By John Mauldin*

“The world’s biggest problems are the world’s biggest business opportunities.”

– Peter Diamandis

One pill makes you larger

And one pill makes you small

And the ones that mother gives you

Don't do anything at all

Go ask Alice When she's ten feet tall

When logic and proportion

Have fallen sloppy dead

And the White Knight is talking backwards

And the Red Queen's off with her head

Remember what the dormouse said

Feed your head

Feed your head

– “White Rabbit,” Jefferson Airplane, 1967 (The link is to Gracie Slick at Woodstock, 1969)

Will they or won’t they? This week the Federal Reserve might raise interest rates. Many of Wall Street’s worker bees have never seen a rate hike. They were still in school (or skipping school) when the Fed last tightened in 2006.

As readers know, I believe the Federal Open Market Committee should hike rates ASAP. A number of very astute analysts and Fed observers agree with me. On the other hand, an equal-sized army of similarly smart analysts think they should not. It seems to me this recovery is getting long in the tooth. The Fed needs to give itself some room to stimulate when the economy turns down again. As it stands now, their only weapons are to take interest rates negative or to resume quantitative easing. We don’t want either of those.

Further, I don’t think there is any question about the potential for malinvestment and distorted economics at the zero bound.

What I think matters much less than what the FOMC’s voting members think, of course. Their public statements mostly seem dovish, but the voters always leave themselves plenty of wiggle room. If you are confused, don’t feel alone. Larry Meyer, former Fed governor and as close as there is to an insider on Fed policy, is pretty well split between a “lift-off” in September or one in December. I was reminded by Bob McTeer, former Dallas Fed president, when we did a panel together this week, that if they raise rates to 0.25%, the effective rate will be much less for this first round.

If they don’t hike rates, the reason may be that they don’t see the kind of inflation that tighter policy is supposed to stop. Specifically, the Fed sees upward wage pressure as a key indicator that inflation is taking hold. Hence the recent obsession with all manner of wage and income statistics.

Even if the Fed sees enough inflation to raise rates, I don’t think the cycle will last long. And thus we come to this week’s topic. I am asked all the time whether I think we will see inflation or deflation in our future. Most of the time the people asking the question are looking out 6 to 18 months. Today I’m going to answer that question, but we’re going to look out 5 and then 20 years.

We now live in a world of relentless deflationary pressure. Very large forces are behind this, and I don’t believe it will change. If anything, the trend will strengthen.

That is not to say a determined central bank cannot create inflation. But just as Paul Volcker and then Alan Greenspan had to fight a general tendency toward inflation, which brought us to a period of disinflation, the Fed and other central banks in the developed world will be dealing with a deflationary tendency.

The Fed’s statutory mandate isn’t simply to stop inflation; its charge is to maintain price stability. Inflation is not price stability, but neither is deflation. The Fed is supposed to keep both at bay.

Volcker, who stamped out the 1970s inflation cycle with aggressive rate hikes, would be bored out of his skull if he were leading the Federal Reserve today. No one needs his inflation-busting skills. In fact, it would take a major policy error on the part of the Federal Reserve before we would ever need him again. In the coming years, though, we may well need an inverse Volcker.

Is Deflation Really So Bad?

Today most people accept inflation, even if they don’t like it. We think of it as background noise. Inflation is always there, more or less, so we make adjustments and then tune it out. Life under deflation is not at all like life under inflation, and most of us lack the analytical framework to deal with deflation. It doesn’t compute. Financial analysts who can make inflation adjustments in their sleep have no idea how to adjust their models to reflect deflationary risk. They had better learn. We need to stop right here and recognize that what I’m going to be talking about today is price deflation. That is a different animal than monetary deflation. One we like; the other we don’t.

Deflation doesn’t sound so bad if you think of it as an environment of generally falling prices. Everyone loves a bargain. The problem is that your salary is simply the price at which you sell your labor. That price can fall, too. If the price of your labor falls faster than the prices of everything you buy, you can find yourself in deep trouble very quickly. Think that can’t happen? Ask the Greeks. Or any of your neighbors who lost their jobs in the Great Recession and subsequently took jobs at lower wages. Deflation at work.

Deflation also isn’t fun if you’re in debt. If prices are generally falling, you have to repay your debts with dollars that buy more than when you first borrowed the money. Just as inflation is the debtor’s best friend, deflation is the debtor’s worst nightmare.

Deflation would be as “normal,” as we currently perceive inflation to be, if we had a fixed money supply. Each currency unit (gold or anything else) would naturally buy more as people produced more goods and more offspring. Bitcoin will be massively deflationary if it ever gets off the ground. In fact, that is one of my major criticisms of Bitcoin. It carries the same deflationary weakness as gold does for a modern world. It heavily favors incumbents and the rich. A properly structured and managed electronic currency – Milton Friedman’s computer running the central bank –would be truly neutral.

Now, of course, we don’t have a fixed money supply; we have a very dynamic money supply. We have central banks continually trying to exert influence, almost always in favor of their home countries to the potential detriment of the rest of the world. Consumers have influence as well through their spending and saving decisions.

Most of the world’s central banks are now trying to inflate and debase their currencies, while most of the world’s consumers are unwittingly stoking deflation. I feel very confident consumers will win this standoff, but when and how they will win are open questions.

Ultimately, we are going to have our cake and then be forced to eat it. We’ll get the low prices we want and demand, and we’ll get the consequences as well.

Good and Bad Deflation

My first economics mentor, Dr. Gary North, drilled it into my head that ever-lower prices are the natural result of a market economy. As people learn to produce more with fewer resources, competition, especially in the form of Schumpeter’s creative destruction, forces prices downward. In a truly free and competitive market, it is only the debasement of the currency that allows the conditions for prices to rise. All things being equal, if the price of something is not falling over time, it raises my suspicions about competitiveness. Think OPEC in the latter part of the last century. OPEC nations are losing their control today as the rest of the world, and especially the United States, becomes more competitive in the production of oil. While it took a long time, the cure for high energy prices was high prices. An enormous amount of money was invested, not just in the search for oil but also for lower-cost ways to produce it.

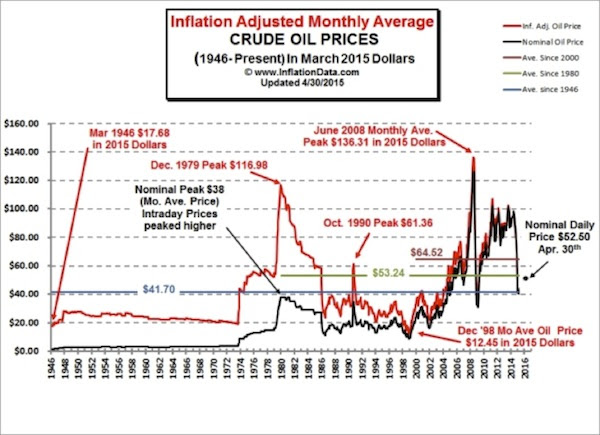

As an aside, the current price of oil, even though it is 10 times higher than it was before OPEC was formed, is only a little bit above its inflation-adjusted long-term average. Look at the chart below. The red line shows oil prices adjusted for inflation in March 2015 dollars. The black line indicates the nominal price (in other words the price you would have actually paid at the time). The price as of April 30, 2015, is US$52.50 a barrel, down significantly from recent highs but still above the average inflation-adjusted price of US$41.70 for the period from 1946 to 2015. It’s a little hard to see, but the red line showing inflation-adjusted prices has dropped right along with the black nominal-price line. With oil currently in the mid-40s, we are almost exactly at the long-term inflation-adjusted average of the past 69 years – and certainly lower than the last seven or eight years.

Gary Shilling wrote the book on deflation, literally called Deflation. It was written in 1999; and if you want more information on the topic, I would recommend that you read his later book, The Age of Deleveraging, Updated Edition: Investment Strategies for a Decade of Slow Growth and Deflation.

What Gary shows us is that, other than for nations in debt, deflation is not only a natural state but is something to be desired. There have been periods of “good deflation” throughout history. The “bad deflation” that we especially associate with the 1930s comes from the twin evils of too much debt and leverage plus monetary policy mistakes. The bursting of a debt bubble always and everywhere produces “bad deflation.” Bad deflation is monetary deflation, and it is devoutly to be avoided. When economists and central bankers talk about their worries over deflation, they are referring to monetary deflation, not price deflation. Just for the record, I concur with their worries.

But the Fed’s method of avoiding monetary deflation does not address the central problem that is created by our government and banking system: too much leverage accumulating in a system without adequate systemic safeguards. Flooding the system with liquidity after a leveraged-induced credit crisis and subsequent monetary deflation is like closing the barn after the horses are in the north 40. As Irving Fisher, one of the greatest economists of the Depression era, wrote to Franklin Roosevelt late in his life, reflecting upon the lessons he had learned over the previous 30 years, the only way to truly prevent another Great Depression is to control debt leverage and the level of fractional reserve banking.

The combined policies of the Federal Reserve and the government helped reduce the effects of the Great Recession, but it was also their policies that helped create the conditions for the collapse. Applauding the Federal Reserve is a little bit like cheering for the arsonist who helps put out the fire.

But today I’m talking primarily about price deflation. I’m in the process of writing a book called Investing in an Age of Transformation. I’ve been thinking about this topic for ten years, and now it’s time to write. I am continually staggered by the implications of the technological and sociological transformations that are in front of us. One of the implications is that things are just going to get less expensive. For most areas of the economy that change will generally come slowly, but there are going to be some truly disruptive transitions that lower costs dramatically in relatively short periods of time.

Fast & Easy Healthcare Disruption

The most important economic phenomenon of our time is rising productivity. The amount of value each human worker can produce went parabolic in the last fifty years – and mostly in the last ten years – even though recent gains are not showing up in current statistics, because the tools we’re using to measure productivity measure dollar outcomes, not lifestyle outcomes.

Productivity would be growing faster still if not for outside interference, mainly from government, but even the bureaucracy can’t hold back the forces of innovation. At worst, government regulations can only temporarily redirect progress.

My friend Peter Diamandis of XPRIZE, who was our keynote speaker at this year’s Strategic Investment Conference, had a great story last week on several industries ripe for disruption. We are going to focus on two. Both illustrate the unstoppable deflationary wave that is coming. The first one is healthcare. -

Healthcare is so massively broken that its disruption will come easy and happen fast. Hundreds of startups are working to make you the “CEO of your own health” – to augment (or replace) doctors and hospitals.

I expect new AI-enabled healthcare options to be free or near-free, and so much better that people will forgo traditional medical care in favor of these superior options. This will cause today’s healthcare system to crater.

Think libraries in an age of Google… Think traditional wired landlines in an age of mobile telephony… Think taxis in an age of Uber… Think long-distance in an age of Skype… the list goes on.

So what’s coming?

The $10M Qualcomm Tricorder XPRIZE will give birth to devices (i.e. the Star Trek Tricorder) that allow you, the consumer, to self-diagnose, anytime, anywhere.

Sick of going to the hospital? Companies like Walgreens and CVS are working to become your healthcare center.

You may have noticed the small clinics popping up in pharmacies and supermarkets. Usually staffed by a nurse practitioner or physician’s assistant, they offer basic primary care services, vaccinations, etc. They are open evenings and weekends, and their prices are lower. And most of the time, for most of us, especially those of us with children, basic primary care is what we need. Seriously, after raising seven kids I can pretty much figure out when one of my kids has the flu and know what to do about it. A US$100 office visit plus the restructuring of my entire day (at God knows what cost) is not productive.

Patients love these places because they’re convenient. Insurers love them because they are inexpensive. Drug companies love them because they write prescriptions. The stores in which they reside love them because they bring traffic. Does anyone lose from this?

Yes, someone loses: the primary-care physicians’ offices and emergency rooms that used to handle these patients. Those places are intentionally overstaffed and over-resourced because they must handle major emergencies with no notice. We’re all glad they are there when we need them, but having them on call is extremely expensive.

Think of all the people who work in a typical doctor’s office, plus all the people who build and supply it. Multiply that amount several times over for even a small hospital’s emergency department. A big chunk of their revenue will shift to these store-based clinics over the next few years. And then they will be able to focus on emergency care and more medically intensive needs.

The clinics will themselves get more efficient. Eventually it will be technologically practical for the practitioner you see to be an AI-driven “robot” (perhaps with assistance from a technician), backed up by a human physician on the other side of the globe who can examine you by remote control. We’ll dispense with the dispensaries completely when someone invents the medical tricorder that XPRIZE seeks.

This isn’t a dream; all of it is already in development. Some of the technology is available right now, but local laws restrict its use. That will change as legislatures grow increasingly frustrated with healthcare costs.

Economically, these are productivity-driven deflationary changes. The healthcare industry will deliver more healthcare with fewer human workers. The displaced workers will have to find other occupations.

Note: this shift will actually lower GDP. That’s is because we’ll spend fewer dollars for healthcare, and it is the spending of dollars that we measure for GDP. The fact that our healthcare will be immeasurably better for the dollars spent doesn’t factor into GDP. I know I keep beating this drum, but dollar-focused GDP is going to become an increasingly unreliable way to measure the well-being and growth of the economy.

Insurance Wants to Be Free

Diamandis says your friendly neighborhood insurance agent is a potential disruptee, too.

Let’s say that I have a genome relatively free of major disease, I don’t smoke, I eat healthy and I work out every day.

Let’s also say that I publish this information (validated by my sensors) to my social graph and say, “Hey, anyone else with good genes, healthy eating and workout habits who wants to self-insure along with me, let’s do it… We’re a low-risk partnership!”

If this was to happen, and the top 10% of the insurance pool pulled themselves out of the marketplace, this would crush the economics of the industry.

Up until now, this kind of knowledge and “peer-to-peer insurance” would never have been possible. It is now.

“Hold it,” you say… “There’s regulation that will stop you.” Yes, sure, there is, for the moment. But just like Uber versus the taxi industry, regulation can only be a stumbling block for so long.

Newt Gingrich calls the bureaucracy and entrenched crony capitalists the “prison guards of the past.” None of them want to give up their favored positions to some new upstart competition. The ubiquitous yellow cabs want to continue to provide inferior service at higher prices. Everybody is all for change except in their own world, where they only want change for the better, not change that actually forces them to do something uncomfortably different. They band together to form lobbying groups to try and create legislation to hinder or prevent competition.

Insurance is all about probabilities and risk pooling. It has been a great business for decades because insurers have better information collection and analysis tools. But, as Google’s founders like to say, “Information wants to be free.”

Peter’s self-insurance scenario is completely feasible. Insurers make their profits from the people who never file claims. The industry’s economic basis evaporates if those people can identify themselves and leave to form their own risk pool.

The insurance industry will survive but will have to change dramatically. Rates will fall as customers gain the ability to gauge their own risk and compare rates between insurers. The large profit margins now common for large policies will shrink.

This change will be very deflationary. The armies of insurers now deployed for sales, claims, and policy service will shrink, replaced by AI-driven systems and a smaller number of very productive humans.

As I have written before, the price of energy is coming down, not because we are finding more oil and gas but because the energy sector is now driven by Moore’s Law and technology every bit as much as the computer world is. The continued reduction in the cost of solar energy is truly astounding. The shift to solar and other forms of “digital energy” will not only be revolutionary in terms of price but will create entire new industries and jobs.

I will have one entire section in the book on the revolution that is taking place in agriculture. Not only are we producing more bushels (of corn, soybeans, wheat, rice, etc.) per acre, we are reducing the associated labor costs. Ten years ago less than 1% of the grapes grown for raisins were mechanically harvested. Today the figure is over 40% and rapidly rising.

I’ve mentioned in the past a robot that can take over the backbreaking manual labor of thinning out lettuce shoots. This robot will do in three hours what it takes 50 people three days to do. And do a better job.

I read yesterday that the Japanese, not to be outdone by California inventors, have created an entire “lettuce factory.” Literally everything involved in growing lettuce is done inside a large warehouse, with the exception of one process that requires human eyes. The business model seems to be to sell lettuce factories. Have a large, empty warehouse near you that you want to put to some use? Buy a lettuce factory and install it. By the way, lettuce production is a multibillion-dollar business. And depending on which source you read, anywhere from 20 to 30% of lettuce is damaged and rendered unusable before it actually gets into the consumer’s hands.

We’ve all been to Disney World, where we’ve taken the little tram ride through Tomorrowland. There we see the pictures of huge agricultural robots harvesting nondescript products. I assume it is still there, since it didn’t change at all during the 25 years I was taking my kids. We get to where we roll our eyes and say “Yeah, sure.” But that age of mechanization and lower costs is happening right now.

Manufacturing is going to end up being much closer to the actual consumer, which is going to reduce transportation costs. Transportation costs are going to go down because trucks and other services will be automated. I could go on and on.

(Just to head off the comments: yes, this does throw a wrench in our traditional ideas of what work is, and we are going to have to adjust. A significant portion of my book will be about the future of work. If you don’t like to change, you’re probably not going to like that chapter.)

A World of Abundance

As you can see, deflation won’t be all bad. If you have a few bucks, you will get far more bang from them than you can now. The problem will lie in acquiring more bucks. In all likelihood, whatever it is you have to sell will also compete with disruptive technologies.

We’ve been here before. New technologies have been disrupting established industry at least since the onset of the Industrial Revolution. The steam engine, cotton gin, railroads, electric lighting, automobile, and other inventions all put people out of work. But they also created new jobs and opportunities for people who were willing to adjust.

The difference now is that the innovation cycle has speeded up. The original iPhone was revolutionary in 2007. Now, just eight years later, it looks laughably primitive. You can’t even begin to compare it to the iPhone 6S that Apple unveiled last week.

The same thing is happening, though often less conspicuously, in practically every industry. We are finding ways to accomplish what we want faster, better, and cheaper. This trend will continue and even accelerate.

Now for the economic question. How can price inflation ever take hold in this world of abundance? When every possible product and service has multiple competitors nipping at its heels, who has pricing power?

I just mentioned one answer. Apple can sell as many iPhones as it can manufacture at handsome profit margins. Such products are getting scarcer every year. But Apple too has competition, even in China, where several local smartphone makers undercut the iPhone on price with arguably better quality.

Further, there are sociological factors that are inherently deflationary, especially in the developed world. The simple fact is that developed-world populations are getting older and not growing. Old age is deflationary. We seniors tend to consume less, and a lot of what younger generations are buying we already have and don’t need more of. Even with the massive amounts of printing that the Bank of Japan is doing, Japan has not seen any significant rise in inflation, because the deflationary forces in the country are just massively strong. That is the future for most countries in the developed world.

On a conference call for investors yesterday I was asked what I thought was the most potentially disruptive thing going on today, and my answer was the huge wave of immigration into Europe from the Middle East. I watched a video in which young male refugees refused to take water from the Red Cross because the water came from “infidels.” As if the whole continent of Europe they want to live in were not populated by “infidels.” What made me smile was that the young girls and women walked right past them, looking at them as if they were crazy, and took as much water and relief food as they could possibly hold in their arms. Truly, I don’t know how the immigration wave is going to work out, sociologically.

But I do know that strictly from an economic standpoint, if you can neutralize the religious animosity, most European countries will be better off with a significant amount of immigration to offset the reduction in their populations. They need workers and especially young workers.

At a certain point, debt becomes deflationary; and it is hard to argue that most places in the developed world do not have too much debt. Reducing that debt to more workable levels is inherently deflationary.

I could (and will in the book and in later letters) talk about other price-deflationary forces that are loose in the world. This kind of deflation is generally a good thing, as wages are typically “sticky”: employers don’t generally come to their employees and say, “We’re in a period of deflation, so we’re going to cut your salary along with the prices we’ve been charging.” We can expect that raises will be smaller and less frequent, though.

Increased productivity, shifting demographics, and too much debt all point to a growing deflationary environment. Given this, is inflation possible anymore? Set aside whatever might happen in banana republics. In the developed world, is there any chance we will ever again see the kind of long-term, embedded inflation that Paul Volcker stamped out in the 1980s?

The answer to that question has big implications for monetary policy. The short answer is that inflation is possible, but it would take a massive monetary mistake in order for it to happen. I can foresee inflation getting to the 4–5% level before the Fed or the ECB turns off the spigot. (The discussions I’ve had with many high-level economists indicate to me that they would favor an environment of 4% inflation until the debt overhang became more manageable. Only a few of them will publicly say that, but that is why you’re not seeing a great deal of alarm as inflation approaches 2%.)

Do I think we will see a return to the ’70s? I don’t think any central bankers want that to happen on their watch, and they will lean against inflation if it ever arises.

Fed Should Reload and Rebuild

Here’s another question. If we have finally arrived at a period of generally restrained inflation, what does that mean for interest rates?

An interest rate is simply the price of money. It reflects anticipated risks, one of which is potential inflation. No significant inflation risk means we should be able to borrow money with little or no inflation premium built into the interest rate.

On the flip side, lenders (i.e. bond buyers and bank depositors) won’t be able to demand higher rates as compensation for taking on inflation risk.

So if we are entering an era of general disinflation or outright deflation, we’re probably also entering an era of generally lower interest rates. And I think that period could last for a very long time. Yes, short-term rates might eventually climb up to 2–3%, but I doubt we will ever see 5% short-term rates, absent some kind of swelling debt bubble, which, again, would be caused by a policy error.

This is the backdrop as the FOMC meets to decide its next move. Frankly, nothing they do will surprise me. I wrote last week that I understand both sides in the debate.

I do not think the economy is overheating by any stretch. The main reason I think the Fed should act is simply to reload the bazooka. I want them to have ammunition if some exogenous shock hits us.

I think a gradual ramp-up to 2% in the federal funds rate would serve this purpose, and maybe it would bring to an end some of the current liquidity-driven bubble behavior, too. Whether the Fed starts now or in December is a minor issue, but I see no reason to wait. Just do it. Just for the record, when I say a gradual ramp-up, I mean let’s take a couple years to get to the destination. I would prefer to see one-eighth of a point per meeting for two years with the ability to stop at any time if the economy begins to seriously slow down.

Now, there is, however, another issue. The International Monetary Fund and the World Bank are frantically sending the Fed smoke signals concerning emerging markets. World Bank Chief Economist Kaushik Basu told the Financial Times on Sept. 9 that he is very concerned about the impact of a Fed lift-off in combination with China’s currency change.

“The world economy is looking so troubled that if the US goes in for a very quick move in the middle of this, I feel it is going to affect countries quite badly,” Basu said. He’s right to be concerned. Higher US rates will tend to strengthen the dollar, which in turn will be hard on other countries that have issued dollar-denominated debt. And by the way, a rising dollar is inherently deflationary to the US as well.

On the other hand, no one at the Fed wants to lift rates straight to 5%. No one is even remotely thinking about 5%. They are bending over backwards to act gradually. Any emerging markets that are so fragile that a quarter-point US rate hike will crush them are probably due to collapse anyway. At worst, Fed action will just speed up the process.

Given the way the world is going, central banks everywhere should really stop worrying about inflation. They are like generals fighting the last war – preparing for something that will never happen again and missing the new, emerging threat.

Monetary deflation is that new threat. The danger is that the Fed will look at price deflation and interpret it as monetary deflation. Price deflation is ubiquitous and ongoing and a good thing. I don’t want to fight falling prices of the goods and services I buy. I can say, only half humorously, that I want only the prices of goods and services that I produce or have already paid for to rise. The Fed, the ECB, and the BOJ are all trying to figure out how to stop good deflation. So far, their only innovations are quantitative easing and negative interest rates, which were designed to deal with liquidity needs and the overhang of the debt crisis. And while the liquidity injections have helped to calm markets, research by Federal Reserve economists has pretty well established that QE has not been very effective. But it certainly did disrupt markets throughout the world. Now, investors generally aren’t upset when the disruption of markets means the prices of their stocks go up, but if those price increases are artificially induced rather than market-driven, are they really going to be helpful to the economy in the long run?

Paul Volcker knew how to stamp out inflation. To do so was painful but not complicated. Stopping monetary deflation is an order of magnitude harder. Waiting to confront it will only make the job harder.

----------------------

* This article comes from Thoughts from the Frontline, John Mauldin's free weekly investment and economic newsletter. It first appeared here and is used by interest.co.nz with permission.

12 Comments

I would like to raise the following points

It is laughable that educated people say silly things like "We need to raise rates so we can have room to move when the next recession arives" hahahaha That is like saying "I have a hole in the bottom of my boat letting the water in so i will make another hole in the bottom to let the water out"

Greece is not a deflationary problem it is a debt problem. That is to say falling prices did not cause their problem - borrowing money thet could not repay caused their problem.

I will comment further when i have finished reading

You say

Deflation also isn’t fun if you’re in debt

But the opposite is also true

Debt also isn't fun if you're in Inflation (interest rates rise and you cant pay)

The pain is asymmetrical however. With deflation the capital you owe is worth more, plus the interest, plus in such an environment unemployment can be quite high.

Bad deflation is monetary deflation

Could'nt agree more

This is getting really interesting - Thanx

"Increased productivity, shifting demographics, and too much debt all point to a growing deflationary environment."

Could it be that demographics is a result of deflation, not a cause as Maudlin believes. He builds a very good case for inflation because of increased productivity, but then says we will have deflation.

No mention of the limits to growth, or the problems caused by economics that believe in exponential growth of finite resources. I don't think the future will be as Mr Maudling believes, good to see an article of this nature though.

The article points to

Product deflation which is unstoppable

And

Monitary Inflation / Deflation

You have to consider both separately

Product deflation? as in the product gets more efficient/effective? Probably fairly minor as an effect. It also assumes ever improving technology which usually results in energy consumption in the making and even use.

The economy has never turned up, ergo you cannot raise rates. Just check out the countries that tried to.

Very thought provoking

It would have been good if you had coverd the future of banking rather than the future of Health as banking is in for big changes. Peer to peer lending and digital curency options as examples.

I believe that the national curency should remain relatively stable (not used for Fractional reserve banking etc) And banks should be allowed to issue their own currency and compete with each other.

The fate of Fiat currency is the next big issue i believe will come under tremendouse pressure. This is starting to be shown now with calls for "Big Kahunda" and minimum wages etc.

I believe your book must cover the future of banking, Fiat currencies the Petrodollar and Globalisation.

A TPP could give Corporate control and block the future you talk about.

A good article. The particular form of QE that has been undertaken does seem to have been a huge sledge hammer smashing the wrong nut for the most part, with some unfortunate consequences.

Ambrose is here explaining how the next version of QE, if required, should be very different.

http://www.telegraph.co.uk/finance/economics/11869701/Jeremy-Corbyns-QE…

He explains how it should be controlled by independent central bankers. He doesn't mention that instead of tens of trillions of printing, it would need maybe one twentieth of that, assuming say a general expectation of return on capital of 5%. His version would lead directly to consumption or infrastructure spending, rather than the circuitous pumping of asset prices that may or may not lead to a fraction of those asset values being spent on consumption or investment.

The world will likely need some measures now to get out of the US dollar debts hanging around, and the asset price distortions caused over the last few years. Whether that is allowing some inflation to get average wages back to reasonable fractions of house prices; or whether the asset prices have to drop materially time will tell.

Prices of some things are still going up:

Council Rates, 5% plus

Electricity

Insurance

Auckland houses

University fees

Most Government charges

Parking charges

Parking tickets

Sky TV

Car Repairs

Credit card interest rates

School fees

Medical charges

Used Car imports

Building and handyman supplies,

Professional fees

All things with a captive market

--------------------------

Deflationary items:

Mortgage interest

Food (most)

Clothes (flat)

International Air travel

Provincial housing

Wages (flat)

That Youtube video of Grace Slickof Jefferson Airplane is well worth taking in.

Reputed to be the most psychedelic song ever; actually a dig at hypocrites who decry dope and at the same time force kids to read Alice in Wonderland (which is full of psychotic delusions.Like when the hookah smoking caterpillar has given you the call!!)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.