*By Cameron Preston

Two years ago I suggested that the insurance industry might be about to hit ‘the wall’ as they approached the halfway mark in their Canterbury Earthquake settlements.

In any endurance event those that hit ‘the wall’ either haven’t prepared, or haven’t planned to go the whole distance.

They either come out of the blocks burning the limited energy and goodwill the body will allow over the short to medium term too quickly, not factoring in the whole distance, or they simply have not thought about the second half of the race.

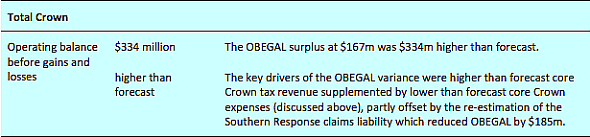

On 10 May Treasury quietly announced Southern Response Earthquake Services Limited (the earthquake challenged rump of the bailed out AMI Insurance retained by the Crown) has just added a further $185 million to its estimate of liabilities to 31 March 2016:

Put this on top of the $325 million jump in 2015 and the $500mln+ promised in 2011 and 2013, and suddenly more than the promised $1 billion in Crown Support is required.

This development is expected to be officially announced in this Thursday’s Budget and makes AMI Insurance the biggest taxpayer bailout in New Zealand history.

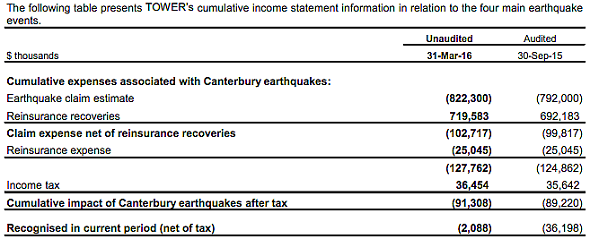

Tower Insurance this week announced that a $2.9 million increase in its Canterbury quake ‘net’ provision in the 6 months to 31 March 2016.

However what is carefully hidden away is the fact that Tower’s ‘gross’ provision (what it has and will need to pay customers) for the Canterbury Earthquakes has actually increased by more than $30 million in just 6 months, from $792mln to $822mln:

Cushioning this blow (and cushioning is very important in any endurance event) was a $27mln increase in its reinsurance, which is the last of its emergency purchase of $50mln “Adverse Development Cover” (ADC) in 2015.

ADC is a special type of reinsurance akin to extending your insurance cover for a collision after you have already had that collision. As a result ADC is very expensive and I doubt anyone will be rushing to extend another $50mln of ADC to Tower again anytime soon.

IAG is another insurer who has hit the wall. Warren Buffett offered help last year.

Buffett provided both ADC and a capital injection. But this came at an eye watering price for IAG (and their customers and shareholders) as the Buffett deal doubled their reinsurance costs from A$143mln to A$340mln and diluted existing shareholdings. Most of the lost profit and earnings will go to Buffett – he has a shrewd eye for value investing when it matters.

The narrative is the same for all insurers with an exposure to the Canterbury Earthquakes, including Vero, AA Insurance, Medical Assurance Society, and Farmers Mutual.

While they all knew they would run out of reinsurance steam at some point in the race, most didn’t believe they would hit the wall this early.

While most are reporting reaching the 70-75% mark, really once you exclude the easy downhill Red Zone settlements gifted by land decisions at the start of the race, they are only at the 60% mark in the race proper.

The private insurers, via their support team the Insurance Council of New Zealand, continue to use New Zealand’s public insurer, the Earthquake Commission (EQC) as an easy and convenient excuse.

EQC appears to have run the course in the wrong direction, only now starting to settle land claims and address foundation damage. Just when it thought it was near the end of its race, it has to start again.

So while none of the competitors can be accused of setting any record shattering paces before they hit the ‘wall’, and while they have been regularly taking on energy as the race progressed, in the form of higher premiums and expensive ADC paid by all their existing customers, the reinsurance energy and goodwill has all but gone.

Anyone that has ever run a marathon will tell you the real secret is training, it’s too late on race day.

The insurance industry, including EQC, was fat, unfit and ill prepared when the starter gun went off for this race of their lives, contrary to the slick marketing that told their customers they were ready to go the distance in the event of the unthinkable.

Once you hit the wall, the easiest thing to do is give up and walk the rest of the way. Unless of course there are people waiting at the finish line shouting for you to start running again, no matter the pain.

---------------------------------------------------------------------------------------------------------------------

*Cameron Preston is a Christchurch chartered accountant and homeowner who has longstanding unresolved quake insurance claims.

39 Comments

Insurance relies on small scale events being the only eventuality. They simply don't factor in (or is it deliberately ignore) major catastrophes.

The Japanese Tsunami and Chch Earthquake showed just how fragile the industry really is.

All the premiums in the world with the best investment knowledge wont cover a disaster hitting in a major city (with good insurance cover). Imagine Tokyo, London, or New York being hit by something serious. Heck, even an Auckland Volcano blowing and the global insurance industry would be crippled.

Only because they take any of the premiums not paid out on claims each year as profits, and haven't salted them away for the major disasters. They have lost sight of the original model of insurance companies and because of that they cannot do what they promise to.

That's just it though isn't it. They have to make some profit otherwise there is no more insurance market.

I just don't think they have realised the business model doesn't stack up anymore. The premiums required to cover all possible claims would so high that no one would take out cover. So you are left with a planned shortfall.

They just hope that never eventuates, or when it does - the Government steps in (as with AMI).

maybe Noncents. But it was only AMI who needed the bailout, and a vast one at that. They did not re-insure properly There needs to be proper law here, and jail time for such levels of mismanagement. Their crappy behaviour could of hurt a lot of people lifelong, but instead the victim is the taxpayer. Lucky us.

We live in the wrong country for justice though.

It was not just AMI that didn't have adequate reinsurance. IAG and Tower have exceeded their reinsurance cover, and probably others have as well. Its just that AMI did not have sufficient reserves, or shareholders with deep pockets.

Yep. But AMI did not manage that Max. They took money from folks, without covering their responsibilities in a way that was realistic to AMIs setup. Folks paid for insurance and were not actually covered.

'Imagine Tokyo, London, or New York being hit by something serious.'I

600 tons of melted radioactive Fukushima fuel still not found, clean-up chief reveals.....

Following the tsunami-caused 2011 meltdown at Fukushima Dai-ichi nuclear power plant uranium fuel of three power generating reactors gained critical temperature and burnt through the respective reactor pressure vessels, concentrating somewhere on the lower levels of the station currently filled with water.

The melted nuclear fuel from Reactor 1 poured out completely, estimated 30 to 50 percent of fuel from Reactor 2 and 3 remained in the active zone, Masuda said.

The official estimates that approximately “200 tons of [nuclear fuel] debris lies within each unit," which makes in total about 600 tons of melted fuel mixed up with metal construction elements, concrete and whatever else was down there........

TEPCO’s inability to locate the melted fuel could be explained by huge levels of radiation near the melted reactor shells. It is so high that even custom-built robots sent there to get information about the current state of affairs there get disabled by the tremendous radioactivity flux. Human presence in the area is understandably out of the question.

https://www.rt.com/news/344200-fukushima-melted-nuclear-fuel/

Hope everyone is taking their X-2 Iodine !

not the case Noncents - insurers reinsure with each other for these eventualities. the issue is that most insurers underestimated the potential liability of the CHCH earthquake - resulting in a shortfall.

Just imagine the impact of Deutsch Bank having defaults on a significant portion of its 20 trillion Euros of derivatives (thats 3 times the size of the German economy) and you bet most other Banks will have exposures so in this event the Canterbury Quakes will be as dropping a stone in a puddle compared to the Tsunami that would follow a derivative default of Deutsch Bank size.

Red zone settlements were not ‘easy’. They had to go through the same scoping and costing process as all other EQ claims. While ill informed comments from contributors ignorant of the insurance business are understandable , Preston claims to be an expert so must know his '60% mark’ comment is misleading. The 60% are settled claims. The remaining 40% will be at various stages, many well advanced to a stage where costs are pretty much set. Not all back at the start line with the extent of damage and costs unknown by insurers, as Preston’s ill chosen race analogy implies.

What I can't understand is that, when most of the central city was leveled by the quake, and, when most of the land to the east of the city is now very risky, and, with rising seas due to global warming making things worse, why oh why did not Christchurch re-think entirely how the stupid place should be organised??

Surely, it would have been smarter, cheaper, easier, faster to just open up land to the west, closer to the airport, in satellite centers such as Rolleston. There's been some really stinky business going on - i assume to save the asses of those who were heavily invested in Christchurch commercial land. I imagine all of what's been going on has simply been, bottom line, bailing them all out. They are trying to rebuild the heart of Christchurch while that heart has already died and left - new hearts even un-supported and unplanned have emerged but instead of running with that the stupid idiots that run the city went hell for leather to rebuild the old core - when in 50 years it will be under water - sheesh - how stupid can they be? That's without even taking into consideration further earthquakes and worse - the big tectonic boundary events that are overdue - 8 or 9 scale events - would simply level the place again. Like really - who are these people - have they no basic education in the things that apply to Christchurch long term???

Rapidly increasing atmospheric CO2

May 23, 2016: 408.86 ppm

May 23, 2015: 403.57 ppm

Up 5.29 ppm (versus a recent average of 2.11 ppm per annum)

https://www.co2.earth/daily-co2

and rapidly rising temperatures

http://data.giss.nasa.gov/gistemp/graphs_v3/

indicate Christchurch will be under water in much less than 50 years.

Cost prohibitive to move the city west. Look at the argument in AKL about massive infrastructure costs for new subdivisions. Alpine tectonic event will not 'level the place'. It will produce shaking in CHCH about the same as September 10.

and you are a geologist specializing in NZ earthquakes? As for your "massive" infrastructure costs - so you are saying that might as well keep it where it is, let it flood and shake - because, ah, the cost is too high to build new in another place than demolish and rebuild and then abandon and move anyway - you're kidding right?

Go to CHCH, drive around the eastern suburbs, let the sheer size of the problem sink in, add up the cost for every one of the thousands of houses there that you propose be rebuilt elsewhere, plus the supporting infrastructure needed and you will quickly figure out why moving those suburbs is not a goer. NZ inc cannot afford it. Retreat from flood zones will happen gradually anyway.

That the alpine fault rupture will in CHCH approximately replicate the shaking effect experienced in Sept 10 is common knowledge. Confirmed again by a recently published study.

What happened to all the money paid to the insurance "industry" for all those years prior to the earthquake - You didn't think that had been safely stashed away did you.

The ugly flip side of the re-build insurance payouts and its one off boost to growth are emerging as per the broken window fallacy.

While John Key and his lot were basking in the glory of the lift in GDP and all that lovely free loot from the insurance companies it was obvious that us poor saps would be saddled with huge boost in our insurance premiums - including a big fat wad to arch parasite W Buffet.

I had my lot on about the continuing increase in premiums - even for my humble wagon in Northland - they reckon it was to pay for Christchurch. Anyone have the total figures for the additional post quake gouging - you can guarantee it will be way more over the years than was ever paid out.

Bailing out AMI was just stupid. Government should of let it go under. Let the people who had insurance with them sue as a collective. How else are we going to learn the hard lessons about this crocked industry? They are nothing but casino's.

Same with SCF. Government should insist on getting that money paid over under false pretenses back.

Sure , why not let thousands of families who had not a chance of understanding how shaky AMI was when they took out their policies, go down the gurgler. Hundreds lose their homes entirely, thousands forced to live in wrecked houses. Misery, pain, suffering, they be the best teacher, eh. And who exactly would the policy holders have sued?

people have to learn somehow - your way nobody learns ever - and your way sees the rich taking over because nobody else can afford to compete - people stupidly believe what they see on TV and such and so waste money on insurance that is never needed. The insurance industry is just like Lotto - you are continuously hammered that you have to be in to win even though your chances are tiny, insignificant - same as insurance. And there's this - for many people the only reason they carry insurance is because the mortgagee banks require it. The banks - blood suckers at the core of world problems but they have power - so we bail out insurance companies so banks don't loose too. Do you think there's ever been any chance that those in control of spending your taxes would ever let banks and insurance companies collapse - it would never ever ever happen so your argument is just rubbish.

Tell the people down in CHCH that 'insurance is never needed' and you'll be laughed out of town. NZrs were paid out $2.5bn in claims last year. 'Tiny, insignificant' ? .... err , don't think so.

I own bank shares and they have been excellent investments. I'm offended that you describe them as blood suckers.

And if a bank gets into trouble the RBNZ will implement the OBR sticking it to depositors big time while ensuring the longer term wealth of shareholders is well looked after.....yes this is a very good system of big corporates obtaining welfare for shareholders.

If things get so dire that OBR is triggered, shareholders will already have been slaughtered. Note the way bank share prices have recently dropped sharply as APRA capital adequacy rules bite, ROE drops and debt provisioning rises. We shareholders are usually first to feel the pain. That's OK, it's called risk and we accept that. As do bank depositors, albeit to a lesser extent. If a black swan flies in and OBR is not triggered, depositors will have it 'stuck to them' to a much worse extent, i.e. they will likely lose it all.

Aorak1 your arguments are simply wrong. I suggest you read up on how the insurance industry works - without sounding patronising i think you may be misinformed. In terms of big business - whenever the government does a bail out - typically the shareholders lose everything - so again your anger maybe misdirected. The State on the other hand will need to weigh up the cost of collapse, and the fall out which is inevitable. If the business can be salvaged then the State can at a later date sell its share and recoup the funds invested, and possibly the profits made subsequently. A win win situation. The US did this with AIG, and many other entities after the GFC. Many of the bailouts have been repaid. All that happened in reality was private debt/equity was picked up by the State. This has subsequently been transferred back to private hands.

What's to understand about insurers? They do have a reputation that should alarm anyone with half an actual brain. And just because someone has kids doesn't automatically warrant a god damn bailout on behalf of taxpayers! "Families" is an emotive word used for political blackmail a great deal. Funny how no non breeding taxpayers seem to get targeted policy just for them.

For obvious reasons. Spot the vulnerability difference between dependent children (who will take the country forward and provide our living) and self sufficient adults.

hows that going to work Justice? why would you sue a failed business? thats never going to work. The state picked up the Tab as this was the only way that those people who insured with AMI would be able to settle. Subsequent to this the government took all the Insuers to task as they recognised most had understated their liabilities for reinsurance.

Not surprising they didn't correctly estimate their full exposures given the fault and how it would behave, were both unknown.

NZ being on the ring of fire is always going to be a high earthquake risk. if the insurers underestimated the liability for CHCH what would they look like now if the same event had struck Auckland?

Wouldn't. EQ risks in AKL much lower because of geology. But who knows if they have estimated the volcanic eruption exposure correctly.

You change the rules and make shareholders personally liable in such circumstances How's that? Apply this policy to any business that takes premiums from people.

That's the start of a rather slippery slope don't you think?

never going to happen. no one would invest in shares, or the risk premium would go sky high. your insurance premiums would treble, or quadruple overnight. besides people would just purchase shares through a limited liability company to circumvent.

AMI was a mutual. Policy holders were ( in theory) the shareholders. .

AMI. What was done was done and you can't wind time back. The taxpyer had to step in to help. But you can't wind the clock back on most crimes and this was a crime. There should be some jail time dished out. "To encourage the rest"

I share your sentiment about sending an 'encouarging' message but don't think AMI management failures were a 'crime' in the accepted sense. Incompetent perhaps but every bit of exposure modelling in CHCH was quite reasonably based on the Alpine fault movement, not on an unknown fault under the city. You can't model what you don't know about. A question though - once AMI management DID learn in September 10 that it wasn't the alpine fault, what assumptions did they make about what was likely to happen next? As you say, done and gone but might be an interesting study in corporate decision making for a student someday.

Did you seriously expect that after one of the worlds worst insured catastrophe events reinsurers would not significantly up their NZ risk profiles and pricing?

Reinsurers will not recover even a fraction of what the EQ has cost them, even after many years of providing reinsurance capacity down under. The NZ market is just too small.

IAG has one of the worlds biggest reinsurance programs, I’m sure if there was a better deal available than ‘arch parasite Buffet’ they would have gone for it.

Loss ratios (the amount of premium collected to claims paid) has stayed within a 7 point range over the last few years since the EQ, so no evidence insurers have been gouging.

Common taters are woefully iggerint about the insurance business.

Insurers are the retail shop-fronts for re-insurers and certainly don't hold massive reserves of their own. They clip the ticket for the marketing and claims processing overheads, and buy re-insurance to suit their local circumstances. So the risk is actually at three or four levels:

- the purchaser/homeowner may have failed to inform the insurer about extra risk e.g. improvements to the property or material changes to their circumstances. Uberrimae fides applies....

- the local insurer may have re-insured for too little or under inadequate terms

- the re-insurer may have mis-priced the insurance bought in relation to the risk and may hold too little or insufficiently liquid reserves thereby

- the world may suffer a cluster of events which test the best reinsurers....

And I, as a Christchurch north-east resident, have exact, local experience: the blogs tell it all:http://waymad.blogspot.co.nz/search/label/earthquake

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.