By Bernard Hickey

When I bought my first home in Wellington in 1992 it was rare for banks to lend more than twice the income of the occupier and generally three times income was seen as the upper limit.

The requirement for a big deposit and the limit on the loan to income multiple meant we could only afford a house worth NZ$112,000, but it was the same for everyone so that house was around the average for Wellington and just fine for a young first home buying family.

Back in 1992, mortgage rates had just dipped under 10%, but they had been as high as 15% less than two years earlier, which meant both the bank and I were reluctant to take on too much debt. This was a time when unemployment was still over 10% and I had been a jobless ex-student just 18 months earlier. Banks and borrowers were as risk averse as each other back then, and the idea of borrowing to buy multiple homes as investment properties was foreign.

Fast forward to 2015 and the lending mathematics are on another planet. That same house in Wellington has more than quadrupled in value, thanks in no small part to interest rates halving and the 'normal' loan to income multiple more than doubling.

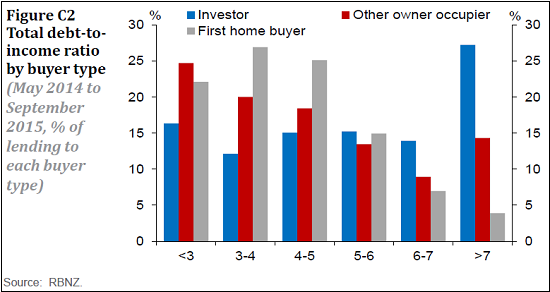

We all knew the leverage had increased, but until this week we weren't sure just how much. The Reserve Bank published its first analysis of loan to income multiples in its Financial Stability Report this week, having only recently begun collecting the data from the five biggest banks -- ANZ, ASB, Westpac, BNZ and Kiwibank. The results were startling.

Around 40% of the mortgages lent between May 2014 and September this year were worth more than five times the borrowers' income. Around 60% of all lending to landlords was at multiples to income of over five. A stunning 27.3% of landlords took loans worth more than seven times their incomes.

This is only possible while interest rates stay at record lows and while tenants and landlords have jobs. The Reserve Bank did not break down what proportion of these loans were in Auckland, but it did note that 60% of the value of all New Zealand house purchases in the past year has been in Auckland.

This, in a nutshell, is why the Reserve Bank warned again this week that there was a growing risk of a sharp correction in Auckland house prices and that the risks to financial stability had increased in the last six months.

It's also why the Reserve Bank toughened its high Loan to Value Ratio speed limits for Auckland landlords from November 1. The drums are also beating for the Reserve Bank to go further than limiting loan to value multiples. Both Treasury and the IMF have suggested in recent months the bank look at limiting loan to income multiples as well. Last year the Bank of England imposed a limit on mortgages with multiples of more than 4.5. If such a limit was imposed here, potentially more than half of all new lending to landlords would be banned.

Governor Graeme Wheeler said this week the bank was not currently looking at imposing loan to income multiples, but it was watching the British experience closely. Instead, Governor Wheeler said he was watching to see how the bank's two rounds of LVR limits were slowing the Auckland market.

He said it was early days yet and he wanted to see another four months of sales figures before looking at whether a 'multiple pronged' attack on Auckland's inflated market was needed.

This week's figures showing a 19.4% fall in sales volumes in Auckland in the month of October, along with a 3.0% fall in the median house price, suggest something is happening. Although Deputy Governor Grant Spencer cautioned that October looked weak in part because August and September had been so strong as buyers rushed in ahead of the new LVR limit and the Government's new two year 'bright line' test and reporting requirements to deter speculators and non-residents.

Time will tell. If Auckland bounces back within a year, as it did after the Reserve Bank's first round of LVR limits in October 2013, then keep an eye out for the other 'prong' of the attack.

------

A version of this article first appeared in the Herald on Sunday. It is here with permission.

32 Comments

Time will tell. If Auckland bounces back within a year, as it did after the Reserve Bank's first round of LVR limits in October 2013, then keep an eye out for the other 'prong' of the attack.

The only attacks the RBNZ has deliberately engineered are OBR and below risk adjusted returns and both are directly aimed at savers, not the speculating banks and borrowers that have little skin in the game.

So the RB has engineered a recession as an excuse to drop the OCR to 2.75% even though 2? years ago it was predicting 4.75%?

Its not savers but the saved.

I dont agree a low OCR is aimed at "savers" btw, its aimed at SMEs and keeping the economy going and ppl employed. Something it seems you do not care about. Simple as everywhere else in the world we need a new policy to deal with the gamblers and not by killing off the economy.

the OCR has become less and less effective to get consumer spending up and the economy going due to more of peoples wages being spent on housing either rents or mortgages.

Cheap credit is undoing any benefit by forcing asset prices up. until risk is reflected back int price we have a problem I.e at the moment banks see no risk at lending on Auckland house prices,.Neither did Ireland, spain, USA, or English banks last time

we need to find other ways to stimulate the productive economy.

I dont agree here. Prices were rising before interest rates started to drop to . What we have seen is there is the perception there is no where else to invest.

I dont agree a low OCR is aimed at "savers" btw, its aimed at SMEs and keeping the economy going and ppl employed.

Hmmmm.

It is really quite clear that the banks are not really keen or interested in business, particularly the SME space. They pay lip service to it and purport to be active and keen, but the reality is that they are doing this because it is expected of them, and to show their true colours would be very bad PR. So they instead play the game of being present, but not really being active in the SME space. Read more

Banks are no longer very interested in credit-worthiness, or in establishing the sustainability of small business’s cash flow. They just want the security of the entrepreneur’s house.

The result, apart from the well-documented dearth of business investment in Australia, is that two new industries are now beginning to flourish in Australia: non-bank lenders focusing on the personal loan and small business sector and venture capital. Read more

would this count as a worked example...

The Commonwealth Bank committed "fraud" when it deliberately impaired more than 1000 performing commercial loans worth more than $8.2 billion, a parliamentary hearing has been told.

The human cost was huge, with valuers instructed to come up with lower valuations on the commercial loan book of BankWest, which CBA bought in 2008 during the global financial crisis.

It didn't fall apart, it was assassinated... I was dead man walking the day they [CBA] took it [BankWest] over.

The lower valuations enabled CBA to foreclose on the loans even if customers had never missed a payment and had adequate security. The loans were business loans, for both family-run businesses and medium-sized ventures. The average loan size was $8 million.

Mr Hall said the bank had two motivations in impairing the loans. The first was to reduce the purchase price of BankWest as per the clawback clause in the acquisition agreement that allowed the CBA to demand repayments from BankWest's former owner British bank HBOS. The bank's second motivation was to lower its cost of capital by culling loans related to the Basel Advanced Accreditation requirements to get the so-called tier-two bank, BankWest, up to first-tier bank status.

Read more: http://www.smh.com.au/business/banking-and-finance/committee-hears-of-c…

Follow us: @smh on Twitter | sydneymorningherald on Facebook

the further reader stories within the limited comments section are sobering...

P.S.

In 2013, the NSW Court of Appeal found Mr O'Brien's loan had been foreclosed on unfairly and awarded him $40,000 in legal costs. After months the CBA had still not coughed up the costs and Mr O'Brien and his lawyers at King & Wood Mallesons were forced to call in the NSW Sheriff to CBA's head office in Martin Place to seize property equivalent to the value of the costs order.

Mr O'Brien said the executive assistant to CBA chief executive Ian Narev told the sheriff assets in the builder were CBA's and there were no BankWest assets that could be seized.

"The sherriff was hoodwinked into believing it was a BankWest problem ... This is standard operating procedure by CBA and it is financial bullying."

classic?.

Maybe re-read paragraph two of BH's article again Steven.....house prices are engineered.... it's the percentage of value that has been engineered that is not well known !! The whole of the economy is engineered and that includes interest rates, exchange rates etc......Have you ever thought about all the talk on increasing interest rates, increasing the OCR and the people who went out and locked in the interest rate at the banks on their mortgages....and all the while the RBNZ kept statistics on the percentage of mortgages that were locked in....I can only assume that when locked in mortgages reached the RBNZ threshold that they then started reversing the OCR hikes that they had previously made .....Got to look at who was locking in profit......and it sure as hell wasn't the sheeple!

When you get numerous bureaucracies all tinkering around the edges and sometimes dipping right into the core then they will achieve the result they want......"Birds of a feather flock together" is a quote that wasn't written in error but from observation.......you got to put on your 3D glasses on look carefully at the hologram to get the real picture.......the free market is an illusion.......as soon as you regulate something you are engineering an outcome!!

An investor buying at 80% LVR, on a 7% yielding property, which is likely just cashflow positive, is borrowing at 11.4x debt to income on the deal.

At 10% yield which will be cash flow posititve and represents a great return compared to most other investments, he's still borrowing at debt to income ration of 8x.

If an investor was limited to 4.5x income, at 80% LVR, he would need 17.7% yeild on the deal before he could buy!

OR, for a 7% yielding property, he would require 70% DEPOSIT, i.e only borrow 30% of purchase.

Would have massive impacts on rental market in NZ this measure was implemented, no investor can get 18% yielding deals, or runs their portfolio with only 30% debt.

Oh, wait, you mean banks are lending recklessly again? Who would have thought.

I think you mean the banks are increasingly using depositors funds to gamble on houses, at no risk to the bank CEOs collective wallets, and little risk to their covered bond holders

Yes and its all legal! I should have been a banker and not an engineer. Hopefully of course at little risk to the tax payer either.

Yep, got to earn bonuses.

Poor old BH.

He still living in the 90's. If he is not careful he will snap one of the cobwebs under his armpits.

The world has moved on since then for better or for worse but it will never be the same again.

If you want to use history as a lesson why not go back to the 1890's where only land owners could vote, (if they were male), women could only borrow if guaranteed by their husbands, and money was reckoned in gold, silver and copper? Better still we had a true class system, people worked 12 hours a day, 6 and half days a week, taxes was virtually nil, and the poor could hardly read or write. Yet is was the time when the Western World was at its zenith of power, the sun never set on the British Empire, and there was strict order or risk hanging or deportation.

We are in a new normal and harking back to the so called "good old times" is an act of futility.

we are in cycle not a new normal, interest will rise again, people that binged on credit will default. those that have been around have seen it before, those that look through rose tinted glasses will most likely be the ones caught out.

Not sure interest rates will be heading up any time soon - banks are now offering 4.4% fixed for 4 years or 4.45% for 5 years if you push them hard enough so that should provide a level of protection. Likely that rates will dip below 4% fixed for 3 or 4 years soon. Many will be gutted that they fixed well above that 6 to 12 months ago - the break fees would be hefty too!

"Likely that rates will dip below 4% fixed for 3 or 4 years soon."

Can't see how that's "likely" given the Fed is tipped to tighten monetary policy, starting next month - so the yield curve will steepen. You're the only person I've heard say that is a "likely" scenario - Let me know what unicorns you've been talking to.

The problem is you are looking at the past and assuming the future will be just like it, on a finite planet.

Bernard I've noticed the same thing happening in the personal loan space. A couple of the banks are lending absurd amounts (unsecured) at very high Dsr. Many counterparies are not paying or are in default. The trading banks have taken on riskier lending policies.

I find it fascinating as finance companies have secured positions, generally secured against mv, whereas the banks appear to have unsecured positions now. The reverse of 5-10 years ago

Many savers out there would be horrified. Personally I don't believe yields for savers are high enough considering the risks out there, especially coupled with obr.

One question - are the income multiples for Investors based on their wages - or Wages + rental income so total income? A considerable difference exists and equally for most investors - even those with just one rental - their wages cover all their living costs - and so the rental income is only required for the interest and property costs - not day to day living as these have already been met

This is why all investors should be required to make P and I payments - could be the next target on Wheelers radar.

When I purchased my first home in Wellington in the mid 1980's the price was approx 40% of my wages at the time. Even on that ratio it was difficult to get finance - took about 30 days to get approval. Today that house has a CV of 13 times what I paid for it! Solicitor nominee accounts were used to fund many house purchases and interest rate back then was from memory about 17% or 18%. It was difficult to buy unless you had about 33% deposit. It was the repayments banks were most interested in back then and you could only do P and I. There were schemes like capitalizing the Family Benefit payment and the government also introduced home start in the late 80's to help people into first homes.

So if we went back to 66% being the maximum loan and repayments on P and I unable to exceed 33% of your income where would prices be today? The latest LVR rules and 2 year capital gains tax will probably fail to achieve the Reserve Banks objective - then the only moves they have left are - no more interest only loans for everyone, or maybe just investors, limiting amount of income that can be dedicated to repayments and maybe the new proposal from the UK i.e. Mortgage interest unable to be offset against rental income on buy to lets. I do not trust Wheeler - he will be looking at all of these schemes so watch out! Although I agree with Big Daddy above, these government/Reserve Bank rules could send us back to times past.

Back to sensible lending practices, back to sensible house prices - oh the horror !!

High debt is by design. Debt is control.

Some simple math that might explain lending multiple increases...Bernard earns $50k in 1992, he borrows 3x that with an interest rate of 15%, this implies interest payments of $22.5k...flash forward to 2015, Bernard still earns $50k, he borrows 5x that with an interest rate of 8% (remember inflationary pressure is far lower these days then 20+ years ago), this implies interest payments of $20k. The example illustrates that even though headline leverage multiples have increased, the serviceability of loans is fairly similar, which is ultimately all that banks care about.

.....25 year mortgage (so plenty of time for interest rates to go up)... many interest only, wage increases non existent (and likely to go down or be lost as east & west equalise) = slave to the bank for life and potentially no equity at the end of it all.....Fools paradise.

Gee, from the title I thought young Bernard was writing about the economic outfall of the Paris massacre.

Glad that he is sticking to his usual melange of real estate and (on other occasions) climate change with a bit of pro-immigration propaganda strewn in. Whats the weather like, on the ivory tower?

Bernard, you cannot compare income to debt ratios of home occupiers to landlords... you should know better than that, as a home owner who pays for your mortgage ? You do, for a landlord the tenant pays the majority of the interest to the bank via rent. Of course landlords justifiably have much higher debt to income ratios

In my view that type of investment is insane. ONLY FHB should be able to take mortgages. You want to invest - buy the property for rental - it should be paid CASH or 80% deposit. Otherwise investors will be always in much better position to buy.

And that thinking to have multiple rental houses, investment portfolio - it is just crazy locking out families from the market.

Only an imbecile would suggest limiting investment (ie business) loans to low multiples of income.

If I borrowed $1m and it returned $200,000 per year (ie a multiple of 5) and I paid $45,000 a year to borrow that money, then I would be a mug not to take out that loan (if it were on an appreciating asset), because it would earn me $155,000 extra per annum.

Any restriction needs to be one put purely on the serviceability of the loan. ie Wiith lower interest rates the maximum term of the loan should be reduced so that the credit is not so cheap...

ie If total payments on a $1m loan were $100,000 PA (principal and interest), then the bank would require a good $130 or $140k income on that, which would limit total lending to multiples of about 7.

That would be the solution for low interest rates, and as rates increase, the restrictions on minimum principal repayments could be eased...

Things are tightening up again but there was a period where the banks really did not care how much you borrowed as long as you could meet the repayments. I guess it came down to individual responsibility and common sense, fast forward 10 years and this has gone out the window, its always someone else's fault now and greed and the "must have" took over.

I hope this is not too far off topic but six months ago the Fat Prophets outfit recommended to me seven Aussie stocks. AJA, BOQ, GXL, MGR, QBE, SIV and SUN.

Two have them have appreciated the best by 2.2%. The other five have all dropped, one by as much as 14.6%.

Any real estate agent who put you onto such a load of junk would have been sacked some time ago.

On the bright side you could have stuck it all in Glencore

http://angelachaoblog.com/2015/11/13/flooding-the-oil-market-opecs-stra…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.