fiscal position with plenty of room to borrow and invest...

The article seems too much like saying that Aucklanders have enjoyed a lot of betterment from the city...but property betterment has now slowed down...Can we get some more infrastructure to improve things more? But don't raise our rates to do that, we'd like the cost of this spread over others instead - step up, central government! That'll be great, thanks!

All economists' prescriptions for NZ have been tried in Japan without success:

Ah yes, the old "Auckland wants infrastructure to support the disproportionate migration burden forced on it by the rest of the country, those bastards". Funny how the rest of the country is quite happy to hoover up more than their share of money for projects their own population base can't fund, but as soon as Aucklanders want to get to work or home to their families without spending hours in congestion caused by the last decade's population surge, the rest of the country wags its fingers about financial prudence.

Don't forget Auckland's reaped most of the benefit of our mass (mainly) low-skilled immigration policy, and it shows in the economic results.

Ah yes. The benefits such as congestion, high house prices and difficulty accessing state services like hospitals or education. How fortunate are we.

Keep on crying

Here we go again how to give a quick fix to all our problems BAN AND TAX

"Gisborne, Whanganui/Manawatū and Southland have maintained or even seen a rise in their regional score - which were already decent. Housing markets in these regions have surged as they catch up to the larger centres, and investors hunt for decent rental yield." Fascinating how a negative statistic can be put into a context that makes it look positive.

Housing markets surging is most definitely not a positive for the regions because what it means is that accommodation is becoming increasingly unaffordable for the locals as mostly moneyed outsiders snap up what they perceive to be bargains. Pay in the regions is most definitely not keeping up!

Measuring regional strength by an investor-driven surge in local property prices is insane. Investor and speculator targeting of asset price inflation and increased rental yields is a direct cause of poverty and homelessness. There is more to prosperity than house prices. How about the effect on regional businesses needing people in secure housing and income to spend? The case studies up and down the country are staring us in the face.

The Top 5 is contributed by a Bank employee. What else but 'Property Price Up = Goodie' would you seriously expect? Mo' price = mo' Mortgage = mo' interest stream revenue. The reverse ain't necessarily true......

So many valid points in your comment it's hard to pick the best one; so I'll just applaud them all....

Yep!!!

Workingman, this thinking, how is it fixed without making things worse!.

I am seeing a case, a case not for kiwibank, but more a case for DFC. - Development Finance Corporation.

A bank instructed to avoid all things residential property, all things. A bank that funds GDP creation, a bank that funds productivity. Makes good things, makes good things better!

A Workingman's bank!

Retail banks, Henry, are fundamentally myopic when it comes to wealth creation via business activity, and have, of course, no concern with the rest of social value (via employees, suppliers, etc). Instead banks, being ignorant of, or uninvolved in, these aspects of life, lend on things they can see - whether land, a house, or a Mack truck. Even farm lending has largely been based on capital values and hoped-for capital gain. Bankers and property investors/speculators most resemble a PNG cargo cult, expecting wealth to appear out of the sky. And that, in short, has been NZ's economic strategy too, praying for money via property and immigration. (And this, as a business owner fortunately without need of them, is no personal gripe.)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.