This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

1) Should we be worrying about inflation?

Inflation has been a major focus this week. Locally we had the latest quarterly survey of business opinion from the New Zealand Institute of Economic Research saying businesses are finding it easier to pass their higher costs through to price rises for customers. And in its Official Cash Rate review we had the Reserve Bank pointing to global supply chain disruptions and higher oil prices creating price pressures.

From the US we had news that consumer prices rose by the most in more than eight and a half years in March with both the headline and core inflation measures higher than forecast. The annual figure came in at 2.6%, which was ahead of the forecast of 2.5% and up from 1.7% in February.

And from The New York Times we have a report that the Biden Administration is "quietly keeping tabs on inflation." This, of course, is against the backdrop of the President's multi-trillion dollar economic stimulus package and infrastructure spending plans. Biden’s advisers believe any price spike is likely to be temporary and not harmful. Basically a one-off event caused by a pandemic recession that ruptured supply chains and depressed activity in the likes of restaurant dining and tourism.

Armed with their internal data and conclusions, administration officials have begun to push back on warnings that a stimulus-fueled surge in consumer spending could revive a 1970s-style escalation in wages and prices that could cripple the economy in the years to come.

Yet they remain wary of the inflation threat and have devised the next wave of Mr. Biden’s spending plans, a $2.3 trillion infrastructure package, to dispense money gradually enough not to stoke further price increases right away. Administration officials also continue to check on real-time measures of prices across the economy, multiple times a day.

The article goes on to note it has been some time since there was any real concern about inflation. Indeed, in recent years we've probably heard more about deflation.

Economic teams in recent administrations spent little time worrying about inflation, because inflationary pressures have been tame for decades. It has fallen short of the Fed’s average target of 2 percent for 10 of the last 12 years, topping out at 2.5 percent in the midst of the longest economic expansion in history.

But Biden's team sound wary.

Mr. Biden’s aides are sufficiently worried about the risk of that spending fueling inflation that they shaped his infrastructure proposal, which has yet to be taken up by Congress, to funnel out $2.3 trillion over eight years, which is slower than traditional stimulus.

Bloomberg's Odd Lots podcast, co-hosted by two excellent financial journalists in Joe Weisenthal and Tracy Alloway, is often an interesting listen. Their latest episode features an interview with Zach Carter. Carter's the author of a very good book on economist John Maynard Keynes. In the podcast Carter talks about what caused the hyperinflation in Weimar Germany, an issue that features in his book. Now that was inflation...

Below is the blurb accompanying the podcast.

Whenever the government is engaging in fiscal or monetary expansion, people like to invoke the history of Weimar Germany and how soon we might all go around transporting dollars in wheelbarrows. But what really happened with Weimar and how did it come about? On this episode, we speak with Zach Carter, the author of the best-selling book “The Price of Peace: Money, Democracy, and the Life of John Maynard Keynes.” He explains how the story of collapse of the German currency was less about money printing and more about domestic political collapse and the destruction of the country's productive base.

2) Why Richard Prebble could look in the mirror rather than blame Social Credit for the RBNZ's quantitative easing.

Richard Prebble, a Rogergnome from the 1980s Labour government who subsequently became leader of the ACT Party, has written an article typically laced with bluster and hyperbole for the NZ Herald. In it he labels the Reserve Bank's bond buying, or quantitative easing (QE), social credit and puts the boot into the Social Credit political party, which received just 1,520 votes, or 0.1%, of the total votes in the 2020 election, and has never been in government.

Today the Reserve Bank has a programme to create $100 billion to lend to the Government at near-zero interest via the secondary market so they can pretend it is not social credit.

He's referring to the Reserve Bank's Large Scale Asset Purchase Programme, although you could almost be forgiven for not realising that. Through this the central bank is buying government bonds and local government bonds in the secondary market off the banks listed here. Treasury's 2020 Pre-Election Economic and Fiscal Update forecast the Government, effectively buying back its own debt at a premium from banks, would cost $11.1 billion over three years.

The official aim of the programme is to lower borrowing costs to households and businesses by injecting money into the economy through bank intermediaries. The Reserve Bank is currently planning to spend up to $100 billion buying these bonds with new money by June 2022. Starting in March last year, so far it has got to just over $51 billion.

Below is a QE explanation from the Reserve Bank.

When we buy assets, this increases their price and so reduces their yield. That means the interest rate, in this case on government bonds, fall. This has the effect of ‘lowering the tide’ on other interest rates in the economy, particularly longer-term interest rates of two years or more. It also reduces the cost of borrowing for households and businesses.

Secondly, when we buy these government bonds, it encourages the sellers of assets to use the money they receive from us to switch into other financial assets like company shares, bonds, or new lending – helping to inject money into the economy.

This explanation aligns QE with trickle-down economics, through which tax breaks and benefits for big corporates and the wealthy are expected to trickle down to everyone else. And as with the trickle-down economics theory, after more than a decade of experience with QE in the likes of the US and UK, there are plenty of questions over whether its biggest achievement is actually helping widen wealth and income inequality between asset owners and non-asset owners.

QE is being implemented by our independent, inflation targeting central bank, set up as such by the Government Prebble was a part of in the 1980s. So Richard, it'd make more sense for you to look in the mirror than blame Social Credit for QE. It's part of your legacy. QE has become an orthodox response from inflation targeting central banks once interest rates hit the zero-bound.

Meanwhile Social Credit leader Chris Leitch, like Prebble, worries about the impact QE is having on house prices. In an article submitted to interest.co.nz last year Leitch advocated for monetary financing, not QE. That is the Reserve Bank giving money directly to the government, and "letting the government spend it into the economy on building infrastructure, providing more resources for hospitals, loans to small businesses, or funding state house building."

Treasury and the Reserve Bank even prepared a paper for Finance Minister Grant Robertson last year comparing QE and monetary financing. The Government has not, however, gone down the monetary financing route.

Egypt has reportedly impounded the Ever Given, the container ship that was stuck in the Suez Canal in March. An Egyptian court has ordered the vessel’s owner to pay nearly $1B in compensation before releasing the ship. There are reportedly 25 Indian crew members on board pic.twitter.com/TBqrkVMHuW

— NowThis (@nowthisnews) April 15, 2021

3) Court action gets curiouser and curiouser as borrowers take on their bank.

This fascinating and bizarre case, that made its way to the Supreme Court, was brought by husband and wife duo Qiufen Lu and Liansen Mao against ICBC NZ Ltd. Readers with long memories might recall them as associates of infamous property manager/developer, Augustine Lau from this story and this one in 2017.

The Supreme Court judgment, released on Thursday, sets the scene.

The first applicant, Ms Lu, a Chinese citizen and resident, borrowed approximately $2.9 million from the first respondent (the Bank) to assist with the purchase of a $6 million property in Auckland. She intended to subdivide the property, but after various defaults on her obligations, the property was sold by the Bank in a mortgagee sale. The Bank then commenced proceedings in China to recover the shortfall owing under the loan agreement. The proceedings in China involved a claim not only against Ms Lu but also against the second applicant, Mr Mao, who is Ms Lu’s husband. The claim against Mr Mao arises because, under Chinese law, a spouse can be jointly liable with the actual debtor for certain debts. The Bank also obtained freezing orders against the assets of Ms Lu and Mr Mao in China.

The freezing orders in respect of Mr Mao’s bank accounts and securities and Ms Lu’s bank accounts were subsequently discharged. Only a freezing order over Ms Lu’s securities remains.

Ms Lu applied in China to have the China proceedings stayed on the basis that New Zealand is the proper forum for the resolution of the Bank’s claim. That application failed. An appeal is yet to be determined.

Lu also sued ICBC in the High Court, making a range of allegations detailed in the judgment. ICBC succeeded in having her claim struck out and was awarded costs of $20,000. Lu then sought to file further proceedings in the High Court with two proceedings struck out and one not accepted for filing. Lu and Mao also filed a notice of appeal in the High Court against the High Court strike-out judgment.

They were advised that they had filed this in the wrong Court, and eventually filed a similar notice of appeal in the Court of Appeal on 5 August 2020, approximately five months out of time. They sought an extension of time to appeal.

The Court of Appeal dismissed the application for an extension of time... In particular, it took the view that the proposed appeal against the High Court strike-out judgment could fairly be described as “clearly hopeless”.

The applicants also applied to stay enforcement of both the High Court strike-out judgment and the High Court costs judgment. Their application was dismissed.

The Supreme Court comes in with Lu and Mao seeking leave to appeal against the decision of the Court of Appeal refusing to extend time to appeal to that Court. They also sought leave to appeal directly to the Supreme Court against the High Court strike-out judgment and the High Court costs judgment.

In relation to the Court of Appeal judgment, the applicants say that it is a matter of public interest for customers of Chinese banks to know that the law of China may be applied to enforce loans from New Zealand in China. We do not see that point as arising in the proposed application. The Court of Appeal judgment involved an orthodox application of this Court’s decision in Almond v Read to an application to extend time to appeal to the Court of Appeal. No point of general or public importance arises and there is no appearance of any miscarriage of justice. The grounds for leave to appeal are not therefore made out and we decline the application for leave in relation to the Court of Appeal judgment.

The application for leave to appeal against the High Court strike-out judgment, and the High Court costs judgment, were dismissed. And the Supreme Court ordered Lu and Mao to pay ICBC costs of another $2,500.

Data from 2 April 2021 shows that only $219m of residential mortgage loans remained on deferral. This is down from a peak of $22.2bn of loans on deferral at 29 May 2020. The stock value data is available from 22 May 2020. More here https://t.co/gIbe5aPItc #rbnz pic.twitter.com/DxeJMCuctt

— Reserve Bank of NZ (@ReserveBankofNZ) April 15, 2021

4) Another way to look at Biden's infrastructure plan.

Writing for The Atlantic, Robinson Meyer argues President Biden's US$2 billion infrastructure plan is the one opportunity to pass meaningful climate change legislation in the US over the next few years.

Since climate change became a political issue in 1988, Democratic presidents have had a single window early in their first term to pass a climate bill. Bill Clinton’s came in 1993, when he tried to levy a tax on certain types of energy; Barack Obama’s arrived in 2010, when he supported a more ambitious carbon-pricing bill. In both cases, the climate bill passed the House, then died in the Senate. The United States continued to muddle through without much of a plan. Most climate policy came through either puny tax credits or the president’s power to spend foreign aid.

The upshot is that the United States, the largest historical contributor to climate change, has limped for the past few decades with no serious climate policy.

But this bill hurls several different and mostly sensible tools at the climate problem. Its marquee policy is probably its clean-energy standard for the electricity sector, which aims to zero out carbon emissions from power generation by 2035. But nearly as important is its extension of certain key green-energy tax credits; it also converts these into direct payouts from the IRS, which should make them simpler, cheaper, and more equitable to implement. Also significant are the plan’s fledgling attempts at industrial policy—it aims to set up 10 “pioneer facilities” that will show how large steel, chemical, and cement makers can decarbonize through carbon capture and storage technology.

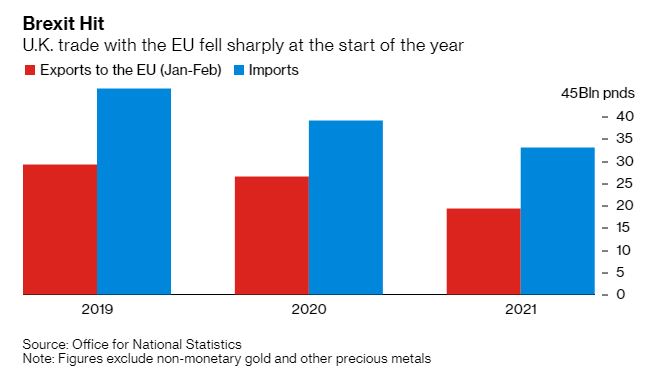

5) Red tape increases for UK firms after Brexit.

Now that the UK has Brexited, how's it working out for the country's businesses?

Not great according to this Bloomberg article.

Customs checks, paperwork and border delays since the U.K. completed its withdrawal from the European Union at the start of the year are sucking cash and time out of firms from big-name retailers to small family-owned businesses. Companies, which warned for years that this would happen, take no pleasure in saying “we told you so,” but the frustration is clear as they grapple with the long-term reality.

For many businesses on tight margins, every pound spent on documentation means less for wages, hiring and investment. While the impact will be far less dramatic than the short-term shock of the Covid-19 lockdowns, over time it will add up, hobbling the economy and eating into sales, earnings and incomes.

Certainly the initial go-it-alone period hasn't been easy.

The story of unwanted hassle is one repeated across the U.K. One in four small exporters have halted sales to the bloc because of red tape, and a survey on Monday showed more than 40% of businesses had lower export revenue in the first quarter. In January and February, total goods exports were down 27% compared with a year earlier, and imports also declined.

UK government promises of its own free trade deals with other countries are being closely watched.

With so much at stake, a group of lawmakers and businesspeople has set up the independent Trade and Business Commission to review trade deals and figure out how the U.K. can best benefit. It will start hearings this week on Brexit’s impact and whether the effects “will be compensated for by greater trade with the rest of the world,” such as the still-distant U.S. accord.

66 Comments

RE:1) Should we be worrying about inflation?

From another thread: The UST 10yr yield is down a sharp -10 bps at 1.55% and its lowest in more than a month.

To put it into 2017 terms, the curves/global markets are pricing the chances of something going wrong to be much, much higher than everything going right. Sour, not soar. That’s how despite vaccines, Uncle Sam, TGA, bank reserves, etc. etc., global bonds have moved so comparatively little, thoroughly unimpressed no matter how many thirteen-digit programs applauded even feared (inflation-wise) in all the mainstream.Link

'QE is being implemented by our independent, inflation targeting central bank, set up as such by the Government Prebble was a part of in the 1980s. So Richard, it'd make more sense for you to look in the mirror than blame Social Credit for QE. It's part of your legacy.'

- Establishing Reseve Bank independence is part of the legacy of Sir Roger Douglas, who was worried about the Reserve Bank having to endure again the kind of direct political interference that occurred during the Muldoon era. Blaming every member of a government in 1989 for the actions of a central bank in 2021 is drawing a pretty long bow, IMO.

Prebble has also not blamed 'Social Credit' for QE. He has said that QE is tantamount to Social Credit. There has been a comprehension fail by Gareth Vaughan.

Richard Prebble is being subjected to a lot of ad hominem attacks of late, by sheep who are angry that someone has the gumption to sing from a different song sheet.

'QE has become an orthodox response from inflation targeting central banks once interest rates hit the zero-bound.'

- So the central bank pulls the lever on interest rates all the way down to zero, and then that triggers them to initiate QE. It's like me putting a gun to my own head and then commanding myself to take some drastic action otherwise I'll pull the trigger. QE has absolutely nothing to do with inflation targeting, and everything to do with propping up the artificially created asset bubbles that central banks have brought into being.

Financial journalists and economists should have been questioning unorthodox monetary actions from the get-go, rather than glibbly allowing them to be bedded in as orthodox responses. The have failed us in the same way that the ratings agencies failed us prior to the GFC.

FYI Tom, it's Vaughan, not Vaughn.

Prebble has a lot to answer for - and Tom Valn is correct in saying the media - particularly the financial media - have, too.

Sometimes they pay lip-service but bury, reminds me of Douglas Adams:

“But the plans were on display…”

“On display? I eventually had to go down to the cellar to find them.”

“That’s the display department.”

“With a flashlight.”

“Ah, well, the lights had probably gone.”

“So had the stairs.”

“But look, you found the notice, didn’t you?”

“Yes,” said Arthur, “yes I did. It was on display in the bottom of a locked filing cabinet stuck in a disused lavatory with a sign on the door saying ‘Beware of the Leopard.”

Touche

"Dont panic"

Sharon Zollner on breakfast TV months ago: "The consensus is now that you can print money without any inflationary consequences".

.....months later, inflationary pressures start to mount.

The trouble with economists and central bankers is that they are increasingly focussed only on the short term. And they use a ridiculously small sample size to come to far-reaching conclusions. Events play out in full over years, not weeks or months.

Pull back the curtain, and you'll find central banks have no real control of consequences - their goal is to try to keep spinning the plates they've set in motion.

Tom you come across as an idealogue while the RBNZ has to operate in the real world, you also fail to acknowledge just how difficult a job they have. As a small open trading economy we are largely importers of monetary policy from our much larger trading partners. Not to have implemented QE would have seen our TWI on all time highs, crushing exports during a period of unprecedented economic crisis. They are never going to get MP correct all the time, simply impossible. The RBNZ have not gotten anywhere close to the stimulus of the ECB, BoJ, Fed for example who have all expanded balance sheets to a much larger extent and into credit, equity and mortgages. Criticise QE by all means, but the RBNZ were left with very little choice

So to put it simply, the decision was made to crush the value of work instead? Probably because only the assetless would fell the burn.

Te Kooti, I will continue to criticize the unelected central bankers and their enablers. When you are going down the wrong road, every opportunity you miss to change course is leading to an even worse eventual outcome. It is the economists and financial journalists that have failed to correctly inform the wider populace, meaning that ignorance of the true situation is widespread. What we do in NZ has mirrored what has happened around the world, I accept that: we have a worldwide problem of widespread apathy and inabilility to learn from past errors. Unconventional monetary policy is still a giant experiment, which is currently producing disastrous outcomes. If we accept that doubling down on failure is the way forward and treat unconventional policies adopted since 2008 (the blink of an eye in historical terms) as the 'concensus' on correct conduct of monetary policy, then we are behaving in a profoundly unintellectual way.

. The RBNZ have not gotten anywhere close to the stimulus of the ECB, BoJ, Fed for example who have all expanded balance sheets to a much larger extent and into credit, equity and mortgages. >

Not correct. Despite all the money printing and QE by the BoJ, h'holds and firms have been paying down debt. In the United States, base money is approx $5.3 trillion, while broad money is $19.5 trillion. Broad money is about 3.7x as much as base money. In Japan, base money is ¥620 trillion, while broad money is ¥1,140 trillion, so broad money is about 1.8x as much as base money.

I would use GDP and not base money, The ECB currently hold securities equivalent to 65% of GDP while RBNZ is around 18% of GDP. You are wrong on the others as well, but don't let that stop you.

Te Kooti,

I agree that without QE, and all other things being equal, then the TWI may well have soared. But the TWI may not have soared as long as the OCR stayed low. And there are other mechanisms the RB can use to discourage speculative inflows such as requiring the banks to source minimum proportions of its capital from onshore.

KeithW

Keith the OCR was already low entering into Covid. Recall for most of 2020 the RBNZ was actively prepping local banks for negative rates, in part to keep the currency low. My point is we are largely hostage to the actions of our much larger trading partners, if we didn't adopt QE it's almost certain we would have experienced a catastrophic external revaluation in the manner of Switzerland who had to adopt the peg and which created massive distortions.

Te Kooti

The Swiss situation is very specific. They removed the peg to the euro in 2015, Having a peg meant they had a fixed exchange rate prior to this and this had created a major distortion. That is what fixed exchange rates do! This is a very different situation to what we currently have in NZ.

KeithW

Vaughan - is this your best / only response to his very accurate criticism of your article ?

He's entitled to his opinion. I don't agree with much of it but I've already had my say. Just get a bit frustrated with names being misspelt. For example, we still regularly have commenters who write John Keys instead of John Key, or Helen Clarke instead of Helen Clark.

I've amended your name and apologise. It's just one of these things where I've made a typo, and then that has become the entire focus rather than anything else I might have stated in my post. Unfortunate really. PDK has done the same thing, referring to my handle as 'Tom Valn' above. As to my real name, it is near constantly misspelled in e-mail correspondence: just seems to be one of those names that people struggle with for some reason.

I did it to make a point......

:)

Agree. More importance should be on content and not on typo.

Coincidentally the YouTube channel"Economic explained" did a video on hyperinflation as well this week. Everyone is talking about it!

https://youtu.be/1HmGLV46L60

My understand is that inflation won't really become a widespread issue, although US retail sales and unemployment today looked white hot economists note there is still enough slack to allow this to continue for a short period.

At least they have tools to actually stay in touch with the data

Administration officials also continue to check on real-time measures of prices across the economy, multiple times a day.

While we appear to still be looking back 6 months and "thinking about it"

Particularly since 2007/8, economists have been blindsided. The parameters they worked within (and it was 'within', all else was 'externalities' to them) sort-of fitted the planetary growth-capability for the last 200 years. Since WW2, then increasingly this last decade, that capability has been lacking.

They were also working with/from a flawed societal narrative; they were part of the front-end-of-the-First-World echelon who were increasingly living at the expense of others, while telling themselves a more comforting story. One of the ways of perpetuating that 'fudge', was via an obsessive insistence on valuing everything in 'money' - now looking ever-more stupid as the amount of keystroke-issued debt goes from unrealistic to downright ridiculous.

Whether we find far too much proxy bidding for far too little in the way of remaining planet, or lose belief in debt, or collapse? is an interesting global question. Further down the chain, which nation blinks/collapses first? is another. Further down again, inflation or deflation or stagflation?

And the get-out-of-political-jail card waiting in the wings; direct the anger at a 'them', then go to war with 'them'. Great way to keep local control and nothing to lose in terms of who-gets-what's-left.

3) I'm really surprised they can be pursued for debts in China. I thought Chinese people could basically just do whatever they want here and bugger off back to China and escape any prosecution.

But I guess it's a Chinese bank so that probably helps a lot.

Richard Yan - Mainzeal - he buggered off owing $38 million - nicely ensconced in China with all the loot

The ICBC NZ Ltd should buy the debt off Mainzeal Liquidators for cents in the $ and go after Yan in China

Up the Yan-see river?

There are so many errors in Richard Prebbles article that it is hard to know where to start. He describes QE as the Reserve Bank creating money for the government to spend which is incorrect as that is not what happens. QE in reality does not create any new money, it only returns money to bond holders, money is created when the government spends it and the Reserve Banks balance sheet is part of the governments balance sheet anyway.

He seems to be totally unaware that it is the banks themselves which are creating the money for lending on housing and he puts the increasing house prices down to the money from QE.

So you are saying that Reserve Bank actions, in buying new government bonds with newly created 'reserves', is not increasing the money supply, even temporarily? (In reality, the money supply increase is never temporary as the Federal Reserve has found that it cannot unwind its balance sheet without causing asset prices to tank. QE proceeds are always 'reinvested').

You can play with semantics all you like, but fresh money is created and - via bond purchase - it is made available to the government to spend .

'Quantitative Eeasing increases the money supply by purchasing assets with newly-created bank reserves in order to provide banks with more liquidity.'

https://www.investopedia.com/terms/q/quantitative-easing.asp#:~:text=Qu….

Excellent comment Tom.

Central banks purchase already monetised government debt from banks when executing QE operations. And yes central bank balance sheets have expanded on both the liability and asset side. But banks are still where they were before the operation - that is an owner of a government liability, but in another form - a floating rate income asset, rather than a fixed rate income asset. No balance sheet expansion in the public arena.

A recent Bloomberg article described central bank easing with the phrase “pumping money into the economy.” That’s a misconception. Monetary easing is actually an asset swap. The public was holding savings in one form, and now it holds it in another. The Fed buys Treasury securities from the public, and replaces them with currency and bank reserves (base money) that someone has to hold, at every point in time, until the Fed sells its bonds and retires the cash. All monetary policy does is to change the mix of government obligations held by the public. Only fiscal policy – specifically deficit spending – changes the total amount of those obligations.Link

The money supply grows when banks purchase new loan contracts from the public and in the process credit the borrower's account with bank IOUs masquerading as new deposits.

The reality that the amount of new public loan contract purchases, undertaken by banks, are not wide spread in the US is reflected by negative real interest rate yields for 5 year and 10 year tenor Treasury Inflation Protected (TIPS) securities. Nothing good arises from negative real interest rates in terms of economic well being.

The majority are being denied access to bank credit creation facilities due to inadequate credit ratings and collateral ownership - graphic evidence.

{kind=link}

Thus around 60% of NZ bank lending is dedicated to residential property mortgages held by one third of already wealthy households because the RBNZ offers them an RWA capital reduction incentive, to do so..

Bank lending to housing rose from $50,788 million (48.36% of total lending) as of Jun 1998 to $301,450 million (60.46%) of total lending) as of February 2021.

Due to QE & FLP NZ banks could end up owning government and RMBS assets greater than outstanding business loan assets, which have already contracted 4.1% to date - source.

So why do they (central banks) do it? (QE)? is it not to encourage private banks to continue lending and creating credit and prevent a credit crunch? So in effect they stimulate money supply, regardless of who actually ends up creating the money (whether it is the central bank or the private banks). If otherwise, is this a totally pointless excercise by the central banks that does not achieve any objectives?

So why do they (central banks) do it? (QE)?

“MR. HENSARLING. And so I am trying to figure out, what is it that--on the Federal Reserve menu, what would two more Operation Twists and two more QEs, even if you supersized them, achieved that haven't already been achieved?”

That’s what science is; you try something and if it doesn’t produce the desired results you know it didn’t work. You stop doing it. In terms of QE, a third go-round would’ve at least proved it couldn’t have been “quantitative.”

Bank reserves at any level, Bernanke replied, “are not the issue.”

“CHAIRMAN BERNANKE. The issue is the state of financial conditions. And we are still able to lower interest rates, improve, broadly speaking, asset prices, and that provides some [stimulus] incentive.”

In the textbook everyone uses, lower is always better where interest rates are concerned. It is the central basis by which all of this madness continues. We hear it over and over, the lie repeated ceaselessly by officials and then regurgitated by the financial media which betrays the decency of its audience swallowing it and repackaging it for them wholesale. Link

This is what Milton Friedman called the interest rate fallacy, and it indeed refuses to die. We can tell what monetary conditions are in the real economy, as opposed to financial liquidity, though the two can be linked, by the general level of interest rates. When money is plentiful, interest rates will be high not low; and when money is restricted, interest rates will be low not high. The reason is as Wicksell described more than a century ago:

[The natural rate] is never high or low in itself, but only in relation to the profit which people can make with the money in their hands, and this, of course, varies. In good times, when trade is brisk, the rate of profit is high, and, what is of great consequence, is generally expected to remain high; in periods of depression it is low, and expected to remain low.

When nominal profits are expected to be robust, holders of money must be compensated for lending it out by higher interest rates. Thus, the same holds for inflationary circumstances, where nominal profits follow the rate of consumer prices. During the Great Inflation, interest rates weren’t low at all, they were through the roof well into double digits and higher by 1980. At the opposite end in the Great Depression, interest rates were low and stayed there because, as Wicksell wrote, the rate of profit was low and was expected to be low well into the future. High quality borrowers were given as much money as they could want while the rest of the economy was deprived of funds; liquidity and safety being the only preferences in what sounds entirely familiar. Link

{kind=link}

QE is a monetary tool that allows The Reserve Bank to set interest rates. It exchanges government bonds for commercial bank reserves and reduces the cost of their funding, but banks do not lend these reserves out. Bonds are bought and sold constantly by the RB depending on whether it wants interest rates to rise or fall. All NZ Dollars are held at the Reserve Bank either as reserves or as bonds, they are only in different accounts. Both of these forms of money are the property of the private sector and they make up our savings which are created through the governments deficit spending.

Some further explanation here, https://www.economicsjunkie.com/sectoral-balances-and-private-saving/

QE keeps bond yields low by Central banks bidding up market price for the fixed rate coupon assets.

This in turn serves two purposes (1) treasury bills remain low yield which in turn impact rates of other assets as they are the ‘risk free benchmark’ (e.g. LIBOR) (2) the large banks have guaranteed market buyer that will pay what ever it takes to maintain low yields... they make easy money selling down tranches of their holdings at a profit

Sorry, but this is so back to front it is almost insane.

Govt adds money to the economy *when it spends it*. So, Govt spends $500m to pay for wages during Covid - thus $500m is added to the money supply. Most of this money (eventually) accumulates in bank reserves. Sometimes the money in bank reserves is swapped for interest-bearing notes (aka bonds). These bond 'purchases' are neutral - just an asset swap for the bank (or a liability swap for the Govt).

QE doesn't create extra money for the government to spend, it swaps bonds for cash. Unlike the eminently sensible overt monetary financing by the Reserve Bank of the government's fiscal policy measures.

Should be usedfor our massive infrastructure catch-up.

'he puts the increasing house prices down to the money from QE.'

---------

'To execute quantitative easing, central banks increase the supply of money by buying government bonds and other securities. Increasing the supply of money lowers the cost of money—the same effect as increasing the supply of any other asset in the market. A lower cost of money leads to lower interest rates. When interest rates are lower, banks can lend with easier terms.'

And how do they (hope to) "increase the supply of money"?....therein lies the misunderstanding. The money supply is increased by the private banks credit creation IF enough think it is beneficial to borrow...lower interest rates are expected to encourage that borrowing as is the 'wealth effect' of RE inflation.

It is a confidence trick (in every meaning of the phrase)....no money is 'printed' and any 'money' created is done so by the banks at our behest.

It is all borrowed money that has to be serviced by underlying economic activity....and that aint expanding....and the banks will want to be repaid, one way or another..

We are issuing credit cards to pay maxed out credit cards.

The misunderstanding is yours and yours alone. Banks create money via fractional reserve banking, which involves banks accepting deposits from customers and making loans to borrowers while holding in reserve an amount equal to only a fraction of the bank's deposit liabilities.

But -

Central Banks also create money to buy bonds to lower interest rate costs!!

Goodness me.

Don't take it from me: just read and comprehend the information that is freely available elsewhere:

https://www.investopedia.com/terms/q/quantitative-easing.asp#:~:text=Qu….

'Quantitative easing (QE) is a form of unconventional monetary policy in which a central bank purchases longer-term securities from the open market in order to *increase the money supply* and encourage lending and investment. Buying these securities *adds new money* to the economy, and also serves to lower interest rates by bidding up fixed-income securities. It also expands the central bank's balance sheet.'

Section 10

https://www.rbnz.govt.nz/-/media/ReserveBank/Files/OIAs/2019/Response-t….

Happy to have been of assistance.

Oh dear, you have directed me to the section regarding 'fractional-reserve banking'. Perhaps you are confusing the process of 'reserving' a fraction of deposits (Fractional-reserve banking) with the name of the central bank (Reserve Bank of New Zealand).

You fail to see that we are discussing 2 different ways in which money is effectively created. You have a total blind spot as regards QE.

"The Reserve Bank of New Zealand requires banks to maintain a specified minimum level of

the owners’ capital invested in the business, on their own balance sheet. The amount of

shareholder capital that banks are required to keep on their own balance sheet varies between

different banks, depending upon their circumstances. We do not require banks to keep a

reserve deposited at an account with the Reserve Bank.

The Reserve Bank exerts control over the money supply by setting an interest rate called the

Official Cash Rate. The Reserve Bank will lend unlimited amounts of money overnight to any

bank that has an exchange settlement account with us, at a small premium to the prevailing

official cash rate; and if a bank deposits money into their exchange settlement account with us

we will pay interest on the balance, at a small discount to the Official Cash Rate. This

influences the price of short-term lending and borrowing (i.e. interest rates on short term

loans), which will always remain close to the Official Cash Rate. By influencing the short-term

interest rate, we influence the demand for loans and incentives to save via bank deposits, and

thereby the rate at which new money is created – i.e. new money supply. "

It pays to read beyond the headlines

Frank, nowhere in that speil does it cover off QE!! If I wrote you an essay about trees would it mean that lions don't exist?

By the same token, because QE is not discussed in a specific piece of text, does that mean QE doesn't exist?

Sorry Tom but it covers QE very neatly...indeed it could have been written with QE in mind. The fact is the limitation upon credit creation is governed by the (private) banks themselves and is assisted by interest rate setting by central banks....the reserves are a consideration after the fact as admitted by the RBNZ and crucially the monitoring of those reserves is largely left to the banks themselves (n.b. Westpac et al).

Deposits are not necessarily a requirement of reserves....though national origin (currently) is.

Not according to The Bank of England, it tells us that banks do not multiply up money. https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati….

The Reserve Bank also has this video from the BOE bulletin. https://www.rbnz.govt.nz/research-and-publications/videos/money-creatio…

Economist Prof Bill Mitchell also discredits the money multiplier here. http://bilbo.economicoutlook.net/blog/?p=1623

Are you responding to me? I haven't discussed a 'money multiplier' at all.

Quantitative easing (QE) is a monetary policy whereby a central bank purchases at scale government bonds or other financial assets in order to inject money into the economy to expand economic activity.

1. Central Bank Creates Money

The central bank creates money through an electronic process that adds funds onto its balance sheet. In a real-life example, it’s similar to adding an extra zero to your savings account.

2. Central Bank Purchases Government Debt

Central bank uses money to purchase government denominated debts such as bonds and gilts from financial institutions. This includes banks, pension funds, insurance companies, and foreign-owned entities. These assets are then transferred over to the central banks balance sheet where it is held as an asset.

3. Interest Rates Decline

Reduced interest rates occur as a result. This is because central banks purchase government debt which increases its price and reduces the yield. For instance, the government may borrow $1 million at 5 percent interest, earning $50,000 in interest per year.

On the market, it will sell for $1 million. However, this price can fluctuate based on demand in the market. So if there is significant demand, its price will go up. In turn, central banks significant purchases push the price of government debt up.

So in this example, it may increase its value to $1.1 million. However, the interest is still $50,000. In turn, this would reduce the real interest rate to 4.5 percent. At the same time, interest rates across the economy tend to fall in line with yields on government bonds.

Seriously - take a month off commenting and do some research. There is literally NOBODY at the operational end of the banking and finance sector that would ever say that fractional reserve banking (or loanable funds theory) is anything more than textbook fantasy. See also QE adding new money to the economy.

The Fractional reserve banking theory might sound nice, but does not reflect how banks actually make loans. No waiting for deposits first and thrn lending most of them out. Rather the lending precedes any deposit,

Exactly that. I generally welcome all kinds of views and opinions because they enrich the debate. But when people literally don’t understand how things work it makes discussion / debate very frustrating.

The Fractional reserve banking theory might sound nice, but does not reflect how banks actually make loans. No waiting for deposits first and thrn lending most of them out. Rather the lending precedes any deposit,

'Neoliberalism is contemporarily used to refer to market-oriented reform policies such as "eliminating price controls, deregulating capital markets, lowering trade barriers" and reducing, especially through privatization and austerity, state influence in the economy.'

I don't see much Neoliberalism in todays monetary and fiscal policies, where the heavy hand of the state is everywhere - from interest rate suppression crushing savers to QE distorting markets and asset prices. Markets are heavily manipulated, price discovery is nowhere, and an arm of the state has deliberately and recklessly inflated asset bubbles.

I wish people would start using terms correctly instead of applying the one 'bogey-man' term of Neoliberalism carte blanche across every action that they percieve as adverse.

I agree 100%. Well said indeed.

I wish there were more commentators like this one, with the intellectual clarity and integrity required to call a spade a spade.

Yes I agree, in most cases Neoliberalism is not the problem but it would be a good solution! For example I am not at all surprised that our most regulated market, housing, is performing so badly.

"The heavy hand of the state".....exposes so much.

The answer to the ills and inequities created by free markets, is, so obviously, liberating the market from Govt interfences.

And, following this logic, smoking cures cancer.

I think Prebble and co were right in setting up a reserve bank that controls inflation. But it seems targeting deflation is not such a good idea. I'm thinking the government should set a minimum OCR for the RBNZ of say 5%.

Why inflation will be big this time and was not in 2008-10

https://www.financialsense.com/blog/19921/money-nothing-checks-free-i-w…

Ah so your point about Prebble is he is somehow culpable for current debacle because he was part of establishment that created independent RBNZ!?

Rather long-bow to pull methinks

My solution is ‘stop spending money on things you don’t need’. In other words, do not participate in the economy. It’ll shut it down.

I choked off most of my spending too. some time ago - need a reserve to pay the rent if it all turns to crap.

I think the most important action to escape the rigged system as much as possible is (non-govt) crypto and precious metals.

My trust in govt has died - we bleat to them to fix everything and save us all, and all they can do is steal from future tax payers and savers to buy time.

Interesting how almost every comment has got stuck on the subject of QE and nobody (apart from the Treasury and the Reserve Bank, who prepared a paper on other options which the government chose to ignore in favour of orthodox financing of government deficits) has considered the benefits of monetary financing.

Now that would be a worthy discussion rather than debate semantics around QE vs 'free market' ideology.

All 'money creation', whether QE injection or fiat levering or house-valuation upping (after all, if your house is 'valued' 100k higher and you spring 80k of it, have you not forced the bank to fiat-lend to you because you 'valued' a piece of entropy-bound infrastructure upward?) is a forward bet. The bet includes the hope that a $ will hold its 'value' vis-a-vis resources and processing. The bet assumes there will be a forward underwrite.

All those bets are being made on a depleting planet, all are betting against entropy, and the total bet is increasing exponentially. Who cares whether it's QE, fiat, MMT, a printing-press or whatever? The method isn't the problem, the remaining underwrite is.

"2) Why Richard Prebble could look in the mirror rather than blame Social Credit for the RBNZ's quantitative easing."

Why? I did not see any reason given by Gareth. Maybe the reason is that Gareth just does not like Prebble ;)

Usa has gone to another level post covid.

M1 money is money circulating .

https://fred.stlouisfed.org/graph/fredgraph.png?g=Cm4f

{kind=link}

FYI, This is a response to the Prebble article from Chris Leitch;

I suppose I should thank Richard Prebble for promoting Social Credit - except that none of the claims he makes about Social Credit policy or its views are actually correct.

We should probably not be surprised at that, given you will recall, that Mr Prebble was the former Labour Minister for State-Owned Enterprises who toured the country in the mid 80s promising to save rail and then promptly sold it (and a host of other state assets built by generations of Kiwis) off to his business mates.

About the only correct claim he made about Social Credit is that one aspect of its policy is to make use of the Reserve Bank capacity to create credit and supply it to the government at zero interest – something his former party, Labour, used to fund the building of 30,000 state houses when it first came to power in the 1930s.

Since this time last year the Reserve Bank has again been creating credit, something that many economists, commentators, and our political opposition had always claimed was ‘funny money’ and neither possible nor credible.

An article in the Sunday Star-Times in June 2020 did correctly quote me as saying that Social Credit had been vindicated in that regard, however the article then went on to say this “But that is served with an uncompromising monetary policy that sees QE (Quantitative Easing) as a cop-out.”

“Social Credit demands the Government (through the Reserve Bank) directly creates the “credit” to fund public spending, rather than living off the left-overs of the free market by continuing the conventional international practice of entirely funding its spending through taxation [and borrowing from the private sector].”

“One of Leitch's concerns with QE is that banks might cream a huge profit through the “merry-go-round” of selling Government bonds to the Reserve Bank and then buying bonds from Treasury when it issues them to pay for the Government's $50b Covid-19 fiscal programme”.

“Why not fund the spending direct, with a giant zero-interest loan from the Crown's balance sheet to itself, it asks?”

I was right. Banks are creaming a huge profit through the “merry-go-round” of selling Government bonds to the Reserve Bank. Over the term of the Bank’s current QE round that profit will amount to roughly $11 billion – money that could have gone instead direct to the government to spend on hospital emergency departments or helping alleviate poverty.

Meanwhile the government continues to borrow from those private banks –building a mountain of debt for future taxpayers to pay interest on and eventually have to repay - further money wasted that could have gone instead direct to the government to spend on hospitals, state housing or infrastructure.

Wasted because the government could have got that funding from the bank it owns – the Reserve Bank – at zero interest and without the requirement to repay it. No debt or interest burden for taxpayers.

Despite what Mr Prebble endeavours to suggest, Social Credit has never advocated unrestricted ‘money printing’ by the Reserve Bank.

On the contrary. A key part of its policy is setting up a New Zealand Credit Authority with independence similar to the Judiciary, accountable to Parliament as a whole. Its task would be to assess the economy, measure its unused capacity and labour capability, and determine how much new money the Reserve Bank could safely create without generating inflation – matching money creation with goods and services.

That does not happen however, with the additional credit that the commercial banks create – approximately $20 billion on average each year. That expansion of the money supply is totally unrestricted, yet Mr Prebble is happy to ignore that fact. It is that unrestricted credit creation, essentially out of thin air, that is driving the speculation in property, shares and other assets, and putting houses beyond the reach of first home buyers.

Both the Government and the Reserve Bank are culpable in facilitating that abomination – the government pandering to a newly acquired asset-speculator voter base, and the Reserve Bank in boosting bank profits through its purchase of bonds off them and its Funding For Lending programme.

Mr Prebble’s suggestion that what is happening now is Social Credit is like owning a petrol/electric hybrid vehicle, but never charging the batteries or running it on the electrics. While it is perfectly capable of being run on battery power, to claim that it’s an EV when that capacity is never used is ingenuous, if not purposely mischievous.

What is ruinous is the current, mostly orthodox, economic management being used.

What could fix it is real Social Credit!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.