New Zealand's businesses are reporting that they are now finding it easier to pass on higher costs by raising prices to customers, according to the latest quarterly survey of business opinion from the New Zealand Institute of Economic Research.

And this suggests inflation will be on the rise.

NZIER principal economist Christina Leung said supply chain disruptions "are contributing to the intense cost pressures across most sectors".

This is consistent with findings from recent ANZ Business Outlook surveys.

But Leung says that Kiwi businesses are now finding they are able to pass on their costs more easily - by raising prices.

"A net 8% of firms raised prices in the March quarter," Leung said.

She said this was "a turnaround" from a net 2% of businesses that cut prices in the previous quarter.

"Higher export-

"These results suggest a pick-up in inflation pressures over the coming year."

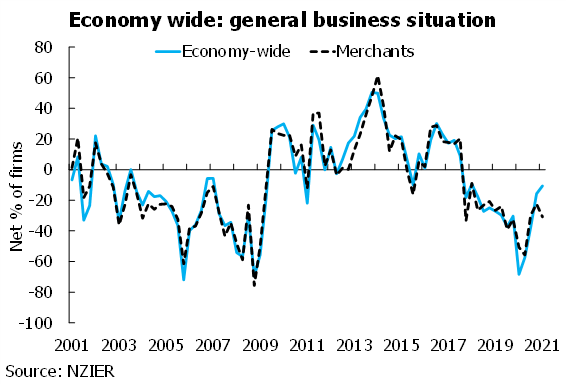

The general results of the latest survey show "a modest improvement" in business confidence in the first quarter of 2021, while demand held steady.

"A net 11% of businesses expect a worsening in general economic conditions over the coming months, on a seasonally adjusted basis," Leung said.

"This is a modest improvement from the 16% of businesses which were pessimistic about the economic outlook in the previous quarter. Meanwhile, firms’ own trading activity was unchanged from the previous quarter. This measure

The survey found retailers most pessimistic of the sectors surveyed.

"The retail sector has become the most downbeat of the sectors surveyed, with a net 38% expecting a deterioration in the economic outlook," Leung said.

"Although retailers report some softening in demand, the significant development has been the surge in costs in the retail sector. This is likely to reflect the effects of Covid-related supply chain disruptions, which are driving up shipping and freight costs and affecting retailers’ ability to restock shelves.

"The building sector has also become more downbeat, despite a still solid pipeline of construction. Supply chain disruptions also look to be affecting activity, along with an acute shortage of skilled labour. Building construction firms report difficulty in finding skilled labour at levels last seen in mid-2017."

However, despite some uncertainty about the economic outlook, firms are continuing to plan for an increase in staff numbers and investment, Leung said.

"A net 8% of firms increased staff numbers in the March quarter, and a net 18% plan to hire in the next quarter. Firms are also feeling more confident about investment, particularly in plant and machinery. Rising labour costs and the reduced ability of firms to bring in workers from overseas given border restrictions has likely sharpened the focus on investment in labour-saving technology."

The NZIER has conducted its Quarterly Survey of Business Opinion since 1961. It is New Zealand’s longest-running business opinion survey. Each quarter about 4,300 firms are asked whether business conditions will deteriorate, stay the same, or improve. The NZIER says the responses "yield information about business trends much faster than official statistics and act as valuable leading indicators about the future state of the New Zealand economy".

38 Comments

Given the valuations many listings are trading at it's implied that not only will costs have to be passed through but profits will have to rocket. However given the tight conditions in the New Zealand labor market I think employees will be well placed until borders reopen.

Until the return for competing cash deposit or debt investment options rise there is not a compelling case for 'profits having to rocket'. Equities are still producing returns at their present ROE levels that are sufficiently attractive at their current valuations.

Inflation may rise 2% or 2.5% but in reality to average person on street - spending has increased much more as the way inflation data is calculated is to suit a particular narrative.

Individual families are already feeling the pinch - they normally do but more so now and if anyone earning has changed or been affected are s$#@%.

Only people who are laughing all the way to the bank is people related to housing market in one form or the other and rest are s#$@%.

Only people who are laughing all the way to the bank - rather all the way to BTC wallet

Property is the only safe bank isn't it?

Yes because even if its value falls to zero you can still live in it.

stuart, what are "Individual families" ?

Each and everyone of us, that goes shopping, can relate to that reality and it has not only just arrived. Still the government and bureaucrats should be happy. Even before CV19 came over the horizon, interest rates were set lower than for decades, supposedly on the premise that people were to borrow to spend to spur the economy. So keep on at folks, it’s working, because you are now even spending more whether you want to or not.

Well reducing interest rates just moves inflation from future periods to the present. In the long term debt causes deflation. That's why monetary interventions are more extreme with every recessionary event because insufficient debt is repaid to allow the economy to stabilise.

Orr will conveniently look through inflation caused by "supply chain disruptions". There is too much debt now - any increase in interest rates will torpedo the economy. Welcome to Stagflation!

In our businesses we are not anticipating an end to supply chain disruptions for a lengthy period. Orr must have a very long lens on his telescope when he does his 'looking through'. We have leased additional warehousing capacity to accommodate the significant increase in stock holdings required to deal with delivery disruption. Price increases have been ramping up since late last year, recently a flood of them. I suspect Orr doesn't fully appreciate how solid the price rise impact is going to be.

What businesses do you own middleman?

Passing on is one thing

But the end consumer doesn't have more disposable to throw round

Something has to break

Just put it on the mortgage, like all the other clever Kiwis. How good is the NZ housing Ponzi!

Minimum wage just went up 7% this month, people do have more money to spend

No, those specific people who were on minimum wage have more to spend. For many others it's "cashflow is tight, input costs are rising, pay freeze for the foreseeable future".

Pay freeze in some industries maybe, but in others like IT, skilled workers are in high demand and pay is going up.

Great, expect that similar number for rent hike. Those essential workers only option is now to do prolong continue work strike to get notice. Perfect!

Why would the essential worker who just got a 7% rise, strike ?

MInimum wage workers have more to spend ? What world do you live in ? Im guessing not the one where 2 minute noodles are a staple for the kids.

He was boasting last year about his million in tax free capital gains. Doesn't have a clue.

Except that I pay staff on minimum wages (cleaners) and they tell me it's great having more money to spend. Do you pay minimum wages Brock or do you maybe earn minimum wages to know better?

The hourly rate of minimum wage workers increased...not necessarily their income.

An article for a change that mentions, how our finance minister has screwed up BIG time :

https://www.stuff.co.nz/opinion/124810915/how-grant-robertson-got-our-e…

Yes. This is the problem when your whole economy relies on credit-driven bubbles.

Two things to de-rail house price growth: rising interest rates OR rising inflation which erodes living standards as it exceeds wage growth. latter is now in pipeline

https://www.financialsense.com/video/19917/weekly-update-highest-food-i…

RBNZ if not mistaken has incite couple months back, they'll do 'whatever necessary' to maintain economic stability (which means in NZ=housing).

Remains to be seen how far world trading partners can set their confidence dealing with NZD. Then the locals confidence supply issue start to pop up.

Time to break your mortgage and fix for as long as possible?

Personally, we will be refixing 5 years.

I'll be taking five years but trying to get more freedom to vary my repayments than we currently get. If I change repayments during a fixed term with my current bank then I'm stuck with the new repayment as a minimum amount for the remainder of the fixing period. Other countries are far more flexible when it comes to early repayments on residential property because they haven't wrapped up their entire financial systems in it.

If you can get 5 years at 2.99% and you're confident you're not going to have to break the term, (break fees can be very expensive) go for it!

Pretty confident and comfortable with paying 2.99%. Mostly upside for us, aside from opportunity cost if rates drop, but with inflation taking off the risk of rate increases outweighs the potential interest saving for us.

Yip, go for that HSBC. Always took the 5yrs loan term for big ticket item like that. Don't sway by those OZ banks, usually the poor greedy mindset that banking with them. When you got spare after that, go for more bonafide Agri bank such Rabo.. for peace of mind that it's not going into housing ponzi. Instead to feed Kiwis.

Better still, to circulate it to OZ, then split into different quart which under guaranteed scheme, after this soon border opening. Dark financial cloud is coming to NZ. Hey, it's no harm done by prep.

"Always took the 5yrs loan term for big ticket item like that." If that's true you have missed out immensely on the dropping interest rates for the last 10 years at the tune of many $10'000.

It's like buying insurance - doesn't always pay off but gives you peace of mind. When the interest rate trend changes it will no doubt be beneficial.

That said, I'm on a 1 year deal right now but the loan is pretty manageable so I didn't pay for the 'insurance'. Lower rates mean I have increased my overpayment.

Yvil

Re break fees

Quite some time since I had a mortgage but in the old days my bank allowed me to transfer my mortgage from one property to another when trading up under the same term and (then attractive) rate.

If looking to fix long term it would be worth asking about the banks attitude to this in the event one transfers due to job, decides to trade up, or even unexpectedly downsize in a marriage breakup.

Great to see a thread about being prudent.

Clearly there are signs of winds of change regarding interest rates. Not sure how long current very low rates will hold but it looks like it could be the bottom with future rates tending to show upside.

Like the comment about having the ability to pay down.

One may be able to currently 2.5% but that minimal extra at 2.99% looks cheap assurance.

Fixed for 5 years 4 weeks ago

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.