By Bernard Hickey

Economists and the Reserve Bank broadly expect the Official Cash Rate (OCR) and floating mortgage rates to rise around 2-3% over the next two years, while house prices are expected to rise in line or slightly below inflation of around 2%.

Fixing or floating is seen as a close call and is dependent on a borrower's view on how quickly interest rates rise and their desire for certainty, although some economists have called this week to fix because they think interest rates will rise sooner and higher\

Most economists now expect the Reserve Bank to start increasing the OCR from its record low level of 2.5% from September 15 and to lift it to around 4.5% by the end of 2012. BNZ sees the OCR rising to 5% by the end of 2012. Westpac sees the OCR raised to 6% by the end of 2013. Both have said now is the time to fix. ANZ National expects the OCR to rise to 4% and says floating remains best, while ASB sees it rising to 4.5% and that floating is better for now.

Stronger than expected GDP growth and inflation figures in mid July have prompted some economists to pull forward or harden up their views on when the Reserve Bank will next hike rates. The Reserve Bank's decision on July 28 to leave the OCR on hold but to signal the removal of its March 10 rate cut has pulled forward the first rate hike to September 15. See our July 28 article on the OCR decision and the reaction of economists.

The Reserve Bank itself forecast in early June that the 90 day bill rate, which is typically around 0.2% above the OCR, will rise around 2% to 4.6% by end of 2012. That would imply floating mortgage rates rising to around 7.7% within the next two years from around 5.75% now.

The Reserve Bank forecast in June that house price inflation would be in line with or below the rate of inflation over the next couple of years. It is forecasting inflation of around 2% per year over the next three years. Economists are not unamimous on house prices, though most see house prices rising by around the inflation rate over the next couple of years.

Floating vs fixing?

Before the Global Financial Crisis this was an easy decision for most borrowers because fixed mortgage rates were almost always cheaper than floating rates. But that changed after the Lehman Bros crisis because banks were unable to find the cheap and easy short term wholesale funding that helped them keep fixed rates lower.

Since then the Reserve Bank has also tightened funding rules that encourage banks to fund more locally and for longer terms than before. This has made fixed more expensive than floating and is likely to keep it that way.

Any decision to fix or to float depends on how quickly and how high interest rates will rise. Floating makes more sense if interest rates stay lower for longer, while fixing makes more sense if the OCR rises soon, quickly and to a high level. Fixing may also make more sense for those who place a premium on having certainty about their repayments, regardless of whether they are higher than staying on floating. It's a close decision if you assume the Reserve Bank's own forecasts for the 90 day bill rate are correct. See our Brother in Law's guide for more discussion on the fixed vs floating debate.

Also see our calculator for working out whether fixing or floating is cheaper over the life of a fixed term mortgage.

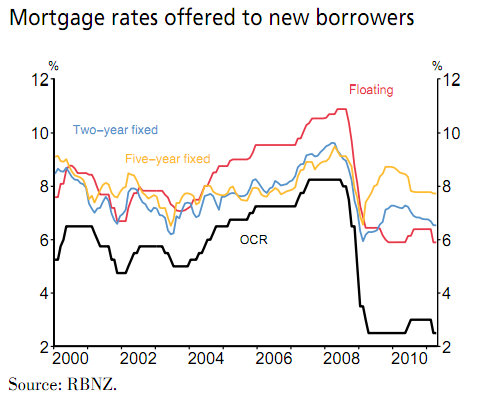

Here's the RBNZ's chart below showing how fixed and floating rates have tracked since 2000. And click here for our interactive chart showing average bank interest rates since 2002.

My view:

I think high household and government debt levels in many large developed economies will restrain global growth for some years to come and New Zealand households are being a lot more cautious about taking on new debt and spending than they were before the Global Financial Crisis.

Further financial market turmoil and a slow Christchurch rebuild may keep the OCR interest rates lower and for longer than economists think. That means I think floating is cheaper than fixing for now, but only because I have a more bearish view on global growth than the RBNZ and economists.

We have a calculator which works out whether fixed is cheaper than floating, given the assumption that the RBNZ's forecast track for the 90 day bill rate is correct and given the current average mortgage rates. See the current mortgage rates offered by banks here. The spreadsheet shows the average one year rate of 5.89% is the best, the average two year rate of 6.42% for 2 years is second best with a 'loss' of NZ$78 over the two period of a NZ$200,000 mortgage, while the floating rate is NZ$880 worse off over the two years or NZ$8.50 a week.

I also think house prices will grow less than inflation and may fall further in some areas. I stick to my longer term view that house prices are still over-valued and will eventually fall to around 15% below their 2007 peaks.

They are currently around 5% below that peak and are down more than 11% in inflation-adjusted terms since that peak, which is the biggest fall in real house prices since the stagflation of the 1970s.

See David Chaston's article here.

The RBNZ's view

The Reserve Bank of New Zealand said on July 28 the economy was recovering and it saw little need to leave its OCR at the 'emergency' level of 2.5% in place for much longer. However it said the high New Zealand dollar reduced the need after the removal of the emergency cut for further increases in the short term.

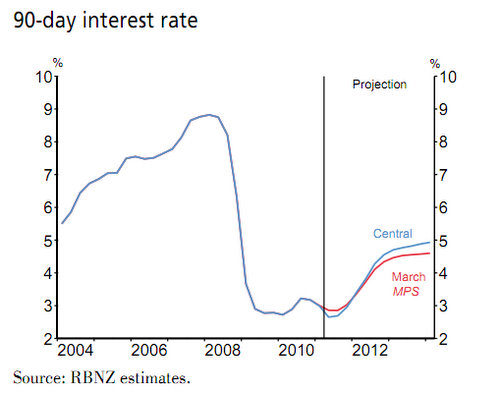

The RBNZ forecast on June 8 the 90 day bill rate would rise from 2.6% in June 2011 to 4.6% by the end of next year and 4.9% by March 2014. The Reserve Bank doesn't forecast the OCR, but the market watches its forecast 90 day bill track as a close proxy of where the Reserve thinks it will be.

Here's the chart of the forecast. The red line is where it the forecast was in the March quarter monetary policy statement. Click here for our interactive chart of bank bill rates going back to 2000.

The Reserve Bank said in its June monetary policy statement it expected house price inflation at or below the inflation rate over the next three years.

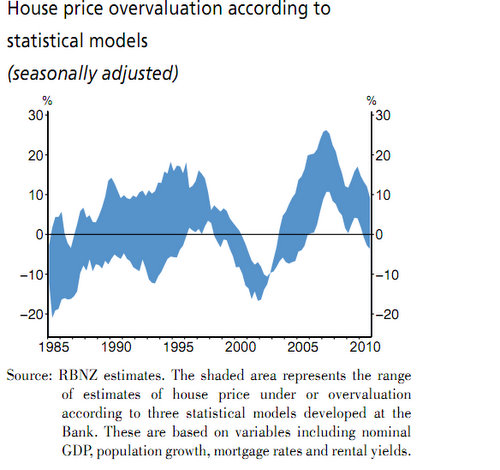

Here's its full comment with its chart below on how overvalued it thinks house prices are:

Consistent with subdued consumption, house prices are likely to increase only modestly over coming years. A number of in-house statistical models suggest that house prices continue to be overvalued when compared to metrics such as nominal GDP or rental yields (chart below).

As a result, house price increases are expected to be at or below the rate of inflation over the projection.

The Reserve Bank hasn't expressed a view on whether borrowers would be better off fixing or floating, but it notes that its ability to control the economy through the OCR is stronger when more people are floating rather than fixing. It said in June that the average duration of all mortgages was now below 6 months, compared with almost 2 years back in 2007.

The BNZ's view:

BNZ Head of Research Stephen Toplis said in a note titled "RBNZ too cuddly by half" that the bank appeared to be making the same mistakes it made during 2006 and 2007.

"In the last major tightening cycle the Reserve Bank got it horribly wrong because each and every time it raised interest rates to contain inflation it suggested that the hike, at the time, might be enough. In that fashion it failed to change the behaviours of the populace as there was no “fear” that interest rate increases might prove painful. Consequently, both interest rates and the exchange rate ended up higher than needed to be the case," Toplis said.

"Lightening appears to be striking twice. In today’s OCR review the Reserve Bank has given the green light for the removal of the emergency rate cut introduced immediately following the February 22 Christchurch earthquake but has then failed to push through with a stern warning that inflationary pressures are building. In fact the Bank goes so far as to downplay inflationary risks," he said.

The bank had sold its message poorly and signalled it would raise rates 50 basis points in September, although Toplis wondered why the bank was waiting until then.

"More worrying, though, is that the RBNZ goes on to say that the strength of the currency “is likely to reduce the need for further OCR increases in the short term”. We interpret this as meaning the Bank, currently, sees rates on hold at 3.0% until March next year. However, we also note the reference to “short term”. Accordingly, we still think the Bank believes rates will move up to its previously proposed 4.75% in due course."

The ASB's view

ASB Economist Nick Tuffley moved his rate hike forecast forward to September from December after the announcement. He now sees a 50 bps hike on September 15 to 3% before a pause until January.

"The RBNZ was very specific that further increases in the OCR (i.e. beyond the removal of the 50bp insurance cut) were dependent on the level of the exchange rate (the Trade Weighted Index is likely to be the most appropriate measure to consider)," Tuffley said.

"What is apparent is the RBNZ wants to take back the March 50bp ‘insurance’ cut very soon. That suggests a September hike is very likely, and in our view a 50bp is more probable than a 25bp. The RBNZ sees “little need for the March 2011 ‘insurance’ cut to remain in place much longer”, and our interpretation is that means an imminent move and also reversing the March cut in one hit," Tuffley said.

"Beyond that we see the RBNZ pausing until January, then resuming steady 25bp OCR increases. Further hikes, beyond removing the ‘insurance’ cut’ are conditional on the level of the NZD, ongoing NZ economic recovery, and the fluid global situation. We expect the NZ dollar will remain elevated, and “likely to reduce the need for further OCR increases in the short term”," he said.

"This means NZ interest rates are going to be trading as if the MCI was still in use. Furthermore, NZ commodity prices (and the Terms of Trade) are likely to moderate, reducing the income boost to NZ. These are reasons, we believe, for the RBNZ to pause (after removing the insurance cut) for the rest of the year."

Tuffley said markets had now fully priced in a 25 basis point hike in September.

"Meanwhile, longer-term domestic interest rates declined slightly, given the uncertainty around further OCR increases beyond the 50bp increase by the end of the year," he said.

ASB said in a July 1 note floating may be cheaper than fixing for the first year, but be more expensive after that, although it notes this all depends on how quickly the OCR rises.

Our calculations suggest floating could prove to be slightly cheaper than fixing for a year, due to the lower floating rate being paid over the coming eight months. However, for horizons beyond the one‐year mark, fixing may turn out to prove a cheaper strategy.

They forecast house price inflation firming to around 3.5% by the second half of 2012.

Westpac's view:

Westpac Chief Economist Dominick Stephens said he now expected two 25 bps hikes in September and October before a pause in December.

"The Reserve Bank today kept the OCR on hold at 2.5%, and issued a rather nuanced interest rate outlook. The upshot is that the RBNZ is planning 50 basis points worth of hikes in the near term, followed by a pause. But the early hike(s) are conditional on the domestic economy continuing to recover (which seems likely), and global financial risks receding (which is less certain)," Stephens said.

"We believe the most likely scenario is two 25bp OCR hikes, one in September and one in October, before a pause in December. A 50bp hike in September is distinctly possible, should global financial concerns about US and European sovereign debt abate. But that’s far from certain at this juncture. Indeed, a significant deterioration in financial market sentiment could yet delay the early hikes altogether," he said.

Stephens said now was the time to fix.

ANZ National's view

ANZ Chief Economist Cameron Bagrie said he now saw the RBNZ removing their March 10 'insurance' cut of 50 bps at the September 15 meeting.

"We see no point in unwinding the insurance cut in multiple steps. But we think the RBNZ will pause thereafter to assess the landscape," Bagrie said.

"The Governor made it clear that the high NZD is a concern, which will lessen the need for further increases thereafter. The bottom line is that the OCR is set to move off emergency settings but still remain stimulatory."

ANZ National's economists said in their June 24 Property focus they favoured floating over fixing for now...just. They said housing turnover was recovering but prices were "listless".

Mortgage rates were unchanged from last month. Given increased uncertainty, we favour floating for now. Broadly speaking, the rises implied by the mortgage curve are consistent with the RBNZ’s projections, and our own expectations. If it were purely a question of cost, it would thus be a line call between remaining floating, or choosing a fixed term like 2-3 years.

BNZ Chief Economist Tony Alexander said in his July Real Estate Overview on July 26 the housing market had entered a cyclical upturn.

New Zealand’s housing market is trading at low levels with prices on average still some 4% below late-2007 peaks, construction near the lowest levels in four decades, and turnover less than half that seen in 2003/04. However there is a shortage of property now manifesting itself in agents reporting a sharp increase in difficulties finding new listings. This is happening at a time when more and more first home buyers are entering the market in an environment of increased discussion of the shortage, awareness of upward creep in rents and prices, and with interest rates set to come off their four decade lows.

While high levels of debt and low affordability by world standards will tend to constrain the extent of the housing upturn, barring a new global economic catastrophe, it appears that New Zealand’s housing market has started a cyclical upturn.

Here is a summary of the various economists (and my) view on interest rates, house prices and fixing vs floating.

| Forecaster | First OCR move | Peak OCR | Fix or float? | House prices |

| RBNZ* | December quarter | 4.75% by Dec 2013 | Prefer you float | <2% pa |

| ANZ National | September 15 by 50 bps | 4% by end 2012 | Float for now | Listless |

| ASB | September 15 by 50 bps | 4.5% by Nov 2012 | Float for short term | 3.5% pa |

| BNZ | September 15 by 50 bps | 4.75% by Dec 2012 | Fix for 2-3 years | n/a |

| Westpac | September 15 by 25 bps | 6.0% by Dec 2013 | Fix | 0% in 2012 |

| HSBC | September 15 by 25 bps | 4.25% by Dec 2012 | n/a | n/a |

| Bernard Hickey | December 8 by 25 bps | 4.0% by Dec 2012 | Float | -5% |

* Forecasts implied from 90 day bill forecast track in June 9 Monetary Policy statement

36 Comments

Bernard gets my vote to be the next Govenor of the RBNZ

Westpac can go back to Aussie

It seems almost certain that the OCR will be back to 3% either in September, or December. It seems reasonable to think that it may be 50bp higher again by around early-mid next year.

Anything beyond that is pure star gazing. Still, it's the economist's job I suppose, so you can't blame them for having a crack. Funny how they're always pretty close to each other though. No one wants to take "career risk" (except BH!)

"Star gazing" ...they will only see what what they want ot see....

No question the piigs fiasco will lead to a rise in the cost of credit as the liar banks set about rebuilding their bonus bins.

Only fools still claim the usa is a land of milk and honey with a growth future...more likely this will be a century of misery and strife as their debt burden and behaviour terminates the Republic as it currently is.

Down here we will cop a faceful of the rate rises regardless of the micro economic matters. Housing therefore is more likely to be in constant decline for two decades unless a swine govt embarks on an immigration drive aimed squarely at masking the crap and faking some growth.

That decline, will in itself be hidden by the ongoing debasement of the currency...making it look as though things are 'steady as she goes'

The demand for credit will continue to fall..leading to more BS advertising by the credit vendors.

Increasingly Joe Kiwi will discover the benefits of not being in debt...and this trend will threaten the power of the banks to dictate RBNZ policy. This is happening now and Bollard's near zirp game is his effort to punnish savers and reward borrowers. Exactly what the banks told him to do.

It is ironic that the very behaviour by Kiwi that will lead to a future of better economic times, is being discouraged because it imposes risks on the credit vendors. QED NZ is a democracy in name only...'banktocracy' is far more accurate. The credit vendors are in total control.

Wolly in your view the world financial situation is pretty dire... what then is the answer? How does a young Kiwi hoping to retire at 65 make plans for his family's future? What does a woman in her early forties after losing everything in a bad relationship do? Do they just have to hang in there and see where the ride takes them? I am asking a serious question...

Cheers

Mandalay

Jeez Mandalay you don't want much!

Depends...how young is 'young'?

The answer:...reduce outgoings..enhance income...divert surplus into a range of commodities and utilities( buying in a big correction...BIG got it) be content with what you need and bugger wasting capital on crap.

As for relationships...burn the bridge but learn from the turmoil. Enhance your positives...scrub away the decay...go healthy and don't do it by splurging on stupid programmes designed to take your money....think about it.

Buy a bloody bike, helmet and glaring jacket and ride your arse off...hell you might run into a real bloke coming the other way!

brilliant, thanks for the relationship help too... but am neither of the above examples. I just talk to lots of different struggling emerging middle-class poor people and I was trying to find a median point of the folk collective and ask a succinct question that would encompass them all...

It just seems most people are finding it really tough Wolly... debt on house, or high rent knocking high percentage of salary... high fuel,gas, electricty, gst and food and all seem to be a fortnights pay cheque from the dole... There are very few people I know and I meet bunches of them every week, who can save anything, because after basic living costs they have nothing... let alone invest in anything. Without exagerrating, 90% of them are looking at Australia and wondering if they should go, or are just getting on the plane and going!

I try to be positive around them, but not being a finance guru there is very little I can advise them on... and so many financial gurus assume all middle-class people have a shite load of disposable income to burn, which the certainly don't... I just don't want to be a catalyst to furthering their dispondancey... most Kiwi middle-class famailies are really struggling!

Soon NZ will discover the meaning of "strategic default" adn "strategic foreclosure" as more and more renters to the banks (excuse me "homeowners") have their homes fall below the value of their property, and start walking away from their debts, and start mailing in their keys to the mortgage company, whoever that may be. It is safe to assume that the mortgage holder is an Aussie bank, so if you want to see the state of lending in this country, all you have to do is look across the ditch at what is happening in OZ, and realize that whatever happens to be happening in Auckland real estate doesn't mean flip compared to the place from whence all our banks come! What makes any of you believe that we little Kiwi's are somehow immune? That the spigot of free cash lent to us by Aussie banks will just continue forever? Do you really believe that if Aussie stop buying homes? If China decides they don't need so much Aussie mined goods for a while? That they too need to stop building so much, and actually start putting people in their empty skyscrapers before building a dozen more?

I maintain my position that real estate is basically stuffed for a generation, there is no savior for the market, that current Auckland activity is a "blip" on the bigger radar screen (one being filled by desperate Asian buyer seeking safe-haven for their money and families for the ultimate collapse and possible war they see coming), and that everybody with half a brain should have already bought gold and silver (as are many Asians).

I first posted this over a year ago, and my position hasn't changed. Gold is the only predictable lifeboat on the ship of fools making so-called "finacial policy." When it all comes crashing down, it will be every country for themselves, and ultimately every family and man for himself. That is why I am also recommending to close friends that they also stockpile food, because you can't eat gold. Thankfully for NZ, we are not densly populated, and not 100% dependent on food imports like other western nations have become. We are closer to self sufficiency than a lot of other countries. That may matter more than anything in a "worst case scenario" that becomes increasingly plasuible as debt shennanigans continue. It's all paper.

Gold is real, food is real, paper is paper.

A mortgage is a noose of debt enslavement at this point, and only maybe helpful if we have hyperinflation, but it is too early to say if "they" will let hyperinflation accelerate, or allow countries to "take their medicine," default, and go through the painful process of restructuring, or better, refuting the debts like Iceland, who is now in recovery. Frankly, I wish they would just get on with it, instead of bringing the corpse back to life with ever more debt gyrations, interest rate moves, etc. I agree with Steve Keen that what we really need is a Jubilee, the ultimate "reset button." It's better that we decide to do it consciously than to let the market do it for us, a far more messy alternative. Debt reshuffling only buys time, and makes the inevitable day of reckoning that much more painful. This is what we should all be planning for...the eventual day of reckoning.

In hyperinflation, wages go more and more towards food and fuel, and less towards property. We are seeing this now, and see no reason why it will not continue. The best plan is to stock-up on both food and fuel (firewood, etc), and have some gold as insurance to protect any wealth, assuming you are lucky enough to have any at this point. This is the part of the economic cycle where those that were not wiped out by the 2008 collapse will now be wiped-out, if they are not prepared. Gold protects purchasing power in both deflationary and inflationary environments, adjusting in value automatically. Silver is an even better deal. When I recommended over a year ago, it was $17. How many of you listened? Did your own research?

Got gold?

Time to flee to Mars? http://blogs.telegraph.co.uk/finance/ambroseevans-pritchard/100011129/f…

NZ house prices are historically very expensive still, even after 4 years of zero growth. The issue is that wages have not kept pace, and also rental yields are far below borrowing costs, this means that both as a homeowner and potential investor, NZ houses are expensive.

I don't think we we will see a repeat of the massive rise in values of 2002-2007 anytime soon. For one, net migration is about to turn negative as our high NZD exchange rate discourages people from Britain and China to immigrate here. More people leaving for Australia than arriving is not good for property prices. Also with interest rates about to rise and property prices still high - affordability is really stretched.

I still think though that overall NZ is in a good position relative to other countries. Who would want to be in the USA, Britain, or Europe right now? As long as our government can keep reducing spending and cut down our public debt, we will come out of this in pretty good shape. I don't think stockpiling gold and food is the answer. Gold is the only investment that does not pay a dividend! Maybe owning a bit would not be bad but I don't see any point in putting all eggs in one basket, in case Gold is the next bubble waiting to burst.

Return on investment? Which investment HASN'T gold outperformed in the last 10 years? Real estate? Tick. Stocks? Tick. Bonds? Tick.

Tick...tick...tick...tick

meanwhile money being actively printed as the "solution." It still amazes me just how few people understand the real cause of inflation- more money means money becomes worth-less, to the point of becoming worthless. Gold simply adjusts accordingly. Silver too, which will be an absolute fireworks display before this is over. I can't believe how few people even have a clue about the history of money- especially fiat currencies. It's all about protecting purchasing power at this point. Yes, you can't eat gold, but you can't take a bite out of your house either, but said house can certainly drain your disposable income, leaving you less to buy things like food.

There is a building flood of property building in the market right now. I predict it will be hitting the market in the next 60 days. A lot of motivated, desperate sellers.

Interest rates aren't going anywhere, by the way. Banks can't raise rates without destroying themselves! If they raise rates, they put more families into mortgage distress, and they end up taking more homes in foreclosure, and banks aren't in the landlording business.

If they raise them in the short term, they will be forced to lower them in the long term, and acknowledge their mistake. If New Zealand loses control of foreign capital markets, and can no logner get easy access to capital, then the cost of said capital will go up, and the mortgage payments as well. Wither option = uncertainty, which is bad for prices. A higher interest rate means higher carrying costs of the property, unsutainable for average buyers = lower house prices. Lower house prices means people owning houses worth less than the value of their mortgage = more people walking away from their property and mailing in the keys to the banks. I am certain that there are far more homes in distress than the official media lets-out. People are really struggling out there. How can this be a good recipe for rising home prices? This is not 2006. Prices might be higher, but wages simply aren't. So where is the catalyst for higher prices? China? Temporary.

"They" know that if they raise rates, they can't fool first time buyers into buying a house on "easy monthly payments." So they will keep rates where they are, or lower them. IF they make the mistake of raising rates, they risk putting more mortgage holders into distress, more homes "underwater," and risk taking on more property via mortgagee repossession, something that banks in America know all-too-well. Bank want ignorant, complacent "homeowners" servicing (what a good word- another word that means "getting fcuked") the debt, a debt rolled-over from the last sucker who paid too much for the house in the first place.

Banks aren't keeping rates low for the good of the people, they are keeping them low so the bank itself can survive, and not choke on a flood of foreclosed property. That's the real reason. Banks are not charitable institutions.

"A rolling loan gathers no loss." Find a sucker to take over the huge debt from the previous owner.

The name of the game now is to float enough loans to keep asset prices up, so they, the banks, don't chock on an orgy of mortgagee sales. Meanwhile, over in Aussie, more and more "homeowners" (renters to the bank) are givng up the ghost on their debts, turning over, going bankrupt. The "lucky country" isn't so lucky any more, as they have a number of their own problems, gathering momentum, because things were so rosy for so long, prices have gone up to match said rosiness to the point that now it is too expensive to live there. I think people considering leaving NZ should really consider this, because grass is often greener on the other side because you simply failed to water your own grass. Their real estate sales figures look atrocious and completely sick in the last quester, with no hope of appreciation. The banks will choke on these. Who will they sell these dogs to? Oh yeah, "ya can't lose with property, maaaaate!" This is the real reason for allowing low-down loans- they need the suckers to take-on the existing debt so as to not crash the bank's books.

Those that wait-out their bluff will buy some real bargains "soon." This bluff cycle will be over soon enough. If you want to believe Olly, be my guest. But I won't jump off a bridge just because Olly, or Barfoots, swears it's safe. If you do, then good luck. I hope it works out for you. Meanwhile, I will be renting for the foreseeable future, until such time that it costs less to own. It might be a while, but I'm in no hurry.

About now, you have thousands of so-called "investors" sitting on a rental property, or two, or three, each losing money by the week as they are servicing the debt and the cost of maintenance, thanks to a new law change.

Right now I can hear the voices of a thousand arguing spouses saying, "how can we pay all these mortgages if the rents don't cover the costs? We can't raise the rents because people will move out. Where do we get the money, now that we have to pay with our AFTER TAX income from our jobs?"

I expect to see a flood of these "soon to be ex-landlords" dumping their properties on the market in the next 60 days. There will be more properties for buyers to consider, driving down costs. Supply and demand says prices stay flat, at best, or go down. Who wants to take on more debt? To encourage they we all DO take on more debt, banks have NO CHOICE but to keep rates low.

Auckland = Vancouver It all sounds great with the easy Asian money. Soon the music stops, and there will be a lot of tears. It's happened before. I won't say when, but all I will say is "soon."

But hey, "this time it's different."

Prediction- house prices 10 years from now are are the same today.

I commented to my wife three years ago that I doubted that house prices would pass the level that they were at in 2007 in the next 18 years.

I still think they will be below that level in 15 years time.

HR. New Zealand real estate and gold are running neck and neck in price terms over the last 10 years in NZD terms. The difference is that gold is not an investment. It is a speculative hedge against inflation that produces no income. It is prone to sudden and huge plunges in price as happened after the price peak in 1979. It lost 75% in a few months. Silver fared even worse losing close to 90% after the Hunt brothers attempt to corner the market failed.

Not saying that your strategy or reasoning is totally without merit, but you don't seem to acknowledge that speculating in commodities is an extremely risky business. I well remember the the gold and silver bugs 32 years ago saying almost exactly your words before it all ended in tears for them. You should talk to PDK or Steven about how much embedded energy there is in an already built house and section. Lots. The price of oil has appreciated just as much as gold over the last ten years.

I have one percent of my money in physical gold. I look on it as insurance.

I don't care if the price of gold plummets. I hope it does. It means that the economy is going ok and the other 99% of my investments are ok.

I hate it when the price of gold goes up. It means that there is fear and uncertainty.

I pay my insurance but I hope I never have to use it. I buy my sovereigns and hope the same.

Good strategy Stuffed. I have a few coins as well. The grandkids are mesmerised by them, (treasure!). Like you I hope they never have to be used. Because in that case it probably would be to swap for food and bullets.

Now it's a matter of placing your bets for the next 10 years. Precious metals are on the launch pad to the stratosphere. Can you say the same for real estate, percentage-wise? I'm sorry but real estate has NOT kept pace with gold prices. Looking from 2001-2011, gold went from $250 an ounce to $1600 an ounce. That's a 7 times increase. That means a $100K house would have to be worth $700K today, and MAINTAIN that value through this recession. I think you will be hard pressed to find those houses.

In terms of it being a bubble, one must ask "compared to what?" That's an empty argument unless you have some figures to back it up. I will go with shadowstats.com and John Williams, who says that the manipulated inflaton figures, when adjusted back to the way they USED to be calculated, say that gold would have to go over $3000 an ounce before you would even consider the word "bubble." And silver? Much higher than $100 an ounce.

You have to consider a few other factors, relative to the price of precious metals, and the differences, as well as the similarities of these markets, as compared to 30 years ago. You have to adjust for inflation, yes, and industrial off-take. It was just 1973 that an Aussie 50 cent coin had .34 ounce of silver in it. Today that same coin is worth around $12. Another fact, the Hunt brothers high in silver was $50, a figure that has not been reached since that time. Meanwhile silver has found a thousand other uses, and there are few fewer ounces "above ground" than there was in 1980, when the US still had a massive stockpile of the stuff. Since industrial uses, and modern electronics like TV's use the stuff, that metal is GONE. Now that it is being re-discovered as a montary metal, supply and demand DEMANDS that the price explode sooner or later. It will probably be about the time the money printing press breaks, I reckon. Yes, real estate will adjust in value, but you can't easily sell a rental property in a broken, unpredictable market, when everybody is equally broke. Who will qualify for a loan when the price changes daily? That's what hyperinflation looks like, and I think we should all get an education because this is the first time in history that ALL of the world's currencies are NOT tied to a metal, so they are ALL free to print at will. It's going to get a lot worse before it gets better. We are in the stage where people are shunning debt, but soon they will want to take on as much debt as they can and spend their savings while it still has purchasing power. We are not immune to this happening.

On the other hand, if the Kiwi dollar surges, our exports become too expense and we have a another recession. How is that going to help NZ home prices?

I suggest listening to John Embry or Jim Sinclair. These guys know a lot more than all of us put together, and are likely a whole lot wealthier. Embry says we will one day reminisce about the days that silver was below $50 an ounce, and Jim Sinclair just increased his goal for gold price to over $10,000 an ounce, CONTINUAL QE roll-outs/bailouts (ie: money printing and inflation), now that his PRIOR prediction of gold hitting $1650 an ounce by January 2011 appears to be happening, albeit a few months off. He made that prediction in 2001.

Looks good, but haven't 'we' been here before? The Gold Confiscation Of April 5, 1933 "http://www.the-privateer.com/1933-gold-confiscation.html"

yep....and other wee things Govn's will do if they have to....For instance I seem to recall Wilson's Govn was ready to seize incoming foreign pensions at one stage to keep them going...screw the ppl waiting for their money.... At least gold can be hidden....pay cash so it cant be traced....not much else is that small, easy to hide and hard to destroy.

regards

A lot of things have changed in the markets for paper and metal. You haven't done your homework. You are extrapolating assumptions and past experiences to today's circumstances. While there are a few similarities, there are far more differences. To sum up, the monetary "solutions" employed by the the US Treasury and Roger Douglas are no longer available. The only "solution" is to print money, and the effects will be devastation, looking back one day as we share our stories. I suggest catching up on your reading.

Right then, im off to the Bank to see if they'll lend me 80% against gold.

I cant lose right ?

Gold only ever goes up in value right ?

HR have you got some gold you can sell me ?

There are a few importers in NZ. I think it would be cheaper to buy it from the US and have it shipped in GST free. It's clearly in the customs rules- GST free for 99% purity. Importers just add their profit to the price. Try tulving.com or Apmex.com There are several others like Miles Franklin who will also export.

I am only buying. Not interested in selling. I suggest buying the real stuff, not paper promises to deliver at a future date and putting it in a safe deposit box and keeping your mouth shut. i will leave it at that.

Silver is now in backwardation. All of you should learn the significance of that. Gold has gone in and out of backwardation in recent years. The next time it goes, it may never leave that state until the price is much higher. Anything under $3000 an ounce is an absolute bargain. Any silver under $50 an ounce is an absolute bargain.

Anyone keeping their savings in dollars stands to get slaughtered before all this is over.

It is time to lifeboats. Do you really think our fearless leaders, excuse me, politicians, will come up with a solution that works well for everybody? Why are central governments now stockpiling gold? Why aren't you?

Submitted by Jim Willie CB, editor of the "Hat Trick Letter"

Conscience Of A Gold Investor

Many deep dilemmas face investors of Gold & Silver. First and foremost we feel an urgent need to defend ourselves against a crippled corrupted USDollar. The level of debilitation cannot be adequately put in words, as it has lost perhaps 70% of its value just since 1980 when the Jackass entered the workforce after years at the university. The USEconomy cannot be rebuilt or sustained on bond fraud, debt auctions covered by the printing press, endless war, phony accounting, outsourced industry, home equity extractions, rigged financial markets, constant deception on economic recovery, falsified economic statistics, and pursuit of the next asset bubble. The end game is fast along, gaining traction as much as public attention. The remedies put in place more.... http://www.zerohedge.com/news/guest-post-conscience-gold-investor

You need to ditch the dogma and deal with facts. On 27 July 2001 the price of gold was USD269oz. The NZD/USD cross rate was 0.41 , so gold was NZD658oz ten years ago.

Ten years pass and gold is usd1600oz and cross rate 0.87 , so gold is now NZD1,839oz. That's 2.79 times, not 7 times. Real estate did better in New Zealand without even accounting for the rental income. If I want to "place my bets" as you say, I'll go to the casino or buy a lotto ticket (or maybe some gold.) I won't however, kid myself that I am investing. Investment requires income producing assets, which gold is not. So you can sit in your rented house with your bar of gold and each week shave of a bit to give to the landlord for rent, until one day it's all gone.

However you ignore some things, guess its the dogma....if house prices drop (which is as far as I am concerned a given) than that income needs to cover the value of the asset loss and then pay bills and then whooppee a return...If you are neg geared to make capital gains but are now in fact losing income and captial as well you are losing twice...

Just like shaving a bit off the gold bar really....

regards

There ought to be a law against shaving sovereigns!

How many shaves does it take to get to a half sovereign?

Don't shave your sovereigns Stuffed. If you scrape off the gold part the chocolate will melt.

You sound like Warren Buffet, whose stock has never fully recovered from the GFC. On that note, I have placed my bets that real estate is set to take a dump in coming months/years. At best it will look like a slow deflation of the the bubble. Have wages gone up to match the price of real estate? I rest my case. You are free to invest how you like. I wish I had more real estate to sell you.

I do still work to pay my bills- haven't had to resort to eating seed cord- yet, but if food prices keep going up and up, that day may eventually come. I have likely owned more real estate than most who post here, and sold most of my property in 2009, after a long wait for a buyer(s). Gold is merely an insurance policy, which is highly needed in these uncertain, manipulated times. A lot of people are going to go broke, and a few are going to get incredibly rich if they place their bets right. This happens about every 80 years.

I have heard stories of people buying farms with a few gold pieces. Those stories are out there and they did happen. I believe we will see it again as people shun everything to pay for basic necessities. A lot of goods will simply go on sale as families are forced to re-assess their priorities, as crisis become average news.

Rental income doesn't count if it doesn't cover your costs, especially in light of the tax law change. That translates into a lot of real estate inventory about to hit the market to be sold, by landlords who can't afford to keep their rental properties. A lot of people heading for the exits all at once. The recent property listing just surged this week in my area, I guess in anticipation for the "selling season"- ha! Supply and demand tells me prices are headed down. Or you can continue to believe the bankers and the evening news.

You can all point fingers at Bernard for his "30% reduction" prediction. i think he's closer to the eventual outcome, and this should also be considered in light of Fuel, groceries, and other living expenses being 30% more expensive, while real estate has not appreciated 30% in the same time. That's the distinction of purchasing power that so many seem to miss.

As the news parrots about how great the economy is, they simply ignore the fact that prices have gone up in response to all the printed money floated into the market. This is the real cause of rising prices.

Meanwhile gold has gone up more than 30% in the same time that real estate has been down or flat. Let's look to the future- where will it be then? I will place my bets with gold, thank you very much.

Warren Buffet says the same things about gold that you do (ie: it doesn't produce anything, doesn't turn a profit, etc), and now parrots the "everything is fine" line just like other mainstream media pundits who never got it right. Do you want your profits paid on something that can be printed on a laser copier? Why not think of it that way? These colored pieces of paper we call "money" are only backed by faith. What happens when that faith disappears? As we are seeing in America right now? Are we really so different? What makes our colored pieces of paper so special? Is our faith somehow more special?

Wouldn't you rather be paid in something real? You were raised with paper money, but this is a relatively new phenomenon. Silver and gold have been in circulation for millenia.

This is not about accumulating income anymore, it's about protecting what you already have. What good is it to get paid dollars for rent if your dollars are only worth the paper they are printed on? Toilet paper? It appears to be the case, and that average life if ANY fiat currency is about 40 years (if you don't know what that means, I suggest getting educated sooner than later). The NZD and the USD are both fiat currencies. The USD is now 40 years old as a fiat currency, when it broke from the gold guarantee in 1971 under Nixon. This all matters. If you don't think it does, I wish you well in your investments, as you well may be walking dead financially and just don't realize it yet.

A NZD that increases in value means a recession for us at best, as exports slow as our stuff gets more expensive for other countries. That's less cash flowing through our economy, to pay things like rents and mortgages. More families move back with Mum, putting yet another house in the market.

Low interest rate policies are only buying the market time, putting off the day of reckoning, made worse by the delay. The banks will be overly accommodating because they DON'T WANT YOUR PROPERTY, especially after seeing the banks in America stuck with millions of foreclosed houses they can't sell.

I'm not being dogmatic. I'm just sayin because I care. Very few people are paying attention. They said all the same things you said 5 years ago- "gold is a bubble, etc" they said that when gold was $500 an ounce. Yes, it is true that gold has not pierced its record in NZD- yet, but just last week I think it was, it broke it's record in British pounds, and the Euro a few weeks ago. This is worth mentioning. With all the currency gyrations, it's only a matter of time before it breaks through on the NZD and the AUD as well. Do you really think our currency valuations won't go up and down in the future? The only remaining lifeboat, that will automatically adjust in value, is gold and silver. Supply and demand dictates higher prices for "real money" like metals, as others realize the ponzi game of paper currencies is up. Zimbabwe and Argentina are recent examples. Belarus, too, just this year. Overnight their currency revalued at 56% less.

If you don't want to listen to me, and want to listen to someone more mainstream, I suggest "Louise Yamada gold $3000," a prediction she made in 2008 that appears right on track.

I believe that real estate is about to be purged wholesale, dumped onto the market. The signs are all there. A lot of motivated sellers and scared buyers- the few that exist AND qualify. Who can qualify? Who wants to pay more than they are paying in rent on an asset that will stagnate in value? In an uncertain job market? The world has too many problems to inspire confidence in any market right now, except safe havens like precious metal.

The longer you hold your assets in something tied to paper, the longer you risk losing purchasing power as paper becomes worth-less.

As for the "gold confiscation" in the US, people were still allowed to own gold. You have to look at the executive order by FDR. There is a lot more to the story than what's on the surface. Most people took their gold to Canada, I understand.

Hey guys. Well, my wife and I just decided to keep renting a while longer. We are living in the Onehunga area, and would love to stay here. Have a very substantial deposit. I have been sitting on the sideline for years, quietly accumulating a deposit. I have had a really cautious approach to buying, and it has caused quite a bit of friction between myself and my wife at times. But i try to keep my head as much as possible. Anyway, this is my first post, but a few observations about property you may or may not agree with.

1) Kiwis love property. Although I love to paint myself as being sober and uninfected, the fact I have been looking at this site (property) for some time shows that. For somebody who tells himself it is just a commodity to be bought and sold I sure do spend a lot of time talking about it! I do however do a lot of reading on it etc. I am no economist. I have given up talking to your average Kiwi about house price trends v inflation rates, longterm graphs etc. A lot of people quickly fly into a temper, and I find it is almost like trying to question somebody's religious beliefs. For the sake of any sort of serenity I have adopted the policy of letting people criticze (rent is dead money etc) and question me on this, and just smle. Hey, maybe they are right.

My head tells me to wait a few more years before buying - I think that is the rational thing to do. But my heart keeps me looking at the Trademe sites etc!

2) I said to my wife yesterday that it is indeed true that people behave irrationally around property in New Zealand. But irrationality does not always equal unpredictability - not when you are looking at group behaviour.

http://www.gmi.co.nz/pages/news/877/House-Prices-–-Not-Quite-Sober-Yet.aspx

I don't agree with all of Gareth Morgan's politics, but a trend has emerged. What interested me yesterday in my net surfing is the following from http://www.marketsunplugged.com/tag/new-zealand-house-prices/

If you look at the Rodrique graph there is an uncanny resemblance to Gareth's graph. Isn't there something about false second winds (suckers rallies) for sharemarkets?

I tend to agree from what I have seen and heard from Gareth that the NZ market doesn't tend to suddenly fall. The emotional belief that property prices never go down is too strong. Offers etc just peter away over time. People will tend to sit their houses on the market for four or five years if they have to (or perhaps more likely bring them on and off every so often), Inflation eats away at everything, and they miss out on unrealised gains from deposits etc. They still come away feeling like a winner.

3) Prices do fall. My wife and I made an offer on a place last week. First ever. Rejected. But the interesting thing is the agent gave a figure they would accept at. QV tells me it is 5 % below what they paid in December 2007. I still thought the figure was too high.

4) In Auckland from my observations, we seem to be seeing a reverse ripple effect on prices - as described elsewhere, a two-tier market.

The outer suburbs were the first to start lowering, and it has slowly worked its way in (I am talking about your classic three bedroom house here, not your apartments). In Onehunga and One Tree Hill people are still holding out for big prices. I wont pay these prices at the moment.

5) In the One Tree Hill are they are still happily taking things to auction, but in areas further out a lot are being quoted with prices.

6) A lot of the buyers in One Tree Hill/Onehunga are Asian. They are totally knocking new buyers out of the market in the Onehunga/One Tree Hill area at auctions (at least they were in the last ones I attended earlier this year). I say good on them. What I think may be happening in central Auckland may be around

Not wanting to travel longer distances

School zoning for children

A more attractive buslte and feeling of centrality.

My question is though, how much of this buyer interest is based on their current feeling of weatlh? Wht happens if the China economy and real estate market starts to stress. If the central Auckland property is a second or third for them wont they be tempted to dump the property in the same way Kiwis dump their holiday homes when things get tough?

7) Worldwide prices for property are in trouble. I have been to the States and seen what has happend there. Can we really be that different?

Anway some thoughts

You make some great points. Values always fall in the outer suburbs first, then move their way in. In the final stages of a Slump, the higher-end properties fall in value.

I don't believe we have seen the last of the falls in value in Auckland yet. Low interest rates have saved a lot of people but how long can this last for? All it will take is a fall in commodity values to trigger a fall in the Kiwi dollar, then the true inflation present in the economy will show up and the Reserve Bank will be forced to start raising rates to counter.

NZ has been somewhat shielded through the GFC by unsually high commodity prices - we are lucky in that regard.

I would say that as an investor rental yields just don't work at the moment, until values fall a bit more or rents rise a bit more. As a home-buyer, if the difference is not too much from what you pay in rent, then what's the harm in putting in a few cheeky offers in, at much less than the asking price? If they don't accept, then keep renting and saving, if they do, then you've got a great bargain. Win-win either way, and you'll help the rest of us out by lowering sellers' expectations!

Excellent first post, and yes, you should be concerned. To console your wife, I recommend buying her a good "new" (used) car. I have seen several people get worked up into buying something that they really want, only to later discover that it is more expensive than they realized. What once was considered "our home" soons gets shattered by the bank knocking on the door. A house is a BET that: 1) interest rates will not rise and crash the value of your house 2) interest rates will be PREDICTABLE 3) Jobs will be there and be plentiful, especially YOUR job, and God forbid, your Partner's job if you need both to pay the mortgage 4) If you need your Partner's income to make your mortgage payment, you are already over your head 5) If my tea leaves are correct, a lot of the so-called "homeowners" who have purchased in recent years, will soon be HOMELESS, BANKRUPTED, and LIVING WITH MUM 6) This esepcially applies to "landlords" with "house plus a rental property" that doesn't cover it's own expenses 7) What happens in the US affects EVERYBODY 8) the China miracle is already slowing 8) We are completely dependent on what happens in Oz, who is dependent on the China miracle/mirage 9) There are too many uncertainties in the market to make for a continuing bull market, and prices NEVER go sideways for long, only UP or DOWN 9) We will all learn soon enough 10) The graph you attached is perfect. I posted it here a year ago, and this site did a story about it soon after. It completely describes the PREDICTABLE nature of humans in a market.

Your comment about people feeling like you were attacking their religion was SPOT ON. Good job. I think your wife will be thanking you in years to come. If you bought some gold or silver, she might be thanking you more.

Currency devaluation is the bigger conern for everybody. Food and fuel will continue to go up, because governments are printing money, and so where is the cash going to come from to pay for all these mortgage payments? Since wages aren't going up, while unemployment is? THIS IS A VERY SICK MARKET.

You are correct in your observation that the prices are going down in the outskirts first. Auckland does not mirror the broader market.

I say that making ANY offers on a house is a BAD IDEA at this stage. I suggest looking 2 years from now, AFTER the US Presidential election. You should have a good idea of what the market is doing, and could grab a bargain. If you can't keep your wife calm for that long, I suggest assuring her that you will start looking after the Rugby World cup is over. If you were smart, I think you should, at the very least, wait until AFTER the spring selling season is over, because with the law change affecting rental property income, I believe we are going to see a surge of property for sale this year, much more than other years. This will be the burst of the bubble.

Another tactic- find out what your wife REALLY wants to do with the house you are hoping to buy. I know that ladies have a desire to nest. Something you can do, to have your cake and eat it too, is to rent your next house but with at twist, only rent from someone who will give you an option to buy the house, in writing, and will allow you to make changes to the house the way you see fit. Those types of landlords are out there- those that are unsure if they should rent it out or just sell it. It might take a bit of looking, but so does looking for any house you might buy. No hurry. You can take the time to find the right situation. You might be surprised at what you find, if you take the time and put notice out to all the rental agents what you are looking for. Where I am in the BOP, nicer and nicer homes are coming for rent for less money than we paid a year ago, and for way less than if we actually bought it. We are in no hurry. Qualified applicants, who can actually pay their rent on time, are becoming more and more scarce around here.

Where is the catalyst for CONTINUED housing price increases that is NOT a temporary catalyst. Everything I see is temporary boosts, but nothing to establish a SOUND trend.

Most houses in NZ are built to poor standards anyway. I reckon that a lot of old stock will simply be torn down when the next boom begins...about 20 years from now. Better to rent a 2005 or newer, well-insulated house, and invest your mortgage payment savings, energy savings, and house maintenance savings elsewhere.

I like the idea of only making one call if I have any problem with the house- to the landlord- it's his problem. I've "owned" 5 homes. I've had enough for 3 lifetimes, as far as I'm concerned. No hurry to make a long term decision on something that I know, on average, people stay in for 5 years or less. We certainly proved that statistic! 5 homes in less than 10 years! I try not to think of all the savings had we rented instead.

aucklandbuyer is Happy Renter. Strange and sad.

No. Not related. Similar observations but not related.

A snowball is going to start rolling down hill starting about now. Aucklandbuyer is just the first the exit, before it gets overcrowded, because he seems to be watching human behavior with a bit of objectivity...something hard to find these days.

Had to laugh over this. Guess nothing I can say will convince our friend that Happy Renter and I are not one and the same. We would have to disagree about something perhaps!

When too many people agree on the same thing, it's best to head for the exit. We "exit-ers" are early, but won't be alone for long. I know that a lot of property owners are looking at their books, scratching their heads, looking at their books, looking at their partner, scratching their head again, etc. It translates into uncertainty, which is not good for any market. Nothing has been fixed from 2008, and that's a real problems.

Our high dollar adds another wrinkle to problems for real estate. How much less tourism do you think will happen as a result? That was the #1 source of income until just recent. Now our #1 source is becoming expensive because of the high NZD. This bodes poorly for NZ cash flow.

Leaky homes are another uncertainty, which also will drag on recovery.

Hoping someone here may be able to asist me...

I have an ongoing arrangement with one of the major trading banks on nearly $25 million of residential loans that qualifies me to borrow at cost of funds plus 85 basis points. The question is how do you calculate the cost of funds...?? Can anyone provide a method by which this can be accurately calculated? I appreciate it is likely to be slightly different for all banks based on where their funding is sourced, but is there an approximate table or transparent process (similar to converting celius into farenheit) that can be relied on? Cheers Ryan

Ask what index they are using to calculate their "cost of funds." That should be in the paperwork. If the cost of funds is not clearly stated in the documents, then you simply ask them where it is and how it is calculated. They are required to disclose it.

85 homebuilders bankrupt this month alone in Aussie http://www.smartcompany.com.au/construction-and-engineering/20110804-ei…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.