By Bernard Hickey

The Productivity Commission report into land use for housing used a surprising word this week to describe what was needed to solve Auckland's housing crisis -- credibility.

It essentially said Governments needed to make property investors believe that they would do whatever it took to stop the mad land price inflation that has made Auckland one of the least affordable cities in the world.

Commission Chairman Murray Sherwin introduced the report as a clear set of recommendations for change, but was blunt in saying it would be only as good as the political will behind it.

"The Commission has identified a number of areas where the responsiveness of urban planning could be improved, but the most important step that needs to be taken is a credible commitment to bring land price inflation under control," Mr Sherwin said.

It's not often an official body of policy experts call out their political masters as not believable or credible in the eyes of the public, but that's what the Productivity Commission did this week.

Mr Sherwin was dead right in pointing to the credibility gap driving investor perceptions. No one believes the Government or Auckland Council when they say they are doing plenty to solve Auckland's housing supply crisis.

Investors are showing that every day when they buy houses that cost them money to hold in the short term. That's because they are confident that neither the Council or the Government have the political will or ability to free up the land and build the infrastructure needed to help supply meet demand.

This credibility gap was illustrated earlier in the week with two surveys and the latest sales figures for lifestyle blocks around Auckland.

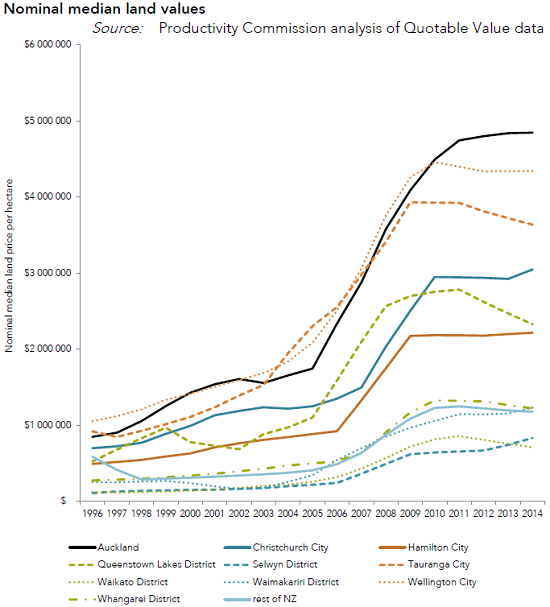

ANZ's annual survey of property investors found landlords in Auckland expect house prices to rise by an average of 8.2% per year over the next five years. That would push up Auckland's median house price another 48% to NZ$1.14 million by 2020, and that's on top of the 83% rise since the beginning of 2009.

These Auckland investors were the most likely to buy again in the next six months, while 84% said the Reserve Bank's LVR changes had not influenced their plans or appetites to borrow and buy more rental properties.

The Property Institute of New Zealand's new quarterly Housing Market Survey of residential valuers, property managers, real estate agents and mortgage brokers found 100% expected further price increases in Auckland over the next six months.

The Real Estate Institute then reported that lifestyle block sales were up 40.5% in the three months to September from a year ago with land bankers driving double digit price growth on the fringes around Auckland. REINZ pointed in particular to the northern fringes of Auckland, "where pockets of lifestyle land are being re-zoned residential and purchasers with long term perspectives are land-banking."

Investors are confident enough that councillors and ministers will never have the political will to open up enough land to build out or relax the densification rules to build up enough to meet the housing demands of an extra one million people expected to be living in Auckland by 2040.

The Productivity Commission made a series of recommendations that could make a difference if these politicians grow a pair to take on the vested interests and NIMBYs who are thrilled with the ever-rising land prices of the last 20 years.

They include:

- encouraging councils to charge targeted rates so those who benefit from new infrastructure for housing and rezoning of land share those windfall gains with councils that pay for that infrastructure;

- allowing councils to toll roads, impose congestion charges and bring in user pays to reduce the painful infrastructure costs that come with growth;

- not imposing very strict debt limits on councils that would stop them borrowing to fund long-term infrastructure;

- encouraging the New Zealand Transport Agency to invest in public transport that would encourage new housing developments;

- encouraging development of Urban Development Authorities with the power to compulsorily acquire land for big new housing developments;

- creating a Central Government 'price trigger' mechanism that would ensure swathes of new greenfields land would opened up if councils allowed the price difference between urban land and rural land on the fringes to grow too large.

- making the Government pay rates on its land in council areas and opening up much more Crown land for housing development.

"A credible commitment to increasing supply to meet demand will encourage landowners holding land in expectation of capital gain to use or release it for development," the Commission pointed out.

Murray Sherwin's description in his foreword of the political drivers for this standoff is the best I've seen and has Auckland written all over it.

"Ratepayers often do not want the higher rates bill and debt levels that accompany more infrastructure expenditure," Sherwin said.

"Homeowners may oppose more development in their neighbourhoods, because of concerns about the impacts on the value and amenity of their homes. Landowners whose properties earn capital gains because of restricted supply may not welcome larger releases of residential land," he said.

"These “insiders” have strong reasons to engage in local political processes to defend their interests, to the detriment of “outsiders”."

Right there is the tragedy of Auckland, and of New Zealand in general. A generation of renting outsiders face decades of being locked in a poverty trap that is only as sustainable as the rent subsidies that are being paid by taxpayers at large. The Government now subsidises 60% of New Zealand's rentals and has to pay over NZ$2 billion a year to landlords because the poorest renters can't earn enough to pay the rents. It is creating a new landed gentry able to help their own kids into homes, but who are surrounded by the working and non-working poor and young who will never own their own homes.

Meanwhile, NIMBYs and land-bankers are more than happy to play their political and legal games to keep the capital gains flowing by blocking new housing developments.

All it would take to bridge this credibility gap is for our politicians to take on these vested interests in the service of the wider public at large over the long term by adopting these recommendations.

But do they have the cojones to do it?

------

A version of this article first appeared in the Herald on Sunday. It is here with permission.

23 Comments

Just shows that property investors aren't the sharpest tools in the shed. Probably would be better investing in some mathematics tuition.

You are right X they are generally not the sharpest tools in the shed. In my 30 years of work where I saw many of them in action they were generally tradies or in jobs such as teaching,police or nursing. They did not earn much so needed housing to build the nest egg. Generally professionals who earn more do not resort to rental housing for investment. They put their excess earnings into equities, commercial investments or managed funds.There are exceptions to the above. I would rather watch paint dry than own housing. Before the boom it had low returns as it was low risk. Hardly intellectually challenging.

It's not right saying that they aren't the sharpest tools in the shed, most of them have done well and we also remember that as you stated above, these are all working class people. They don't earn a heap but have put their money towards something they can touch and feel as a nest egg. When you say "professionals who earn more" who are these professionals and what do they earn? If these professionals are using chunks of money from their savings and not from bank lending then you need to compare apples with apples....I wish the bank would give me a million dollars to use in the sharemarket - my greatest returns are from there but they won't, instead they will give me that lending to buy property and to top it off the Govt gives me a helping hand with tax advantages. The issue we have is the bias towards property. I am not an old investor, I am 30 and may have a whole lot to learn. What I do know in this short time is that I want assets, be it property, shares or businesses but the tax system favors one over the other and Banks won't give me the $ based on "certain" risks. Comparing apples with apples, if you are a middle income earner TODAY what would you do if you want to accumulate wealth in the next 20 years? Most people on here who are well off will suggest other investments because they already have their next egg, but average earning people will invest in property because banks and tax systems allow it.

They aren't the sharpest tools in the shed because they collectively believe they are going to see 8% gains per annum over the next five years.

I'm not sure what magic tree they expect the debt serviceability to support that to appear on, but those of us that can work a calculator would call it delusional. Heaven forbid if interest rates rise during that time.

They may be sharper than you think. The way our monetary and banking system works means that banks will increase the money supply to infinity if the banks' lending criteria are met, and there is demand for the money. If mortgage rates are ~6%, and average rental yields are ~3% (my understanding current Auckland figures are around those levels), then someone with 50% equity can meet their interest costs with rent. If house values increase 8% in a year, then they can also increase their house portfolio by a 12th every year and still be at 50% equity, more than meeting any bank lending criteria.

An economy with this sort of monetary system, and any kind of housing shortage, will also increase rents by more than inflation. As such there is a very strong floor under house prices, and a natural exponential concentration of ownership in the hands of the already large property owners.

It is only if you look at house to income multiples that things look unsustainable. It is not clear that the house market works to that multiple now, if it ever did.

It's true that if interest rates went up 2-3% then the model would suddenly be under some stress. But that outcome looks sufficiently unlikely to be a reasonable bet against. And even then most property owners have a ready made escape valve. Sell some into a high demand market.

It's also true that if supply of housing suddenly became a lot higher, then the market values may finally decline. But it is a pretty good bet that NIMBY politics will stop that also.

So, it all does need some bold political leadership to fix the problem. Does anyone think we have that?

They have done well by accident. No one could predict what happened in Auckland as a result of immigration. Housing has traditionally been the low risk investment. No brains needed. Just borrow and buy something. Not that exciting. Boring compared to studying equities , buying them and watching them grow in value. No tenants, costs and easy to on sell. Admittedly you need some capital to buy equities so smart people with real earning power generally buy them.

The problem with "by accident" or "by luck" is that people can internalize outcomes as a product of their good judgement. Hence, you find the same truths spoken about property across a large number of people. How often have you ever heard a property investor talk about luck in their investment? People who open themselves up to the element of luck or "un-luck" are typically the more honest people to engage.

Thank you Bernard.

I agree completely re the lack of political will. Also agree that NZ needs a creditable response to the housing crisis addressing the broad front of issues. Infrastructure provision, new planning rules allowing cities to be built up and out, tax changes to discourage speculation and encourage the best use of land, reform of rentals to provide more stability for tenants, immigration and foreign investment reform and so on.

On the political front it is worth consider the issue of land value taxes. There is a consensus amongst economic experts that land value taxes are efficient taxes that do not have as much deadweight losses as other taxes and would encourage the best use of the land i.e. discourage land banking. This has been well publicised for at least five years, with for example an article by respected academic and international economics expert of 40 years’ experience -Neville Bennett a long time editor of the NBR, where he concluded in 2009. http://www.interest.co.nz/news/44914/opinion-merits-land-value-tax-less…

"It is inefficient and inequitable to avoid taxing land. Land taxes are avoided, however, by political systems which have a large landed interest.

In the UK it was sought by the liberal party, with powerful advocates like Lloyd George and Winston Churchill, but would never have passed through the self-interested House of Lords."

A helpful commentator on Neville Bennett’s article posted a link to this slideshow, explaining in a short series of slides the history of LVTs in New Zealand and their usefulness. http://www.slideshare.net/deirdrekent/why-land-value-taxes

Winston Churchill's speech on land value taxes is here,http://www.landvaluetax.org/current-affairs-comment/winston-churchill-s…

Obviously in the UK with their class system and House of Lords nothing creditable could be done to challenge the large landed interest.

But in so called egalitarian NZ, what is the problem of taking on these vested interests?

Clearly NZ is no longer egalitarian and the pollies themselves are among the vested interests by owning Auckland rental properties. Looks hopeless.

Agree, there is no way in the world that the National party want to solve the housing crises. It is all about looking after vested interests. National backers are generally business people and multiple property owners. If National brought in any policies that that would cause house prices to flat line or drop, they would suffer financially in the next elections.

The reason National has a high immigration policy is the same, i.e. to keep wages down and house prices up.

It is not rocket science.

The only thing that will change investor's expectations is a significant correction.

I hear this argument a lot. Along with the defeatist argument that the only way to fix the broken housing market is to accept fate and wait until we have a nasty property bubble popping event like happened in Iceland, Ireland and Spain. Only then in the throes of the crisis will we have a chance to fix our broken housing market.

But does that really make sense? Would our most 'popular' PM -John Key who has spent his entire administration protecting the 'landed gentry' vested interests. Would he really change his spots in the event of Auckland property market crash and help out Generation Rent, the tenants, the struggling homeowner or will he help out the banks, landlords, the selfish landowner and the usual sycophants that got us into the mess?

It seems to me that not doing anything and waiting for the crisis is leaving it to chance on whether the policy response will benefit the wider public or just the usual vested interests.

When it happens the government will be impotent. It's just a matter of time.

You've read too much into my comment. I didn't say nothing can be or should be done.

I'm talking specifically about investor sentiment - if you could infer one thing from spending time at interest.co.nz it's that a large proportion of investors cannot imagine a world where property falls. My immediate family fall into this category!

Go back through my previous comments and you'll see non-stop critique of National and suggestions to fix the problem.

Zombie ponzi I wasn't having a go at you. I just saw an opportunity to comment about people who think the only way to fix the housing market is to wait until it crashes,

So, according to the latest news, NZ adults are per capita the second wealthiest in the world behind the Swiss. It is all based on the property ponzi, lifting you and me to $400k each.

Dunno about you but I fondly imagine mine to be lots more than that, so someone must be missing out.

Just let me check my back pocket again.

When was this survey carried out? Last month? Talk to any agent on the North Shore this month and they will tell you the market has died since 1st Oct. It is quickly becoming a buyers market.

Actually this is worse even than Bernard has identified. Interest have posted a report that quotes Bill English as stating that the Government has subsidised property investment through accommodation supplements to the tune of $2 billion. The bottom line is that this $2 billion is our taxes that the Government has used to actively support a state of affairs that has denied average kiwis the opportunity to buy their own home, and even struggle to afford renting one in many places!

In a nutshell, yes, exactly

Why don't all the readers stop and ask if something has changed that is causing the problem. Sure there are more people coming into the country but most of them are students who are not buying houses. The biggest single change has been the tax increases lumped on property investors. These taxes are not just for houses but include all property such as factories, shops, schools, entertainment facilities. Investors need to recover those costs or else pull back on building new rental stock. Surprise most of the new houses going up are not rentals they are almost all over 200 sq m. Not the normal rental unit.

When we lost about 50,000 NZers several years ago, the house market did not drop, now that we are gaining 50,000 odd, we are saying this is causing the high house prices.

It is to do with the world being flooded with cheap money after the GFC, not immigration

misleading - this years intake of international students become buyers in two to three years time, and this years intake will be replaced by another new intake next year, it's called the domino effect

The late William Rees-Mogg had this to say about an exact equivalent in Britain in 2007:

https://web.archive.org/web/20080516013826/http://www.timesonline.co.uk…

Demand of all sorts has grown. There are more households, more people are living on their own and there are more immigrants, with more to come. Without any improvement in housing conditions — which is badly needed — many more houses will have to be built. They are not going to be built under existing plans. The current shortfall is at least 100,000 houses a year, and even that would take ten years or more to bring housing supply into balance with demand.

Apart from being complex, inefficient and bureaucratic, the planning system gives far too much power to existing homeowners, “nimbys”, to prevent new building in their area. The “40-40s” — those who are 40-years-old and earn more than £40,000 a year — have an interest in maintaining a high level of house prices. The localised system of detailed planning control puts them in a strong position to protect that interest.

If one asked a competent graduate of a business school to design a business plan for a national cartel to raise house prices to the maximum, it would have four elements, all of which exist in our present system. It would license housebuilding, so that no one could build a new house without a licence, or even rebuild an old house or a redundant barn. It would encourage developers to maintain large land banks in order to benefit from rising prices. It would leak out new permissions only after long periods of delay. It would combine this with an unlimited flow of mortgage credit and relatively low rates of interest.

If you restrict supply below the market clearing level and increase funding, you will inevitably create a bubble and you will lock people out of the market. That is what has been done; those are the consequences that have followed.

Of course, this is an economic distortion that will eventually have to be unwound, though cartels can last for a long time. It also causes great social evils. The poor suffer the most. The housing shortage is bad for health, for education and for crime.

He was talking about London, of course, but the same "planning" (double-quoted, because the aim of real planning is to avoid precisely this sort of schemozzle) applies in Godzone.

Hey ho

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.