Well, first it was six months and now it's for a full year, potentially.

Yes, that's the mortgage 'holiday' as we first saw it popularly styled, though you will note banks are tending to push the term 'deferral' these days. Which is fair enough. Because while your payments might be taking a break, the interest keeps ticking up. The deferral is putting payment off. But the debt's still there, and it's growing. Not much of a holiday really.

It will be interesting to see how many people do choose to extend out the deferral from the six months (starting in March) to now the full year (ending March 2021).

The Reserve Bank, which is overseeing the scheme, as it has been from the start of the original deferral in late March, is giving the distinct impression that while, okay, a full year's deferral is now available, it would prefer people not to use it.

RBNZ Deputy Governor Geoff Bascand in announcing extension of the deferral scheme last week said for many borrowers, resuming, or continuing payments in some form would "be the most suitable approach," rather than taking up a deferral of their loan payments.

'Not the default setting'

"A deferral should not be the default setting and it will be up to individual lenders to decide whether to offer one to their customers."

The reality is that when the deferral was first offered in March of this year, just prior to the lockdown, a lot of bank customers snapped the offer up. I was surprised how many.

The New Zealand Bankers Association, the industry body representing the banks, says since March 26, when New Zealand first went into lockdown, banks have deferred all repayments on consumer loans totalling around $21 billion for over 61,000 customers. That represents 7% of total consumer lending.

Nearly a quarter of those customers have subsequently restarted their loan repayments.

But that 7% was quite a chunk and it's therefore not surprising there are those out there who would probably rather see such numbers not being repeated or exceeded.

Going 'the full 12 months'

Interest.co.nz's David Chaston had a look at the situation at the time of the initial deferral and now we've had the interest.co.nz spreadsheet out again, doing an illustrative example of what might happen for someone who 'goes the full 12 months'.

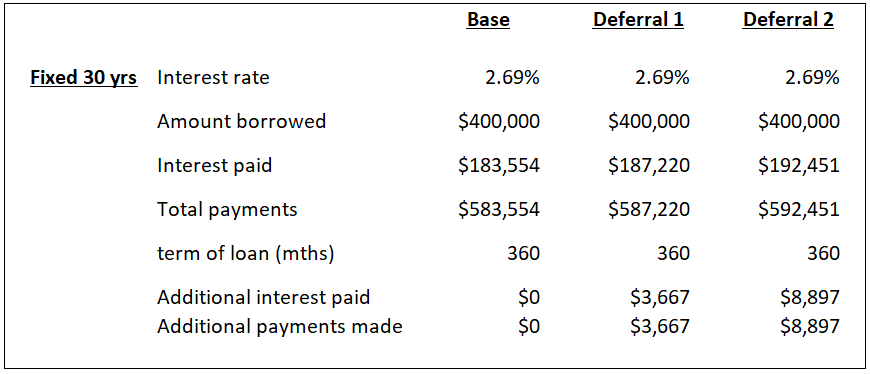

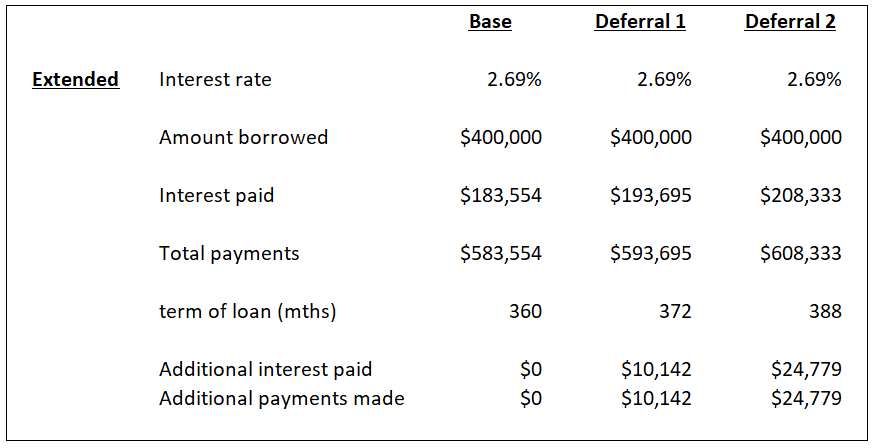

We should say, the example we've chosen (and these things are arbitrary) is probably something of a 'worst case' scenario, since we are making the supposition that our homeowner took out a $400,000, 30-year, loan, interest rate of 2.69%, as of March - and then immediately went into deferral. At time of going into deferral, our homeowner was paying $1,620.28 a month.

While this is, as said, an arbitrary example, it provides a useful illustration of some of the consequences for those who decided to defer and may defer further.

It's very much worth noting that there's no hard and fast approach to what happens when someone comes out of deferral. The banks, it seems, are looking at it on a case by case basis according to the needs and situation of the customer. Which is what you would hope.

Results may vary - a lot

We've looked at two differing approaches in our example and the thing that's worth bearing in mind is that there's very different results based on how you decide to proceed after coming out of the deferral period.

The examples we cite here (based on the $400,000 loan over 30 years at 2.69%) are for the mortgage holder to either:

A/ Increase their monthly PAYMENTS after coming off deferral in order to pay off the loan in the original timeframe, or:

B/ Keep the payments the same, but increase the TIMEFRAME for paying the loan off.

This is the basic outcome of option A, noting that 'Base' refers to what would have happened with the mortgage continuing as usual, 'Deferral 1' covers just the six-month deferral, 'Deferral 2' takes in the full year.

Some quick arithmetic on that:

In order to pay off the loan in the same timeframe under 'Deferral 1' for six months, our homeowner would have to increase the amount they pay each month from the original $1,620.28, up by $33.51 (a 2.1% increase in payment size). Going the full 12 months, or 'Deferral 2', would require a hike in monthly payment of $81.76 (a 5% increase).

Notwithstanding that our mortgage holder would need to be paying more each month they would, owing to the wonders of compounding interest, still need to find in total across the life of the loan an extra $3,667 (for the six month option), or $8,897 (for the full year). That means they would be paying 2% more in interest across the time of the loan if they defer for six months and 4.8% more with a 12 month deferral. In terms of total repayment, someone in this example deferring for six months would pay 0.6% more money (that's interest and principal) across the life of the loan than they would without deferral, while someone deferring for 12 months would pay back 1.5% more money.

Okay, so what about if we decide to keep our monthly payments the same and increase the time taken to pay the loan off? This is where it gets real interesting.

Now, you might not think it would make that much difference, would you?

Here we go:

In this example, keeping those payments at the original $1,620.28 a month, we would need to keep going with the mortgage for an extra 12 months, with 'Deferral1'. So, yes, the six month 'holiday' would keep us on the treadmill for another 12 months. But it wouldn't just cost time. It would cost $10,142 more, which in terms of our interest bill would be 5.5% more than we would pay without a deferral. And in terms of overall payment (interest and principal) it would cost us 1.7% more.

And the 12 month deferral? Well, that would hike the interest bill by $24,779 - some 13.5%. In total, including principal, we would pay 4.2% more across the term of the loan than we would without the deferral.

Time is money, they say. In this instance it really is both. For the 12 month deferral, we would have to extend our payment time by a whopping two years and four months. That's two years and four months of your life you ain't getting back!

A couple of other points to note that apply to both examples:

Assuming we had continued to pay the mortgage after starting in March, the principal would have reduced to $395,678.05 by September. With a six month deferral, regardless of the payment option chosen after restart of payments, the principal would stand at $403,816.32 upon restart. So, the six-month 'holiday' would have seen us racking up an extra $8,138.27 in debt - which works out at $1,356.38 a month. Expensive holiday.

Twelve months? Well, worse. I think you probably figured that. By next March our principal owed would have blown out to $410,167.99 - so, that's an extra $19,684.23 owed, which works out at $1,640.35 of extra debt piled up for every month of deferral.

Final thoughts

You might conclude from the perceived tone of this that I'm suggesting people should not go down the deferral route. Actually I'm not - and I'm not in any case a financial adviser so I would not advise. And the fact is, everybody's financial situation is going to be different. And for some people, being able to put the mortgage payments on ice for a year may be just what they need to ride out the storm. It's not one-size-fits all.

But I think RBNZ's Geoff Bascand is quite right to caution against the 12 month deferral being the default setting.

There's no such thing as a free lunch. A bit of crunching of the mortgage deferral numbers shows us that.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

66 Comments

Yes. But that's at 2.69%. The lower rates go, the more borrowers will become trapped in situ by the facility.

At an extreme (or is it?!) 0% the loan never has to be repaid. Duration is academic and interest due, non-existent.

All you have to do is be able to sell at the amount you borrowed (your equity is your concern), or more when you want and life goes on.

But what if you can't achieve that price level? Answer: You stay where you are.

The other aspect of "extend and pretend" - trapped capital, that remains a drag on economic growth for years to come.

The problem is the value of your asset will be dropping at the same time as you are accumulating more debt. The reality is if you are on deferral, then you can't afford your loan. This is not going to end well for anyone now.

the economy is on life support for now and the wage support program will end at some stage. This will be the testing time for everything including housing market!

"And I'm free, free fallin'

Yeah I'm free, free fallin'..."

Perfect choice of lyrics. Yes "free" from payments, but "free fallin'"in debt.

Some people might like to examine life cycle of a mortgage v average age when taken out

Then, look at when people tend to get thrown out of work. 30 year loan say; usual age about 28? Then which age is it employers like to get rid and replace with cheaper young folk? About 55?

Lots more insecurity for over 50s to be followed by reduced returns on investments with pension pot payments eroding every year and deposit rates being derisory. Finally, bear in mind which demographic has most wealth? And what happens to economic growth if they get hit?

Lots more insecurity for over 50s to be followed by reduced returns on investments with pension pot payments eroding every year and deposit rates being derisory. Finally, bear in mind which demographic has most wealth? And what happens to economic growth if they get hit?

Economic growth gets smashed as the wealth effect disintegrates. This is the single biggest threat, which nobody's giving any thoight to and nobody really understands. I've accessed some papers done by RBNZ on their position but have not yet had time to go through them.

It seems the great unwashed have thrown their lot in with the ruling elite and believe that asset prices are heading to the moon.

I think a decent amount of people are aware our economic growth is mostly a monetary and immigratory ponzi scheme? That’s what most of the debates are about in interest comments it seems.

I think a decent amount of people are aware our economic growth is mostly a monetary and immigratory ponzi scheme? That’s what most of the debates are about in interest comments it seems.

This is not the 'wealth effect.' The wealth effect is more related to the multiplier effect in the consumer economy caused by people feeling wealthier and spending more (volume and value) potentially beyond their means. The wealth effect is best understood from a combination of behavioral and maco-based economics. To be honest, I don't think many people really understand it well because it's hard to quantify. People who work with consumer data analytics should understand it (the proprensity to purchase high-margin products and services increases accordingly with the wealth effect). The govt and central banks implicitly understand it but don't really want to talk about it. It does have a veneer of false economy.

You mean the wealth effect created by our houses going up in value propped up by our money creation system?

I understand the wealth effect. NZ’s wealth effect is underpinned by a ponzi monetary system.

Well that's a very broad brush you're using. I'm more interested into the relationship and how housing bubbles support the wider economy.

The more important thing to most users of this facility is to stay solvent in the short term and protect their investment over the period that they anticipate staying in that property.

Given that for the large part the mortgage holders are not likely to stay put for more than 5 years anyway then the 30+ year scenarios are meaningless to them, they are only interested in protecting their equity in the short term and planning for a cash out in the medium term, when they can refinance the whole shebang on terms to suit.

Cash is king in this scenario and holding back 12 x $1620 (nearly $20k) as a buffer could be seen as good financial planning. They can always just pay it back in after 12 months and catch up if things go ok, thus no real penalty.

Quite right.

And as long as property prices don't fall, then all's good.

But if they do ( and as I asked yesterday" Why do we think interest rates ARE so low?" It's not because the risks are at lifetime lows!) then deferral works against you.

Kinda. Depends if you are trapped and want to move before your losses have recovered, if your property value recovers before you need to sell and you can return to employment and serviceability etc, then a mortgage deferral might work for you. There's a potential opportunity cost of the trapped money in the house, but equally, depends on how much you would be paying in rent elsewhere.

To minimise risk and it’s negative consequences, one needs to be prudent.

To be prudent one should see mortgage deferrals only as an option when in need. The number of those taking this option when it first became available and when business and job support were in place - and the full economic impact of Covid had not been fully realised - suggest that many were not being prudent. This is reflected in the number of initial applications declined by banks.

To avoid risk and it’s negative consequences, one needs to be prudent.

True. But the nature of the housing market itself has not been conducive to being 'prudent' at individual / aggregate levels. If housing costs were lower and people had more liquid savings (trade off), then mortgage deferrals become less necessary.

The negative consequences of bubble economics are biting everyone on the ass. It shouldn't really be any surprise.

Exactly. It's not prudent to invest in housing at current prices for a lot of people.

Yet it's not prudent *not* to if you believe that prices will keep rising.

Low interest rates force people into risk.

(Also LOLing that they consider $400,000 for 30yrs a 'worst case scenario'. You would not find a single FHB in Auckland getting a mortgage for less than that.)

J.C you seem somewhat concerned New Zealand's 1.25 trillion in residential property is problematic, or that the fastest growing sectors of the economy during the past two decades, and spread across almost every region, are somehow related to the same asset class . Given the relative rate of change in the OCR has never been higher than present, in absolute terms, the change in the OCR only briefly behind a short period in 2008, that ditto for the ubiquitous 2 year mortgage , and that in absolute terms the increase in residential real estate values has never been higher than at any time in New Zealand's history during the past three years, I cannot see any potential problem ,particularly in light of current conditions. I'll have one of those interest only, 100 percent ,negative mortgage thingy's ,and defer it if it helps, at least I believe Mr Orr is in that boat.

Hmmm, 1 Orr might row that boat around in circles.

All good....

Incomes fall for first time since records started....Stats NZ labour market statistics for income in the June quarter showed median weekly incomes were lower in the June 2020 quarter than they were a year ago, down 7.6 per cent

Just defer at little longer....

Thanks for highlighting this. I haven't been following this, but it is no surprise. Actually it's more pronounced than I expected.

If I was a gambler, I'd go for the deferral, betting that in a year the price of the house will outweigh the extra interest incurred. With a better cashflow to boot in the meantime. Win win.

The price of the house only matters when you come to sell. If you're selling next year and it is worth more, then it is indeed a win-win.

But if the price falls slightly or stays flat by the time you sell in 5 years time, then you may not have won.

Look around you. House prices will not fall.

Could the banks offer a free Break option as well?

So borrowers on a fixed could break for free (from April to Nov) - and then they could refix at reduced rates, and either keep their repayments the same or lower.

And perhaps banks could show their gratitude to all the borrowers who carried on making their repayments faithfully?!

Thats like putting a band aid over cancer.

Why should those that can afford repayments over this time be rewarded by the banks?

Helping borrowers get out of higher fixed rates and into newer lower rates quicker would Be in line with RBNZ goals.

Rewarding those who carried on paying their mortgage during lockdowns and job setbacks is a positive incentive to reward and encourage this behaviour - so a win-win.

That will just make the rich richer.

Good luck with that one. It will go down like a cup of hot sick.

A household where one partner lost their job or part of a job - & continued paying their mortgage is not an example of the rich getting richer.

Why shouldn’t the banks share some of the Covid/economic disaster?

The time lag from OCR cuts to mortgage rate relief is too long currently.

Apply it to renters who faithfully continue to pay their rent and you might get more traction.

Seems they've been receiving plenty of help from the governments and Reserve Bank over the last few years. More welfare is needed / justified?

As far as fairness goes, underwriting the switching costs to mkae it easier for families stay in homes is a fairly basic win. Maybe make it available to FHBs still living in their first home or similar if you are worried about it being rorted by well-off owner occupiers.

I don't know that the same banks who reward long term faithful credit card customers by charging them 23% interest but offer 2% balance transfer interest rates as a inducement to new customers to swap to them will be rushing to do this.

Any thoughts on how a mortgage deferral affects (or doesn't affect) your credit score would be enlightening.

Should a deferral affect your ability to tap into future deals reserved for "good customers" this will store up quite a bit of future pain for many borrowers.

This is what happened in the UK after the GFC, which was known as "the credit crunch". There were carded mortgage rates at 1.5% available but only if you had 60% LTV and an impeccable credit score and secure job. I had a 25% deposit and was offered between 2.55- 3.04% (depending on length of fix). People who had negative equity got stuck on the floating rate because their bank refused to offer a fixed. They were known as "mortgage prisoners".

I can confirm that a mortgage deferral doesn't count as an "impaired loan" meaning it is still regarded as a "performing loan" by the banks and therefore does not affect a borrower's credit worthiness

Yvil, the processes/ rules regarding defining impaired loans and those cruching credit scores are entirely different processes.

For example if you had a habit if occasionally missing your credit card payment this would not be an impaired loan but would affect your credit score. Likewise a loan restructuring would not be an impaired loan but would affect your credit score. So the likelihood is that a mortgage deferral would impact your credit score (and hence your eligibility for certain loan rates etc).

Glad you agree with me Glitzy, as you always do

When the world has come to an end and humankind has been wiped out at least we can all be confident that the NZ housing market will still be going strong.

If your property, or yourself, has income sufficient to support this, isn't this just a way on extend and pretend on your debt. Aka those that can afford this just see it as an extension of cheap finance?

This is overly simplistic, and makes too many assumptions

The key one being that people intend to string the mortgage out that long in the first place...

For most mortgages only ~33-50% of your total annual payments goes towards principal in the early years of an amortization loan - so by hammering the principal early you dramatically reduce the total interest cost

For those a little more savvy will know that targeting the actual principal, ideally through ad-hoc additional payments while extending the term so that your cash flow improves (so you can apply the rest of what you would have paid anyway to actual principal...) is a much faster way to pay off a mortgage especially in the first 5-10 years where most of the interest is accrued.

Thinking that 'increasing you monthly payment' is the best way to pay it down quicker is simply bad thinking as you are still paying interest on every single payment as it is amortized.. so again 30-60% of that payment is still pure interest so while extra payments do pay it down faster, they still leak money at the same time

There are much smarter ways to do it, including basics such as increasing the frequency of payments to fortnightly or weekly + adding additional principal only payments which go directly to principal and literally cut-off any future interest on that principal

Not talking about investment loans (which you may intend to never pay off) or more advanced debt repayment strategies, but deferring a loan now doesn't mean it has to string out for 30+ years

Paying $1,000 in extra principal per month for one year will save you more interest over the long term, than saving $1,000 a month and making a lump sum payment of $12,000 at the end of the year.

The different won't be huge, but it is there. The downside of paying the $1,000 per month extra is that you don't have the cash available as an emergency savings buffer. But equally the money won't be available to splurge on nice-to-haves like an overseas holiday because you feel like you 'deserve it' for whatever reason your brain comes up with to justify it.

Yes either chunking at the start of the year or paying more monthly is better than at the end of the year - sooner is better,

'emergency funds' sitting in a savings account generally erode in value and basically do nothing for you

Shares growing at 8% (- 2% inflation) is still less than the 45-48% interest that you will pay for every dollar in the mortgage example above - and you have zero control of them

'emergency funds' sitting in a savings account generally erode in value and basically do nothing for you

Unless you have an offset mortgage :)

Exactly - 100% agree... equity line of credit which can be accessed for more productive uses

Can't go too deep as most people won't understand or simply get defensive of the 'status quo' that they have all been taught and accepted

i.e. offsetting amortized vs. simple interest loans, while also releasing equity at the same time... and on and on....

Hardest thing to change is a mindset

Tabled mortgage milestones ( or millstones)

https://www.interest.co.nz/calculators/principal-payback-milestone-calc…

You need to look at the whole picture, not just the mortgage (or correctly, the loans that are secured by mortgage). If you are on a wage, and with a house, home loans, short term credit and KiwiSaver, you need to make assumptions on wage and general inflation, share growth, and Interest rates before you can make a decision. On my 5year assumptions (share growth 8%, inflation 1%, interest rates 2.5%, house inflation 2.5%, short term credit 14%) it’s hard to go wrong with mortgage deferment and increasing home loan debt and still service it in a couple of years time, pay of short term credit and buy shares.

If your shares are returning 8% and your short-term credit is costing you 14%, you should be selling your shares to pay down your credit any way.

Unless that triggers IRD to classify you as a trader and hence be subject to tax on all of your share returns.

Depends entirely on your purpose for buying the shares.

If a pattern is established then it doesn't matter about the "purpose".

Good article!

i wonder what will happen after we go through another 4 or 5 lockdowns, will deferals end up being 36months or longer.

I think everyone seems to be of the opinion that Covid is a 2020 issue and life will be back to normal next year.

What if its not and we have to deal with i for years with multiple lockdowns each year... This to me seems to be the most probably scenario at this point and is the answer always going to be defer, defer, defer...

I struggle to see a situation where someone who cannot afford their mortgage now, will be in a better position to afford the increased mortgage by March 2021… sooo further mortgage extension to March 2022? Seems likely to me since the RB and Government clearly have the aim to go to infinity and beyond to cocoon everyone and not let anyone fail (read QE, negative OCR, various subsidies and also, most likely, mortgage deferrals)

Yes, exactly. Then if we are in a deflationary environment, it will go on for a decade or two, a-laa Japan. Which is why I have been saying I suspect we will have forever LRH's. Or they will be bailed out to "pre covid" amounts. Or we will see mass debt jubilees or similar.

This is what happens when the head room that is dual incomes is slowly eaten away by the ever increasing debt ponzi. Imagine if mortgages were limited to 3 - 4 times single persons salary even at 10% mortgage rates? A $200k mortgage @ 10% = $419 per week over 25 years. But we must not allow people to keep more of their money and spend it in the economy during good times......

But then how would the banks reap record profits year after year at the expense of New Zealand?

deleted, I found my answer elsewhere :)

Slightly off topic, but I would be interested to hear people's opinions of Simplicity home loans - at the moment their rate is 2.25% (so, a bit lower than the fixed one year rate of the main banks, which is mostly 2.55%). Is the difference in rate enough to make it worthwhile, given that you can't fix, or tap into equity, or get a bridging loan or anything like that with Simplicity, and there are no cashbacks (as I gather the main banks are still doing, at least in some cases).

By far the biggest hurdle is not the lack of cashback or inability to get a bridging loan etc, it's that you have to win a lottery in order to be offered a loan to begin with.

Right, but assuming you had - do you reckon it's worth taking over a bank mortgage?

For me personally it would be, because I don't foresee needing any of those other features that banks offer.

It would be interesting to know how many enter the ballot monthly. What I like is that they have fairly strict criteria (I.e loan payments can’t be more than 30% of take home pay). The freedom to make larger lump payments off your mortgage coupled with the best interest rates in the market (assuming rates continue to drop as expected) is enticing.

Outstanding article David.

A lot keep thinking banks are giving mortgage holiday as a charity act while they are actually preserving their own interests while making some extra money at the same time, why not?

b21

Agreed.

There are still some on this site who believe mortgage deferrals mean that those with mortgages are either getting free money or their mortgage paid for them by the government. No matter how often this is clarified - including in this article - there is still that belief.

During Deflation this is akin to borrowing on your home to pay for living expenses.

Debts are rarely written off.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.