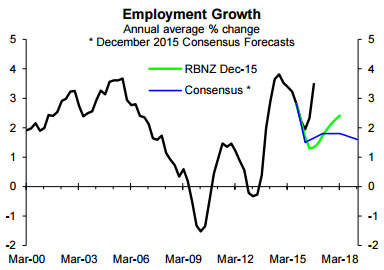

Employment growth has turned out to be dramatically stronger than predicted by my old employer, the Reserve Bank and the economic forecasters more generally; and the same will happen with labour cost inflation.

While Governor Wheeler is turning a blind eye to the overheated labour market it is central to prospects on a wide range of fronts, including the housing market, retail spending, residential building, the exchange rate and interest rates.

This Raving provides some insights into labour market prospects and more so into why they are central to prospects on a wide range of fronts.

We are at a stage in the economic cycle where the future will turn out even more different to what the economic forecasters are predicting than normal. This makes it a critical time for business owners, business managers and investors to have quality insights into prospects for the likes of the labour market and economy more generally.

Don't expect the economic forecasters to warn you about the myriad of implications of the booming labour market because they have no idea of what is going on

If you have any doubt about this, contrast what Governor Wheeler had to say about the labour market at the time of the last OCR decision on 22 September with the insights from the coalface.

This link is to the brief commentary by the governor that accompanied the OCR decision on 22 September. In assessing inflation prospects and the appropriate level of the OCR the labour market didn't warrant a single mention. This contrasts dramatically with the insights from a wide range of sources that suggest the labour market is becoming a major threat because it is extremely overheated as suggested by the strong employment growth.

By contrast, the NZIER September survey of businesses found that "A net 27 percent of firms are looking to increase headcount in the next quarter – the highest level for 43 years." Tony Alexander's August survey of businesses found that "Staff shortages are evident across a wide range of sectors." The Auckland Chamber of Commerce August survey - second link below - found that "Over 48% of Auckland businesses responding to the survey have confirmed they are having difficulty finding the talent they need."

The evidence from the coalface suggests the labour market should be the top of the Reserve Bank's focus in assessing the medium-term inflation outlook and the appropriate level of the OCR rather than not even rating a mention.

The economic forecasters' current predictions that labour cost inflation will remain low will prove to be equally inaccurate as their predictions of only moderate employment growth late last year. They show no signs of having learnt from the mistakes of their previous labour market forecasts but instead perpetuate the myth that the labour market isn't a major threat to inflation.

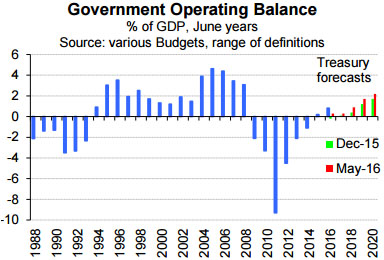

Why is the labour market so important? In a modern economy labour costs are by far the largest cost of production for the average firm, making them of most importance to inflation and interest rate prospects. The income of employees is by far the largest component of income in the economy, making the labour market of major importance to prospects for consumer spending growth; another area where the economic forecasters have been too pessimistic. A stronger labour market and related stronger growth in retail sales are boosting the government's finances and helping lay the foundations for a significant fiscal stimulus to economic growth next year; being an election year with what looks like being a closely fought election (i.e. the political case for fiscal stimulus will be extremely strong).

This is just the start of the strong economy fuelling the fiscal surplus that will allow the government to increase spending and possibly cut taxes in an attempt to win what is looking like being a closely fought election next year. This adds to why the Reserve Bank and economic forecasters more generally have no idea about what will transpire in the labour market and economy, which has major implications for borrowers, exporters, importers, investors, retailers, building firms and a wide range of other firms including business service firms (e.g. lawyers, accountants and consultants). It will be important to importers and exporters because the outlook for the exchange rate is very different to what the Reserve Bank and many of the economic forecasters are predicting.

If the Reserve Bank and economic forecasters more generally can't get close to predicting what is going on in the labour market they have no hope of predicting the outlook for interest rates and the exchange rate or for that matter house prices, retail spending and residential building.

Looking ahead, another area the economic forecasters are off the track is prospects for residential building, an area where the political sands are moving quickly. This is important because of the high correlation between growth in residential building and GDP growth, which means prospects for residential building have significant implications for the labour market, interest rates and even the exchange rate.

If you are serious about making profitable business and/or investment decisions you need the best analysis of economic prospects available (i.e. the analysis contained in our sharply-priced reports). I have been a lone voice in warning that economic and employment growth prospects were much stronger than predicted by the Reserve Bank and economic forecasters, including correctly advising that they were putting way too much weight on the negative impact of the fall in dairy farm incomes. It wasn't by chance that I was able to do this. It was because I undertake quality analysis of the key drivers of the economy. This contrasts greatly with the wishful thinking and preconceptions that play much too large a part in shaping the forecasts by my old employer, the Reserve Bank, while the bank economists are much more focused on getting on the 6 o'clock news than undertaking the quality analysis required to produce reliable insights into the outlook for the economy.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

3 Comments

Don't expect the economic forecasters to warn you about the myriad of implications of the booming labour market because they have no idea of what is going on

But the Fed's failures are even more basic than all that. The guiding doctrine of monetary policy is actually quite easy to understand in its operational intentions; to use a target for the federal funds rate in order to achieve a stable 2% rate of inflation. It is assumed by that method of "monetary" control to that level of economic success (inflation being the economic barometer of money) unemployment will settle easily so as to satisfy their third mandate. Read more

So it seems there is upwards pressure on wages. What a good thing. After all, increased incomes for New Zealanders is the only reasonable goal of this economic management obsession we have isn't it.

Even on an aggregate basis (which is increasingly a poor way to assess income as there are two New Zealands now) I have yet to see these pressures pushing significant or sustainable income growth. I’d love to say otherwise but I don’t yet see an economy with productivity and wages rising at any meaningful rate. It seems however many people are hoping (early days) for a modest improvement in our economy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.