By Kirdan Lees*

Treasury’s scenarios show the economic impact of COVID-19 could be catastrophic. The worst-case scenario shows unemployment could hit one-in-four people by March 2021. Output would plummet, perhaps down a third compared to GDP prior to the COVID outbreak.

But this is indeed the worst-case economic scenario, that assumes a prolonged period of six months in Alert level 4 lockdown with only existing fiscal support measures in place. And Treasury’s scenarios are contingent on the containment policies for COVID-19. So each day of flat or falling cases makes this worst-case economic scenario much less likely.

Instead, low levels of new daily COVID-19 cases make Treasury’s first scenario most likely. This scenario assumes 1 month of Alert level 4 lockdown, 1 month of Alert level 3 requirements and ongoing conditions of Alert levels 1 and 2. Even under this base case, unemployment rises to 13.5%.

The worst-case scenario won’t play out like this: outcomes are not set in stone and fiscal policy can do much more to respond

Treasury rightly point out the scenarios are all about providing insight and are not official forecasts. Taking a scenario-based approach is useful for framing what policy should do. Scenarios establish a framework to monitor data against. This helps ready policy to change when the data points to some scenarios being more likely than others.

Perhaps the most important takeaway from Treasury’s scenarios is the number of jobs that would be supported by additional fiscal policy measures.

Treasury suggest an additional fiscal package of $20 billion could reduce unemployment from 13.5% to 8.5%. Based on their estimates this saves 138,000 jobs. At least on these headline numbers, this comes at a cost of $145,000 per job saved.

But the unemployment rate might not reveal that much. Workers that remain in the economy could be employed at 80 or 60 percent of capacity. In these circumstances, richer analysis should consider underemployment – that is, how many workers want to and are available to increase the number of hours they work.

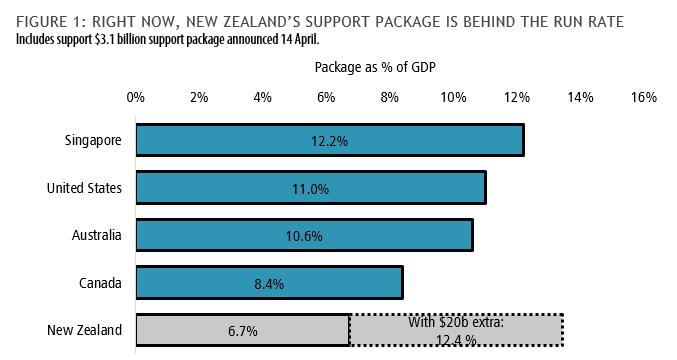

The scenarios show additional fiscal support is much needed. Figure 1 shows New Zealand’s existing package is falling behind the scale (relative to GDP) other countries have provided to support their economies. A further $20 billion of spending would put New Zealand in line with the scale of other countries’ packages – at least for now. But there’s no doubt additional fiscal support will be announced globally.

And different types of policies could be needed

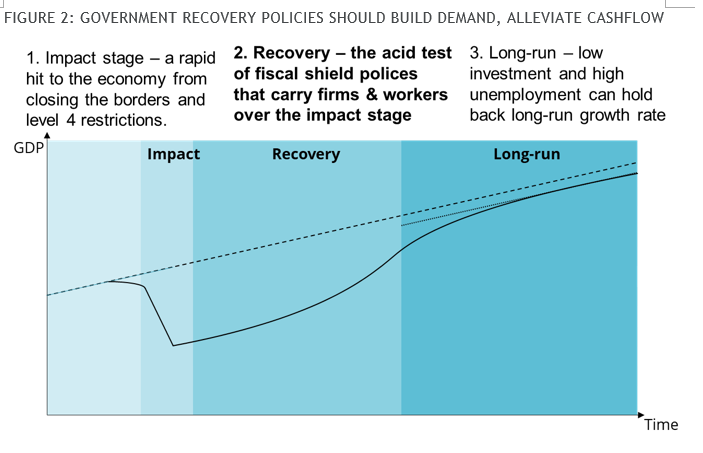

The immediate impact of COVID-19 is all but baked-in: a sharp contraction in output associated with a fall in demand from consumers in lockdown and lower production from workers who cannot work from home.

Rightly, support to date has been targeted at packages to support paying salaries, to help shield firms from the downturn in the economy. But wage costs are not even half of the problem firms are facing.

Wages are only part of the cost equation confronting firms. Many firms have little to no demand for the goods and services they produce. If finances of small to medium firms are similar to the US, then cashflow constraints will start to bite. Recent NBER research says the median US SME business has more than $10,000 in monthly expenses and less than one month of cash on hand. We expect similar numbers apply to New Zealand. So as we pass from the initial economic impacts of COVID-19 to the recovery phase (see Figure 2), fiscal “shield” policies will need to do more to shore up the balance sheet and cash flow position of small firms. Outcomes for firms and works will be contingent on the effectiveness of these policies.

There is much that central government can do

What can government do? Government can scale up several interventions, all of which come at a cost:

(i) Allow deferral of tax and debt payment to ease liquidity constraints for SMEs. The just announced loss carry-back mechanism, where firms can offset tax losses against past profits, will help.

(ii) Extend or instruct banks to give loans directly to firms by underwriting the risk on the riskiest of loans, similar to elements of the Business Continuity Package.

(iii) provide loans directly from the government to firms to help keep and create jobs. This policy is being pursued most aggressively by the British Government who released £330 billion – some 15 percent of their economy – for no-interest loans to small firms.

These measures will all help firms bridge the economic impact of the containment policies needed to stamp out COVID-19. But scale is needed. With such a large chunk of small-to-medium New Zealand firms affected, $20 billion is the starting point of additional fiscal support that will be required.

*Kirdan Lees works at boutique economics consultancy Sense Partners.

81 Comments

Change the headline. The support is from the tax payer of tomorrow. Our younger generations. It is NOT from the government. Governments have NO money..they get it off us.

Interesting how it seems to be the older generations doing everything in their power to keep asset prices elevated - at the same time all the baby boomers about to leave the work force and retire on super. But yeah we can throw billions of dollars to keep everything high. Younger generation, please take on massive private debt to keep our housing valuations at $1million for a crap box in Auckland, and billions more of public debt to be paid via your taxes for years to come so that my share portfolio doesn't fall to much either. All good with you millenials? Thought so...

And then they call young people entitled. Incredible narcissism.

The next dividing line in society will be the young vs old.

Whether it be the environment or the economy, we've left them a mighty mess to inherit, made worse by us borrowing from them to address it, made worse by the way its being addressed.

They have every right to be p*ssed, and the worse thing we can do is ignore them. Whether people like it or not they are at worst a few years away from filling out the same voting form as us, if not already.

I can see this goverments approach being accepted in the short term, but I think accepting personal responsibility will be a component of many election campaigns the world over in the coming years.

The young should recognise that ardern is their generation and her govt is making these decisions that will affect their future and then reflect on what the boomers provided that is now at grave risk of being destroyed.

How old is Winston, who stopped the CGT, for example?

I do admire the reaction of trying to blame it all on the younger generations again though. Only reinforces the problem.

Its not really blaming it on the younger generations, but more serving up sanctimonious BS that they expect them to accept and digest, on the basis that they've somehow done them a favour.

A recipe for disaster in my book. Being annoyed is one thing. Being treated like an idiot in the process brings about rage.

Don't be surprised if when these teens become eligible to vote that their tick is nothing more than a eff you at the older generation. Underestimate it at your peril.

The young should recognise that ardern is their generation and her govt is making these decisions that will affect their future and then reflect on what the boomers provided that is now at grave risk of being destroyed.

The messaging on this needs to be changed permanently, even coming from the government itself. Everything is taxpayer funded, nothing is funded by the government.

The messaging is simple. "Neve's got this!". I don't even have a communications degree.

So where did the tax payers get their money from to fund the government? Last time I looked it came from....the government. Governments only need taxes to drive demand for the currency and to prevent inflation when there are capacity constraints and too much spending. Our government can deficit spend by keystroke. There is no gold or currency conversion standard to defend. The real effects matter. Not the build up of debt...why constrain future real activity to enable the government to save? In a currency it creates costlessly.

So you're saying the government doesn't have investments that return cash to them? Yes, the capital may have originally been taxpayers, but some of those returns will have compounded a lot as well (such as the superannuation fund).

Also, if you want to get really deep - all New Zealand Dollars are created by the government / reserve bank anyway, so the taxpayers only have them on loan from the government.

Governments create new money when they spend.

No, they're just spending the money they've taken from you. The only entity that creates money is the Reserve Bank, and they're quite busy at it right now.

They spend first, then by political choice the DMO issue some debt at the end of the day. Two separate operations, done at different times, one does not require the other. The Reserve Bank buys the bonds, an asset swap, which reverses Step 2.

The Reserve Bank isn't the only buyer of Govt bonds. You can buy some too, with your own money. The Reserve Bank is the only entity that can create money in order to buy the bonds.

Imagine aliens looking down on us. "Yeah, the nz government was just getting things going after a terrible health crisis by sustaining private sector incomes using its currency issuing capacity but then it decided it couldn't do that any more cause it needed to suck dry real activity in the economy to change an accounting entry in a speeadsheet. "

rastus,

It's from both the taxpayers of today and tomorrow. Intergenerational debt is inevitable-think of the life expectancy of any major infrastructure-paid for over generations.

Right now, we face an existential crisis and we must deal with it as best we can and perforce, that means throwing a great deal of money at it. What must also be done is to become significantly more productive per capita. We need to work smarter.

The point made is not to do with wisdom of this spend or not. It is to do with attitudes. Joe dimwit should be constantly reminded that we are spending joe dimwits tax of today and tomorrow NOW. At present joe dimwit has not applied their mind to this at all. Joe thinks there is a endless bucket of money hidden under the beehive.

Every dollar spent should be thought of as cash taken from the wallet of the workers out there. Not thrown around like it is at present (such as giving ma and pa on Nat Super an extra $14k virus payout for their hobby business selling online socks at a loss).

Much of what happens will be completely and utterly out of the control of any one government, including ours, as this is going to be world wide. The USA could well be dead in the water at the rate things are going there. China will be too dangerous to be aligned to in that case. Everything will be much, much smaller, with the exception of debt.

This is the rainy day.

Your last sentence sums it up brilliantly.

Fiscal support : It is obvious, more the money government puts into supporting business and employees (Wage support) less the damage to business or job loss but still can avoid the carnage but not disaster as the virus has already done damage that cannot be reversed and the consequence will be felt for times to come.

Now everyone is in salvage mode. Once the tusunami of corona virus is contained will see what little is left and by paying what price.

As of today everything is guess work and with so many scenarios flying left, right and centre one will hit and can than proclaim to be an expert who predicted.

Too much debt in the system in my opinion. More fiscal support just means more taxation down track. So question becomes, who will that impact more? Post GFC it would indicate it will hit the middle class the most - surely they must be getting sick of it?

Future generations and those that aren't old enough to vote yet I suspect...

Which is why I think if the next period isn't managed well it could result in some type of revolution.

Let's disabuse this notion of a middle class. There is a working class, where in order to feed and house your family you must work for a living - without a job, you will starve. Then there are the owners of capital, those who derive an income from their investments and do not need to work. The notion of a middle class is a fabrication, it is a way of stratifying the working class so that you don't feel as if you are on the lowest rung of society.

If we just had some knights to protect the workers then we could call it feudalism?

Protect the workers, that's a good one!

For many lower down the spectrum; "you must live to work" is more apt... where working hard and harder than many "above" them doesn't keep up with the cost of living let alone enjoy a higher standard of living...

They could start by reducing competition from overseas. If products are manufactured in NZ (or assembled?) take measures that will ensure they can endure against international competition. This will help grow jobs too. Some items will become more expensive, but the Government can also look at supply chains and the costs of materials. Will help in a lot of areas. Then some drive to address productivity - automation, design and so on. start small to grow.

Just throwing money at companies will not help in the medium to longer term.

I think protectionism is the last thing we need right now.

It has the opposite effect on incentivising productivity.

You should watch Arthur Grimes' interview from yesterday.

Disagree Nymad. Protectionism is exactly what is needed to build resilience, jobs, and provide a degree of insulation from being manipulated by or being vulnerable to external sources. We need to be able to identify what we can supply and do for ourselves, and this includes looking at restoring the industries that were exported under the capitalist 'free market'. As much as I hate to quote him, but we do need to take a leaf from Trump's talk - New Zealand First.(Winnie's gonna love that!) With the right approach we may even be able to diversify some of our earnings away from farming too.

I realise capitalists won't agree or like it. But we need to make a choice. This is about people and country first or the almighty dollar? My vote is people and country.

Your opinions seem to be at odds with all experts and history.

If you are forming your opinions on production, consumption and welfare from Trump speeches, I suggest you maybe diversify yourself.

We have Protectionism with us this very day, of course.

Monetary Policy intervention is protectionism.

Extending that policy to other areas of the economy while we recover might make sense. After all, everyone else is going to be doing it, so why would we be better off not to?

I agree BW, but currently it is about preserving jobs and preventing the economy from total implosion. But at some stage that must stop, and policy be reshaped to start rebuilding the economy. How and where this is done is crucial. I can't see funding private banks as a solution, or encouraging debt (essentially the same thing), but supporting and encouraging regional business growth can and should have multiple beneficial effects, not the least will be taking pressure of the resources being consumed by the big cities, water in Auckland for example.

.(DP for some reason!)

Stop being an extremist, I neither like nor agree with virtually everything that Trump says and does, but as the lady being interviewed on TV stated "Even a blind squirrel finds the occasional nut!" However as a capitalist you're probably at the top of his fan list!

I think economic 'experts' and particularly history is less relevant - what we are now seeing is unprecedented. Globalisation was intended to be exponentially beneficial for all parties involved. China/countries that abuse human rights have taken advantage of the system to the extent that our productivity (NOT debt fuelled GDP) has been stagnant/in decline for years now. This is seen around the world. I used to believe that protectionism was the last thing required, however things have changed.

The trouble is Globalisation has NOT been beneficial. And i do not believe it was intended to be, even though that was how it was sold. Globalisation opened the door for the big corporations to increase their span of control, and ultimately wealth and power, and most of them are American. This was evident in the TPPA free trade agreement where international corporates could effectively dictate to Governments, and Governments were restricted in enacting laws in the national interest, but against those corporates.

I completely agree that it hasn't been beneficial. I still struggle that the pioneers would have seen it developing into how poisonous it is today. Going forward - can someone point me in the direction of political policy that is anti-globalism?

Only those that capitalists like Nymad label protectionist. But then the TPPA was also protectionist wasn't it? It protected the rights of the big multi-national corporates over those of national Governments.

This is about clearly identifying and detailing who the beneficiaries will be and how they will benefit. There needs to be transparency from top to bottom. If it is about jobs and people say so, and detail how. Currently there is a lot of talk about taxes, but while Governments need taxes to function, they also work against a functional economy. So ultimately a goal would be to increase wealth from the bottom up. This would be achievable through creating decent jobs at a good level of income, enabling people to spend and save. People could still choose what to do with that money, and the more disciplined will retire relatively wealthy, but at least they'd have a choice, something that in recent years many did not due to the cost of housing.

Interesting note - I came out of uni in 2016 - supply chain and business degree - globalism in universities is STILL being sold as that.

Fascinating - just goes to show how shallow some of the academic thinking is. Too many academics try to ignore or isolate human psychology, but that drives everything we do! Even the most dispassionate, unemotional of us is driven by their psychology and someone else will have issue with.

You are not allowed to use the word unprecedented, Jacinda owns it.

It's a great word for a politician.

Protectionism in very targeted ways has been used to grow fledgling industries into export industries. E.g. the Japanese automotive industry.

How do you build protectionism but at the same time continue to allow inter country on line buying. Several on this site over the years have championed how they can buy cheaper xyz by buying through an offshore, on line trading platform.

Tax offshore purchases online.

"the almighty dollar' Murray means 'stuff'. Goods and services. That's what money is. How much stuff can we get for X amount of input. Unfortunately protectionism means less stuff (or almighty dollars as you put it). What we need is to be able to compete fairly. We manufacture in China as in New Zealand Wayne and Sharlene get 37 warnings before anything can be done then it goes to employment court and company goes bankrupt.

Yes, but this is also about infinite growth in a finite world. Why manufacture in China when that same industry can be created here? Yes some things will be more expensive, but productivity has to be a part of this picture too. We have to put some effort into building resilience.

Protectionism is what we need to build resilience - Correct … but … Protectionism will drive costs higher.

So its the last thing debt stability (all those forward bets on growth) wants.

Living standards MUST drop as a result.

But given debt is going to blow anyway, resilience it is.

I think it is easy to say and extremely hard to do, especially when talking about manufacturing. our remote location is the no.1 impediment. But I agree with you that we should look at the opportunities around AI, automation, industrial design etc. Both Fisher & Paykel companies are good existing examples.

So basically, throw heaps of money/debt at the economy and magically it will grow to be self-sustaining into the future?

What's to stop the syphoning of this money through various overseas pipelines, most obvious being banks but along with so many other overseas owned companies.

We get left with the debt and....well just the debt, to pass on to another generation. This is without even heading down PDKs logical direction.

In 5-6 months time when existing mortgage deferrals have finished. Could the reserve bank print into existence 270 billion. Then loan it to New Zealand owned banks( Kiwi, Heartland, SBS,TSB.Co-op) at 1% fixed for 10 years. Those banks could then refinance all of NZ owner-occupied mortgage debt at say 1.5% fixed for 10 years. Effects?

NZ Dollar is devalued immediately which will make export more competitive. House prices could be stabilised at the level which is likely to be 10-20% lower than now in 6 months time. Those whose employment and income have stabilised will have the option to buy a house. Those who want or need to sell will have a market and ability to exit. A reasonably orderly transfer of existing property from landlords to new homeowners (owner-occupiers) at newly affordable levels.

Why would you want house prices to stabilise?

Just a couple problems with this. Firstly, favouring the domestic banks would breach our world trade organisation obligations, so there goes the export boost. Secondly, that's a huge transfer of wealth to homeowners who have made 50 percent gains in the past three years in most of the country. There are people that actually need support.

that's a huge transfer of wealth to homeowners who have made 50 percent gains in the past three years in most of the country.

There has been no "transfer of wealth." Just because a house price index has gone up 50% doesn't make people any richer unless they can realize that wealth through a sales transaction or leverage the "index value" simply becauser they have their name on a title deed.

The RBNZ does not create new wealth. Like in the last decade, it simply ends up transferring wealth from some (savers) to others (asset holders). This is exactly as described above, devaluing the currency and increasing asset prices.

Pretty immoral protecting of one's lot from those in power, if they do that.

Like in the last decade, it simply ends up transferring wealth from some (savers) to others (asset holders).

Well yes. But let's assume in the case of NZ the bulk of this transfer has gone towards bidding up house prices. But then those prices fall 50%. How has the wealth been transferred?

This also may not work as right now the USD is strong because of a shortage of dollars outside the US but once all the USDs have been printed (trillions) and it filters to outside the US the USD will be much weaker so when looking at the NZD it wont weaken that much to the USD.

The bubble has been blown so enormous that a 20% drop still doesn't touch the sides of affordability.

So the government (taxpayer) would be directly subsidising and propping up the housing market.

Privatise the gains and socialize the losses?

Over my dead body.

Forget helping businesses. Help people from the bottom. Then people can help businesses by keeping them employed after lockdown with the help they've received from the government. Money flows up.

Direct universal payments. A UBI would be a solid permanent solution also.

Our economic system needs CONFIDENCE back. What businessman is wanting to extend debt in a world of uncertainty regarding their market and its desire to consume?! Pussy-footing around at the edges with "adjustments to tax regime, mortgage guarantees (hear stories that banks very cautious who gets funds), Companies Act amendments etc." will do stuff all.

The consume, the Consumer needs security of income; knowing next week they can pay the rent, pay power and have surplus to purchase that Latte.

We need a broad-based approach:

> Helping good business propositions survive in the short-run (particularly those that directly/indirectly require significant labour). Letting others fail.

> Propping up (or nationalising) infrastructure integral to commerce (energy, distribution, communications, finance [not required to large extent]) - most will have good balance sheets and already possess access to capital markets.

> Upskill and retrain our unemployed into sectors that will be needed in the future (technology, coding, engineering, manufacturing & science) - using tutors/professors made redundant due to loss of foreign students. Clear quota and rigorous application will be required - students will be paid a base living allowance, with incentive given to sectors that require it.

> Government can sponsor projects that employ large amounts of people asap. Focus should be on projects that have lasting benefit to the private sector and require minimal-training to start.

Perhaps we had too much confidence, called it a rockstar, but did the wrong things with it?

Some businesses will have to close. Capital and assets won't disappear, they will change hands.

And don't just blame Covid, it's simply the pin that burst the bubble. The main event is now the recession. Covid will probably be gone in 6 months and we will still be in recession. What is the answer then - Government money to underwrite every business forever?? Better to allow them to fail now, than throw good money after bad.

Some businesses will have to close. Capital and assets won't disappear, they will change hands.

Not necessarily. A barber shop closes. Just because the 'property" still exists doesn't mean it will be let to a new barber (or any other) enterprise. And if it does, the cost to the business owner is likely to be lower. Now lets say the barber wants to dispose of all of his clippers and barber chairs. They might sell or they may not sell. But they will likely sell at a discount.

Perhaps the argument here isn't what fiscal and monetary policy will do in a future sense, but what is has already done in the past sense, that will determine how many jobs will be lost.

God help us!

The Minister in charge of the development is no other than Mr KiwiFlop!!!!!!!

What chance have we got with this nil lot in charge?

Vote them out, we need people that have business sense in power

They are already in power.

It doesn't matter 'what's happened' in the past.

None of us could have expected to be where we are today.

So, at the risk of repeated repetition, the only thing that matters is "What happens next?"

Clinging on to 'what was' two months ago is pointless.

Would you prefer the zoologist to be running things ( Steven Joyce)?

No politician was trained to do what's needed of them now; none. So all we can do is look, listen and act, and react to whatever happens next.

By and large, I reckon they've done very well. Let's hope they keep it up.

Jacinda Ardern is great!and her govt will be ok.This is what I thought after all Jacindas promises in the last election to the people of NZ.Well how I have changed my mind.

Kiwibuild-a failure,No homeless-homeless has increased,including street people and people being housed in motels,Keep rents down-rents have increased,No new taxes- 7 new so called taxes,get immigration down-immigration has increased,clean up our rivers-more rivers closed!,and now when they finally get talked into putting NZ into Lockdown by our amazing top Doctors Professors and Business people it was too late!The borders should have been closed much much earlier and all people entering NZ put into 14 day Quarantine,so then the economy could keep going and we would not be in Lockdown.Now we as NZers all have to pay the price economically and it's going to be very tough and difficult times ahead!And yet Jacinda and Labour seem to have the upcoming election won already.Interesting how people forget broken promises so soon!

The main thrust of this piece is that the taxpayer should either loan high risk SMEs cheap money directly or force the banks to abandon their credit risk policies and lend instead ~ backed by the taxpayer

These aren't solutions they are simply kicking the can down the road.

Solutions could be ~

1. Govt grants for new businesses relocating to NZ with gtees of X jobs

2. The imposition of trade barriers to ensure some businesses (like Marsden Point) remain economically viable

3. Breaking of the construction supplies and food retail duopolies to decrease the costs of construction and living in the country

4. Immigration controls to prevent no value immigration ~ older family members being a prime example

5. Lower taxes on the import of capital goods to encourage investment

6. Establishment of economic zones in our less economically prosperous areas where corp tax is low

All we hear about is spend spend spend. We need more thought and strategy.

Agree Glitzy add to those revisit free trade agreements that take away corporate powers over government as well add international students to immigration ban . The duopoly on food and construction is a must break .economic zones to decentralize would assist regional towns and help with poverty in some of these regions as well as easing pressure on the cities also help with home pricing .

MMT 101 - the NZ government can always spend more money into the economy, and tax it out if there is too much already there. We currently have a massive hole growing in the economy, which only the government can fill. Fill the hole with new money, the public deficit doesn't need to be and shouldn't be removed/"paid back".

deficits to infinite and beyond

Aye aye captain

Capitalism it aint

The value of money will be imploded before our eyes

If I was in charge, I would simply spend until everyone was employed. This sets a value for money based on people's work time, which you will note is positive and finite, so no runaway deficit occurs.

many will have cancelled their newspaper subscription,their car insurance monthly premium etc; to reduce the cash burn rate and will be slow to renew them.sunset industries like newspapers are not worth saving .better to support newer technologies.

What the world economy needs is consumers with (viable) jobs

Tech only helps with efficiencies (lowering costs) but it is no silver bullet … hence the need (over the last 40 years) to leverage and releverage debt to keep things running

We are almost out of road to leverage

And let's not forget that the Finance Minister, in his speech yesterday, has faith in 'the State's power to Do Good'.

Now That should send a shiver up many a spine. I quoted C S Lewis in rebuttal yesterday, but the sorry track record of a plethora of central-planning efforts over the last century is another nail in That coffin. The notion that Der State Knows Best and can Do Good thereby, is a recipe for stasis, shortages, and for the ossification of the economy.

The reason is simple: planning of any stripe requires good-enough knowledge of likely demand (so there are customers for what's produced), better knowledge of Supply (so bill-of-materials per product can be costed and a margin assured), excellent knowledge of production processes including the all-important human and intellectual components, assured logistics (so Production can actually be ferried to Customers and inputs brought to points of production), and so on.

That's why there are so many disparate firms, supply chains, and actors, in production generally. It's simply beyond the capability of a few large entities to cover the billion or so SKU's that Matt Ridley estimates are involved in the British economy. Now try doing that with one State.....

Everyone Plans. This is not about Planning or Not-Planning. The hoary old Left/Right continuum can be viewed as one where there are Fewer Entities on one hand, or Many. many More on the other. But, and with qualifications and caveats, the Fewer the planning entities, the worse the practical results. The history of the 20th century bears this assertion out, in spades.

Beware the Do-Gooders, especially when they are wrapped in the mantle of The State.....which has wide Coercive Capability.....

I am going to agree and disagree Waymad. i suggest Robertson is correct in his assertion of the states power to do good, but he did not say the state knows best. I suggest your inclusion of here is unfair obfuscation. At any management level when setting policy and planning, compromises have to be made, and Government has got to be about the worst for trying to find that balance. So there will be winners and losers. There will always points the criticise, but unless we can see and understand all the information they have, and the rationale behind their decision process there will always be questions. The Government will have to be able to sell what comes out, and make it clear and as transparent as possible. Some will say this is a great time to be in opposition, not liable for what you do, but ready to criticise everything!

I'd suggest you take a gander at Michael Reddell's blog. His key and consistent criticism, and it bears directly on the "see and understand all the information they have, and the rationale behind their decision process " you espouse, is that there has been no release of any background papers supporting policy moves, lockdowns, or effect estimations.

Nothing. Zip. Zilch. Nada.

And this from the 'most transparent Gubmint evah'...

"The last century has seen government proliferate to unprecedented levels. The state now owns as much of a worker's labour as a feudal lord, says Dominic Frisby.

In ancient Athens many taxes were voluntary. At the other extreme, in authoritarian or totalitarian societies, such as Soviet Russia or North Korea, people have virtually no ownership of their labour, their produce or their profit. Government takes it all. The developed world today sits somewhere in between. Excluding inflation, itself a form of tax, roughly 45% of everything the typical Briton earns is taken in taxes. In France, the figure is an eye-watering 57% no wonder they're rioting. In the US it's 38%."

https://moneyweek.com/518855/weve-got-plenty-of-taxation-but-not-much-r…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.