What happened to those predictions of weak economic growth?!

The Westpac and ASB economists were at the forefront of calls for lots of OCR cuts over the last year.

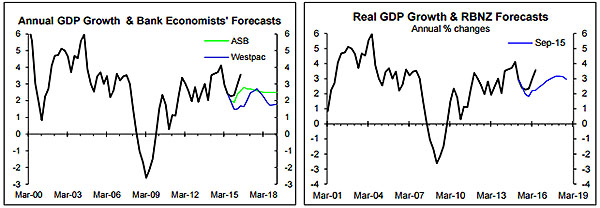

Partly supporting their calls for lots of cuts, the Westpac economists in October 2015 predicted that GDP growth would slow to 1.5% by the 2016 March quarter and remain weak for most of this year, while the ASB economists in November 2015 predicted a slightly better outlook for growth but one that has proved to be well below what has transpired, with GDP growth rebounding to 3.6% (left chart below).

Their forecasts were not too different from the Reserve Bank's (RB's) September 2015 predictions for GDP growth (right chart).

The economic forecasters clearly got something badly wrong.

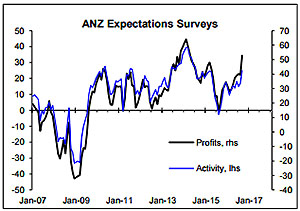

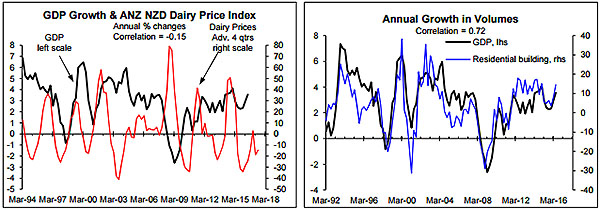

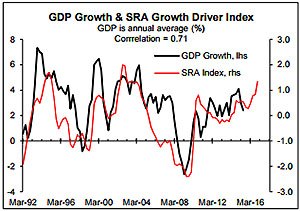

The leading indicators of GDP growth have continued to improve (adjacent chart), with some of the most useful ones pointing to GDP growth heading to around 4% this year.

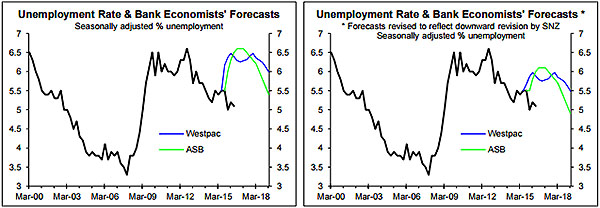

Consistent with their predictions of weak economic growth, the economic forecasters were predicting that the unemployment rate would increase (left chart below for Westpac's October 2015 and ASB's November 2015 forecasts). Instead of increasing, the unemployment rate has fallen. In their defence, Statistics NZ shifted the goalposts by revising down the historical numbers due to a change in the methodology that brought NZ numbers more in to line with international best practice. To compensate for this I have revised down the Westpac and ASB forecasts in the right chart by the full amount of the downward revision in the reported unemployment rate for the 2016 March quarter (i.e. from 5.7% to 5.2%). Even after levelling the playing field, the economic forecasters were well off the mark (right chart).

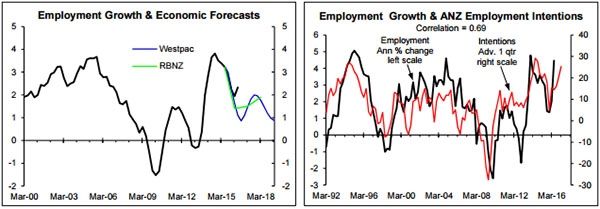

It is the same story with the forecasts for employment growth, with reality turning out much stronger than predicted by the likes of Westpac, the RB and the economic forecasters in general (left chart below for the Westpac October 2015 and the RB September 2015 predictions for annual average employment growth i.e. rolling four quarters over previous four quarters). The right chart below shows annual employment growth (i.e. latest quarter over four quarters ago) has been reported by Statistics NZ to rebound to 4.5% in the 2016 March quarter, a couple of quarters ahead of the strong rebound predicted by the ANZ survey of employment intentions. In reality, employment growth didn’t rebound to 4.5%. Statistics NZ including armed forces living off base in the June quarter for the first time and didn't backdate the historical numbers to include this factor. Silly stuff, but setting aside this qualification, the strong GDP growth and the V-shaped rebound in the leading indicators suggested employment growth has turned out dramatically stronger than predicted by the bank economists and RB last year (right chart).

So why did the economic forecasters get it so wrong?

Nothing strange or unexpected happened to drive GDP and employment growth dramatically higher than what the economic forecasters were predicting last year. They made a pretty basic mistake in putting too much weight on the fall in dairy farm incomes (a bit like journos chasing the latest hot story) and they put too little weight on the major stimulus in the pipeline from the fall in interest rates and super-charged net migration that has driven population growth above 2%.

The left chart below shows the lack of relationship between GDP growth and the annual % change in dairy product prices after advancing the latter 12 months to allow for any trickle-through effect. The economic forecasters acted as if there was a reasonably significant positive relationship rather than a mild negative one between GDP growth and dairy product prices. Equally, they understated the positive outlook falling interest rates and super-charged net migration implied for residential building, with annual growth in residential building activity having a reasonably high correlation with annual growth in GDP (right chart). If they had forecasting licenses they should be taken away. But the economist forecasters got it wrong together, which means no one gets blamed or sacked and they are allowed to continue to tell us what will happen to the economy as if they know what they are talking about, aided by an uncritical media.

I'm not just saying this with the aid of hindsight.

In October 2015 I pointed out that Westpac's labour market forecasts would be well off the mark. If the economic forecasters had done quality analysis of the drivers rather than acting like journos overplaying the current topical issue they could have done what I did and advised clients that growth prospects were much stronger.

Some time ago I constructed the SRA Driver Index that uses a bit of relatively simple maths to combine interest rates, net migration, the exchange rate, export prices and the petrol price. The adjacent chart shows the SRA Index as a reasonably useful leading indicator for upturns in GDP growth, with the chart recreated to look like it did in October 2015. The SRA Index gives weights to the five drivers based on back testing of their respective importance. This reveals that interest rates and net migration are the most important drivers and are much more powerful than export prices and the exchange rate. By contrast, economic forecasters have a tradition of putting too much weight on the exchange rate and more recently on export prices. They aren't very rigorous in assessing the relative importance of the various drivers. This is the case despite the RB being armed with a flash mathematically forecasting model. Having in my earlier years at the RB been involved in building parts of a past forecasting model I can tell you what a nonsense it is. Effectively the RB forecasters torture the model and manipulate the outputs until they fits with the preconceptions and wishful thinking of the day.

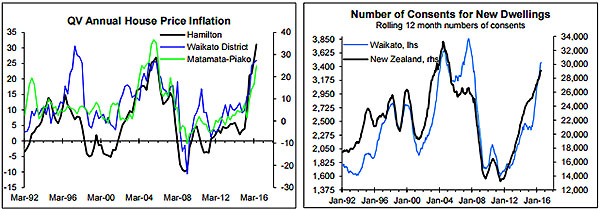

The silliness went beyond overstating the importance of the fall in dairy farm incomes to GDP growth and employment growth. In justifying calls for more OCR cuts some bank economists even suggested falling dairy farm incomes would have a negative impact on housing markets in places like the Waikato when there is no historical precedent for expecting this to be the case and where house prices and residential building have boomed on the back of low interest rates, strong population growth and spill over from the booming Auckland market. The charts below tell the story about how far off the mark some economists were about the relevance of the fall in dairy farm incomes to the Waikato housing market. A key theme looking ahead is the economic multiplier effects the housing booms are setting in play in provincial NZ.

There is a case for congratulating the bank economists

The bank economists and especially the Westpac and ASB economists have done a great job of getting on the bandwagon with Governor Wheeler. It is a bit like they were reading off the same hymn sheet. As a result, they have been correct in predicting that the governor would cut the OCR quite aggressively even though sound analysis of economic growth and inflation prospects suggest doing so isn't a good idea and will end badly (i.e. a repeat of the boom-bust economic and housing cycles sponsored by the Reserve Bank last decade). But credit where credit is due.

So what else have the economic forecasters got wrong?

The calls for OCR cuts on the basis that the fall in dairy product prices would result in economic growth being too weak without the cuts have proven to be wrong. The cuts are contributing to economic growth being too strong. By implication the OCR has been cut too much. In time the view that the OCR needed to be cut lots because inflation would remain too low if it wasn't will also be disproved, but that will take quite a bit longer. The result will be an outlook for interest rates very different to what the RB and bank economists are forecasting, which is par for the course.

There are a myriad of consequences of excessive OCR cuts including for the exchange rate, borrowers, employees, employers, retailers, housing investors, building firms etc. There is a risk that Governor Wheeler, encouraged by most of the bank economists, will largely repeat the mistake Governor Bollard made last decade, also encouraged by the bank economists, and underwrite boom-bust economic and housing cycles.

The emerging labour/skill shortage problem is central to the issue. Feedback from the coalface of the labour market points to labour shortages becoming a significant challenge beyond the building industry. For example, the latest Auckland Chamber of Commerce survey and Tony Alexander's latest survey of businesses (two links below). As Tony put it, "Staff shortages are evident across a wide range of sectors." These insights are consistent with the feedback I have from a range of contacts around the country. Part of the dynamics the RB and economic forecasters are assuming away in assessing the outlook for labour cost inflation relates to the poaching of staff and the 15-20% pay increases being offered to achieve this in many parts of the building industry. This behaviour will spread to more industries as the labour market continues to tighten in response to excessively strong economic growth.

By contrast, the one page commentary accompanying the decision to leave the OCR unchanged last month included not a single direct reference to the labour shortage problem (first link below). In my assessment the August Monetary Policy Statement - second link below - was negligent in the lack of attention it paid to the risk that the unemployment rate is already too low relative to the level consistent with the governor's medium-term inflation target. This reflects a repeat of the major mistake made by the RB last decade when they assumed away the labour cost threat until it had been fuelled to the extent there needed to be many OCR hikes to cool it. Back then I visited my ex-colleagues at the RB to warn them about the threat but they paid no heed of my warnings, just as the current forecasters at the RB would come up with lots of "good" reasons why this time will be different and labour cost inflation isn't a threat (encouraged by looking at the low labour cost inflation they can see in the rear-view mirror).

This is in the context of labour costs being the single largest cost of production in a modern economy. This means the labour market and labour cost inflation should be centre stage in assessing medium-term inflation prospects, as is generally the case in the likes of the US and Australia. By contrast, the RB is focused on surveys of inflation expectations that do little more than move up and down with historical inflation and have no bearing on medium-term inflation outcomes.

The excessive focus by the RB on surveys of inflation expectations in assessing medium-term inflation prospects has strong parallels with the RB's excessive focus over the last year on the fall in dairy farm incomes on GDP and employment growth prospects. Equally, the lack of focus on the worsening labour shortage problem in assessing medium-term inflation prospects has strong parallels with the insufficient weight the RB and bank economists paid to the stimulus to economic growth last year from super-low interest rates and super-charged net migration. Unfortunately, history is set to repeat itself.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

9 Comments

Forecasting is a guess. Call it educated if you want, but it is still a finger in the air guess.

Unfortunately, official actions undertaken by government agencies in response to "forecasts" entail real financial repression for those that have seen their wealth transferred to others without recourse to collective punitive redress.

The problem we have here is that RBNZ has fallen into the same mentality as other government departments. They are immune to input or feedback which means the decisions they make have no likelihood of improving in quality. The forecasting being continuously wrong and detached from reality is compounding the problem, but it is all related to having no mechanism for feedback from people or the economy.

RBNZ does not have the required competence to manage our money supply (especially with their decreased influence). Reform is needed.

Is that then a failing on our forecasters or a failing of our government agencies relying to heavily on mystics?

As i have said before

economic forecasters only exist to make fortune tellers look good

The forecasts are failing because DSGE economic models fail to properly consider the role of credit growth in contributing to GDP (financing through money creation (FMC)).

If there were no easy credit being pumped into the system (private debt still growing at 9%!), then the forecasts might have been more correct.

DSGE models failed to predict the GFC because they assumed that banks only provide intermediation of savers with lenders, and omit to consider that purchasing power is created through lending.

Exactly,

Central bankers can make things worse when they fail to balance elasticity with discipline. Over the decades, Fed policy makers forgot that balance and became preoccupied with eliminating constraints to liquidity, Mehrling says.

Why? Influenced by academic theories about efficient markets and equilibriums, the Fed became willfully blind to asset bubbles and predisposed to pump easy money into the economy to keep it ticking over. For evidence, look no further than the Fed’s current determination to sustain unprecedented stimulus until the recovery strengthens. Read more and more

Well said peri. There is little recognition of the reliance of credit growth to keep GDP growth elevated. Anyone with this understanding will know of the extent of GDP underperformance were credit growth to slow considerably. Unfortunately it has been NZs economic policy for decades and each respective government continues to get away with it.

I look forward to Mister Dickens new, regular column. I imagine it will contain accurate forecasts in the political, economic spheres. And possibly a good selection of winners for the races.

I suggest monthly at first, until you've built your reputation, then ease off to quarterly.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.