By Rodney Dickens

If dwelling sales reported by the REINZ had responded normally to the significant fall in mortgage interest rates since 2017 the monthly seasonally adjusted number of sales would be around 7,500 now versus just over 6,300 in November (i.e. 15-20% higher).

The lack of upside in dwelling sales since 2017 isn't because interest rates have become irrelevant, it is because numerous special factors have offset the boost from the fall in interest rates.

Examples of the special factors are the October 2018 ban on most foreigners and banks tightening lending criteria in response to the findings of the Australian Financial Services Royal Commission.

The impact of some of these factors will have ended or largely ended, however, two of the special factors will have an ongoing impact, with one of these - the interest rates banks use to stress test borrowers - possibly changing the way interest rates impact on the housing market permanently.

This article reviews the special factors.

In light of the potential importance of what banks do with the interest rates used to stress test borrowers, Gareth Vaughan of Interest.Co is surveying banks and mortgage brokers to find out what is happening with the results to be released later this week.

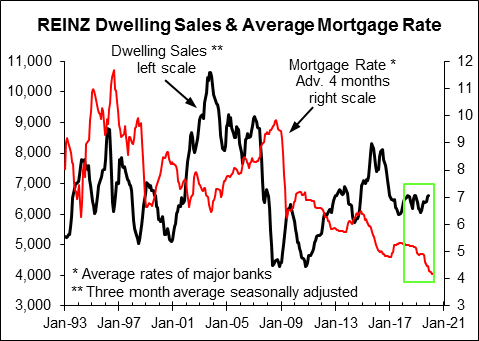

The response to the latest fall in interest rates has been nothing like a normal one

The chart below shows that the previous sizeable falls in the average mortgage rates on offer by the major banks since 1993 were all followed roughly four months later by a large increase in the number of existing dwelling sales; but not the latest one (the boxed area). Reflecting dwelling sales reacting to interest rates with around a four month lag, the red mortgage rate line has been advanced or shifted to the right by four months.

The number of sales should have already benefited from most of the fall in the average mortgage rate from 5.31% in June 2017 to 4.17%.

To put the fall in proper context, the 1.14 percentage point fall in the average rate represents a 21% fall in interest costs. It is a large fall that would normally drive a large increase in existing dwelling sales vs. the sideways drift that has occurred since 2017.

The list of culprits for the lack of upside in sales is quite long and includes one factor that warrants further investigation

The list of culprits I can come up with is:

- The ban on most foreign investors.

- Banks tightening lending criteria following the Australian Royal Commission.

- The dumped plan for a Capital Gains Tax and changes in rental laws favouring tenants.

- KiwiBuild stealing some first home buyers and "second chancers" from the market.

- Banks possibly acting in advance of the increase in capital levels the Reserve Bank confirmed earlier this month.

- Something having a negative impact in the Lower North Island, especially Wellington and to a lesser extent in the South Island.

- Immigration changes and especially the cut in residency visas by the government.

- Banks not cutting the interest rates used to stress test borrowers less than they have cut mortgage rates.

What follows is a brief review of the special factors. Some are no longer relevant, while what banks do with the interest rates used to stress test borrowers could be the most important one in the future.

That is why it is the focus of Gareth's investigation.

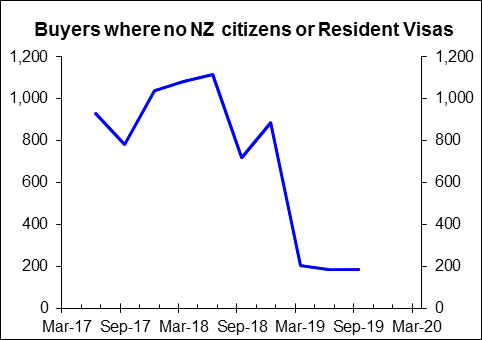

The October 2018 ban on most foreign investors: This had a moderate negative impact on dwelling sales in late-2018, but the impact ended in early-2019 based on the number of sales to foreigners having stabilised this year (next chart). Australians and Singaporeans are exempt from the ban so there will always be some sales to foreigners.

An Interest.Co article investigated how much the Australian-driven tightening in lending criteria made it harder for would-be borrowers to get mortgages, partly because of large increases in the interest rates used to stress test borrower (link below).

This was driven by the findings of the Australian Banking Royal Commission that were released in February 2018.

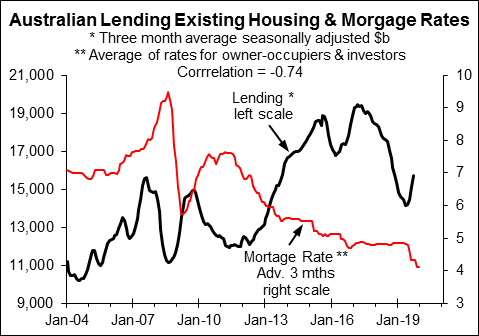

The next chart gives an indication of the impact tighter bank lending criteria in Australia in response to the findings of the Royal Commission had on the existing housing market.

Despite mortgage interest rates not changing, the value of new bank loans to owner-occupiers and investors who were borrowing to buy existing dwellings tumbled in 2018.

However lending has spiked since mid-year in response to falling mortgage rates.

In Australia bank lending on existing housing seems to be responding to interest rates normally again (next chart).

Tighter lending criteria undermining the boost to sales from the fall in interest rates significantly: The Australian experience suggests it stopped being a negative factor some months ago but in NZ banks have been scrutinising expenses more this year.

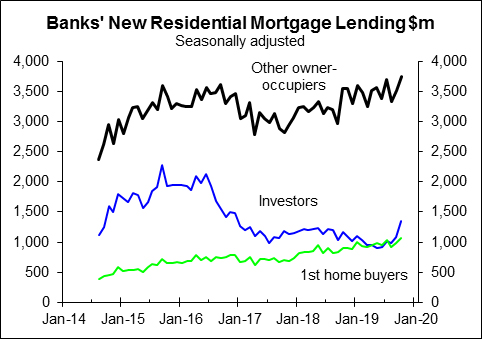

The government's proposal of a Capital Gains Tax: In 2018 this had a minor negative impact on borrowing by investors over the second half of the year and the first half of 2019 based on new mortgage lending by banks to investors (see the blue line in the next chart). Reports at the time also suggested the plan for a CGT encouraged more investors than normal to sell, as did plans for changes to rent legislation that favoured tenants over landlords.

However, in the last few months lending to investors has been the strongest performing of the three categories the Reserve Bank releases info on (next chart). The limited upside in existing dwelling sales this year is down to owner-occupiers including first home buyers not so much investors.

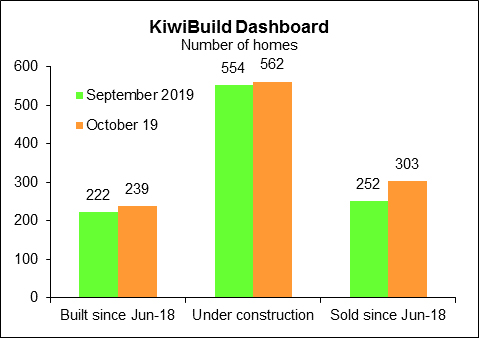

KiwiBuild: Kiwibuild will have stolen some buyers away from the existing housing market last year, but with only 303 KiwiBuild homes sold since June 2018 it hasn't had a significant impact. This is in part because many of the 303 KiwiBuild home buyers probably won't have bought an existing house if they hadn't bought a KiwiBuild home. Progress with KiwiBuild remains slow based on the changes between the September and October "dashboards" (next chart). KiwiBuild may become a bit more of a threat to the existing housing market next year.

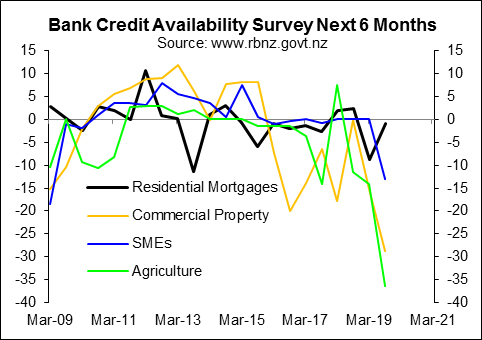

The next chart suggests banks were planning on significantly tightening lending criteria for rural and commercial property borrowers and to a lesser extent SMEs based on the Reserve Bank's latest survey of banks conducted in September 2019, but mortgage borrowers didn't appear to face much of a threat (black line).

We assume the tighter lending criteria implied by the survey was because banks were responding in advance of the Reserve Bank's plan to significantly increase minimum bank capital levels.

Banks acting in advance of the increase in capital levels didn't appear to be a significant threat to mortgage borrowers, but may have played a minor part in muting the boost to dwelling sales from the fall in interest rates this year.

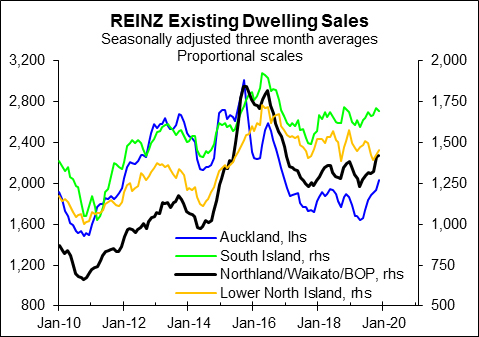

A breakdown of NZ dwelling sales into four super-regions provides some insights but also raises some issues (next chart).

Following the negative impact of the ban on most foreign investors in late-2018 to early-2019, Auckland sales have increased roughly as much in the last seven months as would be expected given the size of the fall in mortgage interest rates (blue line, next chart).

However, this will partly reflect increased investor buying in recent months that is likely to be focused quite a bit on the Auckland market, with a bit of this also relevant to the rest of the upper North Island that has also had a reasonable increase in sales (black line).

Sales in the lower North Island have been a bit of a drag on the national figures (gold line, chart above), with this most the case for Wellington but also the case in other parts of the lower NI. Sales in the South Island have not increased much (green line).

Southland has been a bit of a drag on South Island sales but there has been limited upside in general.

Sales don't behave the same all over the country all the time but it is a bit unusual for sales in the lower North Island not to behave much like sales in the upper North Island.

It isn't strange for South Island sales to behave a bit differently from sales in the North Island but the lack of upside in sales in the second half of the year is a bit puzzling.

It is unlikely banks have adopted different lending criteria for different regions, so the divergence in the behaviour of sales in the four super-regions most likely reflects regional factors at work (e.g. maybe higher insurance premiums in Wellington and more buying by investors possibly focused most on the upper North Island).

The regional differences go some way to explaining the lack of upside in NZ sales in response to the fall in mortgage interest rates, even if it isn't obvious why there hasn't been some recovery in lower NI sales or why upside in the South Island has been so muted compared to the upper NI.

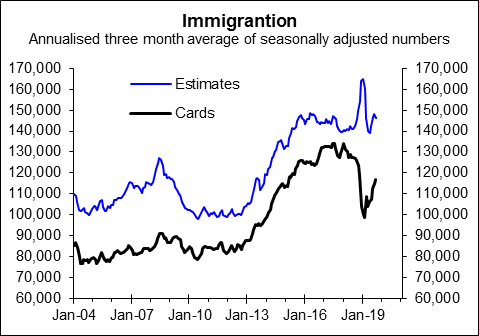

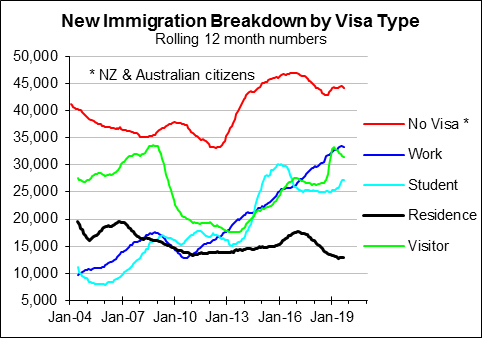

Traditionally immigration has been the second most powerful driver of existing dwelling sales; interest rates having been the most powerful. The official immigration estimates derived from a model Stats NZ built in response to the November 2018 dumping of departure cards show a sharp spike in in late-2018 that was more than fully reversed in early-2019.

Recently there has been a bit of upside (blue line in the next chart).

By contrast, based on info derived from arrival cards, that still exist, immigration tumbled in late-2018 to be followed by a partial rebound this year (black line).

Statistics NZ favours the official estimates (the blue line), but we have no faith in the estimates or the card-based numbers that were somehow corrupted by the dumping of departure cards in a manner Stats NZ has failed to explain adequately.

The lack of certainty over what immigration did this year makes it hard to say if it helped mute the boost to dwelling sales from the fall in mortgage rates,but the government cuts in residency visas (black line, next chart) in conjunction with the October 2018 ban on most foreign investors from buying will have had a mild negative impact on dwelling sales.

The fall in the number of immigrants arriving with residency visas has been more than offset by upside in the other visa categories.

However, the ban on most foreigners from buying existing house applies to immigrants with work, student and worker visas.

The change in the mix of immigrants and the ban on most foreign buyers will mean immigration has had a least a mild negative impact on dwelling sales.

Based on anecdotes from the market like those from this link, banks haven't cut the interest rates used to stress test borrowers as much as they have cut mortgage rates.

This could be creating a bottleneck constraint that mutes the impact of the changes in mortgage rates.

If this is the case it is possible what banks do with the stress-test rates will be more important than changes in the actual mortgage interest rates banks offer.

To help shed light on this potentially important issue, Gareth Vaughan of Interest.Co is conducting a survey of mortgage brokers and banks to find out what banks are doing with stress-test rates and more.

If banks' stress-test rates move much less than mortgage rates in the future, it implies interest rates will be a much less powerful driver of housing and economic cycles than has been the case in the past.

This poses a range of questions including what impact OCR changes will have on the housing market and economy.

This article is here with permission.

39 Comments

It will be interesting to see if the banks here can maintain their downward pressure on mortgage rates which are at historical lows. Given that the big four Australian banks are under a lot of pressure to clean up their acts, so will they be in a position to cut rates further to prop up our housing market?

Considering:-

1) Westpac AML banking scandal, currently they have been ordered by the Australian Prudential Regulation Authority (APRA) – the banking regulator – has ordered Westpac to set aside an additional A$500 million ($520m) in capital. And yes they have already started to increase their mortgage rates, so have BNZ.

2) Our Government will introduce deposit insurance of $50,000 per individual per financial institution, a governance board for the Reserve Bank to oversee financial stability, and plans to follow bank reforms in Australia that aim to strengthen director and executive accountability.

3) Starting from mid-2020, the banks which dominate the sector will have to increase their total capital to 18 per cent, from a minimum of 10.5 per cent now. Herald article: Home loan interest rates set to rise off bank capital increase. https://www.nzherald.co.nz/personal-finance/news/article.cfm?c_id=12&ob…

Think you'll find the big four will be happy to reduce their exposure to unsustainable lending, and let others keep the party going on some of the highest house prices in the world.

As they say, its better to have some business rather than no business should the prices collapse.

While prices are still increasing in some regions, the show is almost over. And the best part about this is government will have to operate with alot more fiscal discipline than governments of the past. Inflation will no longer hide poor governance, and the importing of low pay migrants is not the answer. Sustainable growth is, and a reset will be a good starting point..

A lower OCR isn't all about housing!

I'll suggest it has far more to do with refinancing those already indebted (and stressed), be that households SME's or...Big Business.

New Zealand can't afford a big corporate casualty at this juncture, so if the WMP price collapses; ditto building work, then a lower refinancing rate (OCR) might keep the nearly-dead alive a bit longer.

The poor response to OCR cuts is mostly likely a demonstration that people are getting to the limit of debt they can tolerate. In the figures before the 0.5% OCR cut mortgage defaults had spiked up, and after the defaults settled down. So there is plenty of evidence to support your theory.

It's far worse in Australia where their tax refund appeared to have no effect at all. Their news seems to be continually getting worse.

The argument that falling OCR helps the struggling is flawed. Only those with good credit records get the reduced rate. Those with a spotty record do not. So if you are struggling and the bank knows it, too bad.

...unless you are Too Big to Fail?

How Big is that? I guess all banks have their own list of those. It's the old "If you owe the bank a million dollars, and you can't repay it, you have a problem. If you owe the bank a hundred million dollars and you can't repay it, the bank has a problem' And that, I'll suggest, is what the OCR cuts are aimed at.

It's far worse in Australia where their tax refund appeared to have no effect at all. Their news seems to be continually getting worse.

Precisely. That is keeping their ruling elite up at night.

Good point. But I would join the two halves of what you say: the mortgage cuts allow those WITH existing mortgages to refinance at lower rates and lock them in. This is the piggy bank policy: eventually the piggy bank is empty - that is can no longer cut rates anymore and this means of putting money in people's pockets expires. This is now v close. So, the 7 year gift policy to keep refinance Ponzi going is expiring. This means of covering the fact that wages are not rising fast enough to keep consumption up. This will lead directly to lower GDP, which is indeed what we are seeing.

Cheaper debt isn't attractive when the size of the debt has near doubled in five years... at least not to some of us.

Exactly. Servicing a mortgage now at record low interest rates is more expensive (as a portion of income) than it was in the 80s at record high interest rates.

Agreed, rather telling his "The list of culprits I can come up with is:" does not include high cost of housing compared with incomes.

http://www.munknee.com/which-country-has-the-highest-house-price-to-inc…

Jesus that KiwiBuild dashboard looks sad...

Against original targets, yes.

Against the recalibration, not as bad :)

Thanks for this in depth look at why interest rate cuts (21% in interest payment terms) have failed to produce "expected" increase in sales. I agree with a lot of the explanations provided. However, there is also the one most economists are stipulating for the economy in general, which is: diminishing returns. There is also the issue of there being 20% fewer listings now than in 2017, at the same time of the year. Why are people not selling? Many existing home owners that I speak to on doorstep are telling me that they were minded to move but have now decided to stay put and renovate, or wait til prices recover. Meanwhile, the FHB market for sales (in Auckland) which one might identify as property priced below 900k in Auckland, has fallen in sales terms by 5563 since 2016 (or 27.64%) and that between $900k and $1.2m by 1113 or 18.3%. This encompasses a 51% fall in apartment sales in that 3 year period in Auckland. This tends to support your premiss that credit testing by the banks, of FHB has been tightened and is not being amended in line with interest rate cuts.

The alternative viewpoint is that the banks were not applying the criteria properly pre 2019 and because of Australian experience they are now going over the top to avoid a Royal Commission here.

Panic at the RBNZ? OCR cuts not causing house price boom! Oh no! The end is nigh! Woe, woe, woe.

Actually, here in Nelson, house prices seem to have jumped another $100,000 or so, which is presumably what the governor intended. Makes no sense why he wants this, but there it is. It is good for us, apparently, so presumably we should be thankful.

No one seems to ask that renters and home owners be equally represented on the OCR committee. Too radical, I guess. It is usual to at least declare one's special interests, though. Oh, sorry, I forgot, higher house prices forever is called the 2% inflation target. Now didn't someone called Paul Volcker say there was no evidence at all for that policy?

"Mortgage rate cuts haven't produced the expected rise in house sales"

Experts may and are comming out with so many intillegent reason BUT has anyone thought that may be most imortant reason is Affordability.

A mortage of a million dollar or even $800000 is still a million dollar or $800000 in debt which has to be repaid and if now interest rate falls from already low rates to slightly more by 0.2% or 0.3% does it make a difference (Instead of say $825 per week may have to pay $800.00 per week which will still be quite high). Besides how many FHB can afford the current high price in Auckland and in the absence of foreign money (Money Laundering) - easy and fast moneyis missing - volume cannot be up as expected with fall in OCR.

The law of diminishing returns is a fundamental principle of economics. Am sure most economist must has heard and know about Law of Diminishing Returns : The law of diminishing returns states that as one input variable is increased, there is a point at which the marginal increase in output begins to decrease, holding all other inputs constant. At the point where the law sets in, the effectiveness of each additional unit of input decreases

We've pretty much reached peak debt. If you were looking to upgrade from a $300k house to a $500k house you only had to borrow an extra $200k. But prices then doubled. Now you have to borrow an extra $400k to fund the gap between a $600k and $1M house. Interest rates might be low, but the amounts you now have to borrow in order to move are eye watering.

Economist Rodney Dickens wonders if bank lending criteria are the reason the housing market remains sluggish despite interest rate cuts

Housing market sluggish in Auckland - must be joking. Is he talking about period before September 2019 or after.

So is agreed that fall in OCR has not resulted in boom but sluggishness so the experts should debate and disucuss to find what has changed in last two months that house prices are going up and that too Million dollar Plus houses . Economic conditions, High Immigration and demand level was same as earlier, when the market was stagnant.

So should have an article soon on interest.co.nz by experts, the reason of sudden jump in Million dollar plus houses that is pulling the entire market up and is hapening not only in NZ but also in Canada and Australia where Chinese money was at play.

Some may say summer is boom time in NZ but Canada too has boom and is winter so........... the common element in all based on past history is that foreign money ................as happening at the same time.....not a consiparacy theory nor coincidental.

Circumstantial evidence points to only one thing that Chin.............

The Canadian central bank started buying mortgage bonds in Nov. So has the Federal Reserve. Make of that what you will.

Providing vital liquidity to keep the housing ponzi market moving.

Wellington doesn't have a lack of buyers, it has a lack of sellers.

Well, this is a much more balanced article than we will get from the bank economists.

Tellingly, Rodney is an independent economist.

Great article. He's actually bothered to look at some of the nuances of the immigration numbers and potential impacts on housing.

I recently made an offer on a block of land for residential development. At current rates and on a low LVR I could justify the purchase price, but adding 1-2 % to rates made it too risky a proposition. Suggest many are finding the numbers no longer add up.

Banks have still been calculating interest rates for loan servicing at over 6% so it is still it does make it more difficult,to,borrow for many rather than the excess of 3% as being quoted by the Banks.

Still a great time to be buying and investing as you can still buy property that give a yield of 6% in Christchurch and why wouldn’t you.

Christchurch is continuing to be rebuilt and gives a great standard lifestyle.

Wonder why Yvil and DD haven't come in to mock the article for conducting such a deep analysis of something pretty much irrelevant.

NOTE: This comment has been slightly edited upon request.

You think about me a lot, don’t you? I didn’t say it was totally irrelevant, I said price is much more relevant to most people, and focusing pretty much exclusively on volumes is no good. I care more about price, days to sell and inventory.

If remembering things you write like every day counts as "thinking about you a lot", then I guess I do that.

https://i.ibb.co/DgKq9vx/image.png

{kind=link}

I guess the word "totally" is what you're taking issue with? I'm still not sure why the double standards. This article says nothing about price, days to sell, or inventory, and is probably longer than all of Mike Kirk's comments combined. Surely it deserves to be mocked with the same smug condescension?

Yes, and I am one of the majority of people for whom sales volumes are pretty much irrelevant. "pretty much irrelevant for most people" is different to "totally irrelevant". Words matter, sunshine. For agents it obviously isn’t irrelevant given that their commissions are heavily dependent on sales volumes - in that sense it is the life blood of their industry. People like me care about what our property portfolios are worth - I care very little about how many properties sold last month. Rodney writes wide-ranging and interesting articles, as opposed to spamming this site with almost nothing but sales volume data like an estate agent fixated on commission.

""pretty much irrelevant for most people" is different to "totally irrelevant". Words matter, sunshine"

In the context of what I was asking, it literally couldn't matter less. But I went ahead and changed my original post. I hope that makes you feel better, "sunshine".

"Rodney writes wide-ranging and interesting articles"

I'm glad we can agree this is an interesting article? I personally find it interesting because I consider (with my admittedly little expertise) sales volume to be a pretty good indicator of the state of a market. (I wonder if that's why Rodney wrote it?) Why is it interesting for you?

Good grief, I didn’t say I found this article interesting. Rodney does write wide-ranging and interesting articles, but I care very little about sales volumes, so this one isn’t particularly relevant for me. Good commentary on kiwibuild, CGT, immigration etc, but only because it got me reflecting on the implications for property prices.

A conflation: the word “I” and then “most” people. Quite Trumpian

Here is a simple hint for free.

The PRICES are too f****** HIGH.

The economy now has type 2 diabetes from the endless sugar hits of monetary easing to pump the asset bubble.

From the perspective of the younger generation it doesn't matter what interest rate lipstick you put on the pig when you are still on the hook for a million dollars for a fibro shitbox in a diversity suburb and at the mercy of any interest rate increase for the next thirty years.

Anybody with a brain will be on a plane to elsewhere. Leaving behind the low skilled dross.

Jacinda and Adrian can shove their low wage, high cost housing and mass immigration asset bubble ponzi economy where the sun doesn't shine.

Agree that interest rate : low or lower or lowest does not matter much when prices are sooooo HIGH to FHB.

Who are buying this 1.5 million or 2 million dollar house in herd ?

Even earlier when Chinese buyer were so evident in the market was denied by than government, so one can not expect anything from government in power, as it suits them.

Where do you suggest they go? The grass is always greener...

We may have high house prices, but NZ is still a paradise.

We paved paradise and put up a parking lot.

"We may have high house prices, but NZ is still a paradise."

Is there any maximum price limit that you would pay today for a 3BDRM property on 300 sq m piece of land to live in paradise? $1 million, $2 million, $3 million, $10 million, $20 million, $50 million, $100 million ... ?

What is the key constraint on the maximum price limit?

I get the feeling inflation is coming as a flowon affect of the repo markets in US.. when inflation hits, then i'm guessing the interest rates will go up... I see some banks are going up already, but that's what they did last year over Christmas too. Cheap in December and a sneaky hike back up for the new year. The hundreds of billions of extra reserve currency being printed is what's making prices go up, not entirely and neccessarily demand.

Plus the extra capital the banks require will expect that they raise the funds by interest rate rises.

Prices are too high. It's a long term social disaster for New Zealanders

How about the more obvious one? People are broke. Under this Govt rents have gone up, petrol has gone up, electricity has gone up, GST has been slapped on online purchases, and avocados were selling for $7 each!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.