By Jenée Tibshraeny

The Labour Party’s policy to introduce a new income tax rate of 39% on income over $180,000 is a safe, if not tokenistic, move.

The politics behind its call is obvious - the party doesn’t want to rock the boat this close to an election.

Yes, it has earned a lot of political capital from its Covid-19 response, so could arguably make some attempt to be a little more “transformational”.

However, Labour’s finance spokesperson Grant Robertson is of the view there’s little public appetite for further change, on top of what Covid-19 has thrown at us, so now’s the time for “stability, certainty and balance”.

But perhaps more importantly, he knows if Labour gives an inch on the tax front, the Opposition will take a mile.

National will also keep pushing the line that should Labour and the Greens form a coalition, Labour might be forced to adopt some of the Greens’ more ‘out there’ tax policies.

Labour is sensitive to the issue. Jacinda Ardern didn't join Robertson to make the policy announcement, keeping "Brand Jacinda" clear of tax.

The politics behind the policy is clear. Here’s a simplified version of the economics - which will also be obvious to interest.co.nz readers:

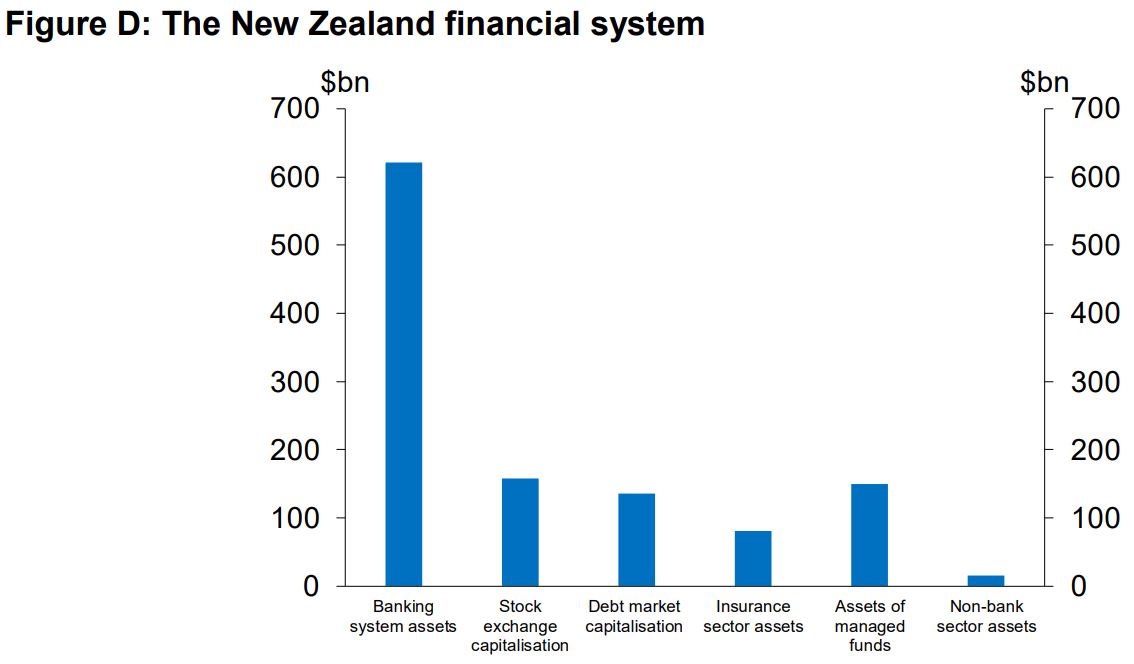

Our financial system in built on housing.

The value of outstanding New Zealand-registered bank loans secured against housing is $282 billion.

This is equivalent to 59% of all bank loans, which comprise 77% of bank assets. These bank assets make up the bulk of the country’s financial system:

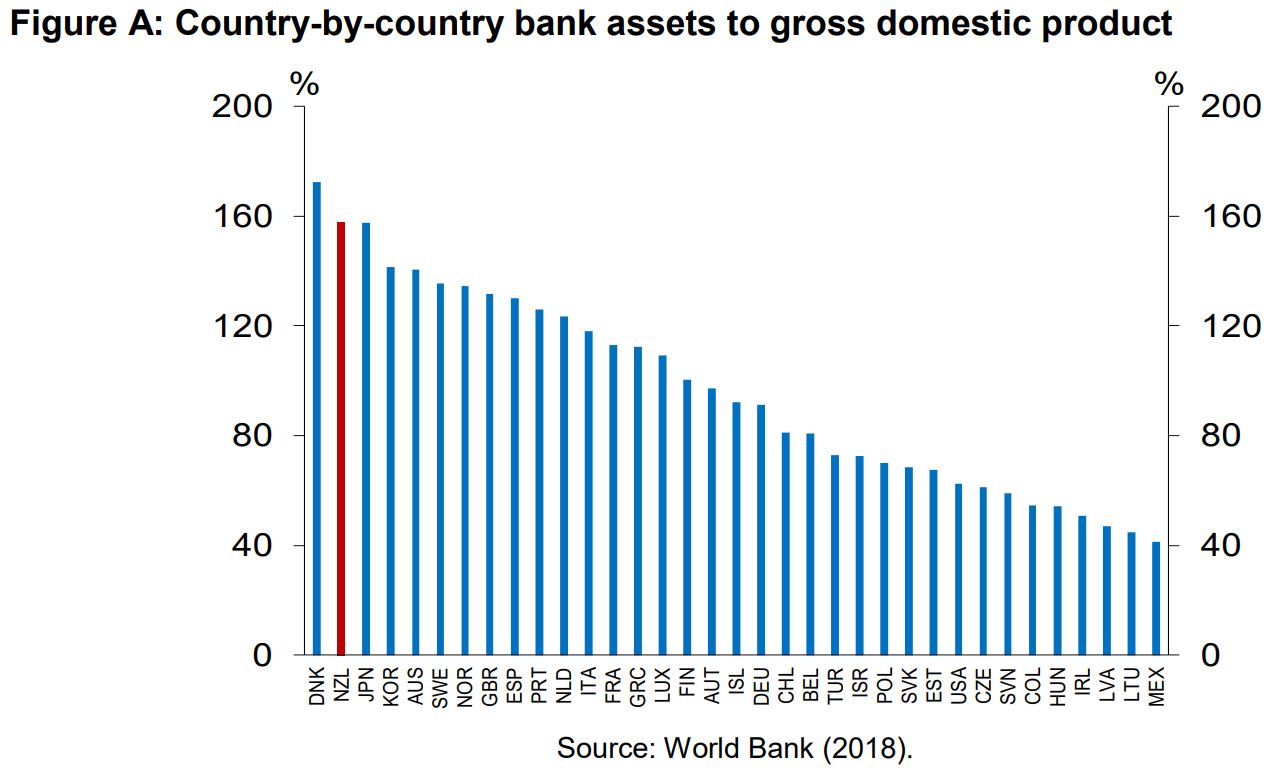

The value of these bank assets relative to the size of the New Zealand economy is enormous by international standards:

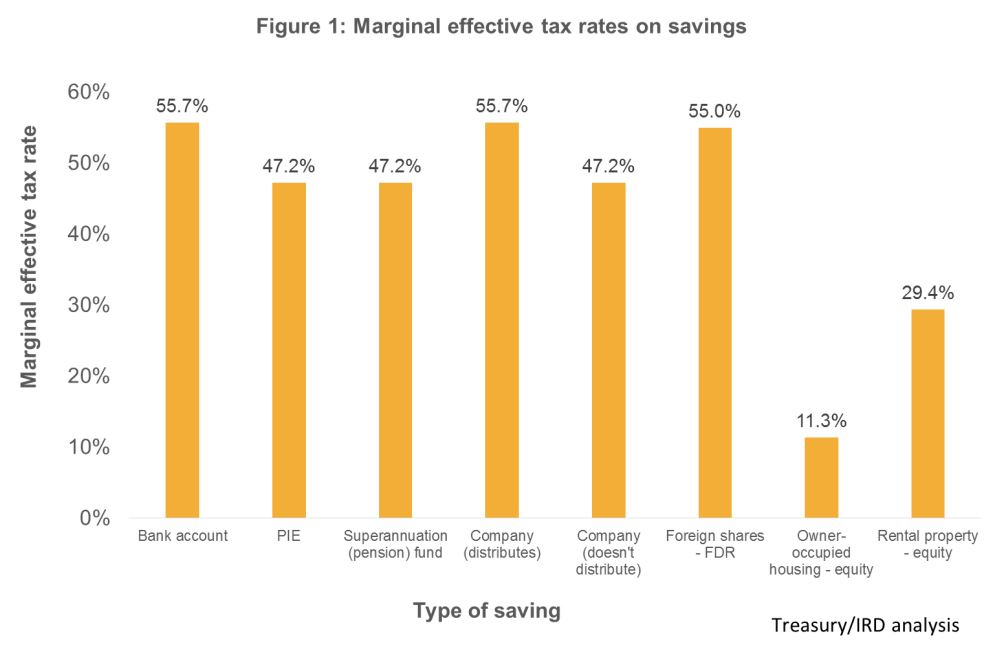

The financial system relies on house price growth and the country’s tax system supports this:

New Zealand’s approach towards monetary policy also supports this.

If inflation and employment fall below target levels, the Reserve Bank is required to use its tools (the Official Cash Rate, quantitative easing, etc) - which aim to lower interest rates - to get the economy back on track.

What do lower interest rates do? Encourage people to take their money out of the bank and invest it in property or shares, driving up asset prices.

High levels of immigration and a convoluted Resource Management Act, and thus supply falling behind demand, have also contributed to house price growth in recent years.

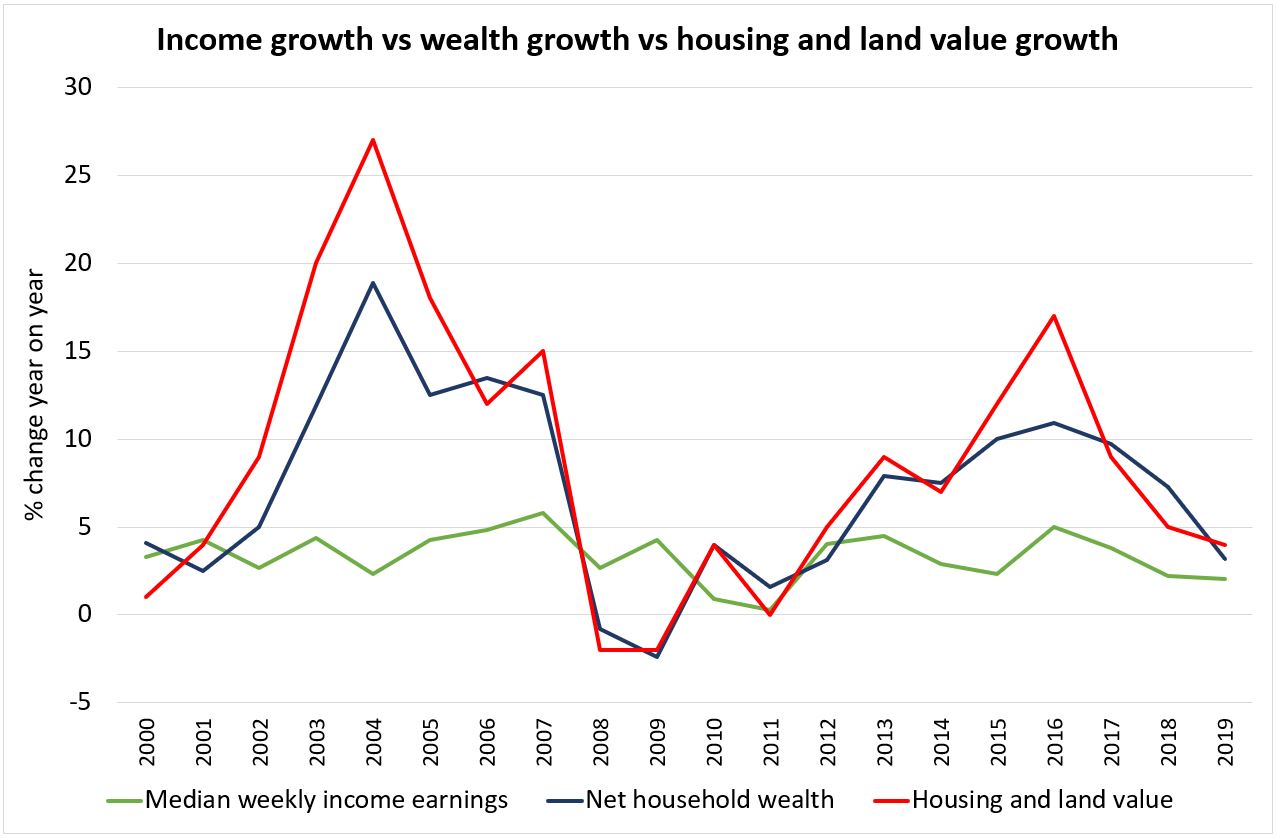

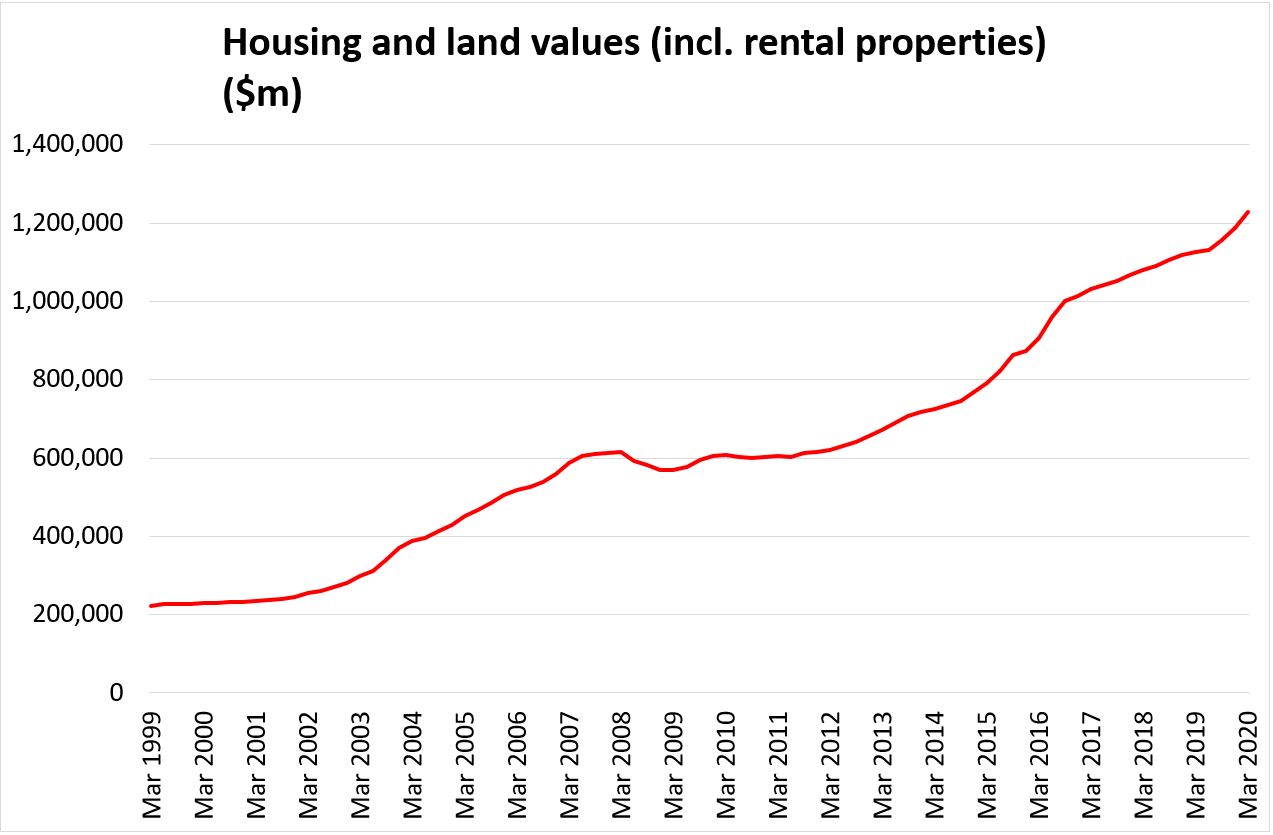

With this combination of factors, it’s no wonder housing and land values, and thus households’ net wealth, has grown much more on an annual basis than median weekly income earnings (income from wages and salaries, self-employment, and government transfers):

The country's housing and land value has now reached $1.2 trillion - more than five times that which it was 20 years. $1.2 trillion is also about four times that of the country's annual gross domestic product (GDP):

Logic would say New Zealand has over many years been putting too may eggs in the housing basket, and the government needs to remove the incentives to change this - if not from an equity or equality perspective, then from a financial stability perspective.

But doing anything to erode confidence in, let alone decrease the value of, the behemoth that is the housing market, takes a very brave government.

A government led by this Labour Party is not that government.

Robertson’s steady as she goes approach aimed at providing certainty and thus confidence is a fair one. It made particular sense at the May budget when there was little understanding around Covid-19 and where it would take us.

But we have a slightly clearer idea now. The spread of the virus is at bay. It is time to start the discussion around the relationship between the tax system and the country’s housing giant, not completely shut it down for another term of government.

Covid-19 is already forcing structural changes to the economy. If it’s too difficult politically to pivot the economy in a more sustainable direction now, it’ll be near impossible once people settle into the new norm and the stimulus being provided further entrenches wealth created from assets.

136 Comments

Thanks. We all know that only economy in NZ is Housing.

Government and Fed have gone all out to support housing (more than actual bisinesses / other industries) but by creating hyperbubble are only delaying the inevitable as decent correction in any asset class be it stock or housing is good and economy cycle of (up and down) can be delayed but cannot be avoided BUT again this government for now is looking till election.

Government and Fed have gone all out to support housing (more than actual bisinesses / other industries) but by creating hyperbubble are only delaying the inevitable....

If the bubble bursts, NZ is toast as the wealth effect disintegrates sending the consumer economy into a tailspin. If the govt knows it and the central bank knows it, they definitely wouldn't talk about it candidly with the public.

Are you sure that if house prices crash (a 50-60% reduction in house prices reduce the median house price to $300k which is about 3 times the annual income of the median family) it will be a good thing? I am just asking. What will happen to the economy, jobs, investment etc if that is to happen? Credit creation does not favor houses automatically, it bias towards the housing market in MHO is due to the fact that more money in industries and businesses is unlikely to have a return justifying the risk. I do not see how a crash in housing and assets will improve that. NZ is such a small market, so most of the money in things other than housing must come from selling more to the world. And NZ is at peak production and selling what it is best at already and have been there for a long time.

Why the assumption NZ is at peak production and selling what it is best at already and there is no viable way to increase exports?

Why is having high house prices, record household debt, and massive profits flowing to Australia each year a good thing? And how do you see that as an economically viable model to take forward and keep increasing?

I do not see expensive housing as good. But I do not agree that 1) credit creation (while obviously a factor) alone is to blame for housing unaffordablity 2) money that flows into housing is depriving the productive sector of NZ from so much needed oxygen.

on point 1: from 2000 to 2008 interest rates were increasing but the house prices increased even more than they did in the 2010-2020 period. Housing unlike many other industries, cannot be send off shore, and the housing trade organisations have very strong hold over the protected house building market, with very limited liability for their performance I have to add. This also applies to proving needed infrastructure. Just look at how much it costs in NZ to build a KM of road. The only way that such expensive projects can go on, is to fuel them with debt. And as there has always been great demand for housing, the politicians were happy to let banks create a credit frenzy. Just imagine if houses were not going to be built because banks were not lending anyone more than 3 times their annual income. Again, I am not sure if billions of dollars we pay to Australia is doing any good to us, but I can see that is the only way we can keep building expensive houses. Expensive labor, monopoly on material, GST and other taxes, council fees etc all add up. We have had a crazy, mad, massive explosion in our house prices and yet our house building slags behind so much. Without the debt frenzy, we would have even less number of houses, thus more expensive housing. If you are going to blame immigration for that, go on, but then you will be more on the money than just blaming "credit creation by banks".

2) I look at NZ export mix over the past decades. It is dominated by primary products, specially dairy. I also hear from government officials that we have already too many cows. I.e. the industries are already heavily invested. Same for wineries etc. So what is NZ proven to be good at does not need any more money.

Now, there is always great potential in innovation. But innovation is hardly ever funded by commercial banks for very obvious reasons (the very high risk of failure would require charging an interest rate that no start-up can afford, the best way to fund innovation is from shareholder equity).

So, no money is being stolen from "productive NZ". It is the lack of demand for money that can be realistically repaid that had pushed banks to focus on residential lending.

In summary, we either through bad policy encourage increased demand and all money into easy property investment, and throw up our hands that we have no value to offer but primary products, and we rely on a standard of living reliant off more and more debt...

OR

We encourage productive investment, living within our means, and free money that's been pushed into property for other purposes.

Your argument re expensive housing does highlight why previous generations' governments were so active in boosting housing supply, acknowledging the importance of supply.

You have summed New Zealand problem in a nut shell But the powers at B (everyone) just won't listen. Too painful

Life goes on.

housing is the back bone of NZs economy and its livelihood.

Agree as NZ has no other meaningfull economy but housing and if it crash for any reason will be bloodbath so has to be avoided at all cost.

Market correction in any asset class should not be manipulated as are healthy in long run but as housing is the only economy in NZ- Politicans of all breed are paranoid even by the very thought, what if it corrects.

The bloodbath has already occurred...the bloodbath is the bubble.

Wrong.. housing in NZ is the backbone of offshore banks profit margins. If housing retrenched by 50% ( and it won't) the only losers are the banks

The irony being - higher house prices make us collectively poorer! 194% of GDP's worth, and rising, at the moment.

I'd have no issue with the median house price being $10 million IF the productivity of the country supported that. But it doesn't. Neither does it supports $1 million or even $500k.

The higher prices go, in the absence of productivity based income rises, the poorer we all are. Because - we have to borrow-more-to-buy what was previously at a lower price, and if wages can't allow that - borrowing from future income has to.

We are on the path to poverty, but we just don't, or won't, accept that.

True, and this is especially applicable to the new generations.

The only ones to get an advantages out of this paradoxical situation are the parasitic house speculators, all at the expense of the real economy.

Why do you call the average "mum and dad" investor parasitic? Some people are trying to increase their overall retirement savings, calling them parasitic is an insult to many hard working Kiwi's

It's an insult to many hardworking kiwis that they're expected to spend extortionate amounts of the money they actually earn by working so mum and dad investors can enjoy massive untaxed gains

Question:

Who is the Richer family?

(1) One with a home 'worth' $1 million and no debt or

(2) One 'worth' $10 million and $9 million of debt?

New Zealand's answer is Family (2) - Because the value of their house is going to double to $20 million and pay off the $9 million in debt, whereas Family (1) will only see with Net Worth increase to $2 million. Right?

Forget about the small fact that at the slightest correction in prices Family (2) will get wiped out and the one without debt will be just fine, what we ignore is that to sell for $20 million someone else has to stump up with that money. And in all probability, it will be borrowed adding to our gross national indebtedness.

That worked for 40 years and those days, for one of several reasons, are over. But we just refuse to see it.

Whatever way we look at it, housing in NZ does have all the typical characteristics of a gigantic Ponzi scheme.

I wonder what the percentage of oversea buyers is these days, and whether many are now selling out of the NZ market. It was a reasonably large percentage down in Queenstown.

What you say has some truth. No one is ignoring it. But, what's the alternative?

Your options are:

- Be mad at the system and wish/hope that it changes.

- Rent, which will continue to rise. Or if you continue to pay the same amount, the quality of your rental accommodation decreases.

- Buy, a home that you're going to live in for 30-35 years. (in which case the correction over the short term will have little impact).

If corrections over the short term will have little impact, it should be let to happen.

100% agree

I disagree with your calcs, Family #1 are by far the richer, they are freehold, have no outgoings to pay a mortgage, and can enjoy their incoming salary unencumbered. Those who chase CGs will eventually trip up, those who don't are by far happier

NZ answer is #3

(3) One 'worth' $1 million and 5 rental properties with $5 million of debt.

Yes, this is the problem, they should never have allowed house prices to go so high. But there were a lot of things pushing up house prices, and at the moment the main thing seems to be the low interest rates. We should have listenedd to the experts where house prices should be restricted to a certain ratio of average income, which can be done with taxes. So in the future we probably have no option but to have some pretty nasty taxes come in. eg Stamp Duty, Capital gains tax, land tax, inheritance tax etc. When this could ave been prevented if we had just not allowed houses prices to go so high,. Yes housing 'affordability' may not have changed much, but that is solely down to the record low interest rates, but it still means that people are paying huge prices and getting into huge debt for their home, and now require a huge deposit..

The irony being - higher house prices make us collectively poorer!

Double irony. The wealth effect is the key driver of incremental consumption.

Because the folk without it are being squeezed by the bubble.

Labour party = National party

Power corrupts.

Correct. But don't look to Politicians for the solution

Don't forget the impact of women working on the need for 2 salaries to buy a house these days.

Just one of the many ways in which 'household incomes' gloss over the increases in affordability issues. Throw in not mentioning how many hours people work (especially those on salaries) a week to meet housing and living costs. You'd think this would be a well-being issue, but apparently not in a way that counts.

All these resources and money wasted on housing are diverted from potential investment and productivity increases in the real economy.

Moreover, families who have to pay big mortgages have much less money to spend on any other economy sector.

All of this to keep parasitic housing speculation inflated against the natural balance and self-correcting mechanism of a normal marketplace, perverted by reckless quantitative easing and irresponsible and structurally damaging ultra-low interest rate policy.

What is your basis for saying that? Do you believe that if mortgage was to be banned, billions of dollars would have flown to businesses and industries? what business and industries in NZ have real unrealized potential that requires money? Primary Industries, where NZ has a proven record in performing, are invested to the hilt, any additional investment is likely to make diminishing returns.

What is to be done though? Until the monetary structure we operate is changed, housing will be untouchable. If the monetary structure is changed, many people are in for a rude awakening.

My best guess is we ride housing until the wheels really fall off. Only that would give genuine change a chance.

can you give an example of change that wasn't violent? I can think of plenty that were.

Jeez Andrew, I didn’t mean anything violent! I meant until the system collapses like housing in the US.

that will be close to a reset with this much debt on non baby boomers. you will destroy a generations wealth and the outcomes are unknown.

Which generations wealth and what wealth?

The homes are still there, the factories are still there, the farms are still there...

What's destroyed... the illusion of wealth?

the wealth they pledged to the banks to cover the mortgage.

Debt they took out for wealth they cannot earn.

So it's been decided, we must destroy other generations to cover for these folks' poor decision making.

The system didn't collapse in the US per se. It was shorted by investment banks that lent to totally unrealistic and and unrecoverable debt holders. Once again the so called "experts" either have no clue or have a vested interest, and "Joe average" pays the price

Roger Douglas and the Lange Labour Government introducing the "free market" economy.

This. It's pretty clear now that we are going to ride it all the way till we fall right off the cliff. At least real change will be unavoidable at that point.

I think that is the plan..... Have listened to many commentators around the world and there is a collective thought that at some point the debt burden will be too much for the 90 percenters. At this point of desperation the central banks will issue their solution to the masses who will be so desperate they accept what’s proposed. All this in the name of cheap credit and false GDP. Give me high interest rates and much much cheaper housing anyday! Would have completely avoided the Financial mess the entire world is now in. The cracks are showing in Australia, are we very far behind?

Have listened to many commentators around the world and there is a collective thought that at some point the debt burden will be too much for the 90 percenters.

The burden is already too great. That's why the govt has to pay for people's incomes.

On top of the existing property investor social welfare subsidies of the Accommodation Supplement and Working for Families.

It certainly is.

It's pretty simple @Withay. Tax captial (housing) fairly. The fact there is not even a dime collected on it is embarrassing to say the least. There is atleast one political party that is campaigning on policy to do this.

Agree. Which vote will acheive that...

Jenee

There's actually a very simple solution, if the will existed.

The government simply needs to start to build affordable housing en masse for first home buyers.

A mix of housing built and sold at cost, leasehold, rent to buy, and shared equity would enable almost every prospective FHB, of almost any income level (other than beneficiaries) to own a home. This would reduce the attractiveness of investment property, because the demand for rental property would drop.

Property prices might drop a bit, but not a lot. So best of all worlds.

Another big advantage would be forward certainty for the construction and related sectors, getting over the 'boom/bust' challenges of the sector.

The only real challenge, and it's a significant but not impossible one, is for the government to develop the capacity to do it. They could do it, though - especially if they got serious about investing in prefabrication plants.

To be honest, the taxation question is just a big distraction.

I think it's the government's lack of vision that's hindering this, nothing else.

A huge state housing program too expanding on what is already happening. Get rid of the slumlords altogether at the lower end of the market. Slum lords are not just at the lower end of the market either. Friend went to see a house For rent in the Eastern Suburbs/ $1250 per week. Advertising photo’s show a lovely house great for a family, large section, sea views. Upon inspection the garden and driveway full of weeds, ceilings peeling and damaged, the once cream kitchen sink was black, bathrooms rundown and the swimming pool a revolting shade of lime green! Time to take back New Zealand properties from overseas ownership.

They'd be putting a lot of housing developers out of business by selling at cost, though.

That's really what did Kiwibuild in, trying to have their cake and eat it by using housing developers who would sell at a profit, and not focusing on economies of scale in fabrication and production to bring costs down.

No, it's completely different to Kiwibuild. Completely.

Yes it would put a few developers out of business, but it's not like we are talking about thousands of people.

Downside is that small business is funded from housing equity. We have clearly seen during Covid that banks do not loan to small business directly.

Build as fast as you can approach will not keep pace with all the printed (and printing) money coming from Central banks around the world. The issue is clearly too much coin looking for a home with too little going into actual productivity investment creating real goods and services that employs people.... that is simple!

No, the govt should not build for buyers, it should build and retain ownership, and rent them out at affordable rents. Sort out the bottom end of the market and that will drag everything above it down. Investors can't compete with govt subsidised rentals and would stop competing with FHB to buy more rentals in that price range.

In my parents day, 30% of rentals was employer housing. One country I worked in (NE Asia) also has employer (subsidised) housing. NZ is so much of a good catch for foreign bosses - they have few costs compared to the countries they came from. It is all user pays in NZ. The end user that is.

That marginal effective tax rate bar graph is absolute nonsense. TOP party/TWG propaganda. https://pimms.nzpif.org.nz/UserFiles/files/NZPIF%20-%20TWG%20Paper%20Re…

Is the tax shown for owner-occupied housing council rates? This is a tax disadvantage incurred by land that other assets don't incur. Owner occupied housing earns no income, it shouldn't even be on the graph. Why don't they include recreational vehicles on the graph to show that they enjoy a massive tax advantage over other assets?

When's the last time you bought a vehicle, drove it for 10 years, and then sold it to someone for twice as much as you bought it for?

Please explain to me what tax advantage the family home has over other assets. If someone sells a classic car (or any other asset that wasn't purchased for profit) for more than they purchased it, they don't pay CGT.

Someone purchases a home for $400K and it increases in value to $600K over a few years. They want to sell for $600K and buy another similar home for $600K. You think they should be required to pay $66K for the privilege? People will just stop moving home (lock-in effect).

I have yet to see a CGT proposal where the primary residence isn't exempt.

With good reason. See my example above.

Solution is simple. Its called Roll Over Relief. Common in CGT rules in other tax jurisdictions. If you sell and buy within 3 months no CGT event. If you cash out then you pay CGT. The lock in effect does occur in Countries with heavy stamp duty as well. People add another floor on a house as no stamp duty. But Roll Over Relief will sort the issue you raise.

If you CGT the primary residence, then you need to allow deductions for expenses - mortgage interest primarily. This is how it works in the US. It doesn't raise that much.

I think for one thing what you intend to do with your money shouldn't be taken into account when deciding whether the money you have made ought to be taxable. That just seems to privilege those with assets over salary earners. I don't get to say 'I earned 200k over the last two years, and I want to spend it on a house, so I shouldn't have to pay any tax on my earnings'.

Someone purchases a home for $400K and it increases in value to $600K over a few years. They want to sell for $600K and buy another similar home for $600K. You think they should be required to pay $66K for the privilege? People will just stop moving home (lock-in effect).

Again, why should it matter what someone intends to do with their money? I want to buy a house. The money I earned through working is taxed. Note also that it wouldn't be such a problem for them if house prices weren't increasing at such an astonishing rate compared to the rate of inflation. Moving already costs money - you have to pay the real estate agent who sells your house, lawyers fees, etc. So someone who sells a house for 600k and buys a house for 600k will spend some extra cash for the privilege of doing so. This doesn't seem to stop people moving. They just factor that in to their decision.

If you think people would or should pay an extra $60k, $80k, $100+ just to relocate into the same standard of house you have a tenuous grasp on reality.

1. Whether they would is one question - but as I've noted, relocation has costs. People already do pay in order to relocate to the same standard of house. It's an open question how increases in those costs would affect people's behavior

2. Again, why should what people choose to do with their money affect whether or not it should be taxable? Should people pay tax on the money they earn if they want to spend it on a house? If not, then why shouldn't I get to declare that I want to spend my income from my job on a house and therefore I shouldn't have to pay tax?

3. The numbers you are throwing round keep going up - but the point of introducing a tax like this is to curb house price growth. If house prices rose at the rate of inflation, then your hypothetical couple wouldn't have to pay extra to move, because they wouldn't have earned anything. And income earners would be better off too, so win win.

If you push relocation costs up to this extent you will get lock-in effect. $15k estate agent commission will have some effect on how frequently people move, but CGT will be tens of thousands, potentially over $100k. This vastly higher expense will be a significant distortion that stops people selling. Are you denying this, or just saying that you don’t care?

You haven’t addressed my point about the graph. The tax advantage enjoyed by the family home in relation to other assets is.... What?

I'm saying that your numbers keep changing. There's no reason to assume a CGT will be over 100k. If we charged it on increases in value over and above inflation, it would potentially be nothing. And in fact part of the point of it would be to decrease house price growth, thus decreasing the amount paid. Of course it's a possibility that some people may not sell because of this, but how many is an open question. As you say, 15k in agents fees etc may stop some people moving. That fact isn't a good reason for the government to subsidize people's relocation costs, which is essentially what not taxing certain types of income is - a subsidy.

I haven't addressed your comment on the graph because I'm not that interested in the tax advantage the family home has compared to other assets (though one important thing to note is that the market in, say, classic cars doesn't have the ability to negatively affect so many people's lives in the way the housing market does).

What I'm interested in is this: why do you think that what people chose to spend their money on should impact whether or not it is taxable? If people get a tax break on money they earn by selling a house because they want to buy another house, why shouldn't I get a tax break on money I earn by actually working because I want to buy a house with it?

If you don’t understand how CGT on a property sale could be over $100k we are done here.

The CGT amount isn’t a fixed number, which is why I gave some example figures - it depends on how much the property value increased between when it was purchased and when it was sold.

I understand how it could be - but there's no reason to assume it would be. If, for example, we set a CGT at 10% and levied it only on increases over and above inflation, 100k bills would be a very rare occurrence- your house would have to increase by over a million dollars even taking into account inflation.

If you get to pull numbers out of the air, so do I - CGT could well be nothing, or could be 5k, or 10k. In which case there is no reason to worry.

And again: why do you think what you intend to spend your money on should affect whether or not it is taxable? If you think people shouldn't be taxed on money the earn from owning something because they want to buy a house with it, why should money I earn from working be taxed, when I want to buy a house with that?

I think one important mistake you (and others) are making is that you are vastly underestimating the costs of decreased and delayed home ownership. People wait longer to start a family because they don't have a stable living situation and so need IVF - taxpayers pay for that. People need to move away from their relatives and buy a smaller house to afford one - the elderly relatives need to go into care earlier than they otherwise might. Taxpayers subsidize that. Rentals on the whole are less healthy to live in - more hospital visits which taxpayers pay for. Fewer people have a home by retirement, so need the accommodation supplement. Kids move more often, fall behind in school, need reading recovery. Taxpayers pay again.

And that doesn't even cover the non-monetary costs of having fewer people connected to their community and committed to their neighborhoods.

Do you just not think any of this matters?

Sorry - double post.

Solution is simple. Its called Roll Over Relief. Common in CGT rules in other tax jurisdictions. If you sell and buy within 3 months no CGT event. If you cash out then you pay CGT. The lock in effect does occur in Countries with heavy stamp duty as well. People add another floor on a house as no stamp duty. But Roll Over Relief will sort the issue you raise.

Fine, but these people aren’t thinking rationally and won’t accept this as roll-over relief would exempt the family home from CGT in almost every case.

DD, can you stop accusing people of 'not thinking rationally' and 'having no grasp on reality' just because they disagree with you? I understand your position. I understand your worry. I just think that your worry is overblown and the benefits outweigh the costs.

You think the lock-in effect is fine, you don’t understand how CGT on a property sale could be over $100k, and you can’t specify what tax advantage the family home has over other assets. Not coming off as particularly rational.

I didn't say or imply any of those things. If you're going to accuse people of being irrational, at least do it on the basis of what they actually say.

As I have said, how bad the lock in effect would be is an open question (and depending on the extent of it, the benefits might outweigh the costs); I see how it could be over 100k, but there is no reason to assume it would be, or would be in the vast majority of cases; I haven't specified that because I'm not interested in specifying that.

I've asked you something a number of times now and you've repeatedly ignored it: why do you think that whether certain types of income should be taxable or not depending on what people choose to spend it on? It is very unfair to those who also want to spend their income on that thing (a house) but earn their income another way (by working).

I don’t think that “certain types of income should be taxable or not depending on what people choose to spend it on”. I think that if you are selling a house and then buying a house of the same value you have actually received no net income and therefore shouldn’t incur tax. Also, family homes do not enjoy a tax advantage. They actually incur a tax disadvantage in the form of council rates.

Well, you don't have any extra money cause you've spent it - that's not the same as no net income. If I earn a wage for mowing someone's lawn, and choose to spend all the money I earn before tax on paying someone else to mow my lawn, I dont get to argue that I shouldn't be taxed because I've actually received no net income.

Family homes certainly seem to enjoy tax advantages compared to salaries and wages - all of the income is taxed, but none of the money people make when they sell are family home is taxed. Do you not think that is an advantage?

I sell $500 of gold and then immediately buy it back again for $500. Final taxable profit of $500. Nice.

No, you sell some gold you bought for $400 for $500. Gross profit of $100. Whether you then choose to buy more gold, blow the money at the casino, or set the notes on fire for the pleasure of watching them burn is neither here nor there when it comes to assessing that profit.

Think about what you are saying - you are saying that whether money I make now on selling something counts as profit depends on what I choose to spend it on at some indeterminate time in the future. Do you realize how weird that would be if we applied it across the board? Everyone earning a wage or salary uses the profit they make from selling their labour to purchase products or services that are the products of other people's labour at some point in the future. Do you think they don't actually earn any net income either if they spend everything they earn at some point in the future?

Just google tax rollover relief - it is a thing for a reason

I understand what it is - but do you understand that it undermines your argument? It means you get to defer payment of the tax you owe on the profit that you made. It doesn't mean that you didn't actually make any profit because you spent all the money, as you seem to be arguing.

And whether there are good reasons for it being a thing in the case of houses is exactly what is at issue.

You earn the profit when you sell the asset, but then you eliminate this shortly thereafter by purchasing the same asset class for the same price. At the end of the transaction you have zero profit. You don’t just ignore the second half of the equation because you feel like it. Selling $500 of gold and then purchasing it back for $500 results in no profit in the end, regardless of how much you originally purchased the gold for.

This is just going round in circles. You do make a profit. What happens later on doesn't change the fact that you made a profit. It might mean you have zero money in your pocket, but this is not the same thing as not making a profit. Rollover relief acknowledges these facts - it acknowledges you made a profit, but means that in certain circumstances the tax you owe on the profit you made gets deferred.

Whether it is right or fair to have this kind of tax relief in some circumstances but not others is precisely what is in question. But you don't get to argue that the question doesn't even arise because you didn't actually make any profit. That's as silly as arguing that someone who spends all the money they earn by working on stuff that other people make by working shouldn't pay any income tax because at the end of the day they don't have any money in their pocket.

You make a profit when you sell something for more than you bought it, simple as that. Sometimes what you choose to spend it on affects whether you pay tax on that profit. Whether and when it should is the issue.

“It might mean you have zero money in your pocket, but this is not the same thing as not making a profit” Read this back to yourself slowly. Totally illogical and ignoring the second half of the equation just because you feel like it.

OK, perhaps you could explain what you mean by profit then. Because gross profit is the revenue minus the costs of the goods sold. Net profit is revenue minus the costs of the goods sold, as well as the operating expenses. You seem to be going by a different definition - that your profit is the same thing as the money you have in your pocket - that is, your profit is the same as your net assets. This us a very strange definition of profit! As I have pointed out numerous times, it means that if you (say) blow all the money you make at the casino (or on blow, for that matter) then we have to say you didn't actually make a profit, which I don't think the IRD is likely to accept. Do you really mean this, or do you have something else in mind?

People already do that with the real estate agency fees. In NE Asia where I lived, the purchase cost is a fixed amount, not a percentage. That there is far less speculation and price increases in normal suburban areas there could infer an advantage of that system.

So charitable donations should not be tax-exempt either ?

Its a rare day that i give DD an upvote. But he is right about the TWG effective real tax rate graph. A complete load of bunkum, based on a bunch of assumptions about inflation and leverage.

Pretty shocking that we agree on something, but I’m glad we do. I’ll return the upvote for good use of the word bunkum.

Easy to reverse though, RBNZ just needs to credit every New Zealander with freshly printed money and begin unwinding QE/ZIRP so normalising asset prices while creating controlled inflation. This is just a product of the tools RBNZ have chosen to fight deflation so far (OCR and LSAP.)

RBNZ just needs to credit every New Zealander with freshly printed money

That's not how it works or was ever intended.

It is actually quite hard not to feel bullish about the current housing market. If you have spare cash and the ability to obtain credit it just makes sense to invest in property, the safest, most protected asset class.

Exactly Apex Andy..... thereby pushing homeownership further and further away from younger New Zealanders! It just shows how totally Unsophisticated the average investor really is. It’s all anyone can think of to do! How on earth are we going to grow our country if the only business we can think of is buying a property.... How sad we have become.

Young New Zealanders don't seem to matter. All about the Boomers and the socially supported housing portfolios.

The more people who think like that, the more likely it is to crash. When Joe Average thinks they can’t lose on an investment the almost certainly will.

"Robertson’s steady as she goes approach aimed at providing certainty and thus confidence is a fair one."

Fair?...depends on your definition of fair I guess, but whether fair or not , it is pointless as the correction will come regardless and meantime we have squandered the ability to make better use of those billions that will be unavailable when that correction comes.

Because just about everyone of them has a rental or two..

Policy announcement 1: Accommodation Supplement is scrapped. 4 billion more in to pay down debt. Rents will fall as tenants wont have the money. Policy announcement 2: All gains on houses, farms and shares are subject to CGT. Rollover relief if sale is going into another property. CPI indexing so not taxing inflation.

Shares are already subjec to CGT. They just don't call it that not upset the average Kiwi who is against CGT

Share are not subject to CGT. NZ Shares Gains are only taxed if you acquired them with the purpose of resale for a gain (so a trader) but if for long term hold for dividend flow you not taxed on capital gains. Just like house gains nobody pays tax on NZ share gain. Offshore investments in shares over 50K are subject to the purely evil FIF tax regime that is a made up tax fiction to rob kiwisavers that only exists in NZ similar to our former give way to cars turning right rule for many years!

Orr / RBNZ and Robertson / Treasury are practicing defacto MMT and inflating asset prices. Orr is pushing for more and more spending and underwriting it with zero or negative interest rates. There is no plan how the debt can be paid back.

"There is no plan how the debt can be paid back." - It's easy! We'll sell those assets for double the price 7 years from now!

This is as interesting article which suggest that NZ can't practice MMT as our external deficits are too high. https://www.manulifeim.com/institutional/global/en/viewpoints/market-ou…

"The financial system relies on house price growth" Everyone relax. This will all be totally fine.

yup, we robbed both Peter and Paul to pay Judas

Spot on.

It's good to see in print that no major political party is going anywhere near taxing housing as its akin to taking a knife to the throat of the economy.

What a mess.

Avoid Mess. Vote for Green party

https://www.newshub.co.nz/home/politics/2020/09/nz-election-2020-grant-…

Note Labour have ruled out any more “income” taxes. Still room for a land tax

Will not happen

I would love to be surprised here, but I think that's clearly not the direction Labour is headed. People need to wake up to this and stop holding out hope that they will do anything to properly address the mess we're in, and start recognizing that they, just like National, are a huge part of the problem.

Exactly and that's why I will vote Green. It would be great if Greens could get to 7-8% to pull Labour in the right (left) direction.

Absolutely agree. I hope that this latest move by Labour is a wake up call for many, that will push the Green vote higher than expected. The kind of centrist hell we'll be in otherwise...

Those on Labour's left need to wake up and seriously think of a vote for Greens.

Greens are FAR from perfect, but they are far closer to what this country needs than any other party.

Yes, exactly. I have no illusions about them either, but they are definitely the closest to what we need right now.

And they are prepared to begin to address the issue of the inability for their to be infinite growth in a finite world, something no other political party that I know of, is prepared to, it is all grow, grow, grow for them, including Labour

Good point. Everything else that seems so important now, means nothing if we keep ignoring the insanity of continuing on as if infinite growth is possible.

If you’re trying to diffuse a bomb don’t cut the wrong wire...

"A government led by this Labour Party is not that government."

Therefore, let's vote them out and bring a party that has common sense policies and willing to fight for kiwis.

I think TOP is that party.

Wasted vote. They will never get 5% or an electorate seat. Vote ACT.

They think they have a chance in Ohirau, we'll see in a few short weeks. (I doubt it personally)

I may weep if they get in. Only half joking.

ACT and TOP aren't comparable, ACT isn't in favour a a universal basic income.

Even if TOP don't get a seat, they might get more funding as that is determined from the percentage of the popular vote of the previous election. Maybe even a spot on the televised debates. Changing an entrenched political system is unfortunately a long game, barring a revolution.

I’d say they are polar opposites. TOP is very close to the Greens. I think they will de-register (again) after this election.

TOP are the choice for those that want to modernisation/ adapt to the current era and drive real economic growth without destroying the biosphere or increasing poverty and crime. It's disappointing to see how misunderstood they are.

TOP is the choice for those who produce meaningless yet "nice" soundbites - like you just did.

Extend the bright-line test to ten years. That'll do for starters. Delete 'five' and insert 'ten'. How hard is that? Easy win.

NZ will be crashed by the OZ equation. IF OZ crashes by 20% or more, anyone who is an NZ citizen will have to decide whether or not to work in a low wage economy with poor housing quality or go to OZ where the quality of housing is better and cheaper than NZ. A lot of these citizens have no long term roots in NZ.. and being able to buy a better house in a larger economy at half the price will be a big factor when things open up.

Education is the answer, and a very carefully tailored tax. Educate young people on how to get on the property ladder and the benefits of house ownership vs renting. Higher levels of education/good employment in young women is also linked to reduction in number of children they have (crisis: mum + her 7 children are homeless, dads gone AWOL, they must be given a big house in Auckland, now). Taking the edge off population growth would reduce housing shortages and help reduce house price growth...and a few other problems we have (Climate change..) People owning a rental property is a good thing, often hard working types who just want to get ahead, but it should be easy to tailor tax to be kind to them but hit those who make excess wealth quickly and get even richer when crisis such as COVID hit (e.g capitial gains tax if you own more than 3 properties,or land tax if you own more than 3, or capital gains tax any gains that total >$500K over 5 yrs. Inheritance tax if you inherit >$400K with ten yrs (there are people who are inheriting farms worth 10M split between 2 kids, all tax free) Need to tax the excessive top end wealth creation, and get as many people into home ownership as possible, then increasing house prices (which seem here to stay) might be less steep and not be so unfair

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.